RSU Tax Strategies: How to Keep More of Your Stock Compensation

Practical ways to reduce your tax bill and make smarter decisions with your restricted stock units

Published March 14, 2026 · Updated March 14, 2026

RSUs create tax bills that catch many employees off guard. This guide walks you through exactly how RSUs are taxed and shows you practical strategies to reduce what you owe, from adjusting withholding to timing your sales strategically.

Why Your First RSU Vesting Creates a Tax Surprise (And How to Avoid It)

Sarah, a software engineer at a tech company, checked her phone one morning and saw the notification she'd been waiting for: 100 RSUs had just vested. At $200 per share, that's $20,000. She started mentally spending it on a down payment for a condo.

Then her paycheck arrived. It was $5,000 lighter than usual.

What happened? Her company withheld taxes on those RSUs, just like they would on a cash bonus. Sarah felt blindsided. The RSUs seemed like free money, but they created a real tax bill the moment they vested.

Here's the part that makes it worse. That $4,400 her company withheld (22% of $20,000)? It probably won't be enough. If Sarah's in the 32% tax bracket like many tech employees, she'll owe another $2,000 when she files her tax return. That's money she needs to have sitting in her bank account, ready to go.

Think of RSUs like a bonus check, not a lottery win. When you get a $20,000 cash bonus, you know taxes will eat into it. RSUs work the same way. The difference is that RSUs feel like play money until they vest and suddenly become very real income on your W-2.

This surprise happens to almost everyone on their first vesting. You're not alone, and you're not doing anything wrong. Most people don't realize that:

- Taxes are due when RSUs vest, even if you don't sell a single share

- Your company's automatic withholding usually covers only the federal minimum (22%)

- You might owe state taxes, Social Security, Medicare, and more on top of that

The good news? Once you understand how RSU taxes work, you can plan ahead and keep thousands more of your stock compensation. Let's start with the mechanics.

How RSU Taxes Actually Work (The Simple Version)

Here's the thing nobody tells you upfront: RSUs are taxed exactly like your regular paycheck the moment they vest. Think of vesting day as getting a cash bonus, except the bonus comes in stock instead of dollars.

The First Tax Event: Vesting Day

When your RSUs vest, the IRS treats those shares as ordinary income. It doesn't matter that you received stock. The government wants its cut based on what those shares are worth.

Here's how it works in real numbers:

You have 50 RSUs that vest on March 15th. Your company's stock trades at $150 per share that day. The math is simple: 50 shares × $150 = $7,500 of taxable income.

That $7,500 gets taxed at your regular income tax rate (the same rate you pay on your salary). If you're in the 32% federal bracket, you owe $2,400 in federal taxes, plus $574 for FICA (Social Security and Medicare), plus state taxes if you live somewhere like California or New York.

Your Company Withholds Automatically

Your employer knows taxes are due, so they handle it for you. They typically withhold 22% for federal taxes, plus 7.65% for FICA. Some companies also withhold estimated state taxes.

Using our example: Your company keeps about 13 of your 50 shares to cover the $2,224 in withholding ($1,650 federal + $574 FICA). You receive approximately 37 shares in your brokerage account.

This withholding shows up on your W-2 at year-end, just like regular wages. The vested value ($7,500) appears as income. The withheld amount ($2,224) appears as taxes paid.

The Second Tax Event: When You Sell

Selling your shares creates a second, separate tax bill. We'll cover this in detail later, but here's the quick version: any gain (or loss) between your vesting day price and your sale price gets taxed as capital gains.

The catch? That 22% withholding rate is often too low, especially if you earn over $100,000. Let's look at why that creates problems.

RSU Taxes Explained + 5 Strategies for 2024

The Withholding Gap: Why 22% Is Usually Not Enough

Your company withholds 22% in federal taxes when your RSUs vest. For most tech employees, that's not nearly enough.

Here's why: The IRS lets companies use a flat 22% withholding rate for supplemental income like bonuses and stock compensation. Think of this 22% like a down payment on a house. It's a start, but it rarely covers the full amount you owe.

Your actual tax rate depends on your total household income, not just what your company withholds. Federal tax brackets range from 10% to 37%. If you're earning $150,000 or more (common at large tech companies), you're likely in the 24%, 32%, or 35% bracket.

Here's how the gap happens:

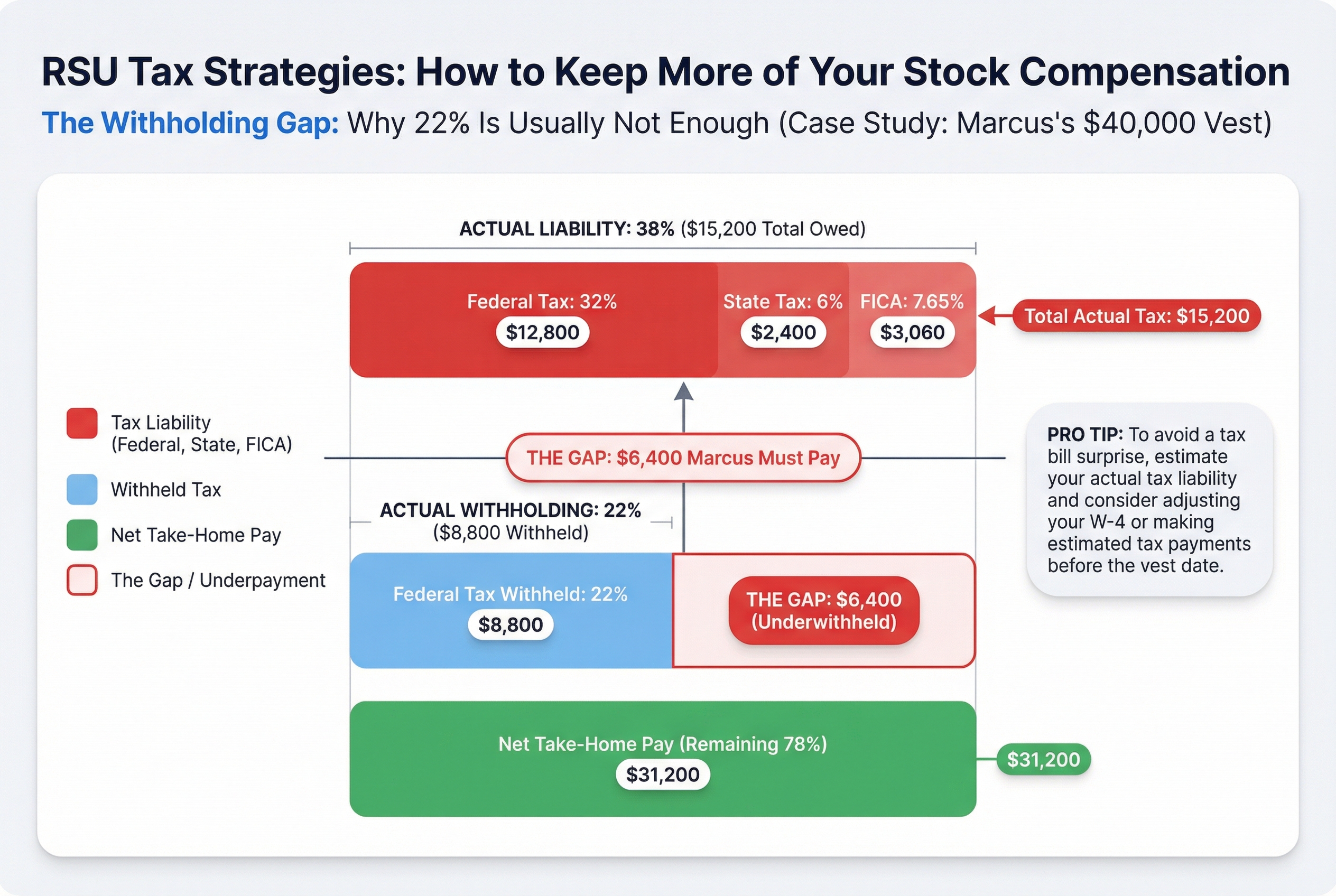

Marcus earns $180,000 in salary plus $40,000 in vesting RSUs this year. His top tax bracket is 32% federal, plus he pays 6% state tax in Massachusetts.

- Company withholds: 22% of $40,000 = $8,800

- Marcus actually owes: 38% of $40,000 = $15,200

- The gap: $6,400 he must pay at tax time

And that's just federal and state. FICA taxes (Social Security and Medicare) add another 7.65% on income up to certain caps. In California or New York, state taxes can reach 13%, making the gap even bigger.

Quick check: Do you have a withholding gap?

| Your Total Income | Your Likely Federal Bracket | Gap vs. 22% Withholding |

|---|---|---|

| Under $90,000 | 22% | Little to none |

| $90,000 to $190,000 | 24% | Small gap (2%) |

| $190,000 to $364,000 | 32% | Big gap (10%) |

| $364,000 to $462,000 | 35% | Huge gap (13%) |

| Over $462,000 | 37% | Massive gap (15%) |

Simple formula: If your top tax bracket is higher than 24%, you have a gap. Add your state tax rate to see the full picture.

The good news? You can fix this gap before tax time arrives. Let's look at how.

Marcus's combined 38% effective tax rate on RSUs results in a substantial withholding gap compared to the standard 22% federal withholding.

Marcus's combined 38% effective tax rate on RSUs results in a substantial withholding gap compared to the standard 22% federal withholding.

Strategy 1: Fix Your Withholding Before You Owe

Think of tax withholding like prepaying a bill. You have three ways to do it: automatic deduction from every paycheck, a lump sum upfront, or quarterly installments. The key is choosing your method before your RSUs vest, not after you already owe the IRS money.

Let's start with the math. Remember the withholding gap from the last section? Here's how to calculate what you need to cover:

Your gap = (Your actual tax rate - 22%) × Total RSU vesting value

Jennifer expects $50,000 in RSUs to vest this year. She's in the 32% tax bracket. Her gap is 10% (32% minus 22%), which equals $5,000 she needs to cover beyond the automatic withholding.

Method 1: Increase Your W-4 Withholding (Easiest)

If you get regular paychecks, this is your simplest option. You tell your employer to withhold extra tax from every paycheck to cover the RSU gap.

How to do it:

- Log into your company's payroll system

- Find your W-4 form (usually under "Tax Withholding" or "Tax Settings")

- Look for "Additional withholding per pay period"

- Enter your gap amount divided by number of paychecks

Jennifer gets paid 24 times per year. She divides $5,000 by 24 and enters $208 as her additional withholding. Done.

This works best if: You have regular paychecks and your RSU vesting is spread throughout the year.

Method 2: Request Extra RSU Withholding (Company-Dependent)

Some companies let you increase the withholding percentage when your RSUs vest. Instead of the standard 22%, you might request 32% or whatever matches your tax bracket.

How to do it:

- Contact your stock plan administrator (Fidelity, E*TRADE, Schwab, etc.)

- Ask if you can customize your RSU withholding percentage

- If yes, set it to match your actual tax bracket

This works best if: Your company allows it and you have large, infrequent vesting events.

Warning: Not all companies offer this option. Many are stuck at the 22% supplemental rate.

Method 3: Make Quarterly Estimated Payments (Most Control)

This is like paying your taxes directly to the IRS four times per year. You calculate what you owe and send it in using Form 1040-ES.

How to do it:

- Download Form 1040-ES from IRS.gov

- Calculate your quarterly payment (annual gap ÷ 4)

- Pay online at irs.gov/payments or mail a check

- Payment deadlines: April 15, June 15, September 15, January 15

Jennifer could skip the W-4 adjustment and instead send the IRS $1,250 four times per year.

This works best if: RSUs are your only income, you're self-employed, or your gap is very large (over $10,000).

You must use this method if: You don't have regular paychecks to adjust or your employer won't increase RSU withholding.

Which Method Should You Choose?

Pick Method 1 if: You have regular paychecks. It's automatic and you won't forget.

Pick Method 2 if: Your company allows it and you want withholding to happen right when RSUs vest.

Pick Method 3 if: Methods 1 and 2 aren't available or you want maximum control.

Use multiple methods if: Your gap is large. Jennifer could increase her W-4 by $100 per paycheck AND make two quarterly payments of $1,200 each.

The important thing is to set this up before your first major vesting event. Fixing your withholding in January is smart. Scrambling in April when you file taxes is stressful.

Now that you know how to cover the withholding gap, let's look at another powerful strategy: controlling when your RSUs vest and sell to manage your tax bracket year by year.

Strategy 2: Time Your RSU Sales to Spread Out Income

Here's something most people miss: you can't control when your RSUs vest, but you absolutely control when you sell them.

That timing matters more than you think.

The Tax Bracket Bucket Problem

Think of tax brackets like buckets stacked on top of each other. Each bucket fills at its own rate. The bottom bucket (10% bracket) fills cheaply. The top bucket (37% bracket) costs way more to fill.

When you sell a huge chunk of RSUs in one year, you're dumping water into the expensive buckets. When you spread those sales across multiple years, you keep filling the cheaper buckets instead.

Here's how this plays out in real life:

David has $200,000 in vested RSUs sitting in his account. He's already earning $150,000 in salary (married filing jointly). If he sells all his RSUs in 2025, here's what happens:

- Total income: $350,000

- The last $100,000 gets taxed at 32% and 35% brackets

- Federal tax bill on RSU sales: approximately $68,000

Instead, David sells $100,000 in 2025 and $100,000 in 2026:

- Each year's total income: $250,000

- All RSU income stays in the 24% bracket

- Federal tax bill on RSU sales: approximately $48,000 (total across both years)

David saves roughly $20,000 just by waiting one year to sell half.

When This Strategy Works Best

This approach makes sense when:

- You don't need all the cash immediately

- You have multiple years of vested RSUs piling up

- Your salary plus one year of sales would push you into a higher bracket

- You can afford to hold the stock for 12 months (though market risk applies)

Important: Tax brackets are marginal, not flat rates. You don't pay 35% on everything just because some income hits that bracket. You pay 35% only on the dollars in that bucket.

What to Consider First

Look at your full financial picture:

- Your salary and expected bonuses

- Your spouse's income (if married)

- Other income sources (rental properties, side gigs)

- Major expenses coming up (home purchase, tuition)

A big life event might change your calculation. Getting married? Having a baby? Those can shift your tax situation significantly.

The Catch

This strategy only works if you can wait. If you need $200,000 for a down payment next month, spreading sales across two years won't help you.

Also remember: holding vested RSUs means taking on market risk. The stock could drop while you're waiting for the next tax year. (We cover the hold vs. sell decision in our separate article on RSU investment strategies.)

How to Strategically use RSUs to Save Tax

Now that you understand how timing your sales can save thousands, let's look at what happens tax-wise when you actually sell those shares. That's where capital gains come in, and it's simpler than you think.

Understanding the Second Tax: Capital Gains When You Sell

Here's what catches people off guard: you've already paid income tax when your RSUs vested. But when you sell those shares, you might owe tax again.

Think of it like reselling a concert ticket. You only pay tax on your profit (the selling price minus what you paid). With RSUs, your "purchase price" is the stock value on vesting day. That's the amount you already paid income tax on.

Here's How It Works

Your cost basis equals the fair market value on the day your RSUs vested. This is the same number that showed up on your W-2 as income.

Let's say 100 RSUs vest when the stock is at $100 per share. That's $10,000 of taxable income. You pay income tax on this amount (covered in earlier sections).

Now you hold the shares and sell them later:

If the stock goes up:

- You sell 6 months later at $120 per share

- Total proceeds: $12,000

- Your cost basis: $10,000 (the vesting day value)

- Taxable gain: $2,000

- You owe capital gains tax on that $2,000 profit

If the stock goes down:

- You sell at $90 per share

- Total proceeds: $9,000

- Your cost basis: $10,000

- Capital loss: $1,000

- You can deduct this loss on your tax return

Short-Term vs. Long-Term Rates Matter

The tax rate on your profit depends on how long you held the shares after vesting:

Short-term gains (you sold within 1 year of vesting): Taxed as ordinary income, just like your salary. If you're in the 32% tax bracket, you pay 32% on the gain.

Long-term gains (you held for 1+ year after vesting): Taxed at lower capital gains rates of 0%, 15%, or 20%. Most people pay 15%, which is a significant savings.

Capital Losses Can Help You

If your stock drops after vesting, you have a capital loss when you sell. You can use this loss to offset other investment gains. If you have more losses than gains, you can deduct up to $3,000 against your regular income each year.

Watch Out for the Wash Sale Rule

You cannot claim a capital loss if you buy the same stock within 30 days before or after selling it. This prevents you from selling to harvest a tax loss while immediately buying back in.

Now that you understand both tax events (vesting and selling), let's look at a powerful strategy that lets you skip the capital gains tax entirely.

RSU Tax Tips: Avoid Double Taxation

Strategy 3: Donate Appreciated RSUs to Charity (The Tax-Free Exit)

Here's a tax move that feels like magic: donate RSU shares that went up in value, and the IRS erases the capital gains tax completely. It's like having a "get out of tax free" card for stock appreciation.

How the Magic Works

When you donate appreciated stock directly to charity, two good things happen:

- You avoid paying capital gains tax on the increase in value

- You get a tax deduction for the full current market value

Think of it as a tax eraser. The government says "we'll pretend that gain never happened" as long as you give the shares to charity instead of selling them yourself.

The Side-by-Side Comparison

Let's say you have RSUs that vested 2 years ago at $50 per share. You paid income tax on that $50 back then. Now those shares are worth $150 each, and you want to donate $15,000 to charity.

Option A: Sell first, then donate cash

- Sell 100 shares at $150 = $15,000

- Pay capital gains tax on $10,000 gain = $2,000 in taxes

- Donate $13,000 cash to charity

- Get $13,000 tax deduction

Option B: Donate shares directly

- Transfer 100 shares directly to charity

- Pay zero capital gains tax

- Charity receives full $15,000 value

- You get $15,000 tax deduction

You just saved $2,000 in taxes by donating the shares instead of cash. The charity gets more money, and you get a bigger deduction.

Important Requirements

This only works if you follow these rules:

- You must hold the shares after vesting. You can't donate at the moment RSUs vest. You need to receive the shares, hold them while they appreciate, then donate.

- Transfer shares directly. Don't sell first and donate cash. That triggers the capital gains tax you're trying to avoid.

- Use a qualified charity. Must be a 501(c)(3) organization or similar qualified nonprofit.

- Deduction is limited. You can only deduct up to 30% of your adjusted gross income (AGI) for stock donations in one year. Excess carries forward five years.

What About the Vesting Tax?

Remember, you already paid income tax when these RSUs vested at $50 per share. That tax isn't going away. This strategy only helps you avoid the second tax (capital gains) on the appreciation from $50 to $150.

When This Makes the Most Sense

This strategy works best when:

- Your RSU shares have increased significantly since vesting (at least 20-30%)

- You already planned to donate to charity anyway

- You're in a high tax bracket (making the deduction more valuable)

- You have shares you've held for over a year (long-term capital gains rates apply)

The Donor-Advised Fund Shortcut

Don't know which charity to support right now? Use a donor-advised fund (DAF). It's like a charitable savings account.

You donate your appreciated RSU shares to the DAF today and get the immediate tax deduction. The shares are sold inside the DAF (tax-free). Then you recommend grants to specific charities whenever you want, even years later.

Popular DAF providers include Fidelity Charitable, Schwab Charitable, and Vanguard Charitable. Minimum contributions start around $5,000.

Real Numbers Matter

The tax savings get bigger as your gains grow. If you have shares that tripled in value, you're avoiding capital gains tax on a 200% gain. At a 20% long-term capital gains rate (federal), that's serious money.

Example: Donate $30,000 worth of shares you bought for $10,000. You avoid paying $4,000 in federal capital gains tax, plus any state taxes.

The Bottom Line

If you're charitably inclined and sitting on appreciated RSU shares, donating stock beats donating cash every time. It's one of the few strategies where you can legally make a tax disappear.

Next, we'll tackle a situation that doubles the complexity: what happens when both you and your spouse receive RSUs from your employers.

Special Situation: Tax Planning for Dual-RSU Households

When both spouses receive RSUs, your tax situation gets complicated fast. Think of it like two rivers flowing into one lake. Each river looks manageable on its own, but together they can overflow the banks.

Here's what happens: Your companies see you as separate employees. Mike's company withholds 22% on his $60,000 RSU vesting. Priya's company withholds 22% on her $40,000 vesting. Each company thinks it's doing the right thing.

But the IRS sees you as one household with $400,000 total income (Mike's $150k salary + Priya's $150k salary + $60k RSUs + $40k RSUs). That puts you in the 35% tax bracket, not 22%.

The math gets ugly:

- Companies withhold: $22,000 (22% of $100,000 RSUs)

- You actually owe: $35,000 (35% of $100,000 RSUs)

- Your tax gap: $13,000

This gap catches dual-RSU households by surprise every April.

How to Coordinate Your Tax Planning

Split the withholding fix between both of you. Mike increases his W-4 withholding by $250 per paycheck. Priya increases hers by $150 per paycheck. Over 26 paychecks, that covers the $13,000 gap. Neither person shoulders the whole burden.

Review your combined vesting schedule. If Mike has RSUs vesting in March and Priya has RSUs vesting in April, you'll get hit with a massive tax bill in Q1. Try to space out vesting dates across quarters if your companies allow it.

Decide whose RSUs to sell first. If Mike's RSUs have been held longer, they might qualify for long-term capital gains rates. Sell those last. Sell Priya's newer RSUs first to minimize the tax bite.

Check your tax situation every quarter, not just once a year. Dual-RSU households can't afford to wait until December to discover a problem. Set a calendar reminder for January, April, July, and October. Run the numbers each time.

Consider making estimated tax payments. If both of you have large RSU vestings, adjusting W-4 withholding might not be enough. You may need to send the IRS quarterly payments directly.

Your HR departments don't talk to each other. You need to be the coordinator who sees the full picture.

Next, let's talk about the things your HR department won't tell you about RSU taxes, and why you can't rely on them for tax advice.

What Your HR Department Won't Tell You About RSU Taxes

Your HR team is like a GPS that shows you the road but can't tell you the best route for your specific trip. They know the RSU mechanics, but they're legally blocked from giving you personalized tax advice.

Here's what most employees don't realize.

HR Can't Calculate Your Real Tax Bill

Tom asks HR how much he'll owe in taxes on his 200 RSUs vesting at $150 each. HR says "about 22% federal plus state." Tom assumes that's his total tax bill and sets aside $7,920.

Reality: Tom's in the 32% federal bracket. HR couldn't tell him his actual rate because they don't know his spouse's $90k income, his rental property, or his $15k in deductions. Tom actually owes $15,840. He's short $7,920.

HR isn't hiding information. They legally can't give tax advice. They can only tell you what the company will withhold, not what you'll actually owe.

The Company Withholding System Is One-Size-Fits-All

Your company picks 22% federal withholding because that's the IRS default for supplemental income. It has nothing to do with your personal tax situation.

Think of it like getting a medium shirt when you ordered clothes online. It fits some people perfectly, but most need a different size.

What most employees don't know: You can request a higher withholding rate. Just ask your equity admin team. Many companies let you withhold 30%, 35%, or even 40%. You just have to ask before the vesting date.

Your Equity Portal Lies (Sort Of)

Log into your equity portal right now. See that big number showing your RSU value? That's the gross amount, before taxes.

Reality check: If it says you're getting $30,000 in vesting RSUs, you're probably taking home $18,000 to $21,000 after all taxes. The portal doesn't show this clearly because the after-tax amount depends on your personal situation.

What Else HR Can't Tell You

Vesting dates: For new hires negotiating an offer, vesting dates are often flexible. HR won't volunteer this. You can sometimes push a vesting date from December to January to spread income across tax years.

Same-day sale options: Some companies let you sell shares immediately to cover taxes. Others make you wait 1-3 days, creating market risk. HR knows which system your company uses, but rarely explains it upfront.

Mortgage applications: Your vesting RSUs count as income for loan applications. But HR won't tell you to time your mortgage application right after a big vest. That's financial advice.

State tax complications: If you work remotely in a different state than your company headquarters, you might owe taxes in multiple states. HR will withhold for one state. You're responsible for figuring out the rest.

The Information Gap Is By Design

Companies want to help, but legal liability prevents them from giving personalized guidance. They can explain the mechanics. They can't tell you what to do with your specific situation.

That's where you need to take control. The next section covers the most common RSU tax mistakes and exactly how to fix them before they cost you money.

Common RSU Tax Mistakes (And How to Fix Them)

RSU taxes are like a minefield. One wrong step costs you hundreds or thousands of dollars. The good news? Most mistakes are fixable, and all of them are avoidable.

Here are the five most expensive mistakes employees make, and exactly how to fix them.

Mistake 1: Doing Nothing and Owing Big at Tax Time

The mistake: You ignore your RSU taxes all year. You figure the company withheld taxes, so you're covered.

Why it happens: RSU vesting feels automatic. Money appears in your account. You assume someone else handled the tax part.

What it costs: Let's say you're Rachel. You earn $80,000 in salary. Another $80,000 in RSUs vests this year. Your company withholds $17,600 (the standard 22%). But you're actually in the 32% tax bracket on that RSU income. You owe $25,600 in federal tax alone.

At tax time, you owe $8,000 you don't have. Plus the IRS charges you a $400 underpayment penalty because you didn't pay enough throughout the year.

The fix right now: Set up a payment plan with the IRS at irs.gov/payments. They charge interest, but it beats ignoring the bill. Then immediately increase your W-4 withholding or start making quarterly estimated tax payments. Use the safe harbor rule: pay 110% of last year's total tax to avoid penalties next year.

Mistake 2: Selling Everything Immediately Without a Plan

The mistake: Your RSUs vest. You sell them all the same day. You repeat this every quarter.

Why it happens: You want cash, not stock. Selling at vest feels safe and simple.

What it costs: You miss out on long-term capital gains treatment. Every dollar of growth gets taxed at ordinary income rates (up to 37%) instead of long-term rates (up to 20%). On a $20,000 gain, that's a $3,400 difference.

The fix: Keep some RSUs for at least one year after vesting. Even holding 25% of each vesting tranche saves you thousands. You already paid income tax at vesting. Now you're just choosing between a 37% tax rate and a 20% tax rate on the growth.

Mistake 3: Forgetting State Taxes When You Move

The mistake: You move from California to Texas mid-year. You assume Texas (no income tax) applies to all your RSUs.

Why it happens: State tax rules for equity compensation are confusing. Different states tax you based on where you earned the RSUs, not where they vested.

What it costs: California still wants tax on RSUs you earned while living there, even if they vest after you move. On $100,000 in RSUs, California's 9.3% rate means you owe $9,300 you didn't budget for.

The fix: Talk to a CPA who handles multi-state returns before you move. They'll calculate how much each state can tax. File returns in both states. It's complex, but the penalty for getting it wrong is worse. Some states have specific formulas for equity comp earned in one state but vested in another.

Mistake 4: Losing Track of Your Cost Basis

The mistake: You don't track what you paid in taxes for each RSU vesting tranche. When you sell shares two years later, you can't prove your cost basis.

Why it happens: Your company tracks vesting, but you need to track basis yourself. It's boring paperwork that seems unimportant until you need it.

What it costs: Without proof of cost basis, the IRS assumes it's zero. You pay capital gains tax on the full sale price, not just the growth. On a $50,000 sale where your real basis was $45,000, you pay tax on $50,000 instead of $5,000. That's $9,000 in unnecessary taxes.

The fix: Create a spreadsheet right now. List every vesting date, number of shares, stock price at vest, and taxes paid. Your brokerage statements show this info. Update it every quarter. Keep all vesting confirmations and tax forms (W-2, 1099-B) for seven years. Think of it like keeping receipts for a big purchase.

Mistake 5: Trusting Company Withholding Is Enough

The mistake: You assume the 22% your company withholds covers your full tax bill.

Why it happens: The withholding happens automatically. It looks official. You figure they know what they're doing.

What it costs: If you're in the 32% or 35% bracket, you're short 10-13 percentage points. On $100,000 in RSU income, that's $10,000 to $13,000 you still owe. Plus underpayment penalties.

The fix: Calculate your real tax bracket (salary plus RSU income). Compare it to the 22% withholding rate. The gap is what you need to cover. Either increase your W-4 withholding on your regular paycheck or make quarterly estimated tax payments. The safe harbor rule protects you: pay 110% of last year's total tax bill through withholding and estimates.

The Cost of Waiting

Every mistake costs more the longer you wait. Underpayment penalties add up monthly. Missing cost basis documentation gets harder to recreate. State tax bills grow with interest.

The IRS would rather you fix mistakes yourself than audit you later. Most of these fixes take an hour and cost nothing except some extra withholding.

Now that you know what to avoid, let's put together your action plan. The next section gives you a step-by-step checklist to implement everything you've learned, starting this week.

Your RSU Tax Planning Checklist (What to Do This Week)

Think of this checklist like a pre-flight safety check. Pilots go through the same steps before every takeoff because missing one item can cause problems. Your RSU tax planning works the same way.

Here's what to do right now, organized by when you need to do it.

Before Your First RSU Vesting

Action 1: Find out what's coming Log into your company's equity portal (usually Fidelity, E*TRADE, Morgan Stanley, or Schwab). Look for your vesting schedule. Write down the total value of RSUs vesting this year.

Action 2: Calculate your real tax rate Go to the IRS Tax Withholding Estimator at irs.gov/W4app. Enter your salary plus your total RSU vesting value. The tool shows your actual tax bracket (probably 24%, 32%, or 35% if you're earning over $100k).

Action 3: Find your withholding gap

Use this formula: (Your tax rate minus 22%) times total RSU value = your gap

Example: You earn $120k salary. You have $50,000 in RSUs vesting this year. The calculator shows you're in the 24% bracket.

- Gap calculation:

(24% minus 22%) times $50,000 = $1,000 - You'll owe an extra $1,000 at tax time if you don't fix withholding.

Action 4: Close the gap If your gap is over $1,000, pick one:

- Submit a new W-4 to your payroll department asking for extra withholding per paycheck

- Set up quarterly estimated tax payments at irs.gov/payments

Action 5: Set reminders Put these dates in your calendar right now:

- April 15, June 15, September 15, January 15 (estimated payment deadlines)

- One week before each RSU vesting date

- December 1 (year-end tax planning check)

At Each Vesting (Do This Every Time)

When your RSUs vest:

- Check your equity portal the next day. Confirm the number of shares you received matches what you expected.

- Save the vesting confirmation email or download the statement. You need this for your tax records.

- Write down your cost basis (the stock price on vesting date). You'll need this when you sell.

Contact: Your equity portal help desk if numbers don't match.

Quarterly Reviews (Four Times Per Year)

Every three months:

- Log into your equity portal and add up year-to-date RSU income

- Check if your withholding is on track (look at your last paystub)

- If you're behind, make an estimated tax payment by the deadline

- Review any shares you sold and calculate gains or losses

This takes 15 minutes. Set a recurring calendar reminder.

Contact: Your tax professional if you're more than $2,000 behind on withholding.

Before You Sell Any Shares

Run through this checklist:

- How long have you held these shares? (Check vesting date in portal)

- Less than one year = short-term capital gains (taxed as regular income)

- More than one year = long-term capital gains (lower 15% or 20% rate)

- What's your gain or loss?

(Current price minus cost basis) times number of shares - Do you have losing positions to offset gains? (Tax-loss harvesting opportunity)

Example: You want to sell 100 shares. Cost basis was $150 (the price when they vested 8 months ago). Current price is $180.

- Holding period: 8 months (short-term)

- Gain:

($180 minus $150) times 100 = $3,000 - Tax impact: $3,000 taxed at your regular rate (maybe 24% = $720)

- Should you wait 4 more months for long-term rate? Maybe, if stock seems stable.

Contact: Your financial advisor if you're selling over $50,000 in shares.

Annual Year-End Tasks (Do in December)

Before the year ends:

- Download all vesting confirmations and sale confirmations from your equity portal

- Compare your W-2 (box 1) with your vesting records. They should match.

- Look at your total tax withholding. Will it cover your bill?

- If you're short, make a final estimated payment by January 15

- Plan next year: What's vesting? What's your strategy?

Contact: Your HR department if W-2 numbers look wrong (do this in January when you get your W-2).

When to Get Professional Help

Hire a tax professional if:

- You're earning over $200,000 total (salary plus RSUs)

- You have RSU grants from multiple years with different vesting schedules

- Your spouse also gets RSUs (dual-RSU household)

- You're considering exercising stock options too

- You got a promotion or big raise this year

- You're moving to a different state

- You owe more than $5,000 in taxes and don't know why

A CPA who specializes in equity compensation costs $300 to $800 for tax prep, but they often save you more than they cost.

Contact: Ask coworkers for referrals, or search "CPA equity compensation" plus your city name.

Tools That Make This Easier

Use these free resources:

- Your company equity portal (check it weekly during vesting months)

- IRS Tax Withholding Estimator (irs.gov/W4app)

- IRS Direct Pay for estimated taxes (irs.gov/payments)

Consider paying for:

- Personal finance software like Quicken or Personal Capital (tracks cost basis automatically)

- Tax software like TurboTax Premier or H&R Block Premium (handles RSU reporting)

- A spreadsheet template (search "RSU tax tracking spreadsheet")

Your This-Week Action Plan

Do these five things before Friday:

-

Log into your equity portal. Find your total RSU value vesting this year. Write it down.

-

Go to irs.gov/W4app. Enter your salary plus RSU value. Find your tax bracket.

-

Calculate your gap:

(Your rate minus 22%) times RSU value -

If your gap is over $1,000, do ONE of these:

- Fill out a new W-4 at mycompany.com/payroll (or wherever your company handles this)

- Set up your first estimated payment at irs.gov/payments

-

Set four calendar reminders for quarterly check-ins: April 15, June 15, September 15, January 15.

That's it. Five concrete steps. You can finish this in one hour.

You've Got This

RSU taxes feel overwhelming because nobody teaches this stuff in school. But you don't need a finance degree. You just need a system.

The checklist above is your system. Do the before-vesting steps once. Do the at-vesting steps each time shares arrive. Do the quarterly reviews four times per year. Do the annual tasks once in December.

Most people spend more time picking a restaurant than planning their RSU taxes. You're already ahead by reading this far.

Start with the this-week action plan. Get those five items done. Then the rest of the checklist becomes easy because you've built the foundation.

Your RSUs are part of your compensation. You earned them. Now make sure you keep as much as possible after taxes.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis