What Are Stock Options? A Simple Guide for Employees

Understanding your right to buy company shares at a discount

Published March 14, 2026 · Updated March 14, 2026

Stock options give you the right to buy your company's shares at a fixed price, potentially letting you profit if the stock price goes up. This guide explains how they work, when you can use them, and what they could be worth to you in real dollars.

The Stock Option Promise: Your Ticket to Future Gains

Sarah just got a job offer. The salary is $100,000, plus something called "1,000 stock options at a $50 strike price." She has no idea what that means.

Here's what it actually means: Sarah gets the right to buy 1,000 shares of her company's stock for $50 each, no matter what happens to the stock price later.

Think of stock options like a coupon that locks in today's price forever. Imagine you have a coupon to buy a concert ticket for $50. The concert gets more popular, and tickets now cost $150. But your coupon still says $50. You can buy the ticket for $50 and immediately resell it for $150, pocketing $100 in profit. Stock options work exactly the same way.

Fast forward three years. Sarah's company is doing great. The stock price climbs to $150 per share. Now Sarah can use her options:

- She buys 1,000 shares at her locked-in price: 1,000 × $50 = $50,000

- Those shares are worth: 1,000 × $150 = $150,000

- Her profit before taxes: $150,000 - $50,000 = $100,000

That's the promise of stock options. You profit when your company's stock price goes up.

Why do companies offer stock options? Two reasons. First, they want to attract talented people like you without paying higher salaries upfront. Second, they want you to care about the company's success. When the stock price goes up, you win. When it goes down, your options might be worthless.

Stock options aren't the same as getting actual shares (like RSUs, which we'll compare later). You have to buy your shares first. But if the company does well, the potential gains can be huge.

Now let's break down the two types of stock options you might receive.

What are stock options, and how do they work?

The Two Types of Employee Stock Options: ISOs and NSOs

Stock options come in two flavors: Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs). Think of them like regular tickets versus VIP tickets to a concert. VIP tickets (ISOs) give you better perks, but you have to follow strict rules to keep those benefits.

Here's what makes them different:

ISOs are only for employees. They offer potential tax advantages, meaning you might pay less to the IRS when you sell. But there's a catch: you must follow specific rules about how long you hold the shares and when you exercise. Break the rules, and your ISOs turn into NSOs.

NSOs are for everyone: employees, contractors, and board members. They're simpler to understand but get taxed more heavily. The IRS treats your gains as regular income, just like your salary.

Most employees at public companies get NSOs. Your grant paperwork will tell you which type you have. Look for the words "Incentive Stock Option" or "Non-Qualified Stock Option" in your documents.

Why the type matters: taxes. Let's say you make a $100,000 gain on your options. If you have ISOs and follow all the rules, you might pay around $20,000 in taxes (20% long-term capital gains rate). With NSOs, you'd pay roughly $37,000 (37% ordinary income rate). That's a $17,000 difference on the same gain.

The catch? ISOs come with complex rules and a potential tax trap called the Alternative Minimum Tax (we'll cover that later). NSOs are straightforward: exercise them, pay taxes, done.

Now that you know your option type, let's talk about the two numbers that determine how much money you actually make: your strike price and the spread.

ISOs vs NSOs Explained | Best Stock Options for Employees

Strike Price and Spread: The Numbers That Determine Your Profit

Your strike price is the price tag that never changes. When your company grants you stock options, they lock in the price you'll pay to buy shares. This number stays the same whether the stock soars to $500 or crashes to $5.

Think of it like getting a coupon for gas that locks in $2.50 per gallon forever. If gas goes to $4.00, you save $1.50 per gallon. If gas drops to $2.00, your coupon is worthless. You'd just pay the regular price instead.

How strike price is set: Your company sets it at the current stock price on your grant date. Get options on a day when the stock is $80? Your strike price is $80.

The spread is your profit zone. It's the gap between your strike price and the current stock price. This number tells you how much you'd make per share if you exercised today.

Here's the simple formula:

(Current Stock Price - Strike Price) × Number of Options = Gross Profit

Let's see this in action. You have 500 options with an $80 strike price.

Scenario 1: Stock at $120 (in the money)

- Spread: $120 - $80 = $40 per share

- Gross profit: $40 × 500 = $20,000

Scenario 2: Stock at $60 (underwater)

- Spread: $60 - $80 = negative $20

- Gross profit: $0 (you wouldn't exercise)

Scenario 3: Stock at $80 (at the money)

- Spread: $80 - $80 = $0

- Gross profit: $0 (break even)

When your options are underwater (stock below strike price), they have no value right now. But they could become valuable later if the stock price rises. This is why options can feel like a waiting game.

Now that you know your potential gross profit, let's talk about when you actually get to use these options.

The spread is the difference between the current stock price and your fixed strike price - this is your potential profit per share.

The spread is the difference between the current stock price and your fixed strike price - this is your potential profit per share.

Vesting: When You Actually Get to Use Your Options

Getting stock options is like receiving a piggy bank that unlocks gradually. You don't get access to all your options on day one. You earn them over time by staying at the company.

What vesting actually means: Vesting is the process of earning the right to exercise your options. Think of it as a loyalty rewards program. The longer you stay, the more options become yours to use.

The Standard Vesting Schedule

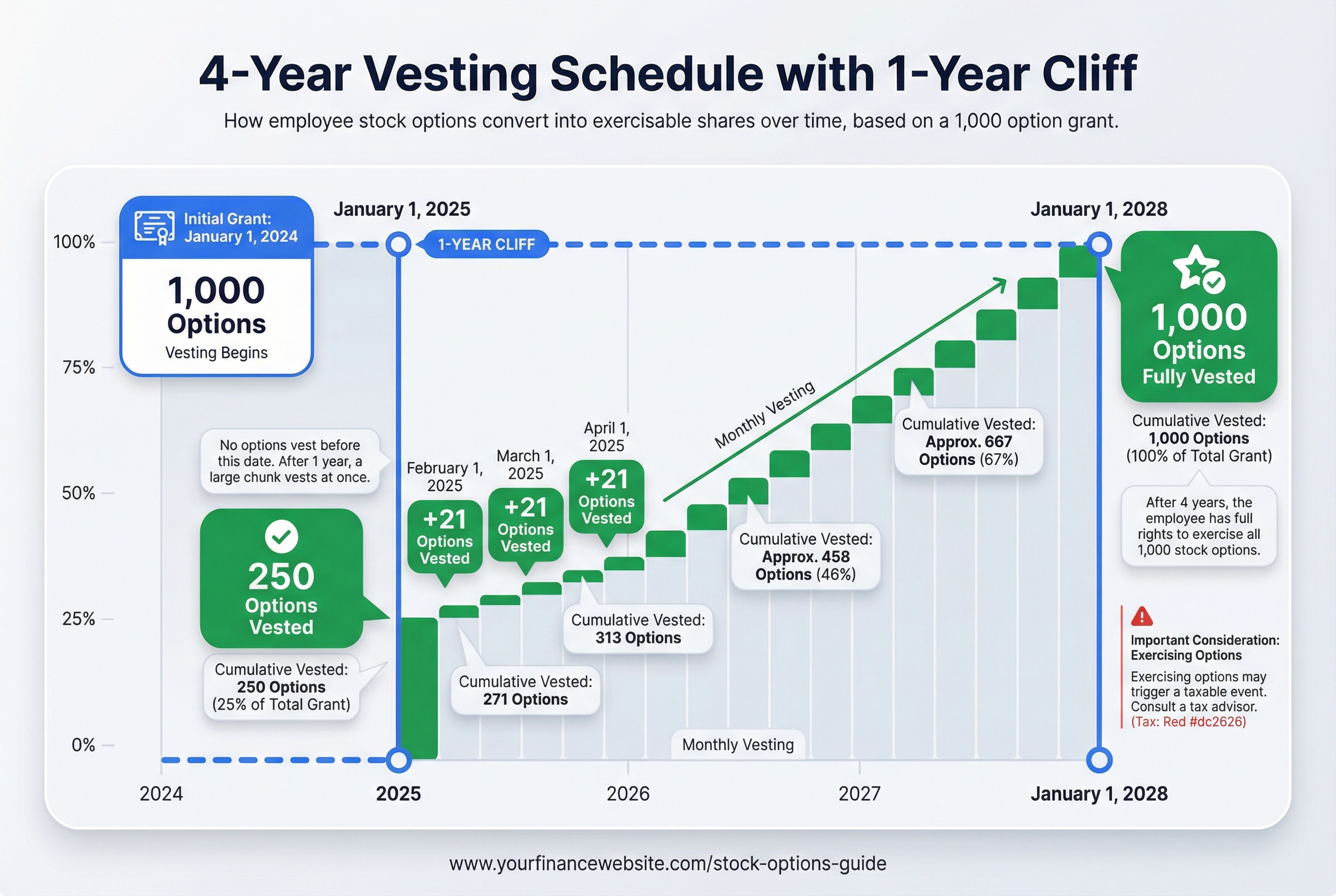

Most companies use a 4-year vesting schedule with a 1-year cliff. Here's what that means in plain English:

The cliff: You get nothing for your first year. Then on your one-year anniversary, 25% of your options vest all at once.

Monthly vesting: After the cliff, you earn a small chunk of options every month for the next three years.

Here's a real example. You receive 1,000 stock options on January 1, 2024:

- January 1, 2025 (one year later): 250 options vest

- February 1, 2025: 21 more options vest

- March 1, 2025: Another 21 options vest

- April 1, 2025: Another 21 options vest

This pattern continues every month. By January 1, 2028, all 1,000 options are fully vested and yours to exercise.

Why Companies Use Vesting

Vesting is a retention tool. Companies want you to stick around. If you leave before options vest, you lose them. It's their way of saying "we value your long-term commitment."

Key point: You can only exercise vested options. Unvested options are still owned by the company. If you quit or get fired, unvested options typically disappear.

Track Your Vesting Status

Check your equity compensation portal regularly. It shows exactly how many options you've vested and when the next batch unlocks. Most portals (like E*TRADE, Fidelity, or Schwab) display a vesting timeline with specific dates and quantities.

Now that you know when you can use your options, let's talk about how you actually turn them into shares.

Vesting schedules typically feature a 1-year cliff, after which options vest monthly over the remaining three years.

Vesting schedules typically feature a 1-year cliff, after which options vest monthly over the remaining three years.

How to Exercise Your Stock Options: Three Methods Explained

When you exercise stock options, you're buying shares from your company at your strike price. But you don't need to pull cash out of your savings account to do it. You have three ways to make this happen.

Let's use a real example for all three methods. You have 500 options with a $50 strike price. The stock is trading at $100 today.

Method 1: Cash Exercise (Buy and Hold)

You pay the strike price in cash and keep all the shares. This is like buying a house with cash instead of getting a mortgage.

Here's the math: You pay $25,000 ($50 x 500 shares). You now own 500 shares worth $50,000. You spent $25,000 to get $50,000 in stock.

The catch: You need $25,000 upfront, plus cash to cover taxes. But you keep all 500 shares, which could grow in value.

Method 2: Cashless Exercise, Sell-to-Cover

Your broker sells just enough shares to cover the exercise cost. Think of this like flipping a house immediately to recoup your down payment.

Here's the math: Your broker sells 250 shares for $25,000 to cover the strike price cost. You keep 250 shares worth $25,000. You paid $0 upfront and now own 250 shares.

The catch: You give up half your shares to cover costs. You still owe taxes on the full $25,000 gain.

Method 3: Cashless Exercise, Sell All

You exercise and immediately sell all shares. You get cash instead of stock.

Here's the math: You exercise 500 shares and sell them all for $50,000. After paying the $25,000 strike price, you get $25,000 in cash (minus taxes and broker fees). You paid $0 upfront and have no shares left.

The catch: You miss out if the stock keeps rising. But you get immediate cash with no money down.

Who Handles This?

Your company's stock plan administrator (like E*TRADE, Fidelity, or Schwab) manages the whole transaction. You just pick your method and click a few buttons on their website.

Each method has different tax consequences, which we'll tackle next.

Stock Options and Taxes: What You'll Actually Pay

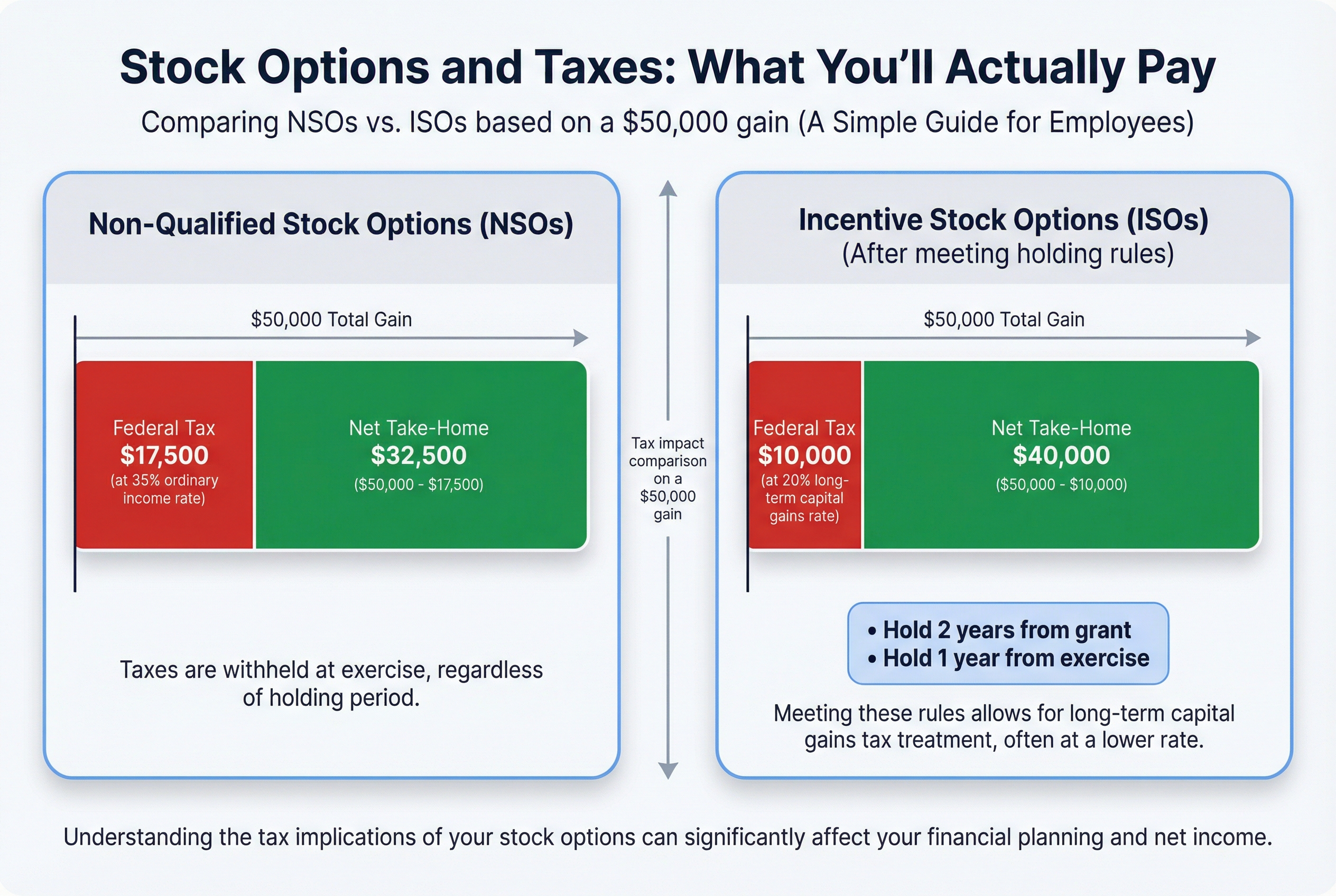

Here's the key difference: NSOs are taxed when you exercise, ISOs are taxed when you sell (if you follow the rules). Think of it like "pay now vs. pay later."

NSOs: Taxed Like a Bonus

When you exercise NSOs, the IRS treats your profit as ordinary income. It's taxed just like your salary.

Your company automatically withholds taxes, similar to your paycheck. You don't need to do anything extra.

Example: You exercise 500 NSO options. The spread is $100 per share. That's a $50,000 gain.

At a 35% federal ordinary income rate, you owe about $17,500 in taxes. Your company withholds this amount when you exercise.

ISOs: Potentially Lower Taxes (With Patience)

ISOs can qualify for long-term capital gains rates, which are lower than ordinary income rates. But you have to follow strict holding rules:

- Hold shares for 2 years from the grant date

- Hold shares for 1 year from the exercise date

Meet both requirements, and your profit gets taxed when you sell at capital gains rates instead of ordinary income rates.

Example: Same 500 options, same $100 spread, same $50,000 gain. You followed the ISO holding rules.

At a 20% long-term capital gains rate, you owe about $10,000 in federal taxes when you sell. That's $7,500 less than the NSO example.

Important: Your company doesn't withhold taxes for ISOs. You pay when you file your tax return.

Quick Decision Tree

Do you have ISOs? Did you hold shares for 2 years from grant AND 1 year from exercise? If yes to both, you might qualify for the lower capital gains rate. If you didn't meet the holding periods, your ISO profit gets taxed as ordinary income, just like NSOs.

These examples use simplified federal rates. Your actual tax bill depends on your total income and tax bracket.

But there's a catch with ISOs that can surprise you: the Alternative Minimum Tax. Let's tackle that next.

Should I exercise my ISO stock options? Tax effects to know!

NSOs are taxed immediately upon exercise as ordinary income, while ISOs offer potential tax advantages if holding requirements are met.

NSOs are taxed immediately upon exercise as ordinary income, while ISOs offer potential tax advantages if holding requirements are met.

The AMT Trap: What ISO Holders Need to Know

Here's the biggest gotcha with ISOs: something called the Alternative Minimum Tax, or AMT.

Think of AMT as a parallel tax system that runs alongside the regular one. The IRS calculates your taxes both ways and makes you pay whichever is higher. It's like getting two restaurant bills and having to pay the bigger one.

When AMT hits you hard

AMT gets triggered when you exercise ISOs but don't sell the shares in the same year. You pay tax on your paper gain, even though you haven't sold anything yet.

Here's a real example of how painful this can be:

You exercise 1,000 ISOs in June 2024. Your strike price is $50, and the current stock price is $150. That's a $100,000 spread ($150 minus $50, times 1,000 shares).

You hold the shares because you believe in the company. You don't sell.

April 2025 arrives. Your tax bill includes roughly $28,000 in AMT on that $100,000 spread. That's 26-28% of your paper gain.

The problem: You owe $28,000 in real cash, but you never sold your shares. You have no money from a sale to pay this tax bill.

This is why many people do same-day sales with ISOs, even though it means losing the tax benefits. They can't afford the AMT risk.

How to protect yourself

The simple rule: Don't exercise more ISOs than you can afford to pay AMT on.

Before you exercise, multiply your expected spread by 28%. That's roughly what you might owe in AMT. If you don't have that cash sitting in your bank account, think twice about exercising without selling.

You can get an AMT credit in future years that reduces other taxes. But you need cash now to pay the bill. Many employees have been crushed by AMT they didn't see coming.

Now let's look at what happens to your options when you leave your company.

When You Leave Your Company: What Happens to Your Options

Your stock options have an expiration date that suddenly speeds up the moment you leave your company. Think of it like a library book: you can renew it as long as you're a member, but once you cancel your membership, you have just days to return it or lose it forever.

Here's what actually happens when you resign, get laid off, or retire.

Your Unvested Options Disappear Immediately

The day you leave, any options that haven't vested yet vanish. Gone. You get nothing for them.

This is true whether you quit, get fired, or take a severance package. Unvested means unearned, and the company takes them back.

Your Vested Options: The 90-Day Countdown

For options that have vested, you typically get 90 days from your last day of work to exercise them. After 90 days, they expire worthless.

This is the standard rule at most companies. Some give you longer, but 90 days is what you should expect.

The clock starts ticking on your actual last day of employment, not when you give notice.

A Real Example: What You're Walking Away From

You have 1,000 stock options with a $50 strike price. The stock trades at $100 today. Of your options, 600 are vested and 400 are unvested.

You resign on March 1st. Here's what happens:

Immediately: Your 400 unvested options disappear. You just lost $20,000 in potential value (400 options × $50 spread).

By May 30th (90 days later): You must exercise your 600 vested options or they expire too. To exercise, you need $30,000 in cash (600 options × $50 strike price). If you can't come up with the money or don't want to take the risk, you lose another $30,000 in value.

What You Need to Exercise

Remember, exercising costs real money. You pay the strike price in cash upfront.

Your three options during the 90-day window:

- Pay cash to exercise and hold the shares

- Cashless exercise where you sell enough shares to cover the cost

- Let them expire if the stock price is below your strike price

Retirement Gets Different Treatment

If you retire (usually after age 55 or 60, depending on your company), you might get more time to exercise. Some companies give retirees up to 5 years.

Check your stock plan documents or ask HR. Retirement rules vary widely.

Don't Wait Until Day 89

The 90-day window sounds like plenty of time, but it goes fast. You need to:

- Decide whether to exercise

- Find the cash if you want to exercise and hold

- Coordinate with your broker or stock plan administrator

- Consider tax implications

Start planning before you give notice, not after.

Now that you understand what happens when you leave, let's figure out what you'll actually take home after taxes and fees eat into your gains.

Calculating Your Real Take-Home: After Taxes and Fees

Your stock options show a $40,000 gain on paper. Exciting, right? But here's the reality check: that $40,000 is like a gross paycheck. You don't take home the full amount.

Let's walk through exactly what you actually get after taxes and fees.

The Step-by-Step Math

Here's how to calculate your real take-home from exercising and selling NSOs:

Step 1: Calculate your gross profit

- Formula:

(current stock price - strike price) × number of options - This is your profit before anything gets taken out

Step 2: Subtract federal income tax

- NSO gains count as ordinary income

- You pay whatever your regular tax bracket is (typically 22% to 37%)

Step 3: Subtract FICA taxes

- Social Security and Medicare: 7.65% total

- This applies up to the Social Security wage base ($168,600 in 2024)

Step 4: Subtract brokerage fees

- Usually small: $25 to $100

- Covers the cost of executing the transaction

Real Example: The Full Picture

You have 500 NSOs with a $60 strike price. Your company's stock trades at $140. You exercise and sell immediately.

Gross profit: ($140 - $60) × 500 = $40,000

Now the deductions:

- Federal tax (35% bracket): -$14,000

- FICA (7.65%): -$3,060

- Brokerage fee: -$50

Net proceeds: $22,890

You take home 57% of your gross profit. The rest goes to taxes and fees.

Another Example: Smaller Grant, Same Pattern

You have 200 NSOs with a $25 strike price. Stock is at $85.

Gross profit: ($85 - $25) × 200 = $12,000

Deductions:

- Federal tax (24% bracket): -$2,880

- FICA (7.65%): -$918

- Brokerage fee: -$35

Net proceeds: $8,167

You keep 68% this time. Why more? Lower tax bracket means less taken out.

What to Expect

For most employees exercising NSOs, you'll take home 55% to 65% of your gross profit. Higher earners keep less (higher tax bracket). Lower earners keep more.

Your company will withhold some taxes automatically when you exercise. But you might owe more at tax time, especially if you're in a high bracket or live in a state with income tax.

Now that you know what you'll actually pocket, the big question becomes: when should you exercise? Let's look at how to make that decision.

Should You Exercise Now or Wait? A Decision Framework

Exercising options is like deciding when to use a gift card. You want to get good value, but there's no perfect moment. The gift card doesn't expire tomorrow, so you can wait for the right purchase. But wait too long, and you might lose it.

Here's a simple framework to guide your decision.

The Quick Decision Flowchart

Are your options underwater (strike price higher than current stock price)? → Wait. No reason to exercise at a loss.

Are you leaving the company soon? → Decide within 90 days of your last day. This is your hard deadline.

Do you need cash now? → Consider cashless exercise. You get money immediately without paying upfront.

Are your options deep in the money with years until expiration? → You can afford to wait and see what happens.

Do you want to start the ISO holding period for tax benefits? → Consider early exercise if you have the cash and believe in long-term growth.

Four Key Questions to Ask Yourself

How far in the money are your options? Options $100 in the money are more valuable than options $10 in the money. The bigger your potential profit, the more you might want to lock it in.

How much time until expiration? Options expiring in 2 years need a decision soon. Options expiring in 8 years give you breathing room.

Do you have cash to exercise? If you have 1,000 options at a $50 strike price, you need $50,000 to exercise. That's real money most people don't have lying around.

What's your tax situation this year? A big bonus or stock sale might push you into a higher tax bracket. Exercising options adds more taxable income on top.

Real Employee Scenarios

Scenario 1: Maria's Cash Crunch Maria has 500 options with a $20 strike price. The stock trades at $100. That's $80 in the money per option, or $40,000 total profit. Her options expire in 5 years.

She needs $25,000 for a house down payment next month.

Decision: Cashless exercise now. She sells enough shares to cover the exercise cost and taxes, pockets the rest for her down payment. She's not trying to time the market perfectly, she has a real need.

Scenario 2: James the Believer James has 1,000 options at a $30 strike price. The stock trades at $50, so he's $20 in the money. His options expire in 8 years.

He believes the company will grow significantly. He has stable income and no urgent cash needs.

Decision: Wait. He has plenty of time, and his upside could be much bigger if the stock keeps climbing. If the stock hits $100, his profit doubles from $20,000 to $70,000.

Scenario 3: Lisa's Departure Lisa is leaving her company in 2 months. She has 800 vested options at a $15 strike price. The stock trades at $45, putting her $30 in the money.

She has 90 days after her last day to exercise, or her options disappear.

Decision: Exercise before the deadline. She has $12,000 to cover the $15 strike price ($15 × 800 shares). She'll pay taxes but keep the shares. If she doesn't have the cash, she'll do a cashless exercise to at least capture some value.

Don't Try to Perfectly Time the Market

Nobody rings a bell at the stock's peak price. Even professional investors get timing wrong.

Your decision should be based on your personal situation, not trying to predict where the stock goes next. Do you need money now? Are you leaving? Do you want to reduce risk by cashing out some gains?

These are better questions than "Will the stock go up or down?"

One important rule: Never exercise options you can't afford to lose. If exercising means draining your emergency fund or going into debt, wait or do a cashless exercise instead.

Now that you know when to exercise, let's talk about what happens after you own shares. The next section covers blackout periods and the rules around selling your stock.

Selling Your Shares: Blackout Periods and Trading Rules

You've exercised your options. You own shares. Now you want to sell them. But there's a catch: at public companies, you can't sell whenever you want.

Blackout periods are like store hours. The stock market is open, but your company says "you can't trade right now." These quiet periods happen around four times per year, when your company is preparing to announce quarterly earnings.

Here's why: Company insiders (that includes you if you have stock options) might know information the public doesn't. To prevent unfair trading, companies block everyone from buying or selling their stock during sensitive times.

When Blackouts Happen

Most companies follow this pattern:

- Blackout starts: 2-4 weeks before earnings announcement

- Blackout ends: 2-3 days after earnings are public

- Total duration: Usually 2-6 weeks

- Frequency: Four times per year (quarterly earnings)

Some companies add extra blackouts for major announcements like mergers or product launches.

Real Example: Bad Timing

You earn $95,000 and hold 200 NSOs with a $50 strike price. The stock trades at $120. You plan to exercise and sell on April 1 to cover a down payment.

Problem: Your company reports Q1 earnings on April 15. The blackout period runs March 15 to April 20.

You have three options:

- Exercise before March 15 (if you have the cash)

- Wait until April 21 (hope the stock price holds)

- Set up a 10b5-1 plan in January (more below)

The 10b5-1 Workaround

A 10b5-1 plan is like setting up automatic bill pay. You decide today: "Sell 50 shares on the 15th of every month for the next year." Once it's set up, the sales happen automatically, even during blackouts.

The catch? You must set it up during an open trading window, and it typically requires a 30-90 day waiting period before the first sale.

Violating Blackout = Serious Consequences

Trading during a blackout period can result in:

- Immediate termination

- Legal penalties from the SEC

- Repayment of any profits

Even if you didn't know about non-public information, breaking the blackout can end your career.

How to Stay Safe

Check your company's insider trading policy. It's usually in your employee handbook or stock plan documents. Most companies send email reminders when blackout periods start and end.

Sign up for notifications. Many companies have an internal system that alerts you to trading windows. Ask your HR or legal team how to register.

When in doubt, ask. Contact your company's legal or compliance team before making any trade. A five-minute email can save your job.

Now that you understand the rules around selling, let's put everything together into an action plan you can actually use.

Your Next Steps: Creating Your Stock Options Action Plan

You've learned how stock options work. Now it's time to take control of this benefit. Think of this action plan like assembling furniture - you need to gather your parts (information) before you can build anything.

This Week: Gather Your Information

Action 1: Log into your equity portal. Your company uses a platform like E*TRADE, Fidelity, Schwab, or Morgan Stanley. Find the login link in your HR emails or ask your manager.

Action 2: Download your grant agreement. This document shows your strike price, number of options, and vesting schedule. Save it somewhere you won't lose it.

Action 3: Identify your option type. Look for the words "Incentive Stock Options (ISOs)" or "Non-Qualified Stock Options (NSOs)" in your grant agreement. Write it down.

This Month: Run the Numbers

Action 4: Calculate your current option value. Find your company's current stock price (ask HR if you're pre-IPO). Subtract your strike price. Multiply by the number of vested options you have.

Example: You have 1,000 vested options at a $10 strike price. Stock trades at $50. Your spread is $40 per option. Current value: 1,000 × $40 = $40,000 (before taxes).

Action 5: Review your vesting schedule. Set calendar reminders for when new options vest. If you have a one-year cliff, mark that date clearly.

This Quarter: Make Your Plan

Action 6: Decide on your exercise strategy. Will you exercise and hold? Exercise and sell? Wait until you leave? Use the decision framework from Section 10.

Action 7: Consult a tax professional. Before exercising more than a few thousand dollars worth of options, talk to a CPA who understands equity compensation. The AMT trap and tax bills are real.

You now have the knowledge to make smart decisions about your stock options. Start with this week's actions today. Your future self will thank you.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis