RSU Cost Basis Explained: How to Avoid Paying Taxes Twice on Your Stock

Your guide to understanding what you actually paid for your vested shares (and why it matters at tax time)

Published March 1, 2026 · Updated March 1, 2026

RSU cost basis is the value of your shares when they vest, which becomes your starting point for calculating taxes when you sell. Understanding cost basis helps you avoid paying taxes twice on the same income and make smarter decisions about when to sell your vested shares.

Why Your RSU Cost Basis Matters: A Real Employee's Tax Surprise

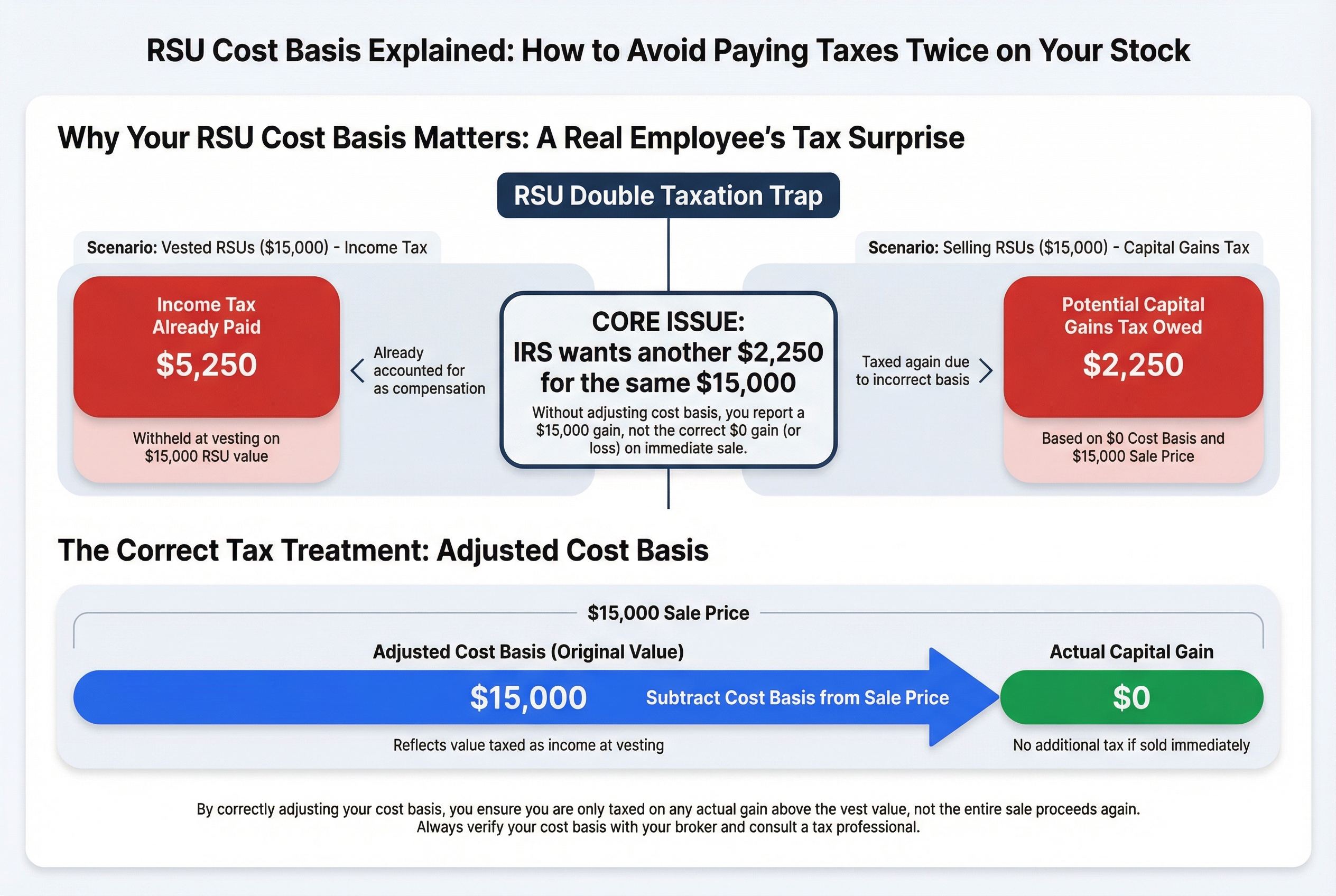

Sarah, a product manager at a tech company, sold 100 shares of her vested RSUs for $15,000. She felt good about the sale until tax season arrived.

