How ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

Everything you need to know about buying company stock at a discount

Published March 14, 2026 · Updated March 14, 2026

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

The ESPP Opportunity: Why Companies Let You Buy Stock at a Discount

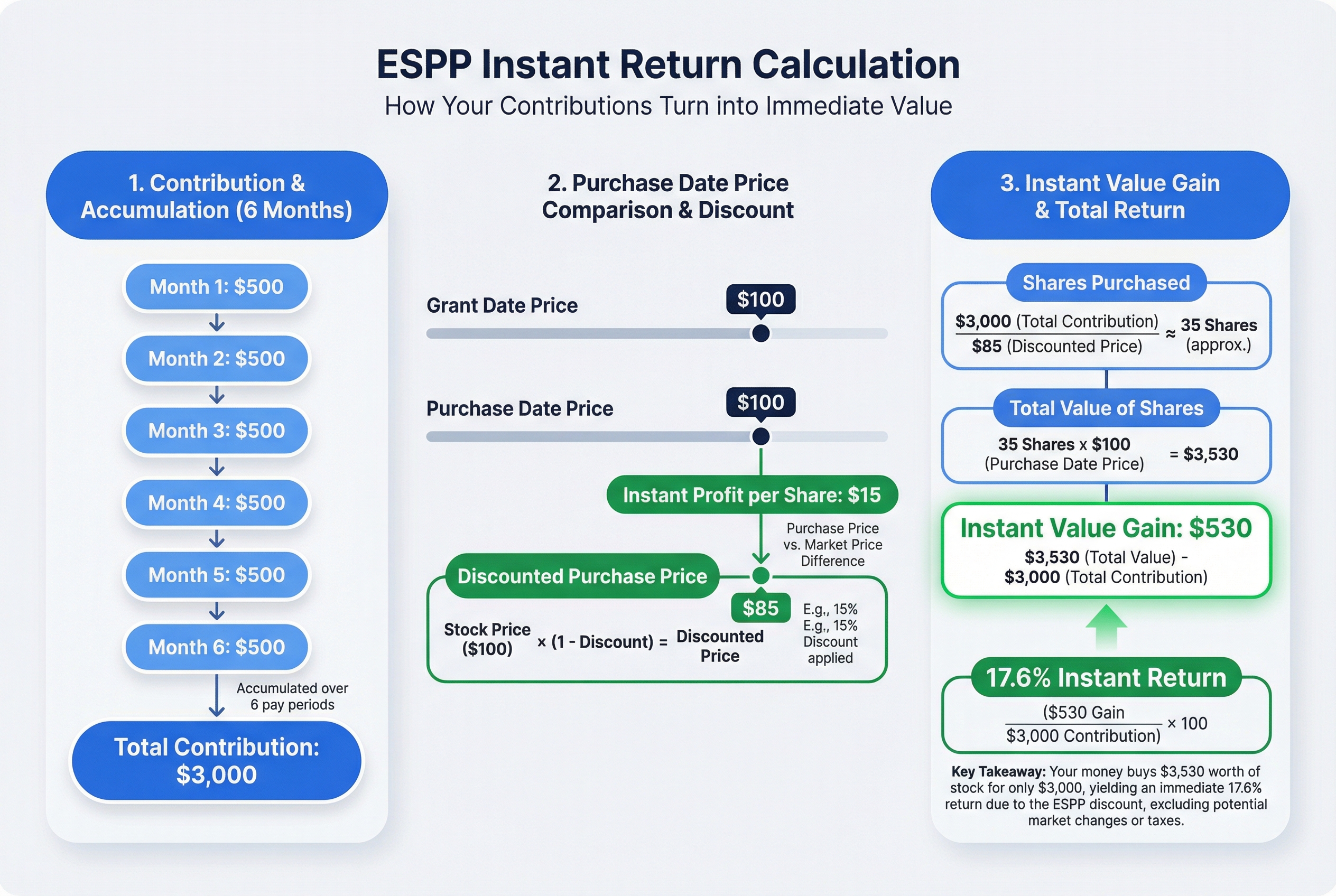

Imagine your company's stock trades at $100, but you can buy it for $85. That's an instant $15 profit on every share, no guessing or waiting required.

That's exactly how an Employee Stock Purchase Plan (ESPP) works. Your company lets you buy its stock at a discount, typically 10% to 15% off the market price. It's like having a members-only coupon that never expires.

Here's a real example. Sarah works at TechCo where stock trades at $100. Her ESPP offers a 15% discount. She contributes $500 per paycheck for 6 months, totaling $3,000. On purchase date, she buys shares at $85 each, getting 35.3 shares worth $3,530. That's $530 in instant value, a 17.6% return on her money.

Why do companies offer this deal? Three main reasons:

- Keep good employees around. You're more likely to stay when you own a piece of the company.

- Build ownership culture. Employee-owners think differently about company success.

- Compete for talent. Top companies offer ESPPs alongside other benefits.

Think of ESPP as a different animal from RSUs or stock options. RSUs are free shares you earn over time. Stock options give you the right to buy at a set price. ESPP lets you buy at a discount using your own money, but you control when and how much.

The basic math is simple: invest $10,000 through your ESPP with a 15% discount, and you immediately own $11,765 worth of stock. That's guaranteed profit the moment you buy.

Now let's look at exactly how your money moves from your paycheck into stock ownership.

Employee Stock Purchase Plan (ESPP): What It Is and How It Works?

The immediate value created by a typical 15% ESPP discount.

The immediate value created by a typical 15% ESPP discount.

The ESPP Timeline: How Money Moves from Your Paycheck to Stock Ownership

Think of ESPP like a layaway plan at a store, but with a twist. Instead of paying full price at the end, you get a discount. And if the price went up while you were saving, you might get to pay the old, lower price instead.

Here's how the money flows from your paycheck to stock in your account.

The Offering Period: Your 6-Month Savings Window

Most ESPPs work in 6-month cycles called offering periods. Some companies use 12-month periods, but 6 months is standard.

Let's say your company's offering period runs January 1 through June 30. On January 1, you enroll and choose to contribute $200 per paycheck. That's your enrollment date, also called the offering date.

Every paycheck for the next six months, your company takes $200 from your after-tax pay and holds it in a special account. If you get paid every two weeks, that's 13 paychecks. Your contributions add up to $2,600 by June 30.

Purchase Date: When Your Cash Becomes Stock

June 30 is your purchase date. This is when your company takes your $2,600 and buys stock with it.

But here's where it gets good. Most ESPPs have a lookback provision. This means you get to buy at the lower of two prices: the stock price on January 1 (enrollment date) or June 30 (purchase date). Then you get your 15% discount on top of that.

Real example: Your company stock is $80 on January 1. By June 30, it climbs to $100. With the lookback provision, you buy at $80 (the lower price). Apply the 15% discount: $80 x 0.85 = $68 per share.

Your $2,600 buys 38.2 shares ($2,600 / $68). Those shares are worth $3,820 on purchase date (38.2 shares x $100). That's $1,220 profit, a 47% return in just 6 months.

What If the Stock Price Drops?

The lookback provision protects you here too. If the stock drops from $80 to $60, you buy at $60 (the lower price). With your 15% discount, you pay $51 per share. Your $2,600 buys 51 shares worth $3,060. Still a $460 profit.

Purchase Periods vs. Offering Periods

Some companies split offering periods into multiple purchase periods. For example, a 12-month offering period might have two 6-month purchase periods.

This means you buy stock twice during one offering period. The lookback provision typically looks back to the start of the full offering period, not just the purchase period. This can create even bigger discounts if the stock keeps climbing.

Now that you understand the timeline, let's look at the rules for getting started.

Enrolling in Your ESPP: Contribution Limits and Eligibility Rules

Think of ESPP contribution limits like a highway with two speed limits. The IRS sets a federal limit ($25,000 per year). Your company sets its own limit (usually 10-15% of your salary). You can't exceed either one.

The IRS Annual Limit: $25,000

The IRS caps how much stock you can purchase through ESPP at $25,000 worth per calendar year. This is measured by the stock's fair market value, not what you pay.

Here's what this means: If your company offers a 15% discount and you contribute the maximum, you're actually buying $29,412 worth of stock for $25,000. The IRS limit applies to the full $29,412 value, not your $25,000 contribution.

Most employees never hit this limit. You'd need to earn at least $166,667 annually (contributing 15%) to bump against it.

Your Company's Percentage Limit

Your employer sets a second limit, usually 10-15% of your base salary. This is the real constraint for most people.

Example: Marcus earns $130,000 annually. His company allows 15% contributions.

- Maximum annual contribution: $130,000 × 15% = $19,500

- Monthly paycheck deduction: $19,500 ÷ 12 = $1,625

- With 15% discount, he buys: $19,500 ÷ 0.85 = $22,941 worth of stock

- Instant gain: $22,941 - $19,500 = $3,441

Marcus stays well under the $25,000 IRS limit. His take-home pay drops by $1,625 per month, though the actual impact is less because ESPP contributions reduce his taxable income.

Calculating Your Personal Maximum

Use this simple formula:

Your annual salary × Company percentage limit = Maximum annual contribution

If that number divided by 0.85 (assuming 15% discount) exceeds $25,000, the IRS limit applies. Otherwise, use your company's percentage.

Common Eligibility Requirements

Most companies require:

- Minimum employment period: Usually 30-90 days after your hire date

- Work hours: Typically 20+ hours per week (no part-time employees)

- Employee status: W-2 employees only (contractors don't qualify)

- No ownership restrictions: You can't own more than 5% of company stock

Some companies exclude highly compensated employees or executives. Check your plan documents.

When You Can Enroll or Change Contributions

ESPPs run on offering periods (usually 6 months). You can typically:

- Enroll: During open enrollment windows, often twice yearly

- Change contributions: At the start of each new offering period

- Stop contributions: Usually anytime, but you might forfeit the current period

Miss the enrollment window? You're stuck waiting 6 months for the next one.

Should You Contribute the Maximum?

Here's a quick decision guide:

Contribute the max if:

- You have 3-6 months emergency savings

- You're contributing enough to get full 401(k) match

- You can afford the paycheck reduction

Start smaller if:

- You're living paycheck to paycheck

- You have high-interest debt (credit cards over 15%)

- You're not maxing your 401(k) match yet

The ESPP discount is guaranteed money, but only if you can afford to tie up cash for 6 months.

ESPP and Your 401(k): Can You Do Both?

Yes. These are separate limits. Maxing out your 401(k) ($23,000 in 2024) doesn't affect your ESPP contributions.

Example: Sarah earns $150,000 and contributes:

- 401(k): $23,000 annually ($1,917/month)

- ESPP: 15% of salary = $22,500 annually ($1,875/month)

- Total paycheck reduction: $3,792/month

This is aggressive but legal. Just make sure your budget can handle it.

Now that you know how much you can contribute and when to enroll, let's look at what type of ESPP plan you actually have.

The Two Types of ESPP Plans: Section 423 vs. Non-Qualified Plans

Not all ESPPs are created equal. Your company offers one of two types: a Section 423 qualified plan or a non-qualified plan. The difference affects how much you pay in taxes.

Think of Section 423 plans like flying with TSA PreCheck. You follow special IRS rules, but you get better treatment. Non-qualified plans are like regular security. Simpler rules, but fewer benefits.

What Makes a Section 423 Plan Special

Section 423 plans are named after the IRS tax code that created them. These plans must follow strict rules:

- Every employee gets the same deal (same discount, same rules)

- Maximum 15% discount off the stock price

- Cannot buy more than $25,000 worth of stock per year

- Must hold shares at least one year from purchase AND two years from enrollment to get the best tax treatment

The big advantage: If you hold your shares long enough, most of your profit gets taxed at lower long-term capital gains rates instead of ordinary income rates.

About 95% of public companies use Section 423 plans. Why? The tax benefits help attract and keep employees.

Non-Qualified Plans: The Simpler Alternative

Non-qualified plans don't follow Section 423 rules. Companies can offer bigger discounts or different terms to different employees. But you lose the special tax treatment.

Here's the money difference: You buy $10,000 worth of stock for $8,500 (15% discount). That's $1,500 in savings.

- Section 423 plan: Hold two years. Pay long-term capital gains (15-20%) on most of the profit.

- Non-qualified plan: The $1,500 discount gets taxed as ordinary income immediately. If you're in the 24% tax bracket, that's $360 in extra taxes right away.

How to Identify Your Plan Type

Check your ESPP enrollment documents or Summary Plan Description. Look for phrases like "qualified under Section 423" or "tax-qualified plan." These mean you have a Section 423 plan.

You can also ask your HR or benefits team directly: "Is our ESPP a Section 423 qualified plan?"

Knowing your plan type matters because it determines when and how you'll pay taxes on your discount and profits.

How Does An Employee Stock Purchase Plan Work? | Money Unscripted | Fidelity Investments

Holding Periods and Tax Treatment: Qualifying vs. Disqualifying Dispositions

The IRS rewards patience. Hold your ESPP shares long enough, and you pay less tax. Sell too soon, and you pay more.

Think of holding periods like aging cheese. Wait longer and you get better tax treatment. But unlike cheese, the exact aging time matters a lot.

The Two Holding Period Rules

For a qualifying disposition (better tax treatment), you must satisfy BOTH rules:

- Hold shares at least 2 years from the offering date (when the offering period started)

- Hold shares at least 1 year from the purchase date (when you bought them)

Miss either deadline and you have a disqualifying disposition (worse tax treatment).

Let's use real dates. Your offering period starts January 1, 2024. You purchase shares on June 30, 2024.

For qualifying disposition, you must hold until:

- January 1, 2026 (2 years from offering start), AND

- June 30, 2025 (1 year from purchase)

Since January 1, 2026 comes later, that's your target date.

How Each Sale Gets Taxed

Here's where it gets interesting. The IRS taxes your discount and your gains differently.

Disqualifying Disposition (sell early):

- Your discount gets taxed as ordinary income (same rate as your salary)

- Any additional gain gets taxed as short-term capital gains (also ordinary income rates)

Qualifying Disposition (hold long enough):

- Your discount still gets taxed as ordinary income

- Any additional gain gets taxed as long-term capital gains (lower rates, usually 15%)

Real Dollar Comparison

You purchase 100 shares on June 30, 2024 at $85 each ($8,500 total). The market price was $100, so you got a 15% discount. Later, the stock hits $120.

Disqualifying Sale (sell July 2024, one month later):

- Ordinary income from discount:

$1,500($15 x 100 shares) - Short-term capital gain:

$2,000($20 x 100 shares) - Total tax at 24% bracket:

$840 - After-tax profit: $2,660

Qualifying Sale (sell July 2026, after both holding periods):

- Ordinary income from discount:

$1,500($15 x 100 shares) - Long-term capital gain:

$2,000($20 x 100 shares) - Tax: $360 (discount) + $300 (gain at 15%):

$660 - After-tax profit: $2,840

Waiting saves you $180 in this example. That's real money for doing nothing but waiting.

Quick Decision Guide

Sell immediately if:

- You need the cash now

- The stock feels risky

- Your profit is small enough that tax savings don't matter

Hold for qualifying disposition if:

- You can afford to wait

- You believe in the company's future

- The tax savings justify the risk

The next section shows exactly which tax forms report these transactions and how to read them.

ESPP Tax Forms and Reporting: Understanding Forms 3922, W-2, and 1099-B

Tax forms are like receipts for your ESPP. Each one tells part of the story. Your employer and broker send you different forms at different times. You need all of them to report your taxes correctly.

Form 3922: Your ESPP Purchase Receipt

You get Form 3922 every time you buy ESPP shares. It arrives in January for the previous year's purchases.

What Form 3922 shows:

- Box 1: Grant date (when the offering period started)

- Box 2: Purchase date (when you actually bought shares)

- Box 3: Fair market value on purchase date

- Box 4: Your purchase price (the discounted price you paid)

- Box 5: Number of shares you bought

Think of Form 3922 as your discount receipt. Box 3 minus Box 4 shows your discount per share. This becomes important later when you sell.

Example: Your Form 3922 shows grant date 1/1/24, purchase date 6/30/24, FMV $100, purchase price $85, and 100 shares. Your discount is $15 per share or $1,500 total.

Form W-2: Where Disqualifying Sales Appear

If you sell ESPP shares before meeting the holding periods, your discount becomes ordinary income. This shows up on your W-2 in Box 1 (wages).

Your employer adds this income to your regular paycheck. It happens automatically. You don't get a choice.

Using our example: You sell those 100 shares on 9/15/24 at $110 (a disqualifying disposition). Your employer adds $1,500 to Box 1 of your W-2. You already paid tax on this through paycheck withholding.

Important: Your W-2 only shows income from disqualifying sales. Qualifying dispositions don't appear here.

Form 1099-B: Your Sale Receipt from the Broker

Form 1099-B comes from your broker (like E*TRADE or Fidelity). It reports every stock sale to the IRS.

The problem: Form 1099-B often gets the numbers wrong for ESPP.

What it shows:

- Box 1d: Sale proceeds (what you received)

- Box 1e: Cost basis (what the broker thinks you paid)

In our example, your 1099-B shows:

- Proceeds:

$11,000(100 shares ×$110) - Cost basis:

$10,000(100 shares ×$100)

Wait. That basis looks wrong. You only paid $85 per share, right?

Here's the trick: The broker adjusts your basis upward by the $1,500 already taxed on your W-2. This prevents double taxation. Your adjusted basis is $8,500 original cost + $1,500 W-2 income = $10,000.

Verifying Your Broker Got It Right

Brokers make mistakes. Check their math.

Your true basis formula:

- Start with what you paid (

$85× 100 shares =$8,500) - Add any amount on your W-2 from this sale (

$1,500) - Final basis:

$10,000

If your 1099-B shows a different basis, your broker messed up. Call them. Get a corrected 1099-B.

Reporting on Your Tax Return (Form 1040)

You report ESPP sales on Schedule D (Capital Gains and Losses).

For our example:

- Sale proceeds:

$11,000(from 1099-B) - Cost basis:

$10,000(from 1099-B, already adjusted) - Short-term capital gain:

$1,000

Your total tax bill covers two pieces:

$1,500ordinary income (already on W-2, already withheld)$1,000short-term capital gain (you report on Schedule D)

Common mistake: People see the $8,500 they paid and use that as basis. Wrong. You'll pay tax twice on the $1,500 discount.

Why You Might Owe More Than Expected

Your W-2 withholding covers the discount. It doesn't cover the additional gain.

In our example, you made $2,500 total profit ($110 sale price minus $85 purchase price, times 100 shares). The $1,500 discount was withheld from your paycheck. The extra $1,000 gain wasn't.

You owe capital gains tax on that $1,000. If you're in the 24% tax bracket, that's $240 due at tax time.

Your Tax Form Checklist

At purchase:

- Save Form 3922

- Note your discount per share

At sale (disqualifying):

- Check W-2 Box 1 for added income

- Get Form 1099-B from broker

- Verify basis = purchase price + W-2 amount

- Calculate remaining gain for Schedule D

At sale (qualifying):

- No W-2 adjustment

- Form 1099-B still arrives

- Entire gain goes on Schedule D (possibly as long-term)

The forms can feel overwhelming. But they're just documenting what already happened. Your real tax decisions happen when you choose to sell, not when you file the forms.

Next, we'll cover what happens to your ESPP when you leave your job, retire, or take a leave of absence.

What Your HR Won't Tell You: ESPP Rules for Termination, Retirement, and Leave

Your ESPP is like a gym membership - once you leave the company, the rules change immediately. Most plans cut you off fast, but what happens to your money depends on timing and your specific plan.

What Happens to Your Paycheck Contributions

You're laid off April 15. The offering period ends June 30. You've accumulated $2,400 from paycheck deductions.

Here's what typically happens:

Scenario A (Most Common): Your company returns $2,400 cash within 30-60 days. No purchase happens. You get your money back, but you miss out on the discount.

Scenario B (Less Common): The company completes the purchase on June 30. You get shares at the discounted price. This is rare but generous.

Scenario C (Very Rare): You can choose to continue through the purchase date even though you've left. Almost no companies offer this.

Check your plan document before you assume anything. Most plans return cash, which means you lose the discount opportunity.

Your Already-Purchased Shares Are Always Yours

Think of this like money in your savings account. Once ESPP shares hit your brokerage account, they're yours forever. The company can't take them back.

Getting fired doesn't change this. Quitting doesn't change this. Even getting walked out by security doesn't change this.

You keep every share you've already purchased, no matter how you leave.

Different Exit Scenarios, Different Rules

Termination (Fired or Laid Off): Contributions stop immediately. Most plans return accumulated cash within 60 days. Already-purchased shares remain yours.

Voluntary Resignation: Same as termination. You typically can't finish the offering period. Your $1,500 in accumulated contributions comes back as $1,500 cash, not discounted shares.

Retirement (Age 55+ or Company Definition): Some plans let you complete the current offering period. Others treat retirement like any termination. This varies wildly by company.

Medical or Family Leave: If you're on paid leave, contributions usually continue. Unpaid leave typically pauses your ESPP. You might restart when you return, but you lose that offering period.

Timing Strategies If You're Leaving

Know your offering period dates. If you're quitting voluntarily and the purchase date is two weeks away, waiting means you get discounted shares instead of cash back.

Example: You have $3,000 accumulated. Purchase date is May 15. You want to quit.

- Quit May 1: Get $3,000 cash back

- Quit May 16: Get shares worth $3,530 (assuming 15% discount)

That's a $530 difference for waiting two weeks.

Questions to Ask HR Before You Leave

- "Do I get my accumulated contributions back as cash or shares?"

- "How long until I receive my money or shares?"

- "Can I complete the current offering period after my last day?"

- "What happens if I'm on unpaid leave?"

- "Are retirement rules different from termination rules?"

Get answers in writing. HR might not know the details off the top of their head. Ask them to check the plan document.

Protecting Your Money

Your accumulated ESPP contributions aren't FDIC insured like a bank account. They're held by your company or a third party administrator.

If you're leaving, getting that money back quickly matters. Most companies process returns within 30-60 days, but some take 90 days.

Already-purchased shares sit in your brokerage account (E*TRADE, Fidelity, Schwab, etc.). Those are protected like any brokerage assets, separate from your employer.

Now that you know what happens when you leave, let's tackle a tax surprise that catches high earners off guard: the Alternative Minimum Tax.

ESPP and Alternative Minimum Tax: When Your Discount Creates an AMT Problem

Think of AMT (Alternative Minimum Tax) as a parallel tax universe. The IRS makes you calculate your taxes two ways, then pay whichever is higher. For most people, regular taxes win. But if you earn a high income and use lots of deductions, you might get pulled into the AMT universe instead.

Here's the problem: Your ESPP discount can push you into AMT territory.

How ESPP Triggers AMT

When you buy ESPP shares, the discount you receive becomes what's called an "AMT preference item." This means:

- Regular tax world: You don't pay tax on the discount until you sell

- AMT tax world: The discount gets added to your income immediately

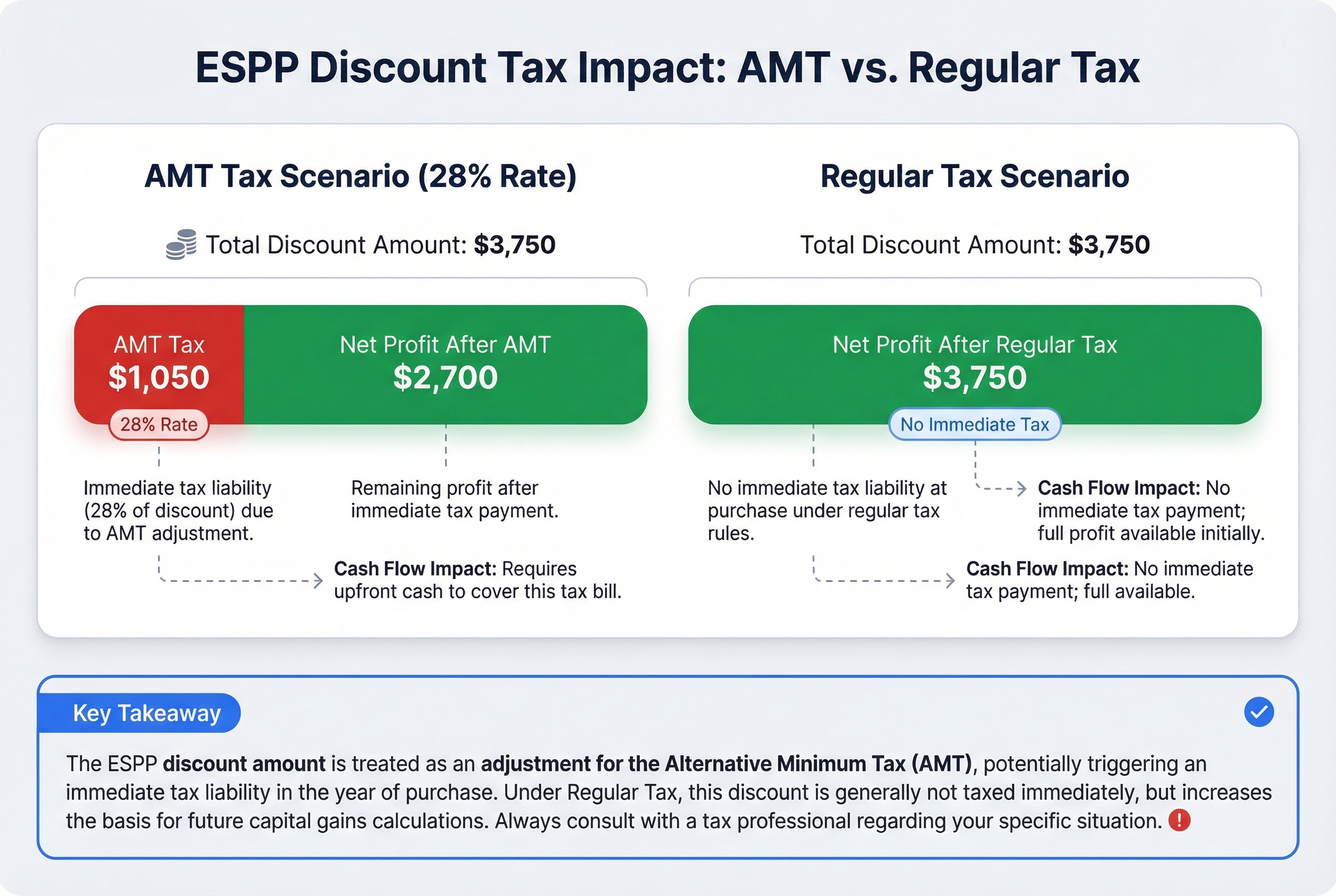

Let's make this real. You earn $200,000, live in California, and max out your ESPP. You purchase $25,000 worth of stock with a 15% discount, saving $3,750.

In regular tax world, you'd pay nothing now. In AMT world, that $3,750 gets added to your income today. If you're subject to AMT (which taxes at 28%), you pay an extra $1,050 immediately. You're still making money from the discount, but $1,050 less than you expected.

Should You Worry About AMT?

Most ESPP participants won't hit AMT. Here's a quick decision guide:

You probably DON'T need to worry if:

- You earn under $150,000 (single) or $200,000 (married)

- You live in a low-tax state

- You don't have large deductions or other preference items

You SHOULD check AMT if:

- You earn over $200,000

- You live in high-tax states (California, New York, New Jersey)

- You max out ESPP contributions ($25,000 purchase value)

- You exercise ISOs or have other AMT items

Real Numbers: When AMT Bites

Say you're a senior engineer in San Francisco earning $250,000. You participate in ESPP at the maximum level: $25,000 purchase with 15% discount = $3,750 discount.

You also have:

- High state income taxes (California)

- Property tax deductions

- ISO exercises from previous years

These factors combined push you into AMT. That $3,750 ESPP discount now costs you $1,050 in immediate taxes (28% AMT rate). You still profit $2,700, but it's a smaller win than the full $3,750 you expected.

How to Minimize AMT Impact

You have a few options:

-

Reduce ESPP contribution percentage. Instead of maxing out at 15% of salary, drop to 10%. Smaller discount = smaller AMT adjustment.

-

Sell immediately at vest. If you're going to pay tax on the discount anyway through AMT, selling right away locks in your profit without additional market risk.

-

Time other deductions carefully. If you control when you exercise ISOs or take other deductions, spread them across tax years to avoid AMT spikes.

The Bottom Line on AMT

Here's what matters: AMT doesn't make ESPP unprofitable. It just reduces your immediate benefit. You're still buying stock at a discount. You're still making money.

The math: Even with AMT, a 15% discount minus 28% AMT on that discount still leaves you 10.8% ahead instantly. That's better than any savings account.

When to Get Professional Help

Talk to a tax professional if:

- Your household income exceeds $200,000

- You're maxing out ESPP contributions

- You exercise ISOs or have other AMT preference items

- You live in a high-tax state

- You want to optimize your total tax picture

A CPA who specializes in equity compensation can run the numbers and show you exactly how AMT affects your situation. They might find the $300-500 consultation fee saves you thousands in taxes.

Now that you understand the tax implications, let's talk about the most important question: when should you actually sell your ESPP shares to maximize your after-tax profit?

Net profit realized by immediately selling shares to lock in the discount.

Net profit realized by immediately selling shares to lock in the discount.

ESPP Selling Strategies: When to Sell for Maximum After-Tax Profit

You bought stock at a discount. Great! Now comes the hard part: deciding when to sell.

Choosing when to sell ESPP shares is like choosing when to harvest crops. Wait too long and bad weather might destroy value. Harvest too early and you miss potential growth. There's no perfect answer, but there are three main strategies.

Strategy 1: Sell Immediately (Lock In Your Discount)

Sell your ESPP shares the day they hit your account. You keep the discount, pay ordinary income tax on it, and walk away with guaranteed profit.

Example: You spend $8,500 to buy shares worth $10,000. You sell immediately and pocket $1,500. After paying $360 in taxes (24% bracket), you keep $1,140 in pure profit. Zero risk.

This strategy treats your ESPP like a bonus program. You get your discount, you cash out, you move on. No guessing about stock prices.

Strategy 2: Hold for Qualifying Disposition (Tax Savings)

Hold your shares for 18+ months to get better tax treatment. You pay less tax on the discount, but you take on stock price risk.

Same example, different outcome: You hold 18 months and the stock drops to $95 per share. You keep your $1,500 discount minus $300 in taxes (better rate), but you lose $500 when the stock price falls. Total profit: $700. You saved $60 in taxes but lost $440 overall.

Or this happens: The stock rises to $115. You keep $1,500 minus $300 tax, plus you gain $1,500 from price growth. Total profit: $2,700. Now the wait paid off.

Strategy 3: Hold Even Longer (Maximum Growth Potential)

Some people hold ESPP shares for years, betting on long-term growth. More potential upside, more potential downside.

This only makes sense if you believe strongly in your company's future AND you can handle the risk.

The Risk You Must Understand: Concentration

Here's the danger: your paycheck, your health insurance, and your ESPP shares all depend on one company. If that company struggles, you lose on multiple fronts.

The rule: Don't let ESPP shares become more than 10% of your total investments. If they creep above that, sell some. This protects you from putting too many eggs in one basket.

How to Decide Your Strategy

Sell immediately if:

- You need the money soon

- ESPP shares are over 10% of your portfolio

- You're uncomfortable with stock market risk

- Your company's stock is volatile

Hold for qualifying disposition if:

- You can afford to wait 18 months

- Your company is stable

- The tax savings matter to you

- You're under the 10% concentration limit

Hold longer if:

- You believe strongly in your company's growth

- You have plenty of other diversified investments

- You can stomach potential losses

- You're investing for long-term goals

Most financial advisors recommend selling immediately or soon after. The guaranteed profit beats the gamble of holding for most people.

Now that you know when to sell, let's look at the mistakes that cost people thousands in ESPP programs.

Should I Participate in My Company’s Employee Stock Purchase Plan (ESPP)?

Common ESPP Mistakes and How to Avoid Them

ESPP mistakes are like leaving money on the table at a restaurant. You earned it, but you walked away without it.

Most ESPP errors cost real money. Here are the biggest ones and how to avoid them.

Mistake 1: Not Participating at All

The cost: Huge. If your ESPP offers a 15% discount, you're turning down an instant 17.6% return on every dollar you contribute.

Let's say you could contribute $100 per paycheck for 26 paychecks. That's $2,600 per year. With a 15% discount, you buy $3,059 worth of stock. You just left $459 on the table.

How to avoid it: Contribute something, even if it's just 1% of your paycheck. Some discount is better than zero discount.

Mistake 2: Selling During the Wrong Holding Period

This is the most expensive tax mistake.

Example: Sarah sells ESPP shares 11 months after purchase, thinking she met the holding period. Actually, she needs 1 year from purchase AND 2 years from the offering start. Her sale is disqualifying.

The cost: Her $1,500 discount gets taxed at 32% ordinary rate instead of 15% long-term capital gains rate. Extra tax: $255. She could have avoided this by waiting one more month.

How to avoid it: Mark your calendar with two dates for every ESPP purchase:

- 1 year from purchase date

- 2 years from offering period start date

Don't sell before BOTH dates pass.

Mistake 3: Forgetting to Track Your Cost Basis

Your W-2 already includes the discount as income. If you don't adjust your cost basis when you sell, you pay taxes on that discount twice.

Example: You buy 100 shares at $85 (15% discount from $100). Your W-2 shows the $1,500 discount as income. You already paid tax on it.

When you sell at $110, your gain is $2,500 ($11,000 minus $8,500). But if you forget to adjust your basis, your broker's 1099-B might show a $3,500 gain ($11,000 minus $7,500). You overpay taxes on $1,000.

How to avoid it: Keep a spreadsheet with these columns for every ESPP purchase:

- Purchase date

- Shares bought

- Price paid per share

- Fair market value on purchase date

- Discount amount (already taxed)

Mistake 4: Over-Contributing and Hitting the $25,000 Limit

The IRS caps ESPP purchases at $25,000 per year (based on fair market value). If you contribute too much, your company refunds the excess. You lose the discount on that money.

Example: You set your contribution to max out at $25,000. But your stock price drops during the offering period. You actually need less in contributions to hit the cap. Your paycheck deductions continue anyway. You tie up extra cash for months with no benefit.

How to avoid it: Check your ESPP balance mid-year. Adjust contributions if needed. Don't set it and forget it.

Mistake 5: Concentration Risk (Too Much Company Stock)

Your paycheck already depends on your company. If you hold too much ESPP stock, your wealth does too.

The danger: If your company hits trouble, you could lose your job AND watch your stock value crash at the same time.

How to avoid it: Financial advisors suggest keeping company stock to 10-15% of your total investments. Consider selling ESPP shares soon after purchase to lock in the discount and diversify.

Mistake 6: Ignoring Form 3922

Form 3922 tells you the key dates and prices for your ESPP purchase. Without it, you can't calculate your taxes correctly.

Many people file it away and forget about it. Then at tax time, they can't figure out their holding period or cost basis.

How to avoid it: When you get Form 3922, immediately add the information to your tracking spreadsheet. Don't wait until April.

Your ESPP Mistake Prevention Checklist

Before you enroll:

- Confirm you can afford the paycheck reduction

- Understand your plan's holding period rules

- Know the offering period dates

During the offering period:

- Monitor your contribution total

- Check if you're approaching the $25,000 cap

- Review your overall company stock exposure

After purchase:

- Save Form 3922 immediately

- Record cost basis in your spreadsheet

- Mark holding period end dates on your calendar

- Plan your selling strategy

At tax time:

- Verify your W-2 includes the discount

- Adjust cost basis on your tax return

- Keep all ESPP documents for 7 years

The good news? All these mistakes are preventable. You just need a system.

Now let's put everything together with a clear action plan you can start today.

Your ESPP Action Plan: What to Do Right Now

Think of this action plan like a choose-your-own-adventure book. Your next steps depend on where you are in your ESPP journey.

If You're Not Enrolled Yet

Do this week:

-

Find your ESPP plan document. Check your benefits portal or email HR. You need the discount percentage, lookback period, and contribution limits.

-

Calculate your maximum contribution. Take your salary and multiply by 10%. Example: $120,000 salary x 10% = $12,000 per year = $1,000 per month. That's your legal limit.

-

Check the next enrollment date. Most companies open enrollment twice a year (January 1 or July 1). Mark it on your calendar.

-

Decide your contribution amount. Start with 5% if you're unsure. You can always increase later.

-

Set up automatic contributions. Log into your payroll system and elect your percentage. The deductions start next offering period.

Example: Sarah earns $80,000. She contributes 10% ($667/month). With a 15% discount and lookback, she could gain $1,500 to $3,000 per year. That's free money for clicking a few buttons.

If You're Currently Participating

Track these details in a spreadsheet:

- Offering start date

- Purchase date

- Number of shares purchased

- Purchase price per share

- Fair market value on purchase date

- Total contribution amount

You need this information for taxes. Your broker statement might not show everything.

Do this today:

-

Add purchase dates to your calendar. Set a reminder for one week after each purchase date.

-

Decide your selling strategy now. Will you sell immediately? Hold for qualifying disposition? Don't wait until purchase day to decide.

-

Review your contribution percentage. Can you afford to contribute more? Are you hitting the $25,000 annual limit?

If You're Ready to Sell Shares

Before you click "sell":

-

Check your purchase date. Count the days you've held the shares. This determines your tax treatment.

-

Find your cost basis. For immediate sales, it's the fair market value on purchase date (already taxed). For qualifying dispositions, it's your actual purchase price.

-

Calculate your gain. Current price minus cost basis = taxable gain.

-

Understand which tax forms you'll get. Immediate sale = W-2 income. Qualifying disposition after two years = mostly capital gains on 1099-B.

-

Consider selling in batches. You don't have to sell everything at once. Spread sales across tax years if it helps.

Information Gathering Checklist

Documents you need:

- ESPP plan document (official rules)

- Benefits portal login

- Brokerage account login (where shares are held)

- Last year's W-2 (shows ESPP income)

- Form 3922 from each purchase (shows discount amount)

- Paystub showing ESPP deductions

Numbers you need to know:

- Your discount percentage (usually 15%)

- Lookback provision (yes or no?)

- Offering period length (6 months or 12 months?)

- Your current contribution percentage

- Next enrollment deadline

- Next purchase date

Questions to Ask HR or Your Benefits Team

About plan rules:

- "Does our ESPP have a lookback provision?"

- "What happens to my contributions if I leave the company mid-period?"

- "Can I change my contribution percentage during an offering period?"

- "Where do I find my Form 3922 after each purchase?"

About your situation:

- "I'm going on parental leave. Can I stay enrolled?"

- "I just got promoted. Does my new salary change my contribution limits?"

- "Can I contribute to the ESPP and max out my 401(k) in the same year?"

What to Track Going Forward

Create a simple spreadsheet with these columns:

- Purchase date

- Shares purchased

- Purchase price

- FMV on purchase date

- Contribution amount

- Discount received

- Sale date (when you sell)

- Sale price (when you sell)

- Holding period (days held)

This spreadsheet becomes your tax cheat sheet. When you sell shares three years from now, you'll know exactly what you paid and how long you held them.

Example tracking: On July 1, 2024, you bought 50 shares at $80 (15% discount). FMV was $94.12. You contributed $4,000. Your discount was $706. Write it down immediately.

When to Review Your ESPP Strategy

Quarterly check-in (15 minutes):

- Review your contribution percentage. Can you increase it?

- Check your stock's performance. Any major changes?

- Confirm next purchase date is on your calendar.

After each purchase (30 minutes):

- Record purchase details in your spreadsheet.

- Decide whether to sell immediately or hold.

- If selling, place the trade within one week.

- Update your tracking spreadsheet.

Annual review (1 hour):

- Calculate total ESPP gains for the year.

- Review tax forms (W-2, 3922, 1099-B).

- Reassess your selling strategy. Is immediate sale still right?

- Check if you're approaching the $25,000 annual limit.

- Adjust next year's contribution if needed.

Where to Get Help

For plan-specific questions: Your HR benefits team knows your company's ESPP rules. They can't give tax advice, but they can explain how your plan works.

For tax questions: Talk to a CPA or tax advisor familiar with equity compensation. The $200 to $500 you spend could save you thousands in taxes.

For selling strategy: A fee-only financial advisor can help you decide when to sell and how ESPP fits your overall finances. Avoid advisors who charge based on assets (they might push you to hold when selling makes sense).

Online resources: Your brokerage (E*TRADE, Fidelity, Morgan Stanley) usually has ESPP calculators and educational materials. Start there for free help.

Your Action for Today

Pick one thing from your pathway above and do it right now. Not enrolled? Find your plan document. Currently participating? Create your tracking spreadsheet. Ready to sell? Calculate your holding period.

ESPP is like a discount coupon that expires. The longer you wait to use it, the more money you leave on the table. You don't need to understand every tax rule to get started. You just need to take the first step.

The best time to enroll was last offering period. The second-best time is right now.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

TaxThe ISO AMT Trap: How Exercising Stock Options Can Cost You Thousands in Unexpected Taxes

The ISO AMT trap catches thousands of employees off guard every year. When you exercise incentive stock options, you might owe Alternative Minimum Tax on paper gains you haven't actually received - sometimes tens or hundreds of thousands of dollars. This guide explains exactly how the trap works and how to avoid it.

Not sure what to do with your equity?

Get a free personalized analysis