Free equity analysis

Complete guide to understanding your ServiceNow equity compensation, including RSU, ISO, NSO, ESPP, vesting schedules, and tax strategies.

Employees

17.6K

Worldwide

Equity Programs

4

programs

Vesting Period

4 years

RSU vesting

ServiceNow offers 4 equity compensation programs to employees. Click on each program to learn more about eligibility, vesting, and tax implications.

Standard RSU program with 4-year vesting and 1-year cliff. Annual refresh grants available for eligible employees.

Learn about ServiceNow's Incentive Stock Options program, including vesting schedules and tax treatment.

Learn about ServiceNow's Non-Qualified Stock Options program, including vesting schedules and tax treatment.

Learn about ServiceNow's Employee Stock Purchase Plan program, including vesting schedules and tax treatment.

ServiceNow offers a comprehensive equity compensation package designed to align employee interests with the company's long-term success. As a publicly traded technology company (ticker: NOW), ServiceNow provides multiple equity vehicles including Restricted Stock Units (RSUs), stock options (both ISOs and NSOs), Performance Stock Units (PSUs), Restricted Stock Awards (RSAs), and an Employee Stock Purchase Plan (ESPP).

Equity compensation represents a significant portion of total compensation at ServiceNow, particularly for technical and senior roles. As your equity vests, you gain actual ownership in a leading enterprise software company, allowing you to benefit directly from ServiceNow's growth and stock price appreciation. This ownership stake can become a substantial wealth-building component of your overall compensation package.

