Vesting Cliff Explained: What Happens to Your Stock Before You're Fully Vested

Understanding the waiting period before your equity compensation becomes yours

Published March 14, 2026 · Updated March 14, 2026

A vesting cliff is a waiting period before any of your stock compensation becomes yours to keep. Think of it as a probationary period for your equity - nothing vests until you hit a specific date, then a chunk becomes yours all at once. This guide explains how cliffs work, what happens if you leave early, and how to plan around them.

The $80,000 Mistake: Why Your Start Date Matters More Than You Think

Sarah got a job offer at a tech company with a base salary of $120,000 and 10,000 RSUs. At $80 per share, those RSUs were worth $800,000 on paper. She was thrilled.

Eleven months later, a recruiter called with an even better opportunity. Sarah gave her two weeks' notice and moved to the new company. When she checked her brokerage account a month later, she expected to see some stock. Instead, she saw zero shares. Nothing. She had walked away from $200,000 worth of vested stock by leaving just one month early.

This is completely legal. And it happens every single day.

The culprit? A vesting cliff. Think of it like a loyalty rewards program with a cruel twist. You don't earn points gradually. You earn nothing, nothing, nothing, then suddenly everything at once, but only if you stay long enough.

Most equity grants at big companies have a one-year cliff. You could work for 364 days and leave with zero stock. But if you stay just one more day past that first year, a huge chunk of your equity vests all at once.

The difference between 11 months and 12 months at a company can literally be worth six figures. Yet most employees don't realize this until it's too late. If you're sitting on unvested equity right now, your start date might be the most expensive calendar entry you own.

So what exactly is a vesting cliff, and how does it work? Let's break it down in plain English.

What Is a Vesting Cliff? (The Simple Definition)

A vesting cliff is a waiting period before you earn any of your stock compensation. Think of it like a video game checkpoint. You don't save any progress until you reach that checkpoint. But once you hit it, all your progress up to that point counts.

Here's what happens during a cliff period:

Before the cliff date: You own zero shares. If you leave the company, you walk away with nothing from your equity grant.

On the cliff date: A chunk of shares vests all at once. This is your "cliff vesting" moment.

After the cliff date: The rest of your shares vest gradually, usually monthly or quarterly.

A Real Example

You start at Google on January 1, 2024. Your offer includes 4,800 RSUs with a 1-year cliff.

During 2024 (the cliff period): 0 shares vest. Even though you're working and those RSUs exist on paper, you don't actually own any of them yet.

January 1, 2025 (cliff date): 1,200 shares vest immediately. That's 25% of your total grant, all at once.

February 2025 through December 2027: 100 shares vest each month for the remaining 36 months.

Picture a timeline. There's a wall at the 1-year mark. Nothing gets through that wall until you reach it. Once you do, a big batch of shares comes through, and then shares flow steadily every month after.

The most common cliff is one year. But some companies use 6-month cliffs, 2-year cliffs, or no cliff at all. The cliff length matters a lot for your financial planning, especially if you're considering leaving the company.

Now let's look at the specific cliff schedules you'll actually encounter at major tech companies.

Sil Valley’s "Golden Handcuffs" Break: OpenAI, xAI Scrap Equity Cliffs in War for AI Talent

Common Vesting Cliff Schedules (With Real Examples)

Think of vesting cliffs like different gym membership contracts. Some make you commit for 6 months before you can cancel without penalty. Others lock you in for a year. The length varies, but the concept stays the same: you need to stick around for a set period to get the full benefit.

Here are the three most common cliff schedules you'll see:

The Standard Tech Schedule: 1-Year Cliff, 4-Year Vesting

This is the default at most public tech companies. You get nothing for your first year, then 25% of your grant vests all at once on your one-year anniversary.

Real example: You receive 4,000 RSUs when you join. Here's what happens:

- Months 1-12: 0 RSUs vest (you're still in the cliff period)

- Month 12 (your anniversary): 1,000 RSUs vest at once (25% of 4,000)

- Months 13-48: 83.33 RSUs vest every month (the remaining 3,000 RSUs divided by 36 months)

If your company's stock is worth $150 per share, that first cliff vesting gives you $150,000 worth of stock in one day. Then you earn about $12,500 worth each month after that.

The Startup Variation: 6-Month Cliff

Some companies, especially startups trying to compete for talent, use a shorter cliff. You wait 6 months instead of 12.

Real example: You get 2,400 RSUs with a 6-month cliff and 4-year total vesting.

- Months 1-6: 0 RSUs vest

- Month 6: 300 RSUs vest (12.5% of 2,400, which is 6 months out of 48)

- Months 7-48: 50 RSUs vest monthly (the remaining 2,100 divided by 42 months)

The math gets a bit messier, but you start earning equity twice as fast.

The Executive Schedule: 2-Year Cliff

Senior executives sometimes face longer cliffs. This schedule is rare for regular employees but common in C-suite offers.

Real example: An executive receives 10,000 RSUs with a 2-year cliff and 4-year vesting.

- Months 1-24: 0 RSUs vest

- Month 24: 5,000 RSUs vest at once (50% of 10,000)

- Months 25-48: 208.33 RSUs vest monthly (the remaining 5,000 divided by 24 months)

At $200 per share, that's a $1,000,000 payday after two years, then about $41,666 monthly.

The pattern: Notice how every schedule follows the same logic. The cliff determines when you get your first chunk. After that, the remaining shares vest in equal monthly installments until you hit the total vesting period.

But why do companies structure equity this way in the first place? Let's look at the business reasons behind vesting cliffs.

Master Incentive Programs: Cliff Vesting, Linear Vesting & Negotiation Tips! | Lawyer's Insight

Why Do Companies Use Vesting Cliffs? (The Honest Answer)

Think of vesting cliffs like a gym membership that requires a one-year commitment. The gym knows many people quit after two months, so they lock you in. Companies do the same math with new hires.

Here's what HR will tell you: cliffs are a retention tool. They want you to stay at least a year before you earn any equity. This filters out employees who aren't committed and rewards those who stick around.

But there's more to the story.

The Official Business Reasons:

- Reduces the cost of bad hires. If someone quits or gets fired in month 8, the company doesn't lose any equity from that grant.

- Industry standard. Every tech company uses cliffs, so they have to offer them to stay competitive.

- Protects the equity pool. Shares saved from early departures can go to high performers or future hires.

What Companies Won't Advertise:

Many people leave before their cliff. And companies know this.

Here's a real example: A company hires 100 employees, each receiving 1,000 RSUs with a one-year cliff. If 20 people leave before hitting their cliff date, the company saves 20,000 shares. At $100 per share, that's $2 million worth of stock back in the pool.

Without cliffs, those 20 people might have vested 5,000+ shares total through monthly vesting. That's a big difference.

The Bottom Line:

Cliffs serve dual purposes. They encourage you to stay and prove yourself. But they also save companies serious money when employees leave early, whether by choice or not.

Now, let's talk about what actually happens if you're one of those people who leaves before the cliff.

What Happens If You Leave Before Your Cliff Date?

Here's the hard truth: if you leave before your cliff date, you get zero shares. Nothing. It doesn't matter if you leave voluntarily or get laid off. It doesn't matter if you're one day away from the cliff. You walk away with no equity.

Think of a vesting cliff like a layaway plan at a store. You make payments for months, but if you stop before the final payment, you don't get the item. The store keeps everything. Same deal with your equity.

Here's exactly what happens:

- All unvested shares disappear

- They return to the company's equity pool

- You receive no compensation for the time you worked

- There's no prorated vesting during the cliff period

Let's use real numbers. You have 8,000 RSUs with a 1-year cliff. You leave at 11 months and 29 days. Result: 0 shares vest. You keep nothing. The full 8,000 RSUs are forfeited.

If you had stayed just 2 more days? 2,000 shares would have vested (worth $160,000 at $80 per share).

This applies to every departure scenario:

- You quit for a better job

- You get laid off

- You're terminated for performance

- You leave for personal reasons

Even if you were the best employee and got laid off at 11 months, you still get 0 shares. This feels harsh, and honestly, it is. But it's standard across the industry.

The only common exception is certain acquisition scenarios, where the acquiring company might accelerate vesting. We'll cover that later.

Action item: Check your exact cliff date right now. Look at your equity grant documents or ask HR. Put it in your calendar with multiple reminders. This date is worth tens or hundreds of thousands of dollars.

Once you pass the cliff, the rules change completely. Let's look at what happens next.

After the Cliff: How Vesting Continues (Month by Month)

You made it past your cliff date. Congratulations! Now your equity works like a subscription service that just ended its trial period. You get regular deposits of stock every single month, automatically.

Here's what happens next.

Your Stock Vests on Autopilot

After your cliff, a small portion of your remaining shares vests each month. You don't need to submit forms or request anything. It just happens on the same date every month (usually the anniversary of your hire date).

Think of it like a loyalty rewards program. Once you're past the initial waiting period, points (shares) drop into your account monthly as long as you stay with the company.

The Month-by-Month Math

Let's use a real example. You started March 15, 2024 with 4,800 RSUs on a standard 4-year schedule with a 1-year cliff.

March 15, 2025 (cliff date): 1,200 RSUs vest (25% of total)

April 15, 2025: 100 RSUs vest

May 15, 2025: 100 RSUs vest

June 15, 2025: 100 RSUs vest

July 15, 2025: 100 RSUs vest

August 15, 2025: 100 RSUs vest

This pattern continues every month until March 15, 2028, when your final 100 RSUs vest. That's 36 monthly vesting events after your cliff (3 years × 12 months).

At $75 per share, your cliff gives you $90,000 worth of stock. Then you get $7,500 every month for the next three years.

How to Track Your Vesting

Your company uses an equity management platform (like E*TRADE, Fidelity, Schwab, or Morgan Stanley). Log in and look for "Vesting Schedule" or "Equity Awards."

You'll see a table with dates and share amounts. It shows:

- Vested: Shares you own right now

- Unvested: Shares you'll get if you stay

- Next vesting date: When your next batch arrives

Set a calendar reminder for your monthly vesting date. Check that the shares actually show up as vested. Mistakes happen, and you want to catch them early.

Vesting Runs Until You Leave or Hit 4 Years

Your monthly vesting continues automatically as long as you're employed. It stops on your last day of work, even if you're mid-month. Any unvested shares disappear unless you have special terms (which we'll cover in the special cases section).

Now that you understand how ongoing vesting works, let's look at how vesting cliffs differ between RSUs and stock options.

Vesting Cliffs for Different Equity Types: RSUs vs. Stock Options

Here's the good news: vesting cliffs work exactly the same way whether you have RSUs or stock options. The timing is identical. You wait the same amount of time. You get nothing if you leave early.

But what you actually receive at the cliff? That's totally different.

RSUs: You Own Shares Automatically

Think of RSUs like a direct deposit bonus. When they vest, shares appear in your brokerage account. You own them. Done.

Example: You receive 1,000 RSUs with a 1-year cliff and 4-year vesting. On your one-year anniversary, 250 shares automatically become yours. If the stock is trading at $100 per share, you now own $25,000 worth of stock. You didn't pay anything. The shares just showed up.

Stock Options: You Own the Right to Buy Shares

Options are like a discount coupon at a store. The coupon vests, but you still need to use it. You have to pay money to actually get the shares.

Same example with options: You receive 1,000 stock options at a $50 strike price, same 1-year cliff and 4-year vesting. On your one-year anniversary, you can now buy 250 shares at $50 each. If the stock is trading at $100, you pay $12,500 to get shares worth $25,000. You pocket the $12,500 difference, but you had to spend money first.

ISOs vs. NSOs: The Cliff Works Identically

Some employees worry that Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) have different cliff rules. They don't. A 1-year cliff is a 1-year cliff, regardless of option type. The difference between ISOs and NSOs only matters for taxes, not for when they vest.

The One Thing That's the Same

Whether you have RSUs or options, leaving before your cliff date means you get zero equity. Nothing. The type of equity doesn't matter if you don't make it to the finish line.

Now let's talk about what happens at that finish line from a tax perspective, because the IRS treats RSUs and options very differently when they vest.

Vesting Schedules Explained: How Startup Equity Works | Employee Stock Options Guide

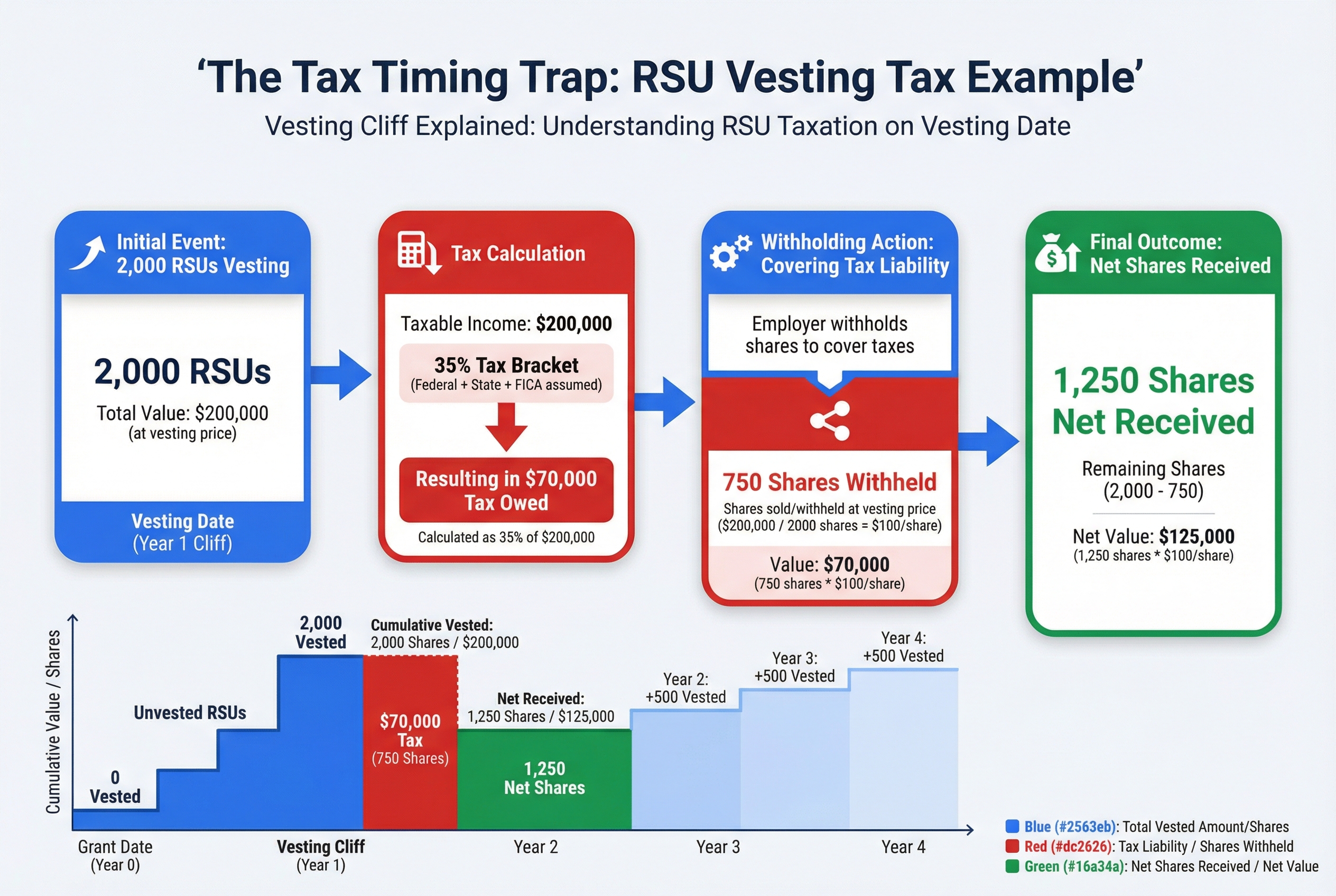

The Tax Timing Trap: When Cliff Vesting Triggers a Tax Bill

Here's the surprise that catches thousands of employees off guard: when your RSUs vest at the cliff, you owe taxes immediately. Even if you don't sell a single share.

Think of it like winning a car on a game show. You're excited, you won! But the IRS sees that $30,000 car as $30,000 of income. You owe taxes on it right away, whether you keep the car or sell it.

RSUs: The Immediate Tax Hit

When your RSUs vest, the IRS treats them as regular income. Just like your salary.

Here's what happens on your cliff date:

Your 1-year cliff hits: 2,000 RSUs vest worth $200,000. You're in the 35% tax bracket (federal + state + FICA). Tax owed: approximately $70,000.

Your employer withholds 750 shares (worth $75,000) to cover taxes. You receive: 1,250 shares net.

If you weren't prepared for this, seeing 750 shares disappear immediately can be shocking. But it's normal and required by law.

The bigger your cliff, the bigger your tax bill. A 4,000 RSU cliff at $150 per share? That's $600,000 in taxable income. Your tax bill could hit $200,000 or more.

Stock Options: Different Rules

Options work differently. Good news: no tax when they vest at your cliff.

The tax comes later, when you exercise (buy the shares). At that point, you pay tax on the difference between your strike price and the current stock price.

Example: Your options vest at the cliff with a $50 strike price. Stock is now at $150. No tax yet. You exercise 1,000 options next year when stock hits $200. You pay tax on $150,000 ($200 - $50 = $150 profit per share).

What You Need to Do Now

Don't let the tax bill blindside you.

Action steps before your cliff date:

- Calculate your expected tax bill (shares vesting × current price × your tax rate)

- Check your company's withholding policy (usually 22% federal minimum, but you might owe more)

- Set aside extra cash if the automatic withholding won't cover your full tax liability

- Talk to your payroll team about how withholding works

- Consider selling shares immediately at vest to cover any tax shortfall

The tax bill comes whether you're ready or not. Plan ahead.

Now, what happens to your vesting cliff if your company gets acquired or you get laid off? The rules change, and you need to know them.

When your cliff vests, the IRS treats the value as immediate income, often requiring a significant portion of shares to be withheld for taxes.

When your cliff vests, the IRS treats the value as immediate income, often requiring a significant portion of shares to be withheld for taxes.

Special Cases: What Happens to Your Cliff in Mergers, Layoffs, and Job Changes

Think of your vesting cliff like an insurance policy. Most of the time, the standard rules apply. But certain life events trigger special exceptions that completely change the outcome.

Here's what happens when your situation gets complicated.

When Your Company Gets Acquired

An acquisition can be your golden ticket or your biggest disappointment. It all depends on one phrase in your grant agreement: "acceleration clause."

Single-trigger acceleration means your unvested shares vest immediately when the company is acquired. The cliff disappears.

Example: You're 9 months into a 1-year cliff with 5,000 RSUs. Your company gets acquired at $100 per share. Your grant has single-trigger acceleration. Result: All 5,000 shares vest immediately. You receive $500,000 instead of $0.

Double-trigger acceleration requires two events: the acquisition AND you getting terminated within a certain period (usually 12-18 months). This protects you if the new company eliminates your role.

No acceleration means the standard cliff rules still apply, even after acquisition. You're at the mercy of the acquiring company's decisions.

When You're Laid Off

Here's the hard truth: layoffs typically don't waive your cliff.

Example: You're laid off at 11 months into a 1-year cliff. You have no acceleration clause. Result: You receive 0 shares, exactly as if you quit voluntarily.

Some companies include "involuntary termination" exceptions in their grant agreements. These are rare, but worth checking for. They might accelerate some portion of your unvested shares if you're laid off through no fault of your own.

When You're Fired for Performance

Performance terminations are treated the same as voluntary departures. No cliff exception. No partial vesting. You leave with only what had already vested before your termination date.

When You Change Roles Internally

Good news: moving to a different team or getting promoted usually doesn't affect your vesting cliff. Your original grant continues on the same schedule.

Exception: If you move to a different subsidiary or legal entity within the same company, check your grant agreement. Some companies treat this as a termination and rehire.

When Disability or Death Occurs

Most grant agreements include compassionate acceleration for disability or death. Your unvested shares (including those before the cliff) often vest immediately or on an accelerated schedule.

These provisions vary widely by company. Some vest 100% immediately. Others vest a prorated amount based on time served.

Your Action Items

Check your grant agreement for these specific clauses:

- Change of control provisions

- Involuntary termination exceptions

- Disability and death acceleration

- Internal transfer language

Don't assume anything. What applies to your coworker's grant might not apply to yours, especially if you joined in different years or at different levels.

Now that you understand the exceptions, let's talk about the practical question: how do you plan your career moves when you have unvested equity on the line?

How to Plan Your Career Moves Around Vesting Cliffs

Deciding whether to leave before your cliff is like deciding whether to break your apartment lease early. Sometimes the penalty hurts. Sometimes what you're moving to is so much better that the penalty doesn't matter.

Here's how to make this decision with actual numbers instead of gut feelings.

The Simple Math Framework

Step 1: Calculate what you're leaving behind

Multiply your unvested shares by the current stock price. That's real money you're walking away from.

Example: 2,000 RSUs at $90 per share = $180,000 you lose by leaving early.

Step 2: Calculate what you're gaining

Add up everything the new job offers:

- Salary increase (annual amount)

- Signing bonus

- New equity grants

- Better benefits (401k match, etc.)

Step 3: Compare over the same time period

If you're 10 months from your cliff, calculate what you'd gain in those 10 months at the new job versus what you'd earn by staying.

Real Decision Examples

Scenario 1: Worth Waiting

You're 2 months from your cliff. 2,000 RSUs vest, worth $180,000. New job offers $50,000 more in salary.

The math: $180,000 divided by 2 months = $90,000 per month to wait. The new salary only gives you about $4,000 more per month.

Wait for the cliff. Set a calendar reminder for your last day and start planning your exit.

Scenario 2: Leave Now

You're 10 months from your cliff. 500 RSUs vest, worth $30,000. New job offers $40,000 more salary plus a $100,000 signing bonus.

The math: You gain $130,000 by leaving (bonus plus 10 months of higher salary). You lose $30,000 by leaving. Net gain: $100,000.

Leave now. The opportunity cost of staying is too high.

Beyond the Spreadsheet

Money isn't everything. Factor in:

Your mental health. No amount of unvested stock is worth staying in a toxic job that's destroying you. If you dread Monday mornings and can't sleep Sunday nights, that's data.

Career growth. A role that teaches you new skills or puts you on a better career path has long-term value. Will staying another 8 months for your cliff mean missing a chance to level up?

The new opportunity's timeline. Great jobs don't wait. If this company will hire someone else next week, that changes the calculation.

Set a Personal Deadline

Don't let vesting cliffs trap you forever. Decide right now: "I'll stay until [specific date], but not one day longer, regardless of what vests."

Write that date down. This prevents the sunk cost fallacy, where you keep waiting "just a little longer" for the next vesting date, then the next one, then the next one.

The $50,000 Rule of Thumb

If waiting for your cliff means giving up more than $50,000 in other opportunities (new salary, signing bonus, career growth), seriously consider leaving anyway. The exception: you're less than 3 months from a massive cliff (over $150,000).

Your unvested equity is valuable. But it's not handcuffs. Run the numbers, trust the math, and make the choice that sets up your next five years, not just your next paycheck.

Now that you know how to time your exit, let's talk about whether you can actually change your vesting schedule before it becomes a problem.

Can You Negotiate Your Vesting Cliff? (What Actually Works)

Negotiating a vesting cliff is like trying to negotiate lease terms at an apartment complex. Some things are flexible, like move-in dates or parking spots. Other things are building policy, set in stone for everyone.

Here's the reality: your leverage depends entirely on company size and your role.

At Large Public Companies: Usually Non-Negotiable

Big tech companies like Google, Microsoft, or Salesforce have standardized vesting schedules. They apply the same cliff to everyone from entry-level engineers to VPs.

Failed negotiation example: A mid-level product manager at a Fortune 500 company asked HR to waive the 1-year cliff on her 2,000 RSUs. HR response: "Our vesting schedules are standardized across all employees. No exceptions."

She pivoted and successfully negotiated a $30,000 higher base salary instead.

At Startups: More Room to Move

Smaller companies and startups have more flexibility. They're competing for talent without big-company brand names.

Successful negotiation example: A senior engineer had two competing offers. Company A wouldn't waive the 1-year cliff, but they agreed to:

$50,000signing bonus (offsets the cliff risk)- 20% larger equity grant (5,000 options instead of 4,000)

She got more total value even with the cliff intact.

What You Can Actually Ask For

If the company won't budge on the cliff itself, try these alternatives:

Signing bonus. Ask for cash upfront equal to 6-12 months of equity value. If you leave before the cliff, you keep the bonus.

Larger grant. Request 15-20% more equity to compensate for the cliff risk.

Shorter cliff. Some companies will reduce a 1-year cliff to 6 months for senior hires.

Faster refresh grants. Ask for your first refresh grant after 6 months instead of 12 months.

How to Ask (Actual Language)

Don't say: "Can you remove the vesting cliff?"

Instead say: "I'm excited about this offer. Given the 1-year cliff, would you consider a signing bonus to offset that initial period? Or perhaps a larger equity grant?"

Always get changes in writing. Verbal promises about equity mean nothing. Your offer letter must specify the exact terms.

When You Have the Most Leverage

You can negotiate more effectively when:

- You're in a senior or highly specialized role

- You have competing offers

- The company has been trying to fill the role for months

- You're relocating or taking a risk to join

Now that you know what's negotiable, let's create your action plan for managing vesting cliffs at your current or future job.

Your Action Plan: What to Do Right Now

You've learned how vesting cliffs work. Now it's time to take action. Think of this like checking your bank balance - the information only helps if you actually look at it.

Here's your 30-minute checklist. Do these steps today:

1. Find Your Exact Cliff Date

- Log into your equity portal (E*TRADE, Fidelity, Schwab, Morgan Stanley, etc.)

- Look for "Vesting Schedule" or "Grant Details"

- Write down the exact date your cliff hits

- Can't find it? Check your offer letter or email HR

2. Calculate Your Cliff Value

- Find how many shares vest at your cliff (usually 25% of your grant)

- Multiply by your company's current stock price

- Example: 100 RSUs × $150 = $15,000 vesting on your cliff date

3. Set Your Reminder

- Add a calendar alert for 2 weeks before your cliff date

- Label it "Equity Cliff - Review Vesting & Taxes"

- This gives you time to plan, not scramble

4. Estimate Your Tax Bill (RSUs Only)

- Take your cliff value and multiply by 0.37 (roughly 37%)

- Example: $15,000 × 0.37 = $5,550 withheld in taxes

- Your company withholds this automatically, but you should know the number

5. Review Your Grant Agreement

- Download and save a PDF copy from your equity portal

- Look for sections on "Termination" and "Change of Control"

- Note any special provisions (some companies accelerate vesting)

6. If You're Considering Leaving

- Use the decision framework from section 10

- Calculate exactly what you'd forfeit by leaving early

- Compare to your new job's total compensation, including equity

Save this article. You'll want to reference it as each vesting period approaches. Now you have the information to make smart decisions about your equity and your career.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis