ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

Understanding what you'll owe when you sell your employee stock purchase plan shares

Published March 14, 2026 · Updated March 14, 2026

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

Why Your ESPP Tax Bill Might Surprise You

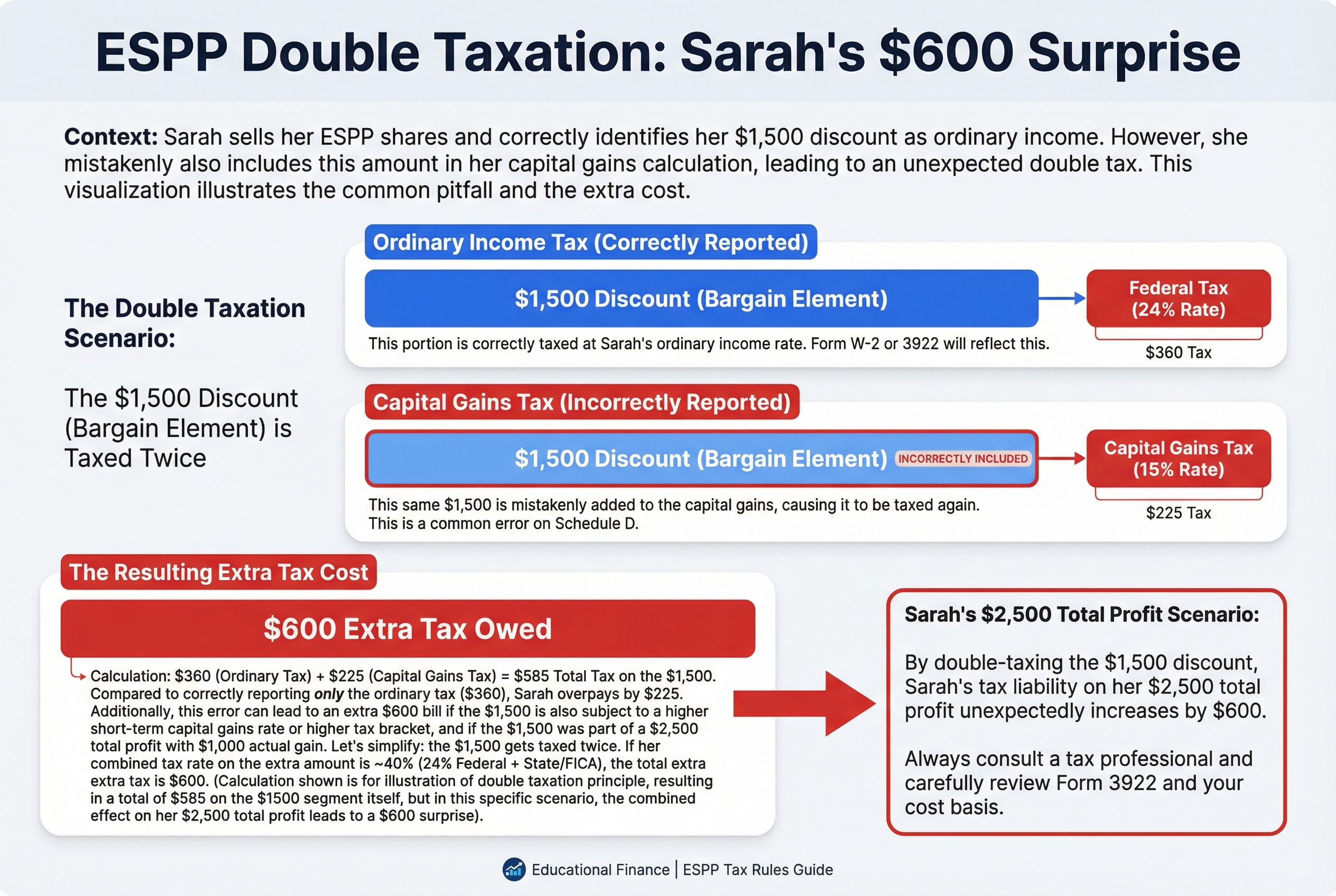

Sarah sold $10,000 of ESPP shares last year and made a clean $2,500 profit. She set aside money for capital gains tax, filed her return, and waited for her refund.

Then she got a letter from the IRS. She owed $600 more than expected.

Here's what happened. Sarah's company had already reported $1,500 of her profit as ordinary income on her W-2. She paid her regular 24% tax rate on that amount. But she didn't know to look for it, so she reported the full $2,500 as capital gains. She paid tax on the same money twice.

This happens to thousands of ESPP participants every year. The confusion comes from one surprising fact: the IRS doesn't treat all your ESPP profit the same way.

The Discount Creates Instant Taxable Income

When you buy ESPP shares, you typically get a 15% discount. Buy shares worth $100 for just $85. That $15 discount is real money in your pocket.

Think of this discount like a cash bonus from your employer. The IRS sees it the same way. They want to tax it as ordinary income, just like your salary. That means your highest tax rate, not the lower capital gains rate.

But here's where it gets tricky: how long you hold the shares changes everything.

Hold them long enough, and some of that discount gets taxed at lower capital gains rates instead. Sell too soon, and the entire discount gets hit with ordinary income tax. The tax timer starts ticking the moment you buy those shares, not when your company first offered them to you.

The difference between these two scenarios can mean hundreds or thousands of dollars in extra taxes. Let's break down exactly how this works.

ESPP Taxation

Sarah's $600 surprise tax bill resulted from paying tax on her $1,500 discount twice.

Sarah's $600 surprise tax bill resulted from paying tax on her $1,500 discount twice.

The Two Types of ESPP Sales: Qualifying vs. Disqualifying

When you sell ESPP shares, the IRS treats your sale one of two ways: qualifying or disqualifying. Think of it like a waiting game with two finish lines. You must cross both to win the tax break.

Here's what makes a sale "qualifying":

You hold your shares for at least 2 years from the offering date AND at least 1 year from the purchase date. Both timers must run out. Miss even one by a single day, and you get disqualifying treatment.

Most ESPP participants (about 70%) make disqualifying sales. They sell within the first year to lock in their discount. Nothing wrong with that, but the tax treatment is different.

Understanding the Two Important Dates

The offering date is when your 6-month purchase period begins. This is usually January 1 or July 1 at most companies.

The purchase date is when shares actually get bought with your paycheck deductions. This happens at the end of the offering period, typically June 30 or December 31.

A Real Timeline Example

Your company's ESPP offering period starts January 1, 2023. You buy shares on June 30, 2023 at the discounted price of $85 (regular price is $100).

For a qualifying disposition, you must hold until:

- July 1, 2024 (1 year from purchase date)

- January 2, 2025 (2 years from offering date)

Sell on December 15, 2024? That's disqualifying. You crossed the 1-year finish line but not the 2-year one.

Sell on January 15, 2025? That's qualifying. You crossed both finish lines.

Here's a simple timeline:

Jan 1, 2023: Offering starts (2-year timer begins)

Jun 30, 2023: You buy shares (1-year timer begins)

Jul 1, 2024: First finish line (1 year from purchase)

Jan 2, 2025: Second finish line (2 years from offering) ← Qualifying sales start here

Now let's look at what you actually owe when you make a disqualifying sale.

RSU ESOP ESPP explained || Taxation rules in India || #finvestomate

Disqualifying Disposition: What You'll Owe When You Sell Early

Most ESPP participants sell early. That means you're looking at a disqualifying disposition, which splits your profit into two tax buckets.

Think of it like this: the IRS wants to tax your discount like a bonus from work. The rest of your profit gets taxed like any stock you bought and sold.

The Two-Part Tax Split

Part 1: Your discount becomes ordinary income

The difference between what you paid and the fair market value on purchase date counts as wages. Your company adds this to your W-2 automatically. It gets taxed at your regular income tax rate (the same rate as your salary).

Your employer already withheld some tax on this amount when you bought the shares. But you might owe more depending on your tax bracket.

Part 2: Any additional gain becomes capital gains

If the stock price went up after you bought it, that extra profit is a capital gain. Your cost basis for this calculation is the FMV at purchase, not your discounted price.

Hold less than one year from purchase? Short-term capital gain, taxed at your ordinary income rate.

Hold more than one year from purchase (but still sell before qualifying)? Long-term capital gain, taxed at the lower 0%, 15%, or 20% rate.

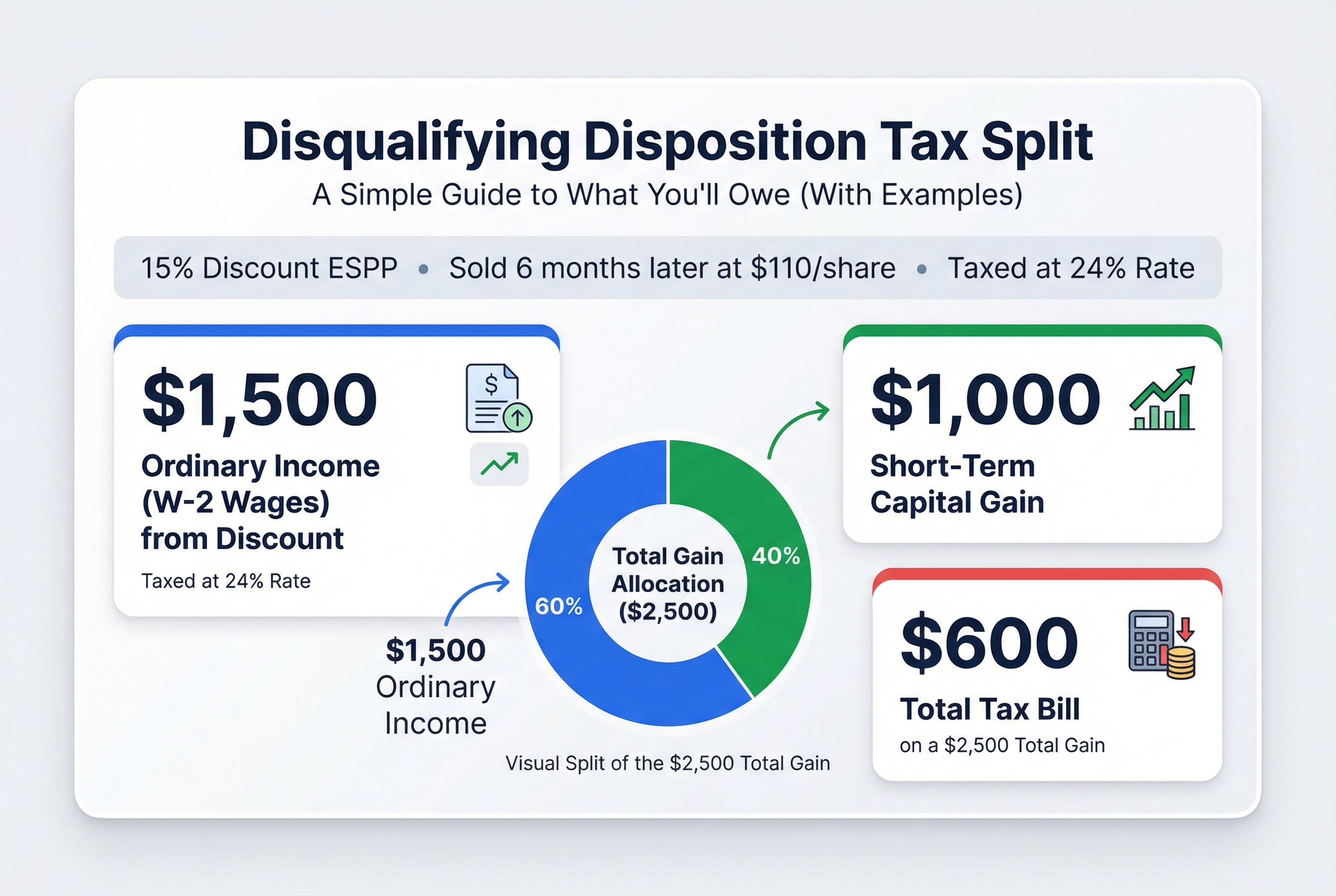

Real Example: The Complete Breakdown

You participate in your company's 15% discount ESPP:

- You pay: $85 per share

- FMV at purchase: $100 per share

- You buy: 100 shares ($8,500 total)

- Six months later, you sell at: $110 per share

Your ordinary income (the discount):

- $100 FMV minus $85 purchase price = $15 per share

- $15 × 100 shares = $1,500

- This shows up on your W-2 as wages

- Taxed at your rate (let's say 24%) = $360

Your short-term capital gain (the price increase):

- $110 sale price minus $100 FMV at purchase = $10 per share

- $10 × 100 shares = $1,000

- Also taxed at 24% (short-term rate) = $240

Total tax bill: $600 on your $2,500 total gain.

Why This Isn't Necessarily Bad

Yes, you're paying ordinary income tax on the discount instead of the lower capital gains rate. But you still got free money (that 15% discount). And if you sell soon after purchase, the stock price hasn't had much time to move anyway.

The real question is whether holding longer for a qualifying disposition saves you enough tax to be worth the risk. We'll run those numbers next.

Disqualifying dispositions split your profit into ordinary income (the discount) and capital gains (the rest).

Disqualifying dispositions split your profit into ordinary income (the discount) and capital gains (the rest).

Qualifying Disposition: The Tax Break for Patient Holders

Think of a qualifying disposition as the IRS giving you a reward for patience. Hold your ESPP shares long enough, and you get a better tax deal. Sometimes much better.

The Two Holding Periods You Must Meet

To qualify for this tax break, you need to hold your shares for:

- At least 2 years from the offering date (when you enrolled)

- At least 1 year from the purchase date (when you bought the shares)

Miss either deadline by even one day? You're back to a disqualifying disposition with higher taxes.

How the Tax Math Works (And Why It's Better)

Here's where qualifying dispositions get interesting. The IRS uses a "lesser of" rule to calculate your ordinary income.

Your ordinary income = the LESSER of:

- The discount you got at purchase, OR

- Your total gain when you sell

Everything beyond that ordinary income portion? That becomes long-term capital gains, taxed at a lower rate (typically 15% instead of your regular income tax rate).

Real Example: Same Shares, Lower Tax Bill

Let's use the same scenario from the disqualifying disposition section. You bought 100 shares at $85 each (15% discount from $100 fair market value). But this time, you hold for the qualifying period and sell at $110.

Step 1: Calculate ordinary income

- Discount at purchase:

$15per share ($100 - $85) - Total gain at sale:

$25per share ($110 - $85) - Ordinary income:

$15per share (the lesser amount) - Total ordinary income:

$15 × 100 = $1,500 - Tax at 24% bracket:

$1,500 × 0.24 = $360

Step 2: Calculate long-term capital gains

- Remaining gain:

$10per share ($25 total gain - $15 ordinary income) - Total capital gain:

$10 × 100 = $1,000 - Tax at 15% rate:

$1,000 × 0.15 = $150

Total tax: $510

Compare that to the disqualifying disposition from the previous section: $600. You just saved $90 by waiting.

The Tax Break Gets Even Better When Your Stock Rises

Now imagine you held those same shares and sold at $120 instead of $110.

Your ordinary income stays the same: $1,500 (still the lesser of the $15 discount or the now $35 total gain). But your long-term capital gain jumps to $2,000 ($20 per share gain beyond the discount).

New total tax: $660

If you'd sold this as a disqualifying disposition at $120, you'd owe $840. That's a $180 savings just for holding longer.

One Important Difference: You Report This Yourself

Unlike disqualifying dispositions, this ordinary income does NOT appear on your W-2. Your employer doesn't track it. You need to calculate and report it yourself on your tax return (we'll cover exactly how in the reporting section).

What If the Stock Price Dropped?

Here's a pleasant surprise. If your stock price fell below the original fair market value, you might owe ZERO ordinary income.

Say you bought at $85 (15% discount from $100), but the stock dropped to $90 by the time you sell. Your total gain is only $5 per share. Under the "lesser of" rule, your ordinary income is $5 (the smaller number), not the full $15 discount.

The qualifying disposition protects you when stock prices fall.

Now that you understand both types of sales and their tax implications, let's look at the specific tax forms you'll need to handle when tax season arrives.

The ESPP Tax Reporting Forms You'll Need to Handle

Tax season brings a pile of forms for your ESPP sales. Think of these forms like puzzle pieces that must fit together correctly. Your broker sends some pieces, your employer sends others, and you need to make sure they connect without gaps or overlaps.

Here's what lands in your mailbox (or inbox) and what each one means.

Form W-2: Your Wages and the ESPP Discount

What it shows: Your regular salary plus any ordinary income from ESPP sales.

Key detail: Look at Box 1 (Wages). If you made a disqualifying disposition, your employer added the discount to this box. For example, if you bought shares at $85 when they were worth $100, that $15 per share discount shows up here as wages.

What it doesn't show: Qualifying dispositions. Those don't appear on your W-2 at all.

Form 1099-B: Your Sale Proceeds

What it shows: The total amount you received when you sold ESPP shares. Your broker (like E*TRADE, Fidelity, or Schwab) sends this.

The trap: Box 1e shows your cost basis, but it's often wrong. Your broker only knows what you paid for the shares ($85 in our example). They don't know that $15 of discount already got taxed through your W-2.

Form 8949: Where You Fix the Basis Problem

This is the detailed transaction form that feeds into Schedule D. You list each ESPP sale here.

Here's where you prevent double taxation:

Let's say you sold ESPP shares for $11,000. Your 1099-B shows proceeds of $11,000 and a cost basis of $8,500 (what you actually paid). But your W-2 already included $1,500 as ordinary income (the discount you got).

On Form 8949, you must adjust your basis:

- Starting basis from 1099-B: $8,500

- Add back W-2 income: +$1,500

- Adjusted basis: $10,000

Without this adjustment, you'd pay tax on that $1,500 twice. Once as wages on your W-2, and again as capital gains. Your actual capital gain to report is $1,000 ($11,000 minus $10,000), not $2,500.

Schedule D: Your Final Capital Gains Summary

Form 8949 calculations flow into Schedule D. This is where you report your total short-term and long-term capital gains or losses from all stock sales.

For qualifying dispositions: You skip the W-2 step. Instead, you report the ordinary income portion directly on Schedule 1 (attached to Form 1040). Then you handle the capital gain part on Form 8949 and Schedule D as usual.

Documents to Keep in Your Files

Your broker's forms won't have everything you need. Save these:

- Purchase confirmation showing the fair market value on the purchase date

- Your ESPP enrollment showing the discount percentage

- Sale confirmations with exact dates and amounts

- Your own spreadsheet tracking the W-2 income for each batch of shares

The IRS gets copies of your W-2 and 1099-B. They'll notice if your numbers don't match or if you're missing a form.

The Timeline: When Forms Arrive

January: Your W-2 arrives from your employer.

February: Form 1099-B comes from your broker.

Tax filing: You complete Form 8949, adjust the basis, then transfer totals to Schedule D.

Common Mistake: Trusting the 1099-B Basis

Your broker doesn't communicate with your HR department. They can't know about the W-2 income. If you just copy the basis from your 1099-B onto your tax return, you'll overpay.

Think of it like this: you already paid income tax on the discount through payroll withholding. Adding it to your basis means you don't pay tax on it again as a capital gain.

Now, what happens when your ESPP shares lose value instead of gaining? The tax rules flip in ways that might actually help you.

When Selling at a Loss Changes Everything

Selling your ESPP shares at a loss doesn't erase your tax bill. In fact, you might owe taxes even when you lost money. This trips up thousands of employees every year.

Think of it like this: the IRS treats your ESPP discount like a bonus you received on day one. Even if you later lose money on the investment, you still got that bonus. And bonuses are always taxable.

Disqualifying Disposition Losses: You Still Owe Tax on the Discount

Here's the painful reality. You bought ESPP shares at $85 when the fair market value was $100. The stock drops and you sell at $80 after 8 months (a disqualifying disposition). You lost $5 per share from your purchase price.

But you still owe ordinary income tax on the $15 per share discount. On 100 shares, that's $1,500 in ordinary income. At a 24% tax rate, you owe $360.

The good news: you have a $2,000 short-term capital loss (100 shares × the $20 drop from $100 FMV to $80 sale price). This capital loss can offset other investment gains.

Net effect: You're out $500 in actual stock value but owe $360 in taxes on income you never really received. Frustrating, but that's the rule.

Qualifying Disposition Losses: A Slightly Better Deal

If you hold long enough for a qualifying disposition and then sell at a loss, the math works differently.

Your ordinary income is the lesser of the discount or your gain. Since you had a loss, your gain is $0. So your ordinary income is $0.

You can claim the full loss as a capital loss. This is one of the few times a qualifying disposition actually saves you money compared to selling early.

The Wash Sale Rule Trap

Here's where it gets worse. If you buy the same stock within 30 days before or after your sale, the IRS disallows your capital loss. This is called the wash sale rule.

The ESPP problem: Your company buys ESPP shares for you every six months. If you sell at a loss in November, but the next ESPP purchase happens in December, you just triggered a wash sale. You can't claim the loss at all.

You must track wash sales across all your accounts. That includes your ESPP, regular brokerage account, IRA, and even your spouse's accounts.

Many employees sell ESPP shares at a loss, expecting a tax deduction, and then discover the wash sale rule wiped it out. The loss isn't gone forever (it gets added to the cost basis of your new shares), but you can't use it right now when you need it.

Now that you understand how losses work, let's look at another complication: state taxes can add a whole new layer of rules to your ESPP.

Even if you sell at a loss, the initial ESPP discount is always taxed as ordinary income.

Even if you sell at a loss, the initial ESPP discount is always taxed as ordinary income.

State Tax Rules: Why Your ESPP Taxes Might Be Different at Home

Think of ESPP taxes like a game where the federal government sets the basic rules, but each state has its own rulebook. Most states follow the federal playbook. A few states play by completely different rules. And some states don't play at all.

The Big Winners: No Income Tax States

If you live in Texas, Florida, Washington, Nevada, Alaska, Tennessee, South Dakota, Wyoming, or New Hampshire, you just won the ESPP lottery. These states have no income tax on wages or investment income. You only pay federal taxes on your ESPP gains. That's an automatic 5-10% savings compared to your coworkers in California or New York.

Most States Follow Federal Rules (With Exceptions)

About 40 states treat ESPP sales the same way the IRS does. Qualifying disposition? Long-term capital gains. Disqualifying disposition? Ordinary income on the discount, capital gains on the rest.

But a few states march to their own drummer. California is the biggest headache.

California's Special Rules

California taxes qualifying dispositions differently than the IRS. Even if you hold long enough for a qualifying disposition at the federal level, California might still tax part of your gain as ordinary income instead of capital gains. The exact calculation gets messy fast.

Here's the practical impact: You buy ESPP shares at $85 (15% discount from $100). You hold for two years and sell at $130. The IRS treats this as a qualifying disposition with favorable tax treatment. California might tax the $15 discount as ordinary income (up to 13.3% state rate) even though the IRS gives you a break.

When You Move States: Double Trouble

Moving between purchase and sale creates a tax puzzle. States generally want to tax income you earned while living there.

Real example: You worked in California when you purchased ESPP shares, then moved to Texas (no income tax) before selling. California may claim the right to tax the discount portion because you earned it while working there.

Say you bought at $85 (15% discount from $100) and sell at $110 after moving to Texas. California might want tax on the $15/share discount even though you're now a Texas resident. You'd need to file a part-year California return reporting that income.

Texas won't tax you (no income tax), but California won't let that discount escape. You end up filing returns in both states.

Which State Gets to Tax What?

The general rule: The state where you worked when you earned the compensation gets to tax the bargain element (the discount). The state where you live when you sell gets to tax the capital gain.

This creates three common scenarios:

- You stayed put: One state taxes everything according to its rules. Simple.

- You moved before selling: Old state taxes the discount, new state taxes the gain. File returns in both.

- You moved to a no-tax state: Old state taxes the discount, new state taxes nothing. You still file in the old state.

States That Don't Follow Federal Qualifying Rules

A handful of states don't recognize the federal qualifying vs. disqualifying distinction. They might tax all ESPP sales the same way, regardless of holding period.

Pennsylvania, for example, taxes the discount as ordinary income when you purchase the shares, not when you sell them. This means you might owe Pennsylvania tax before you've even sold anything.

Your State Tax Checklist

Here's how to figure out what you owe:

- Do you live in a no-tax state? If yes, you're done with state taxes. Lucky you.

- Did you move states between purchase and sale? If yes, expect to file returns in both states. Get help.

- Does your state follow federal ESPP rules? Check your state's department of revenue website or tax forms.

- Did you work in multiple states during the offering period? This gets very complex. Hire a professional.

Where to Find Your State's Rules

Start with your state's department of revenue website. Search for "ESPP taxation" or "employee stock purchase plan." Most states publish guides on equity compensation.

The Federation of Tax Administrators (taxadmin.org) maintains links to all state tax agencies. Your state's instructions for Schedule D (capital gains) often explain how they treat stock compensation.

When to Get Professional Help

Multi-state ESPP situations get complicated fast. If you moved states, worked remotely in different states, or live in California with a qualifying disposition, spend $200-400 for a tax professional who specializes in equity compensation. It's cheaper than getting it wrong.

The next section reveals the tax traps that catch even experienced ESPP participants off guard, including the double taxation mistake that costs people thousands.

The Hidden Tax Traps Your HR Department Won't Mention

Your HR team isn't trying to hide anything from you. They're just not allowed to give tax advice. That leaves you walking through a field of tax landmines with no map.

Here are the seven traps that catch even smart employees off guard.

Trap 1: The Double-Taxation Disaster

The mistake: You sell $50,000 of ESPP shares. Your 1099-B shows you paid $42,500 (your discounted purchase price). You report a $7,500 gain and pay capital gains tax on it.

The problem: That $7,500 discount already showed up on your W-2 as ordinary income. You already paid tax on it once. If you don't adjust your cost basis to $50,000 on Form 8949, you pay tax on the same $7,500 twice.

The cost: At a 15% capital gains rate, that's $1,125 in unnecessary tax per sale. Make this mistake three times a year for five years? You've overpaid $16,875.

How to avoid it: Always add the discount amount from your W-2 to your purchase price when calculating gains. Your real basis is higher than what the 1099-B shows.

Trap 2: Underestimating Your Discount

The mistake: You think you got a 15% discount because your plan offers 15% off.

The problem: If your plan has a lookback provision (most do), you got 15% off whichever price was lower on the offering date or purchase date. When the stock rises during the offering period, your actual discount is much bigger.

Example: Stock is $100 at offering start, $140 at purchase. You pay $85 (15% off $100). Your actual discount is $55 per share, not $21.

How to avoid it: Check both dates. Calculate your discount from the lower price, not just the purchase date price.

Trap 3: Mixing Up Your Dates

The mistake: You count your holding period from the offering date instead of the purchase date.

The problem: The IRS counts from when you actually bought the shares (purchase date), not when the offering period started. Sell one day too early and you blow the qualifying disposition.

How to avoid it: Mark your calendar with the actual purchase date plus one year and one day. That's your earliest qualifying sale date.

Trap 4: Assuming Your Plan Matches the Internet

The mistake: You read an ESPP guide online and assume your plan works the same way.

The problem: ESPP plans vary wildly. Different discount rates. Different lookback rules. Different offering periods. Some let you sell immediately, others have blackout periods.

How to avoid it: Read your actual plan documents. They're usually in your benefits portal under "Stock Purchase Plan" or similar.

Trap 5: Skipping Estimated Tax Payments

The mistake: You sell $100,000 of ESPP stock in May. You figure you'll pay the tax when you file in April next year.

The problem: The IRS wants quarterly estimated payments on large gains. Skip them and you owe penalties plus interest, even if you pay the full tax bill on time in April.

The cost: Penalties run about 8% annually on what you should have paid quarterly. On a $20,000 tax bill, that's $1,600 in penalties you didn't need to pay.

How to avoid it: If you're selling more than $50,000 of ESPP stock, talk to a tax pro about estimated payments before you sell.

Trap 6: The December/January Timing Trap

The mistake: You sell shares on December 28th instead of waiting until January 2nd.

The problem: You just moved a big tax bill forward by a full year. Selling in December means you owe tax by April 15th. Selling in January gives you until April of the following year.

The benefit of waiting: An extra year to save for the tax bill, plus you keep that tax money invested longer.

How to avoid it: Unless you need the cash immediately, wait until January to sell year-end shares.

Trap 7: Losing Your Purchase Confirmations

The mistake: You throw away (or ignore) the purchase confirmations from your ESPP administrator.

The problem: Three years later, you sell those shares. Your brokerage 1099-B shows the wrong basis. You have no proof of what you actually paid.

The cost: Without documentation, the IRS can assume your basis is zero. That means you pay capital gains tax on the entire sale amount, not just your gain.

How to avoid it: Save every purchase confirmation email or statement. Create a folder called "ESPP Purchases" and file them by year. You'll need them when you sell.

Why HR can't warn you: Your benefits team can explain how the plan works. They can't tell you how to report it on your taxes or which mistakes to avoid. That's considered tax advice, and they're not allowed to give it.

Think of these traps like potholes on a dark road. Now that you know where they are, you can steer around them.

But knowing the traps is only half the battle. The bigger question: Should you even try for a qualifying disposition, or is selling early actually smarter? The math might surprise you.

Should You Hold for Qualifying Disposition? The Math Behind the Decision

You know qualifying dispositions save taxes. But is the savings worth the risk of holding your company's stock for 1-2 years?

Think of it like insurance. Selling immediately costs more in taxes, but it protects you from the risk of your stock tanking. Holding saves on taxes, but you're betting your company's stock won't drop more than you save.

The Tax Savings Are Usually Small

Here's what most people don't realize: qualifying disposition tax savings are typically just 5-10% of your sale proceeds.

Real example: You bought $10,000 of ESPP shares (100 shares at $85, FMV $100).

- Disqualifying sale tax (sell now): $600

- Qualifying sale tax (hold 18+ months): $510

- Your tax savings: $90

That's it. You save $90 by holding for 18 more months.

Now Add the Stock Price Risk

Let's say you hold those shares. The stock is trading at $110 when you buy. Eighteen months later, you finally hit the qualifying period.

If the stock drops from $110 to $95, you lose $1,500 in value (100 shares x $15 drop). Your $90 tax savings just cost you $1,500.

The break-even question: How much can your stock drop before the tax savings disappear?

In this example, the stock only needs to drop 0.9% ($110 to $109) to wipe out your $90 tax benefit. If your company's stock regularly swings 10-20%, you're taking huge risk for tiny savings.

The Concentration Risk Problem

You probably already own too much company stock:

- ESPP shares you're holding

- Unvested RSUs

- Maybe company stock in your 401k

- Your paycheck depends on this company too

That's a lot of eggs in one basket. If your company hits trouble, you lose on multiple fronts at once.

Most financial advisors recommend selling ESPP shares immediately, even with the tax hit. The diversification is worth more than the tax savings.

When Holding Actually Makes Sense

Holding for qualifying treatment works better if:

- Your company is stable. Think utility companies or boring, profitable businesses that don't swing wildly.

- Your ESPP position is small. You're holding $5,000, not $50,000.

- You're diversified otherwise. No RSUs, no company 401k stock, secure job.

- You're in a high tax bracket. The higher your bracket, the more you save from qualifying treatment.

A Simple Decision Framework

Sell immediately if:

- Stock is volatile (regular 10%+ swings)

- You already own company stock (RSUs, 401k)

- You need the money soon

- You're not confident in the company's future

Consider holding if:

- Stock is stable (moves less than 5% typically)

- Your ESPP position is tiny compared to your net worth

- You're well diversified in other investments

- You're in the 32%+ tax bracket (bigger savings)

The Bottom Line

For most people, the tax savings from qualifying disposition don't justify the concentration risk. You're saving $90 to risk losing $1,500.

The math works differently if you're holding $50,000 in ESPP shares (saving $450-500 in taxes). But then your concentration risk is even worse.

A balanced approach: Sell most shares immediately. If you want to gamble on qualifying treatment, hold a small portion you can afford to lose.

Now that you understand the hold-or-sell decision, let's talk about what to do right now to manage your ESPP taxes effectively.

What to Do Right Now: Your ESPP Tax Action Plan

You've learned the rules. Now let's build your ESPP command center. Think of this like setting up a home filing system. It takes a couple hours upfront, but it saves you from tax-season panic later.

Here's your action plan, organized by when you need to do it.

Do This Today (Takes 30 Minutes)

Step 1: Find your ESPP purchase confirmations

Log into your stock plan account (Fidelity, E*TRADE, Schwab, or wherever your company holds shares). Download every purchase confirmation you can find. Save them in a folder labeled "ESPP Taxes."

Step 2: Check if you sold shares this year

If yes, you need to act fast. Your tax bill is coming. If no, you're just setting up for the future.

Do This Month (Takes 2 Hours)

Step 3: Create your tracking spreadsheet

Open a simple spreadsheet. Create columns for:

- Offering date

- Purchase date

- Number of shares

- Purchase price per share

- FMV at purchase

- FMV at offering (if different)

- Date sold (leave blank for now)

- Sale price (leave blank for now)

Fill in what you know. This is your tax roadmap.

Step 4: Decide your sell strategy

Read our "Should You Hold for Qualifying Disposition?" section again. Pick a plan: sell immediately, hold for qualifying, or something in between. Write it down. Having a strategy stops you from making emotional decisions later.

Do This Before Year-End (If You Sold Shares)

Step 5: Calculate your estimated tax

Here's a real example. You sold 100 ESPP shares 6 months after purchase:

- Purchase price:

$85per share - FMV at purchase:

$100per share - Your discount:

$15per share =$1,500total - Your tax bracket: 24%

- Ordinary income tax owed:

$1,500 × 0.24 = $360 - You also sold at

$110, so short-term capital gain:$10per share =$1,000 - Capital gains tax:

$1,000 × 0.24 = $240 - Total tax owed:

$360 + $240 = $600

Step 6: Make estimated tax payment if needed

If you owe $1,000 or more in taxes on ESPP sales, the IRS wants quarterly estimated payments. Download Form 1040-ES from IRS.gov. It has a worksheet and payment vouchers. You can also pay online at irs.gov/payments.

Quarterly deadlines:

- January to March sales: Pay by April 15

- April to May sales: Pay by June 15

- June to August sales: Pay by September 15

- September to December sales: Pay by January 15

Skip this if your employer withheld enough tax or you owe less than $1,000.

Do This During Tax Season

Step 7: Collect your tax forms

You'll receive:

- W-2 from your employer (shows ESPP discount as income in Box 1)

- 1099-B from your brokerage (shows stock sales)

Get them by early February. Check that the numbers match your records. If your W-2 is missing the ESPP discount or your 1099-B shows the wrong purchase price, call HR or your brokerage immediately.

Step 8: Decide if you need help

Consider hiring a tax professional if:

- You made multiple ESPP sales with different holding periods

- You moved states during the year

- You have ISOs or RSUs on top of ESPP

- Your 1099-B shows a different cost basis than you calculated

- You're just overwhelmed and want peace of mind

A good CPA costs $300 to $800 for a return with equity compensation. That's cheap compared to getting it wrong.

Set Up for Next Year (Takes 1 Hour)

Step 9: Set calendar reminders

For each ESPP purchase, set two phone reminders:

- One year from purchase date (qualifying disposition eligible)

- Two years from offering date (full qualifying disposition eligible)

Label them clearly: "ESPP from March 2024 offering now eligible for qualifying sale."

Step 10: Review concentration risk quarterly

Put a recurring calendar event every 3 months: "Check ESPP position size." If your company stock is more than 10% of your total investments, consider selling some. Diversification protects you if your company hits trouble.

Your Situation-Specific Next Steps

If you already sold shares this year:

- Pull your purchase confirmation (10 minutes)

- Note the FMV at purchase from the confirmation

- Estimate your ordinary income tax: discount amount × your tax rate (5 minutes)

- Calculate if you owe

$1,000+in tax on this sale - If yes, make estimated tax payment by next quarterly deadline (30 minutes)

- Download Form 1040-ES and calculate payment (20 minutes)

- Set up tracking spreadsheet for future purchases (30 minutes)

Total time: about 2 hours to get fully organized.

If you're planning to sell soon:

- Create your tracking spreadsheet first (30 minutes)

- Calculate the tax difference between selling now vs. waiting for qualifying (20 minutes)

- Decide based on the math, not your gut (5 minutes)

- Set a calendar reminder for when you'll execute the sale (2 minutes)

If you just bought shares:

- Download and save your purchase confirmation today (5 minutes)

- Add the details to your tracking spreadsheet (10 minutes)

- Set calendar reminders for qualifying dates (5 minutes)

- Relax. You have time to plan.

You've Got This

ESPP taxes feel complicated because they are. But you just learned more than 90% of ESPP participants ever will. You know the difference between qualifying and disqualifying sales. You know what forms to expect. You know how to calculate what you'll owe.

The tracking system you set up today saves you hours of stress later. It turns tax season from a scramble into a simple box-checking exercise.

Want to learn more? Check out our ESPP Strategy Guide for help deciding when to sell. Or read our Tax-Loss Harvesting article to learn how to offset ESPP gains with losses from other investments.

The most important thing? Take action today. Even 30 minutes of setup right now puts you ahead of almost everyone else with ESPP shares.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

How ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

TaxThe ISO AMT Trap: How Exercising Stock Options Can Cost You Thousands in Unexpected Taxes

The ISO AMT trap catches thousands of employees off guard every year. When you exercise incentive stock options, you might owe Alternative Minimum Tax on paper gains you haven't actually received - sometimes tens or hundreds of thousands of dollars. This guide explains exactly how the trap works and how to avoid it.

Not sure what to do with your equity?

Get a free personalized analysis