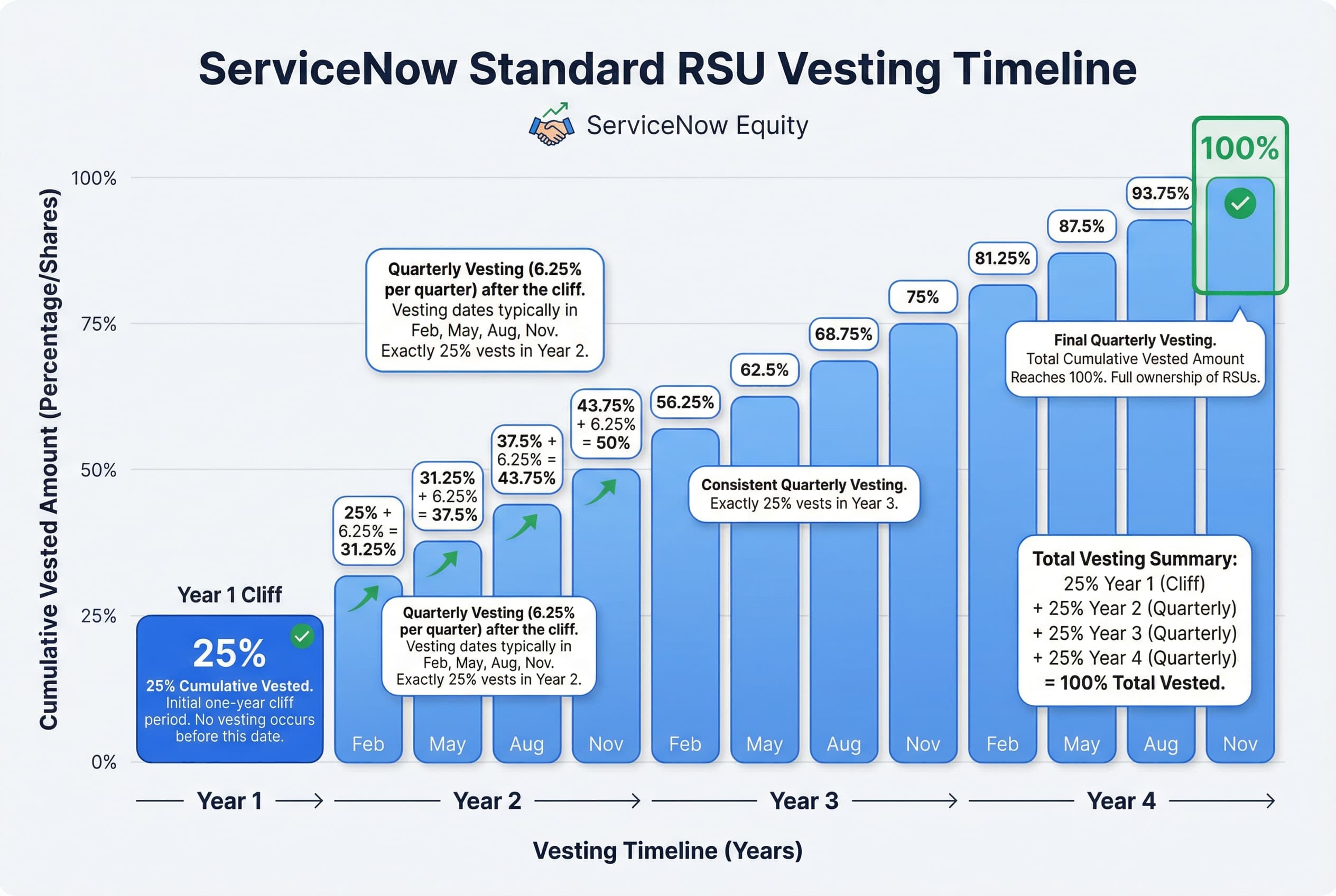

RSUs at ServiceNow typically follow a four-year vesting schedule with a one-year cliff, meaning 25% of your grant vests on your first anniversary. The remaining shares vest either quarterly or biannually depending on your grant size, with vesting dates typically occurring in February, May, August, and November. Annual performance-based refresher grants are common, helping to maintain your equity compensation over time, though specific refresher amounts are generally not disclosed during the hiring process.

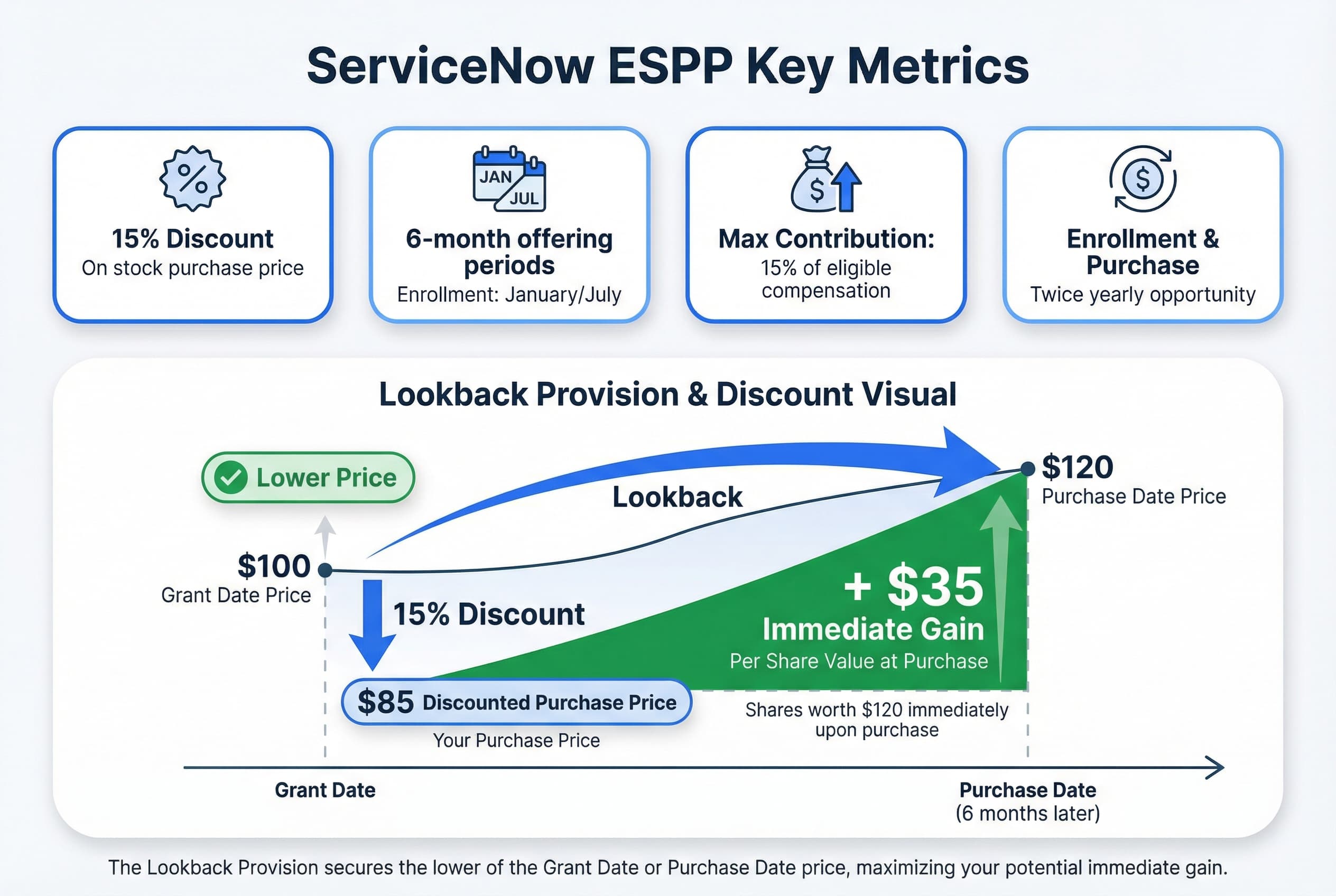

The company also offers an ESPP with a 15% discount and lookback provision, allowing you to purchase ServiceNow stock at favorable prices through payroll deductions of up to 15% of your salary, with enrollment periods in January and July.

ServiceNow uses a four-year vesting schedule with a one-year cliff for Restricted Stock Units (RSUs). This means you won't receive any shares during your first year of employment. On your one-year anniversary, 25% of your total grant vests all at once. The remaining 75% then vests over the following three years.

The vesting frequency for the remaining shares after your cliff depends on your grant size. Larger grants typically vest quarterly, while some grants may vest biannually. For quarterly vesting, shares are distributed in February, May, August, and November each year.

This structure results in uniform annual vesting - you'll receive 25% of your total grant each year over the four-year period, but the actual share delivery happens more frequently than once per year for most employees.

During the 12-month cliff period, you're earning equity but not yet receiving it. If you leave ServiceNow before completing one full year of service, you forfeit your entire grant. However, once you pass the one-year mark, you immediately receive that first 25% of shares. This cliff protects the company's investment in new hires while ensuring employees who stay receive meaningful equity compensation.

ServiceNow provides annual performance-based refresher grants to retain and reward continuing employees. However, there's some ambiguity around when these refreshers begin vesting. Some information suggests they start vesting from the second year, while other sources indicate they may vest immediately or after a one-year period. Unfortunately, recruiters typically don't share expected refresher amounts during the hiring process, so you'll need to discuss this with your manager during performance reviews.

ServiceNow's vesting schedule is uniform rather than backloaded or frontloaded - you receive exactly 25% of your grant value each year. This predictable structure makes it easier to plan your financial future and understand the value of your equity compensation over time.

ServiceNow offers a valuable ESPP that allows employees to purchase company stock at a significant discount. The program provides a 15% discount on the stock price and includes a lookback provision, creating an attractive opportunity for employees to build wealth through company ownership.

The ESPP operates on 6-month offering periods with enrollment windows in January and July. During each period, you can contribute up to 15% of your eligible compensation through payroll deductions. At the end of each 6-month purchase period, your accumulated contributions are used to buy ServiceNow stock.

The lookback provision is particularly valuable: your purchase price is based on whichever is lower - the stock price at the beginning of the offering period or the price at the end of the purchase period. You then receive an additional 15% discount on that lower price.

The combination of the lookback provision and 15% discount can generate substantial returns. If ServiceNow's stock price increases during the offering period, you benefit from both purchasing at the earlier, lower price and receiving the 15% discount on top of that. In a rising market, this can result in immediate gains of 15% or more when you purchase shares.

Understanding the difference between qualifying and disqualifying dispositions is important for tax planning. A qualifying disposition requires holding shares for at least 2 years from the offering date and 1 year from the purchase date, which can provide more favorable tax treatment. A disqualifying disposition occurs when you sell before meeting these requirements, resulting in different tax consequences on your gains.

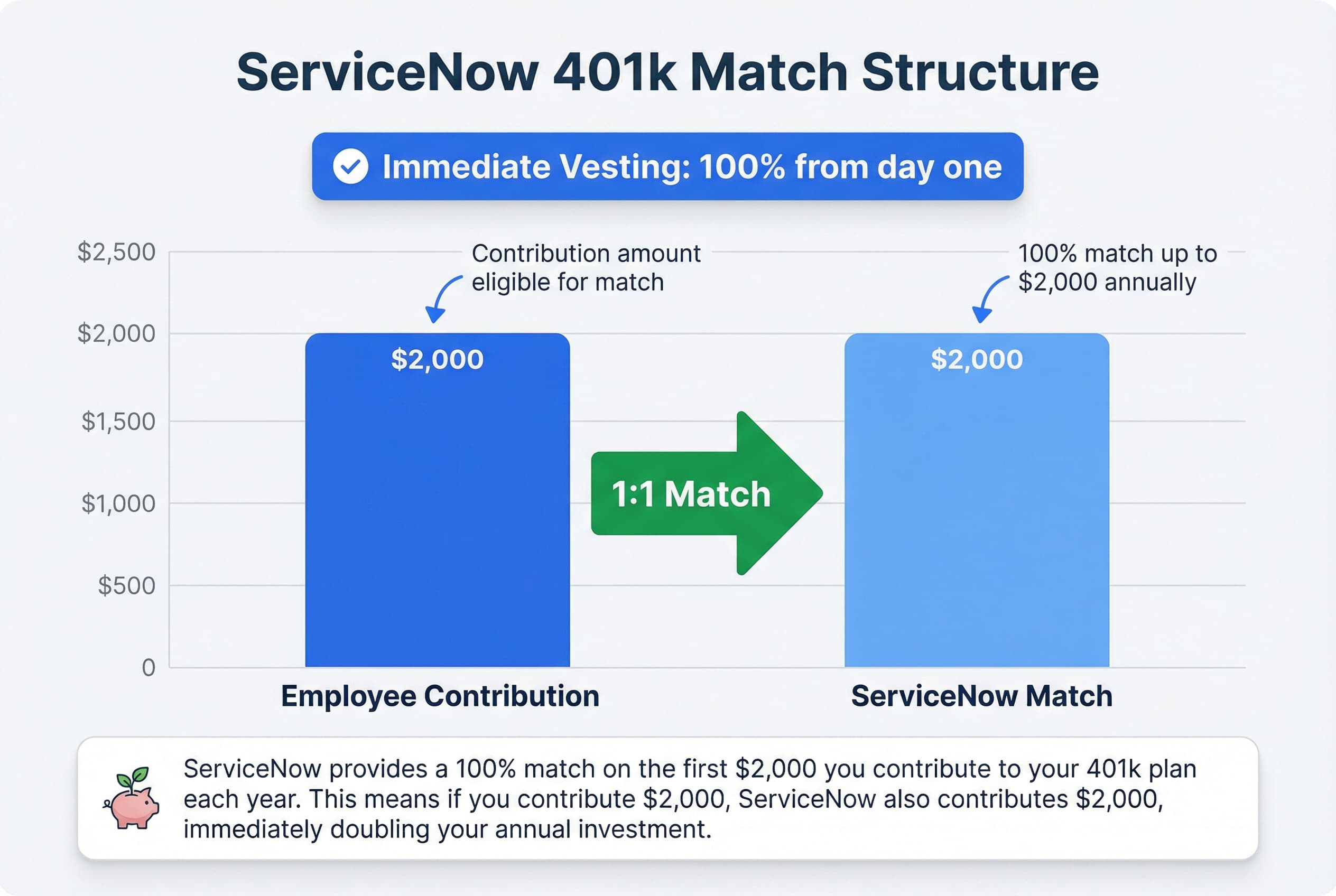

ServiceNow offers a competitive 401(k) retirement savings plan with immediate company matching. The company provides a 100% match on contributions up to $2,000 annually. This means ServiceNow will match your contributions dollar-for-dollar until you've received the full $2,000 match.

One of the standout features of ServiceNow's 401(k) is immediate vesting of employer match contributions. Unlike many companies that require you to stay for several years before you fully own the company match, at ServiceNow you own 100% of the match from day one. This is a significant benefit if you're considering career mobility.

ServiceNow's 401(k) plan includes several advanced features for tax-optimized retirement savings:

These features make ServiceNow's 401(k) particularly attractive for employees looking to maximize their retirement savings and implement sophisticated tax strategies. The mega backdoor Roth option is especially valuable for those who exceed traditional Roth IRA income limits or want to save more than standard 401(k) contribution caps allow.

Understanding the tax treatment of your ServiceNow equity compensation is crucial for effective financial planning. Different equity types trigger taxes at different times and rates.

RSUs: You owe taxes when your RSUs vest, not when you sell the shares. At each vesting event (February, May, August, and November for ServiceNow), the fair market value of the vested shares becomes taxable as ordinary income, just like your salary. You'll owe taxes regardless of whether you hold or sell the shares.

Stock Options (ISOs and NSOs): NSOs trigger ordinary income tax when you exercise them, based on the difference between the exercise price and the current market value. ISOs receive preferential treatment - no regular tax at exercise, but you may face Alternative Minimum Tax (AMT). For ISOs, regular taxes apply only when you sell the shares.

ESPP: Taxes depend on how long you hold the shares. To qualify for favorable tax treatment, you must hold shares for at least two years from the offering date and one year from the purchase date. Otherwise, the discount is taxed as ordinary income.

When RSUs vest, ServiceNow typically withholds shares to cover taxes. However, the default withholding rate often falls short of your actual tax obligation, especially for high earners. This creates a "gap" that you'll need to cover when filing your tax return. You can adjust your withholding settings to sell additional shares at vest to better cover your total tax liability.

The value of RSUs at vest is taxed as ordinary income at your marginal tax rate. Any subsequent gain (or loss) from the time of vest to when you sell is taxed as a capital gain - long-term if you hold for more than one year after vest, short-term if less.

ServiceNow is headquartered in California, a high-tax state. If you work remotely in another state, consult a tax professional about multi-state tax implications.

Disclaimer: This information is educational only and not tax advice. Tax situations vary significantly based on individual circumstances. Please consult a qualified tax professional for guidance specific to your situation.

As a ServiceNow employee, your equity compensation can become a significant portion of your wealth - but concentrating too much in a single stock creates substantial risk, regardless of how promising the company appears.

When your financial future depends heavily on one company, you're exposed to both your employment income and investment returns from the same source. If ServiceNow faces challenges, you could simultaneously experience job insecurity and declining portfolio value - a double impact that diversified investors avoid.

ServiceNow operates in the competitive technology sector, where companies face unique vulnerabilities: rapid innovation cycles, changing customer preferences, emerging competitors, regulatory scrutiny, and market volatility. Even well-established tech companies can experience significant stock price swings based on quarterly earnings, product cycles, or broader market sentiment toward the sector.

Financial advisors typically recommend limiting single-stock exposure to 10-20% of your total net worth, including retirement accounts. This doesn't mean selling all your ServiceNow equity immediately - especially given tax implications - but rather developing a systematic plan to diversify over time.

Consider selling vested RSUs on a regular schedule and reinvesting proceeds into diversified index funds or other asset classes. Take advantage of your 401(k) with its company match, and use the ESPP strategically - perhaps selling shares shortly after purchase to capture the 15% discount while minimizing concentration risk.

As your ServiceNow RSUs vest quarterly (typically in February, May, August, and November), you'll face regular decisions about whether to hold or sell. Consider selling vested shares when ServiceNow represents more than 10-15% of your total investment portfolio, as concentration risk increases significantly beyond this threshold. Additionally, evaluate selling if you need funds for major life goals like home purchases or debt reduction.

Given ServiceNow's position in the technology sector, holding substantial company stock creates both company-specific and sector-specific concentration risk. If your career, income, and investments are all tied to one technology company, consider diversifying into other asset classes and sectors. The quarterly vesting schedule provides natural opportunities to rebalance your portfolio without making large, one-time decisions.

ServiceNow's ESPP offers a 15% discount with lookback pricing, creating immediate value. For maximum tax efficiency, consider holding ESPP shares for the qualifying period (2 years from offering date, 1 year from purchase date) to achieve long-term capital gains treatment on the discount. However, weigh this tax benefit against concentration risk - immediate sale may be prudent if ServiceNow already represents a large portion of your portfolio.

Maximize your 401(k) contributions to the $2,000 match threshold, and consider utilizing the Mega Backdoor Roth option for additional tax-advantaged savings.

ServiceNow makes 10b5-1 plans available and requires preclearance for equity transactions. These plans allow you to establish predetermined selling schedules during open trading windows, providing automatic diversification even during blackout periods. This is particularly valuable given ServiceNow's pre-earnings blackout windows, ensuring you can execute your diversification strategy consistently regardless of trading restrictions.

This information is educational and not personalized financial advice. Consult a qualified financial advisor for guidance specific to your situation.

Let's walk through a realistic scenario to see how equity vesting works at ServiceNow.

Sarah joins ServiceNow as a Software Engineer and receives 100 RSUs as part of her initial equity package. At her start date, ServiceNow stock is trading at $800 per share, making her total grant worth $80,000 over four years.

ServiceNow uses a four-year vesting schedule with a one-year cliff:

Year 1 (12-month anniversary): 25 RSUs vest (25% of grant)

Years 2-4: The remaining 75 RSUs vest quarterly

When RSUs vest, they're treated as ordinary income. While ServiceNow's specific withholding rate isn't provided in the data, let's assume a typical supplemental wage rate applies. The company will withhold shares to cover taxes.

For example, at Sarah's first vesting event:

Over four years, assuming the stock price remains at $800:

Sarah can hold these shares for potential appreciation or sell them immediately - the choice is hers after vesting.

Even experienced employees can stumble when managing their ServiceNow equity. Here are the most frequent missteps to avoid:

ServiceNow RSUs vest on a four-year schedule with a 12-month cliff, meaning you receive nothing if you leave before your one-year anniversary. Many employees underestimate this timing risk, especially when considering competing offers in their first year.

When your RSUs vest, ServiceNow withholds taxes, but this may not cover your full tax liability - especially if you're in a high-income bracket or live in a state with additional taxes. Without proper planning for estimated quarterly tax payments, you could face an unexpected bill at tax time.

As your equity vests over time, it's easy to accumulate a portfolio heavily weighted toward ServiceNow stock. This concentration creates significant risk - your income and wealth both depend on the company's performance. Consider diversifying as shares vest to protect your financial future.

ServiceNow's ESPP offers a 15% discount with lookback pricing, providing immediate gains on purchase. Many employees either don't enroll or undercontribute, missing out on this essentially guaranteed return during the six-month offering periods in January and July.

If you hold stock options, remember you typically have only 90 days post-termination to exercise. Waiting until you leave without understanding the tax implications and cash requirements can force difficult decisions under time pressure.

Understanding what happens to your equity compensation when you leave ServiceNow is crucial for making informed career decisions.

Unvested RSUs are forfeited upon termination. Since ServiceNow RSUs follow a four-year vesting schedule with a one-year cliff and quarterly or biannual vesting thereafter, any shares that haven't vested by your termination date will be lost. This applies regardless of whether you leave voluntarily or involuntarily.

Your termination date is critical. ServiceNow RSUs typically vest in February, May, August, and November. If you leave just before a vesting date, you'll miss that vesting event entirely. For example, leaving in late January means forfeiting shares that would have vested in February.

If you hold stock options at ServiceNow, you have a 90-day window after termination to exercise any vested options. This is a relatively standard timeframe, but it requires quick decision-making. After 90 days, unexercised vested options will expire. Remember that unvested options are also forfeited upon departure.

For the Employee Stock Purchase Plan, if you leave during an offering period (which runs for six months with enrollment in January and July), your participation typically ends. You'll generally receive a refund of accumulated payroll deductions, and you won't participate in that period's purchase.

Key takeaway: Plan your departure timing carefully, especially around vesting dates, to maximize the equity you've earned.

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

ServiceNow RSUs follow a four-year vesting schedule with a one-year cliff, meaning 25% of your grant vests on your first anniversary. After the cliff, the remaining 75% vests either quarterly or biannually depending on your grant size. Vesting typically occurs in February, May, August, and November.

If you leave ServiceNow, you have 90 days to exercise any vested stock options. After this 90-day post-termination window, you'll lose the right to exercise those options. Your options expire 10 years from the original grant date if not exercised earlier.

Yes, ServiceNow offers an ESPP with a 15% discount and lookback pricing. The plan has 6-month offering and purchase periods, with enrollment windows in January and July. You can contribute up to 15% of your eligible compensation to purchase stock at a discount.

When your RSUs vest, they're taxed as ordinary income based on the fair market value on the vesting date. ServiceNow allows you to adjust your tax withholding rate to ensure you have adequate withholding or to manage your cash flow preferences.

ServiceNow typically provides annual performance-based refresher grants. However, recruiters often don't share expected refresher amounts upfront, and there's some variability in when refreshers begin vesting. Refreshers are part of ServiceNow's ongoing retention and performance compensation strategy.

To receive favorable tax treatment (qualifying disposition) on ESPP shares, you must hold them for at least 2 years from the offering date and 1 year from the purchase date. Selling before these periods results in a disqualifying disposition with different tax consequences.

Yes, you must comply with ServiceNow's Insider Trading Policy and may be subject to blackout periods, particularly before earnings announcements. Preclearance is required for certain stock transactions, and ServiceNow offers 10b5-1 trading plans that allow you to set up predetermined trading schedules.

ServiceNow offers a 401(k) match of 100% up to $2,000 of your contributions, with immediate vesting. The plan also includes valuable features like Mega Backdoor Roth conversions and Roth 401(k) options for additional tax planning flexibility.

Get a free personalized analysis from our equity compensation experts