Equity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Everything you need to know about getting paid in company stock

Published March 14, 2026 · Updated March 14, 2026

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

What Is Equity Compensation? (And Why Your Company Offers It)

You just got a job offer. The salary looks good at $140,000. But there's another line: "$40,000 annual equity grant." What does that even mean?

Equity compensation means getting paid in company stock instead of just cash. Think of it like your employer saying, "We'll pay you partly in shares of our company. If we do well, those shares become more valuable. If we don't, they might be worth less or even nothing."

It's different from your salary in one big way. Your $140,000 salary hits your bank account as guaranteed cash. That $40,000 in equity? It's a target, not a promise. The actual value depends on your company's stock price when you can sell those shares.

Why Companies Use Equity Compensation

Companies, especially tech firms, offer equity for three reasons:

-

It saves cash now. A startup might not have $200,000 to pay you, but they can offer $140,000 salary plus $60,000 in stock.

-

It makes you think like an owner. When you own company stock, you care more about the company succeeding. Your interests align with the company's interests.

-

It keeps you around longer. Most equity comes with strings attached. You have to stay at the company for years to get all of it (more on this in the vesting section).

What This Looks Like in Real Life

Sarah gets an offer from a tech company. Here's her compensation breakdown:

- Base salary: $140,000 (guaranteed cash)

- Annual bonus target: $20,000 (depends on performance)

- Annual RSU grant: $40,000 (depends on stock price)

- Total target compensation: $200,000

Only $140,000 is guaranteed. The rest depends on company performance and stock price. If the company's stock doubles, that $40,000 equity grant could be worth $80,000. If the stock drops 50%, it's worth $20,000.

Your total compensation package includes both cash and equity. Understanding the equity piece is crucial because it can be the difference between a good offer and a great one.

Now let's break down the different types of equity you might see in your offer letter.

WTF is Stock-Based Compensation (SBC)? EASY guide

The Four Main Types of Equity Compensation

Think of equity compensation like different types of coupons. Some give you free stuff after you wait. Others let you buy things at a locked-in price. Each type has different rules.

Here are the four main types you'll see:

RSUs (Restricted Stock Units): You get actual shares after a waiting period. It's like a gift card that unlocks over time. The company says "we'll give you 100 shares, but you have to stay for 2 years to get them."

ISOs (Incentive Stock Options): You get the right to buy shares at a set price, with special tax benefits. Think of it like a Costco membership that locks in today's prices for future purchases. If your company grows, you can still buy at the old, lower price.

NSOs (Non-Qualified Stock Options): Same idea as ISOs (you can buy shares at a locked-in price), but different tax treatment. These are more flexible but you'll pay more in taxes.

ESPP (Employee Stock Purchase Plan): You can buy company stock at a discount, usually 15% off. It's like an employee discount at a retail store, but for your company's stock.

Which Type Will You Get?

Your company type determines what you'll likely see:

Public companies (Google, Microsoft, Apple):

- RSUs are the standard

- ESPP is common as an extra benefit

- Example: You get 100 RSUs worth $200 each = $20,000 value, plus you can join ESPP to buy stock at 15% discount

Private companies and startups:

- Stock options (ISOs or NSOs) are the norm

- Example: You get options to buy 10,000 shares at $1 each, hoping the shares become worth $10+ someday

Quick Comparison

| Type | What You Get | When You Pay | Best For |

|---|---|---|---|

| RSUs | Actual shares (after waiting) | Nothing upfront | Public companies |

| ISOs | Right to buy at set price | When you buy | Startups, early employees |

| NSOs | Right to buy at set price | When you buy | Contractors, later employees |

| ESPP | Discount buying program | Paycheck deductions | Anyone at public companies |

Most people have 1-2 types of equity, not all four. Your offer letter will spell out exactly what you're getting.

Now that you know the basic types, let's talk about the catch: you don't get this equity all at once.

Equity Compensation 101: How RSUs, ISOs, NSOs, and ESPP Plans Work

Stock Options vs RSUs: Complete Guide to Equity Compensation for Beginners

How Vesting Works (Your Equity Isn't Yours Right Away)

Here's the catch with equity compensation: when your company grants you shares, you don't actually own them yet. You have to earn them over time by staying at the company. This process is called vesting.

Think of vesting like a coffee shop loyalty card. You don't get your free coffee after your first visit. You earn stamps with each purchase, and only after 10 stamps do you get the reward. Vesting works the same way, except instead of coffee, you're earning shares, and instead of purchases, you're earning them by working at the company.

Why Companies Make You Wait

Companies use vesting schedules for one simple reason: to keep you around. If they gave you all your equity on day one, you could quit the next week and walk away with everything. Vesting creates what's called "golden handcuffs." The longer you stay, the more you earn.

The Standard Vesting Schedule: 4 Years with a 1-Year Cliff

Most tech companies use the same basic vesting schedule:

- Total vesting period: 4 years

- The cliff: You get nothing for your first year

- After the cliff: Shares vest monthly or quarterly for the remaining 3 years

The "cliff" is exactly what it sounds like. You're walking toward a cliff edge for 12 months. If you quit (or get fired) before you reach it, you fall off and get zero shares. But once you make it past that one-year mark, a big chunk of your equity vests all at once.

A Real Example: Marcus's Vesting Timeline

Marcus joins a tech company on June 1, 2024. His offer includes 400 RSUs with standard vesting.

Here's exactly when his shares vest:

- June 1, 2024: Marcus starts. He has 400 RSUs granted but 0 vested.

- June 1, 2025 (the cliff): 100 RSUs vest (25% of total). This is his reward for making it one year.

- July 1, 2025 through May 1, 2028: 8.33 RSUs vest on the 1st of each month for 36 months.

Let's say Marcus decides to leave on December 1, 2026. That's 18 months after his cliff. Here's what he keeps:

- 100 RSUs from his one-year cliff

- 150 RSUs from 18 months of monthly vesting (8.33 × 18 = 150)

- Total vested: 250 RSUs

The remaining 150 RSUs? Gone. He forfeits them because they haven't vested yet.

What Happens If You Leave Early

This is crucial to understand: unvested equity disappears when you leave the company. It doesn't matter if you quit, get laid off, or get fired. If the shares haven't vested yet, you don't get them.

This is why timing matters when you're thinking about leaving a job. If you're two weeks away from a big vesting date, those two weeks could be worth thousands of dollars. Check your vesting schedule before you turn in your notice.

Different Vesting Frequencies

While the 4-year timeline is standard, companies vest shares at different intervals:

- Monthly vesting: 1/48 of your total grant vests each month after the cliff (most common)

- Quarterly vesting: 1/16 of your total grant vests every 3 months after the cliff

- Annual vesting: 25% vests each year (less common, but some companies still do this)

Monthly vesting is better for you because you're earning equity more frequently. With quarterly vesting, you could leave a job two months after your last vesting date and lose two months of potential equity.

Your Vesting Schedule Is in Your Offer Letter

Your offer letter should spell out exactly how your equity vests. Look for phrases like "25% after one year, then monthly thereafter" or "quarterly over four years with a one-year cliff."

If it's not clear, ask HR to explain it before you sign. Get specific dates. Know exactly when you'll hit your cliff and when shares vest after that.

Now that you understand how you earn your equity over time, let's talk about what those shares are actually worth.

Understanding Your Equity's Value (What Are Your Shares Actually Worth?)

Figuring out what your equity is worth is like pricing collectibles. If you own baseball cards, you can check eBay to see what people are paying right now. That's easy. But if you own something rare with no active market, you need an expert to guess what someone might pay someday. That's the difference between public and private company equity.

If You Work at a Public Company

Your math is simple: number of shares × current stock price = your equity value.

Let's say you work at Adobe. You have 200 vested RSUs. Adobe stock is trading at $475 per share today.

Your calculation: 200 shares × $475 = $95,000

You can check your company's stock price anytime on Google Finance, Yahoo Finance, or your brokerage app. The price updates throughout the trading day (9:30am to 4pm Eastern, Monday through Friday). This is real money you can access. You can sell your shares today if you want.

If You Work at a Private Company

Your situation is trickier. Private companies don't trade on public markets, so there's no daily stock price. Instead, your company gets something called a 409A valuation every 12 months (or when something big changes, like a funding round).

A 409A valuation is an independent appraisal. Think of it like getting your house appraised. An outside expert estimates what your company's shares are worth based on financials, growth, and comparable companies.

Here's an example. Tom works at a startup. He has 5,000 vested options with a $2.50 strike price. The latest 409A values each share at $8.

His paper gain: 5,000 shares × ($8 - $2.50) = $27,500

But here's the catch. Tom can't sell these shares. There's no market for them. This $27,500 is "paper value," not real money. He won't see actual cash until there's a liquidity event (the company goes public or gets acquired).

The Reality Check

If you work at a private company, your equity might be worth a lot on paper. But paper value and spendable money are completely different things. You can't pay your mortgage with illiquid shares. You need to wait for an exit event, which might take years or might never happen.

Now that you know what your equity is worth today, let's talk about the part nobody likes: taxes.

The Tax Basics You Need to Know

Here's the thing nobody tells you upfront: equity compensation creates tax bills at weird times, and the amount you owe depends on what type of equity you have.

Think of equity taxes like fees charged at different stages of buying a house. You pay some fees when you sign the contract, others when you close, and more if you sell later. Same with equity, different fees (taxes) hit at different moments.

When You'll Owe Taxes

RSUs: You owe ordinary income tax the moment they vest. Even if you don't sell a single share.

Stock options: You owe taxes twice. First when you exercise (buy the shares), then again when you sell them.

ESPP: You owe taxes based on your discount and how long you hold the shares before selling.

The Big Surprise Most People Miss

When 100 of Maya's RSUs vest, they're worth $18,000. Her company automatically withholds 22% for federal taxes ($3,960) by keeping 22 shares and giving her 78 shares. She still owes more at tax time because her actual tax rate is 35%, so she'll owe an additional $2,340 (13% of $18,000) when she files her return.

See the problem? Maya got shares worth $18,000 but only received 78 shares (worth about $14,000). She still owes $2,340 in cash when she files taxes.

What You Need to Remember

Your company handles RSU taxes automatically by withholding shares. But you're on your own for option taxes, you have to pay when you exercise.

Expect to pay 30-50% total in taxes depending on your income, your state, and whether it's ordinary income or capital gains. Yes, that high.

Important: This is a simplified overview. Tax rules get complicated fast, especially with ISOs, AMT, and state taxes. Always consult a tax professional before making big equity decisions.

Now that you understand the tax implications, let's talk about what happens to all this equity if you decide to leave your job.

What Happens to Your Equity When You Leave Your Job

Leaving your job is like canceling a gym membership. Some benefits stop immediately. Others you keep forever. Your equity works the same way.

Here's what happens to each piece:

Unvested Equity Disappears Immediately

Any equity that hasn't vested yet? Gone. You forfeit it the day you leave.

Think of unvested equity like an unfinished rewards card at a coffee shop. You needed 10 stamps to get a free drink, but you only have 7. When you stop going to that coffee shop, those 7 stamps are worthless. You don't get a partial reward.

If you have 1,000 RSUs and only 400 have vested, you lose the other 600. No exceptions. No partial credit.

Vested RSUs Are Yours to Keep

Good news: vested RSUs stay in your account. They're your property now.

These shares will remain in your brokerage account (like E*TRADE or Fidelity). You can sell them whenever you want. You can hold them for years. The company can't take them back.

Vested Stock Options Have a Ticking Clock

This is where things get urgent.

You typically have 90 days from your last day of work to exercise vested options. After that, they expire. Worthless. Even if they could have made you rich.

The 90-day countdown starts on your final employment day, not when you give notice. Mark this date on your calendar immediately.

A Real Example: Derek's 90-Day Deadline

Derek leaves his startup job on April 1. Here's what he owns:

- 8,000 vested stock options (strike price: $3 each)

- 4,000 unvested stock options

What happens:

- The 4,000 unvested options vanish on April 1

- He has until June 30 (90 days later) to exercise the 8,000 vested options

- To exercise, he needs $24,000 cash upfront (8,000 shares × $3)

- The current 409A value is $12/share

- His paper gain would be $72,000 if he exercises (8,000 × $9 difference)

- But he also owes taxes on that $72,000 gain

Derek has three months to find $24,000 plus tax money, or those options disappear forever.

Why the Rush?

Stock options require cash upfront to exercise. You're buying the shares at your strike price.

If Derek's options had a $10 strike price instead of $3, he'd need $80,000 cash in 90 days. Most people don't have that sitting around.

This is why people often let valuable options expire. They can't afford to exercise them in time.

Voluntary vs. Termination: Same Rules

It usually doesn't matter if you quit or get fired. The same equity rules apply.

Some exceptions exist for retirement or disability, but these vary by company. Don't count on special treatment.

Some Companies Offer Extended Windows (But Don't Count On It)

A few companies (mostly well-funded startups) give you longer than 90 days. Some offer 5 or 10 years.

This is rare. Very rare. Don't assume your company does this.

Check Your Documents Now

Every company has an equity plan document and individual grant agreements. These spell out exactly what happens when you leave.

Find these documents in your equity portal or HR system. Read the "termination" section before you need it.

Key things to look for:

- Exact post-termination exercise window (90 days is standard, but confirm)

- Whether the window differs for retirement or disability

- Any acceleration clauses (equity that vests early in certain situations)

- Blackout periods that might affect when you can sell

Bottom line: Leaving your job puts your equity on a deadline. Vested RSUs are safe. Unvested equity is gone. Vested options give you 90 days to make an expensive decision.

Now that you know what happens when you leave, let's talk about how to actually keep track of all this equity while you're still employed.

How to Track and Manage Your Equity

Think of your equity like a bank account. You wouldn't go months without checking your balance, right? The same goes for your stock compensation.

Where Your Equity Lives

If you work at a public company, your equity sits in a brokerage account. The big ones are:

- E*TRADE

- Fidelity

- Morgan Stanley

- Charles Schwab

You got login credentials when your company first granted you equity. Can't find them? Call your HR department or the brokerage directly.

If you work at a private company, you'll track your equity through platforms like:

- Carta

- Shareworks

- Certent

These platforms show what you own, even though you can't sell yet.

What Your Dashboard Shows

When Lisa logs into her Fidelity account, here's what she sees:

- Total RSUs Granted: 800 shares

- Vested: 350 shares (she owns these now)

- Unvested: 450 shares (still earning these)

- Current Value of Vested: $87,500 (at $250 per share)

She clicks on "Unvested" and sees exactly when her next 100 shares vest: in 47 days. No surprises.

Your dashboard works the same way. Look for these key numbers:

- Granted (total promised to you)

- Vested (what you've earned)

- Unvested (what's still locked)

- Current value (what vested shares are worth today)

How Often to Check

Check your equity once per quarter at minimum. Mark your calendar. Set a reminder. Make it a habit like paying bills.

Why quarterly? That's when most companies release earnings reports. Stock prices often move after these reports. You want to know where you stand.

What to Save

Download and keep these documents:

- Annual equity statements (download every January)

- All grant agreements (the paperwork when you first got equity)

- Vesting schedules (when your shares unlock)

- Cost basis information (what you paid in taxes, needed later)

Lisa downloads her annual statement in January and saves it in a folder called "Taxes 2024." When April rolls around, she has everything her accountant needs.

Track Your Cost Basis

Your cost basis is what you "paid" for your shares (usually the taxes you owed when RSUs vested). You need this number when you sell. Otherwise, you might pay taxes twice.

Most brokerages track this automatically. But double-check. Download a spreadsheet once a year with:

- Vest date

- Number of shares

- Price per share at vest

- Taxes paid

The Bottom Line

You don't need to obsess over your equity dashboard daily. But ignoring it completely? That's leaving money on the table.

Set a quarterly reminder. Log in. Check the numbers. Save your statements. That's 15 minutes every three months to protect potentially hundreds of thousands of dollars.

Now that you know where your equity lives and how to track it, let's talk about the things your company might not volunteer to tell you.

Red Flags and What Your HR Won't Tell You

Your equity compensation is part of your pay. You wouldn't ignore missing paychecks, so don't ignore equity problems.

Think of your equity grants like a contract to buy a house. If the seller keeps delaying the paperwork or the numbers don't match what you agreed to, you'd speak up immediately. Do the same with your stock benefits.

Get Everything in Writing (Seriously)

Verbal promises mean nothing. Your manager might say "we'll give you 5,000 RSUs" in your interview, but that's worthless without a signed grant agreement.

What matters:

- Your signed offer letter

- Your official grant agreement

- Confirmation emails from HR or your equity platform

Save all of these. Take screenshots. If your company uses DocuSign or a similar system, download the PDFs.

Common Red Flags to Watch For

Your numbers don't match. Paulo's offer letter promised $50,000 in annual RSU grants. His grant agreement showed only $40,000 worth of shares. He assumed it was a typo and didn't ask. Big mistake. By the time he noticed, his offer letter window had expired. Always verify the numbers match before you sign anything.

You can't access your equity account. Your equity account should be set up within 30 to 60 days of starting. If you're at day 90 and HR keeps saying "it's being processed," escalate immediately. Email your manager and HR in writing: "I need confirmation of my equity grants and access to my account by [specific date]."

Missing vesting dates. Check your account every time shares should vest. If 25 shares were supposed to vest on March 15 and they're not there by March 20, ask why. Sometimes it's a processing delay. Sometimes it's a real problem.

The company keeps changing the story. First they say you're getting options. Then it's RSUs. Then maybe phantom stock. Changing equity types isn't always bad, but you deserve a clear explanation in writing about why and how it affects you.

Private Company Warning Signs

Startups love to hype their valuations. "Your options are worth $500,000 based on our Series B!" sounds amazing. But that number might be fantasy.

Be skeptical if:

- The valuation is more than 6 months old

- The company is burning through cash quickly

- They can't explain how they calculated your equity's value

- Leadership keeps pushing back the IPO or acquisition timeline

A 409A valuation (the official IRS-approved number) is more reliable than a funding round valuation. Even then, private company stock can become worthless if the business fails.

Questions HR Might Not Answer (But You Should Ask Anyway)

"Can I see my actual grant agreement, not just the summary?" Summaries leave out important details like vesting acceleration terms or what happens if the company is acquired.

"What's the current 409A valuation?" For private companies, this tells you the real strike price for options or the taxable value of RSUs.

"What happens to my unvested equity if I'm laid off?" Most companies say you lose it, but some have acceleration clauses.

"Has the company ever repriced options or modified grants?" This tells you if leadership has helped employees when stock prices dropped.

What to Do If Something Seems Wrong

Don't wait. Don't assume it will fix itself.

Step 1: Email HR with specific questions. "My offer letter states 10,000 options, but my grant agreement shows 8,000. Please explain the difference."

Step 2: If you don't get a clear answer within a week, loop in your manager.

Step 3: If it's still unresolved, consider talking to an employment lawyer. Many offer free consultations.

Keep records of everything. If you eventually need to escalate, you'll want proof of what was promised and when you raised concerns.

The Bottom Line

Your company isn't trying to cheat you (usually). But mistakes happen. Systems glitch. HR gets overwhelmed. It's your money, so it's your job to verify everything is correct.

Now that you know what to watch out for, let's look at the mistakes people make even when their equity is set up correctly.

Missing the 90-day exercise window can result in losing significant potential gains.

Missing the 90-day exercise window can result in losing significant potential gains.

Common Mistakes People Make With Equity Compensation

Think of your equity compensation like a garden. If you ignore it, you won't get the harvest. Worse, you might lose everything you've grown.

Here are the most common mistakes people make, and how to avoid them.

Mistake 1: Never reading your grant agreement

You got an email with a PDF attachment. You clicked "accept" and moved on. Bad idea.

Instead, read your grant agreement. Look for your vesting schedule, the type of equity, and what happens if you leave. It takes 10 minutes and could save you thousands.

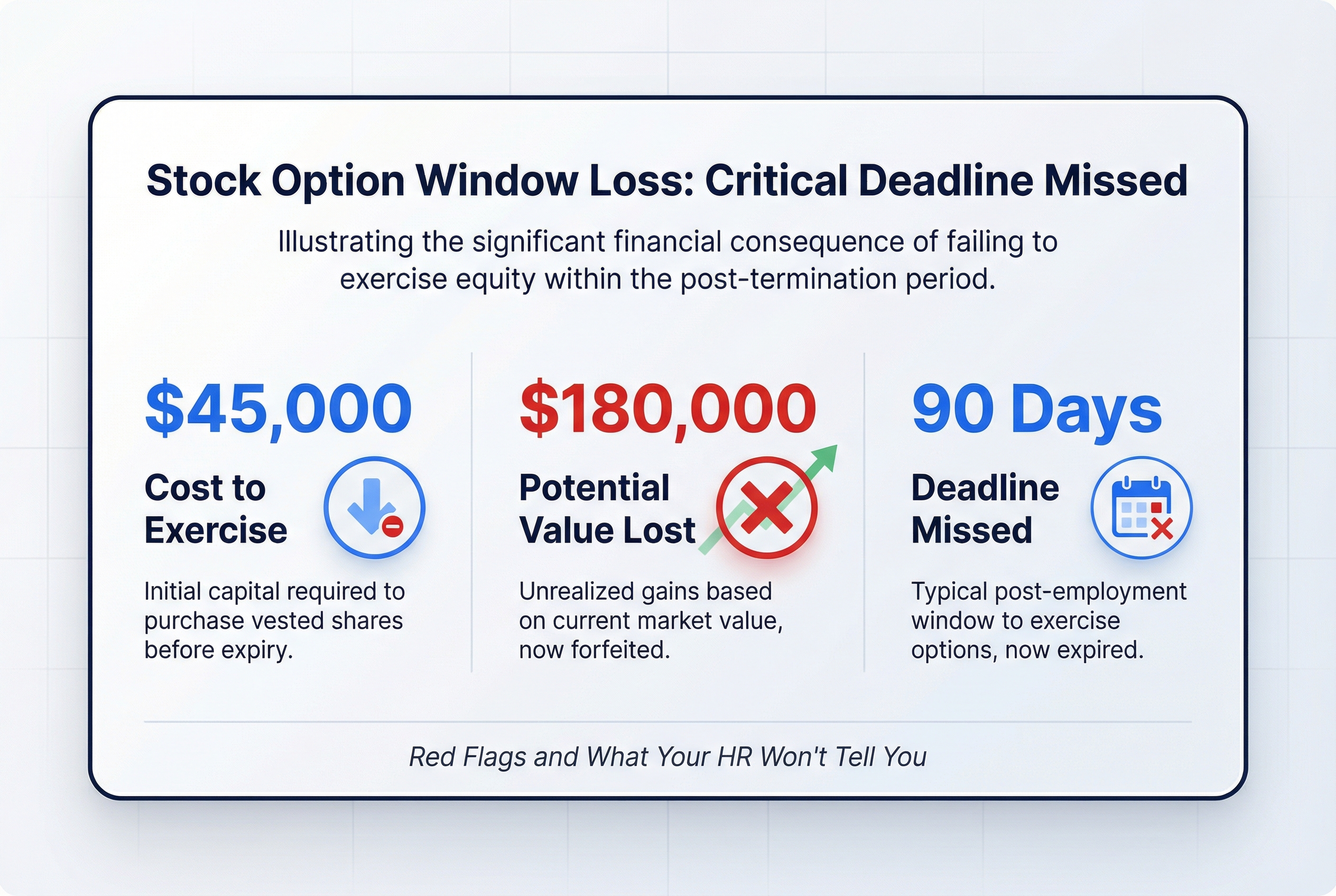

Mistake 2: Missing the 90-day exercise window

Chen had 15,000 vested options when he left his startup. He thought he had a year to decide. He actually had 90 days. He missed the deadline and lost options that would have cost $45,000 to exercise but were worth $180,000.

Instead, check your post-termination exercise window the day you give notice. Mark the deadline on your calendar immediately.

Mistake 3: Not saving for tax bills

Your RSUs vest. You get shares worth $30,000. You owe taxes on $30,000 of income. But you might only get 60% of the shares after automatic withholding. That might not cover your full tax bill.

Instead, set aside cash for taxes before RSUs vest. Talk to a tax professional about your actual tax rate.

Mistake 4: Keeping all your eggs in one basket

Aisha's RSUs at her public company now represent 85% of her net worth. That's $340,000 of her $400,000 total savings. If her company stock drops 30%, she loses $102,000 of her wealth overnight.

Instead, sell some equity and invest in a diversified portfolio. A good rule: company stock shouldn't be more than 10-20% of your total investments.

Mistake 5: Making emotional decisions

You panic when the stock drops and sell everything. Or you hold because you love your company, even when you should diversify.

Instead, make a plan when you're calm. Decide in advance when you'll sell and stick to it.

Mistake 6: Not getting tax help before exercising options

Exercising ISOs can trigger AMT (Alternative Minimum Tax). Exercising NSOs creates immediate taxable income. These mistakes can cost you thousands.

Instead, talk to a tax professional before you exercise any options. The consultation fee is worth it.

Mistake 7: Trusting private company valuations

Your startup says your equity is worth $200,000 on paper. But you can't sell it. The company might never go public. The valuation might be inflated.

Instead, treat private company equity as a lottery ticket. Hope for the best, but don't count on it for your financial plans.

Now that you know what to avoid, let's talk about what to do next.

What to Do Next: Your Action Plan

Getting equity compensation is like receiving a high-end appliance. It has real value, but you need to read the manual and set it up properly to actually benefit from it.

Here's your step-by-step action plan. We've included time estimates so you can tackle this without feeling overwhelmed.

Today (30 minutes)

Find and read your grant agreements. These documents explain exactly what you own and when you'll get it.

Email HR or check your equity account portal for PDF copies. Look for documents with "grant agreement" or "award letter" in the name. Read them once through, even if parts seem confusing. You'll understand more after finishing this guide.

This Week (1 hour total)

Set up or verify access to your equity account. Your company uses a platform like E*TRADE, Schwab, Fidelity, or Morgan Stanley. If you haven't logged in yet, find your welcome email or ask HR for the link.

Mark your vesting dates on your calendar. Look at your grant agreement and add reminders for each vesting date. Set them for one week before the actual date so you have time to plan.

This Month (2-3 hours total)

Calculate the tax impact of your next vesting event. Use our RSU tax calculator or ISO tax calculator (links at the end of this guide). This helps you avoid surprises.

Example: You have 1,000 RSUs vesting 25% per year starting June 1, 2025. Your company stock trades at $150. When your first 250 shares vest, you'll owe roughly $8,000 in taxes (assuming a 35% combined rate). Start saving $200 per month now so you're ready.

Decide if you need professional help. Consider talking to a financial advisor or tax professional if you have ISOs, if your equity is worth more than $50,000, or if you're planning to leave your company soon.

Ongoing Actions

Check your equity value quarterly. Set a recurring calendar reminder. This takes five minutes and helps you make informed decisions.

Review your overall financial plan. Your equity should fit into your bigger picture. Are you saving enough in your 401(k)? Do you have an emergency fund? Don't let equity compensation distract you from the basics.

Real Example: Sarah's First Month

Sarah just started at a tech company. Here's what she did:

Day 1: Asked HR for her grant agreement during onboarding.

Week 1: Read the agreement and highlighted key facts. She has 1,000 RSUs vesting 25% per year starting June 1, 2025.

Week 2: Set up her Schwab account and confirmed all 1,000 RSUs appeared correctly.

Month 1: Used our calculator and learned she'd owe about $8,000 in taxes when her first 250 shares vest. She started saving $200 per month.

Month 1: Read our detailed RSU guide to understand when to sell and when to hold.

Sarah now feels confident instead of confused. You can too.

Your Next Steps

You've learned the basics. Now dive deeper into your specific equity type:

- RSU holders: Read our complete RSU guide for selling strategies and advanced tax planning

- ISO holders: Check out our ISO guide to understand AMT and the qualified small business stock exclusion

- ESPP participants: Learn how to maximize your 15% discount and avoid surprise taxes

- Stock option holders: Understand when to exercise and how to avoid leaving money on the table

The most important thing? Take action this week. Thirty minutes today to find your grant agreement beats hours of stress later.

You've got this.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

How ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

ESPPESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

TaxThe ISO AMT Trap: How Exercising Stock Options Can Cost You Thousands in Unexpected Taxes

The ISO AMT trap catches thousands of employees off guard every year. When you exercise incentive stock options, you might owe Alternative Minimum Tax on paper gains you haven't actually received - sometimes tens or hundreds of thousands of dollars. This guide explains exactly how the trap works and how to avoid it.

Not sure what to do with your equity?

Get a free personalized analysis