Her 1099-B form from her brokerage showed a cost basis of $0. That made it look like she had a $15,000 capital gain. At a 15% capital gains rate, she owed $2,250 in taxes.

But here's the problem: Sarah already paid income tax on those shares when they vested a year earlier. Her company withheld taxes treating the shares as a $15,000 bonus. She paid roughly $5,250 in income tax back then.

Now the IRS wanted another $2,250 for the same $15,000. Sarah was about to pay taxes twice on the same money.

Think of cost basis like a receipt from a store. When you return an item, the receipt proves what you paid. Without it, the store might think you got the item for free. Cost basis is your proof that you already paid tax on your RSUs when they vested. It shows the IRS: "I already counted this as income once."

The $0 cost basis on Sarah's statement was wrong. Her actual cost basis was $15,000 (the value when the shares vested). With the correct cost basis, her capital gain was $0. She owed no additional tax on the sale.

This mistake happens to thousands of employees every year. Many pay the extra tax without realizing it. Others scramble to fix it after the fact.

The good news? This is completely preventable. You just need to understand what cost basis is and how to track it correctly. Let's start with the basics.

Sarah's Tax Surprise: Paying income tax ($5,250) and then being asked for capital gains tax ($2,250) on the same $15,000 value because the cost basis was reported as $0.

Sarah's Tax Surprise: Paying income tax ($5,250) and then being asked for capital gains tax ($2,250) on the same $15,000 value because the cost basis was reported as $0.

What Is RSU Cost Basis? (The Simple Definition)

Your cost basis is the dollar amount the IRS considers your "starting point" when you sell stock. Think of it like buying a used car. The cost basis is what you actually paid for the car, not what the dealer originally paid for it. When you sell the car later, you calculate your profit or loss based on what you paid, not what anyone else paid.

Here's the key thing to remember: Your RSU cost basis equals the fair market value of your shares on the day they vest.

Let's look at a real example:

Your company grants you 200 RSUs when the stock is $40 per share. One year later, 50 shares vest when the stock is $60 per share. Your cost basis for those 50 shares is $3,000 (50 shares × $60). It's NOT $2,000 (the original grant value) and it's definitely NOT $0.

Why does cost basis exist? The IRS uses it to figure out how much profit you made when you sell. If you sell those 50 shares later for $70 each ($3,500 total), you only owe capital gains tax on the $500 profit ($3,500 minus your $3,000 cost basis).

Two common mistakes people make:

- Thinking cost basis is $0. Wrong. You already paid income tax when the shares vested, so your cost basis reflects that.

- Using the grant price. Wrong. The stock price probably changed between grant and vesting.

Your cost basis gets set in stone on vesting day. That's the number you'll need later when you sell.

Now, here's where it gets tricky. The actual calculation involves tax withholding, which affects how many shares you really own.

How RSU Cost Basis Is Calculated (With Real Numbers)

Think of your RSUs like a paycheck. Your paycheck stub shows gross pay and net pay after taxes get taken out. RSUs work the same way. You have gross shares (the total that vest) and net shares (what you actually keep after tax withholding).

Here's the part that trips people up: your cost basis per share equals the stock price on the day your RSUs vest. Period. It doesn't matter how many shares got sold for taxes. Every share has the same cost basis.

The Step-by-Step Calculation

Let's walk through a real example:

Example 1: Sarah's March Vesting

- 100 RSUs vest on March 15

- Stock price on March 15:

$75 per share - Total value:

100 shares × $75 = $7,500(this is taxable income) - Tax withholding: 35 shares sold to cover taxes (worth

$2,625) - Shares Sarah keeps:

65 sharesland in her brokerage account

Sarah's cost basis: $75 per share for all 65 shares she kept, totaling $4,875

Not $0. Not $7,500. But $4,875.

Here's the key: those 35 shares that got sold for taxes? They had the same $75 cost basis. Your employer already paid taxes on all 100 shares at $75 each. The withholding just reduced how many shares you ended up with.

Another Example With Different Numbers

Example 2: Marcus's June Vesting

- 200 RSUs vest on June 1

- Stock price on June 1:

$120 per share - Total value:

200 shares × $120 = $24,000 - Tax withholding: 80 shares sold (worth

$9,600) - Shares Marcus keeps:

120 shares

Marcus's cost basis: $120 per share × 120 shares = $14,400 total

The formula is always:

- Cost basis per share = stock price on vesting date

- Total cost basis = shares you keep × price per share on vesting date

What Your Brokerage Should Do (But Doesn't Always)

Your brokerage (like E*TRADE, Fidelity, or Schwab) should automatically track this cost basis for you. They should record that you received 65 shares at $75 each or 120 shares at $120 each.

But here's the problem: sometimes they don't. Sometimes they show $0 cost basis. Sometimes they get the numbers wrong. That's why you need to understand this calculation yourself.

Now that you know your cost basis, let's talk about why it matters so much. You're about to pay taxes twice on these shares, but understanding cost basis ensures you don't pay the same tax twice.

The Two Tax Events: Why You Pay Taxes Twice (But Shouldn't Pay the Same Tax Twice)

Here's the truth that freaks everyone out: you DO pay taxes twice on RSUs. But here's the relief: you're not paying the same tax twice. Think of it like buying and selling a car. You pay sales tax when you buy it. Then years later, if you sell it for more than you paid, you pay capital gains tax on the profit. Two taxes, but on different things.

Your RSUs work the same way. There are two separate tax moments, and understanding both keeps you from accidentally overpaying.

Tax Event #1: Vesting Day (Ordinary Income Tax)

The day your RSUs vest, the IRS treats those shares like a cash bonus. You pay ordinary income tax on their full value.

Example: On January 10, 50 RSUs vest. The stock price is $100/share. You now owe ordinary income tax on $5,000 (50 shares x $100). Your employer withholds some for taxes, and the shares hit your account. Your cost basis is now locked in at $100/share.

This is the "buying the car" moment. You've paid your first tax.

Tax Event #2: Sale Day (Capital Gains Tax)

When you eventually sell those shares, you only pay capital gains tax on the increase in value since vesting.

Same example continues: On June 15, you sell all 50 shares. The price has jumped to $120/share. You receive $6,000 total.

Do you pay tax on the full $6,000? No. You only pay capital gains tax on the $1,000 gain ($6,000 sale price minus $5,000 cost basis). That $5,000? You already paid tax on it back in January.

Your Cost Basis Is Your Receipt

Your cost basis ($100/share in this example) is your proof to the IRS: "I already paid ordinary income tax on this amount. Only tax me on the growth."

Without tracking this cost basis correctly, you'd pay ordinary income tax at vesting AND capital gains tax on the same original $5,000. That's actual double taxation, and it's exactly what we're trying to avoid.

This two-tax system isn't a penalty. It's just how equity compensation works. The key is making sure the IRS knows your cost basis so you only pay capital gains on the real profit.

Now let's break down exactly how much tax you'll owe at each event.

Stop Paying Double Tax on Your RSUs (Common 1099-B Mistake) | McCarthy Tax Preparation

How Much Tax You'll Actually Pay (Income Tax at Vesting vs. Capital Gains at Sale)

Think of RSU taxes like paying tolls on two different roads. The first toll (at vesting) is expensive. The second toll (when you sell) might be cheaper, but only if you take the right route.

The Vesting Tax: Ordinary Income (The Expensive Toll)

When your RSUs vest, the IRS treats that money like your regular paycheck. You pay ordinary income tax at your marginal rate.

Your rate depends on your total income:

- 22% if you earn $47,150 to $100,525 (single)

- 24% if you earn $100,525 to $191,950

- 32% if you earn $191,950 to $243,725

- 35% if you earn $243,725 to $609,350

- 37% if you earn over $609,350

Here's the problem: your employer typically only withholds 22% federal tax, even if you're in a higher bracket.

Real example: You're in the 35% tax bracket. 100 RSUs vest at $100 per share. That's $10,000 in income.

- Your employer withholds: $2,200 (22%)

- What you actually owe: $3,500 (35%)

- Surprise tax bill in April: $1,300

This gap catches people off guard every year. You got shares worth $10,000, but only saw $7,800 after withholding. Then you owe another $1,300 at tax time.

The Sale Tax: Capital Gains (The Potentially Cheaper Toll)

When you sell your shares, you pay tax on any gain above your cost basis. How much depends on how long you held them.

Short-term gains (held less than 1 year): Taxed as ordinary income again. Same rates as above (22% to 37%).

Long-term gains (held over 1 year): Taxed at lower capital gains rates:

- 0% if your income is under $47,025 (single)

- 15% if your income is $47,025 to $518,900

- 20% if your income is over $518,900

Continuing our example: You hold those 100 shares for 2 years. They grow to $130 per share. You sell for $13,000.

- Your cost basis: $10,000 (what you already paid tax on)

- Your gain: $3,000

- Tax on the gain: $450 (15% long-term rate)

That's way better than the 35% you'd pay on ordinary income. Holding for over a year saved you $600 in taxes ($1,050 vs. $450).

Why This Matters for Cost Basis

Your cost basis determines how much of your sale is taxable gain. Get it wrong, and you might pay tax on that $10,000 all over again instead of just the $3,000 growth.

Next, we'll look at the most common cost basis mistake: the dreaded $0 cost basis problem that makes brokers think you owe tax on everything.

Avoid an RSU Double Tax

The Dreaded $0 Cost Basis Problem (And How to Fix It)

Picture this: you sell your RSU shares and get a Form 1099-B in January. The form shows you sold stock for $9,600. Great! But in the cost basis column, it says $0.

This is like a store receipt that didn't print the item price. You still paid for it. The IRS just doesn't see the proof.

Why Your 1099-B Shows $0 Cost Basis

This happens for two main reasons:

-

Your brokerage never received the cost basis data from your employer. When RSUs vest, your company reports the income on your W-2. But sometimes that information doesn't make it to your brokerage's system.

-

You transferred shares between accounts. Maybe you moved shares from E*TRADE to Fidelity. The new brokerage doesn't have your original vesting records.

How to Spot the Problem

Look at your Form 1099-B in Box 1e (cost basis). If you see:

$0.00- A blank space

- "Basis not reported to IRS" checked in Box 3

You have a problem.

What Happens If You Do Nothing

The IRS sees a sale for $9,600 with a cost basis of $0. They think you made a $9,600 profit. You'll pay capital gains tax on money you already paid income tax on. That's paying taxes twice on the same dollars.

Let's say you're in the 24% tax bracket. You'd pay an extra $1,440 in federal taxes (15% capital gains on $9,600). All because of missing paperwork.

How to Fix It: The Step-by-Step Process

Step 1: Find your true cost basis

Check these places in order:

- Your pay stub from the vesting date (look for "RSU income" or similar)

- Your employer's equity portal (Schwab, Fidelity, E*TRADE)

- Brokerage statements from the day shares vested

- Your company's HR or stock plan administrator

Step 2: Calculate what you actually paid

You sell 80 shares for $9,600 total ($120 per share). You find records showing these shares vested when the stock was $110 per share.

Your true cost basis: 80 shares x $110 = $8,800

Your actual gain: $9,600 - $8,800 = $800

Step 3: Report the correction on Form 8949

Form 8949 is where you fix 1099-B errors. Here's what you write:

- Column (a): Description of stock and number of shares

- Column (d): Proceeds from 1099-B:

$9,600 - Column (e): Your correct cost basis:

$8,800 - Column (f): Code "B" (for basis adjustment)

- Column (g): The adjustment amount:

$8,800

In the adjustment column, write "Cost basis per employer records."

Step 4: The math that saves you money

Wrong way (using $0 basis):

- Sale proceeds: $9,600

- Cost basis: $0

- Taxable gain: $9,600

- Tax owed (15% capital gains): $1,440

Right way (using correct basis):

- Sale proceeds: $9,600

- Cost basis: $8,800

- Taxable gain: $800

- Tax owed (15% capital gains): $120

You just saved $1,320 by filling out one form correctly.

This Is Common and Fixable

Thousands of employees see $0 cost basis on their 1099-B every year. It's not your fault. The systems that track RSU vesting and stock sales often don't talk to each other.

The key: keep your own records. Don't rely on your brokerage to get it right.

Now that you know how to fix cost basis errors, let's look at other situations that can change your cost basis after you receive your shares.

RSU Cost Basis Reporting 2026: Form 8949, Code B & The "Zero Basis" Error

When Cost Basis Changes: Stock Splits, Dividends, and Account Transfers

Your cost basis isn't always set in stone. Corporate actions and account moves can change the numbers you see, but here's the key: the total dollar amount stays the same.

Stock Splits: Same Pizza, Smaller Slices

Think of a stock split like cutting a pizza. If you cut one slice into two pieces, you still have the same amount of pizza, just in smaller pieces.

Here's a real example: You own 50 shares with an $100 cost basis each. That's $5,000 total. Your company announces a 2-for-1 stock split. After the split, you own 100 shares with a $50 cost basis each. Still $5,000 total.

The math:

- Before split: 50 shares × $100 = $5,000

- After split: 100 shares × $50 = $5,000

The number of shares doubled. The cost basis per share got cut in half. Your total basis didn't change.

Stock Dividends Work the Same Way

When companies pay dividends in stock instead of cash, you get additional shares. Your cost basis spreads across all shares, including the new ones.

You had 100 shares at $80 each ($8,000 total). You receive a 10% stock dividend, giving you 10 more shares. Your cost basis becomes 110 shares at $72.73 each (still $8,000 total).

The Account Transfer Danger Zone

Here's where things get messy. You transfer your 400 shares (from that 4-for-1 split example) to a new brokerage. Sometimes the cost basis transfers correctly. Sometimes it doesn't.

What often happens: The new brokerage shows $0 cost basis or the wrong amount. This isn't just annoying. If you sell without fixing it, the IRS thinks you made a huge profit and you'll pay tax on money you already paid tax on.

Your safety net: Keep your original vesting documents. They show you paid tax on $8,000 when the shares vested. That's your proof of cost basis, no matter what your new brokerage says.

Your Tracking Checklist for Corporate Actions

When a stock split or dividend happens:

- Note the split ratio or dividend percentage

- Calculate your new per-share cost basis (total basis ÷ new share count)

- Verify your brokerage updated the numbers correctly

- Save the company's announcement about the corporate action

When transferring accounts:

- Print cost basis reports from your old brokerage before transferring

- Check that cost basis transferred correctly to the new brokerage

- Keep your original RSU vesting statements as backup proof

- Contact the new brokerage immediately if numbers look wrong

Bottom line: Corporate actions change how many shares you own and the cost basis per share, but your total cost basis stays the same. Always keep your vesting records. They're your insurance policy against lost or incorrect cost basis data.

Now that you understand how cost basis can change, let's tackle the big question: should you sell your RSUs right away or hold them?

Should You Sell Immediately or Hold? How Cost Basis Affects Your Decision

Here's the good news: your cost basis is locked in at vesting, no matter when you sell. The question is what happens after that.

Think of holding your vested RSUs like holding onto a gift card. You could use it today and get exactly what you expect. Or you could wait and hope for a better sale, but you're also risking the store could have a going-out-of-business clearance instead.

The Three Paths After Your RSUs Vest

Let's say 50 shares vest when your company stock is at $100. Your cost basis is $5,000 (you already paid income tax on this at vesting). Here's what happens in each scenario:

Scenario A: Sell immediately at $100

- Sale proceeds: $5,000

- Cost basis: $5,000

- Capital gain: $0

- Capital gains tax: $0

You walk away clean. No additional tax. No risk.

Scenario B: Hold 8 months, sell at $110

- Sale proceeds: $5,500

- Cost basis: $5,000

- Capital gain: $500

- Tax rate: 35% (short-term, taxed as ordinary income)

- Capital gains tax: $175

You made $325 after tax, but you took on 8 months of risk that the stock could have dropped below $100.

Scenario C: Hold 15 months, sell at $110

- Sale proceeds: $5,500

- Cost basis: $5,000

- Capital gain: $500

- Tax rate: 15% (long-term capital gains)

- Capital gains tax: $75

You made $425 after tax. Better than Scenario B, but you risked 15 months of potential stock decline.

The Real Risk: Your Stock Could Drop

Here's what many employees miss. In Scenario C, yes, you saved $100 in taxes by waiting for long-term rates. But what if the stock dropped to $90 during those 15 months?

Now you're sitting on a $500 loss compared to your cost basis. You held for over a year, hoping to save on taxes, and instead you lost money.

A Simple Decision Framework

Consider selling immediately if:

- You're in a high tax bracket (the tax savings from long-term rates won't be huge)

- More than 10% of your net worth is in company stock

- You need the cash for a specific goal within 12 months

- Your company stock has already had a big run-up

Consider holding for long-term gains if:

- You're in a lower tax bracket (22% or below)

- Company stock is less than 5% of your portfolio

- You have a strong emergency fund already

- You believe in your company's long-term prospects

- You can stomach watching the stock price bounce around

The Math on Tax Savings

The difference between short-term and long-term capital gains rates varies by your income:

- High earners: Short-term at 37%, long-term at 20% = 17% difference

- Middle earners: Short-term at 24%, long-term at 15% = 9% difference

- Lower earners: Short-term at 12%, long-term at 0% = 12% difference

On a $10,000 gain, that 17% difference saves you $1,700. Sounds great, until you realize you're risking $10,000+ in stock value to save $1,700 in taxes.

What Most Financial Advisors Recommend

The classic advice: don't let the tax tail wag the investment dog. Translation: don't hold a risky, concentrated stock position just to save on taxes.

If you work at a stable company and company stock is a small part of your wealth, holding for long-term rates might make sense. But if you're already heavily concentrated in your employer's stock (hello, tech employees), selling at vest is often the smarter move.

Remember, your cost basis protects you from paying tax twice on the same income. But it doesn't protect you from a falling stock price.

Now that you know how to think about selling versus holding, let's talk about the mistakes that trip up even experienced employees, mistakes that can cost you thousands in unnecessary taxes.

What Your HR Won't Tell You: The Real Cost Basis Mistakes Employees Make

Here's what most companies won't tell you: tracking your RSU cost basis is your responsibility, not theirs. And the information you need passes through a game of telephone from your employer to payroll to your brokerage. Sometimes, critical details get lost along the way.

Let's talk about the mistakes that cost employees real money.

Mistake #1: Assuming Your Brokerage Has the Correct Cost Basis

Your brokerage statement might show $0 cost basis for RSUs that vested years ago. Don't assume this is right.

Think of it like this: your employer knows what you paid in taxes when shares vested. Your brokerage only knows when shares arrived in your account. They're looking at different pieces of the puzzle.

Real impact: You could pay tax on $20,000 in gains when your actual gain was only $2,000.

Mistake #2: Not Saving Vesting Day Documents

The day your RSUs vest, your pay stub shows the share value. That's your proof of cost basis.

Most employees delete these emails or never download the pay stub. Two years later when they sell, they have no documentation.

What to save:

- Pay stubs from vesting dates

- Screenshots from your equity portal showing vesting events

- Year-end equity compensation statements

Mistake #3: Forgetting About Shares From Previous Employers

Here's where it gets messy. Maria changed jobs in 2022. In 2024, she sells old company RSUs still sitting in her Schwab account.

The 1099-B shows $0 cost basis. Why? Those shares originally vested at E*TRADE. When she transferred to Schwab, the cost basis didn't come along.

She didn't keep her 2022 pay stubs. Now she's scrambling to contact her old employer's equity team to reconstruct her $12,000 cost basis. If she can't prove it, she'll pay tax on the full $15,000 sale amount instead of just the $3,000 actual gain.

The fix: Before leaving a job, download every equity document you can find. You won't have portal access after you leave.

Mistake #4: Checking Your 1099-B Only at Tax Time

You get your 1099-B in February. You notice wrong cost basis in March. Good luck gathering pay stubs from 2-3 years ago now.

Better approach: Check your brokerage's cost basis tracking quarterly. Fix errors while you still have easy access to records.

Mistake #5: Thinking 22% Withholding Covers Your Tax Bill

Your employer withholds 22% for federal taxes at vesting. But if you're in the 32% or 35% tax bracket, you'll owe more in April.

This isn't a cost basis mistake, but it trips up employees who think they're done paying tax when RSUs vest.

The math: 100 RSUs vest at $200 each = $20,000 income. Your employer withholds $4,400 (22%). If you're actually in the 35% bracket, you owe $7,000 total. That's a $2,600 surprise.

Mistake #6: Not Understanding the Information Gap

Your HR team manages grants and vesting schedules. They're not tax advisors. They assume your brokerage handles cost basis tracking.

Your brokerage receives shares. They're not connected to your payroll system. They don't automatically know what taxes you paid.

The gap: Your employer reports vesting value to the IRS on your W-2. Your brokerage reports sale proceeds on your 1099-B. Nobody automatically connects these dots for you.

Mistake #7: Trusting Account Transfers to Preserve Cost Basis

When you transfer RSUs between brokerages (like from E*TRADE to Fidelity), the cost basis should transfer too. But it doesn't always happen correctly.

Check immediately: Log into your new brokerage within a week of transfer. Verify every share shows the correct cost basis and acquisition date.

Why This Happens

Your HR team isn't hiding information from you. They genuinely believe the system works. They think:

- The brokerage receives all necessary data

- Your tax software pulls everything together

- You'll figure it out or ask questions

But most employees don't know what questions to ask until they're staring at a huge tax bill.

Now that you know the common mistakes, let's create a simple system to avoid them. The next section gives you a checklist of exactly what to save and when.

Your Cost Basis Tracking Checklist: What to Save and When

Think of cost basis records like receipts for expensive purchases. You need proof of what you paid in case the IRS questions your tax return or your brokerage gets the numbers wrong.

The good news: you don't need a complicated system. A simple folder and spreadsheet will protect you from paying thousands in extra taxes.

On Vesting Day (Save Within 24 Hours)

Every time RSUs vest, grab these three documents:

1. Your pay stub showing RSU income

- Look for a line item like "RSU Income" or "Equity Compensation"

- This proves what amount got taxed as regular income

2. Screenshot from your equity portal (like E*TRADE or Fidelity)

- Shows exactly how many shares vested and at what price

- Captures the official vesting date

3. Brokerage confirmation email

- Shows how many shares you actually received after tax withholding

- Example: "25 shares vested, 7 sold for taxes, 18 deposited to your account"

Real example: On June 15, 25 shares vest at $88. Save your June 30 pay stub showing $2,200 RSU income. Screenshot your equity portal showing 25 shares vested at $88. Save the Fidelity email confirming 18 shares deposited (after 7 sold for taxes).

Your Simple Tracking Spreadsheet

Create a spreadsheet with these columns:

- Vesting date

- Shares vested

- Price per share

- Total cost basis

- Shares kept after taxes

- Sale date (fill in later)

- Sale price (fill in later)

For the June 15 example above, enter: 6/15/2024 | 25 shares | $88 | $2,200 total basis | 18 shares kept

Quarterly Maintenance (15 Minutes Every 3 Months)

Download and save your brokerage statements. Check that your share count matches your spreadsheet.

If you see mystery shares or missing shares, call your brokerage immediately. Mistakes are easier to fix when they are fresh.

At Year End

Save your employer's equity compensation summary. Most companies send this in January. It lists every vesting event for the tax year.

Compare it to your spreadsheet. They should match perfectly.

When You Sell Shares

Save the trade confirmation immediately. Write down:

- How many shares you sold

- What price you got

- Which vesting date those shares came from (if you can tell)

Update your spreadsheet the same day.

At Tax Time (Before You File)

This is critical. When you get your 1099-B form in February, compare it to your records before filing your taxes.

Look for these red flags:

- Cost basis shows

$0or is blank - Cost basis is way lower than what you know you paid

- Shares are missing from the form

If you spot problems, call your brokerage and request a corrected 1099-B. Do this in February, not April 14th.

How Long to Keep Records

Keep everything for at least 7 years after you sell the last share from a vesting event.

Why 7 years? The IRS can audit returns up to 6 years back in some cases. The extra year gives you a safety buffer.

Example timeline: Your June 2024 RSUs vest. You sell the last share in March 2025. Keep all records until at least 2032.

Your Simple Filing System

Create one folder (digital or paper) named "RSU Records, [Your Company Name]."

Inside, create subfolders by year: "2024 Vestings," "2025 Vestings," etc.

Drop all documents into the right year folder. That is it.

If you prefer digital, scan paper documents and save PDFs in Google Drive or Dropbox. Name files clearly: "2024-06-15 Vesting - 25 shares at $88.pdf"

The 5-Minute Monthly Check

Once a month, spend 5 minutes reviewing:

- Did any RSUs vest this month? If yes, did I save the documents?

- Does my brokerage account show the right number of shares?

- Is my spreadsheet up to date?

This tiny habit prevents massive headaches at tax time.

Now that you have a system for tracking your cost basis, let's put it all together with a clear action plan you can start today.

What to Do Next: Your Action Plan for Getting Cost Basis Right

Think of cost basis tracking like maintaining your car. Regular oil changes are easy. Rebuilding the engine after years of neglect? Expensive and painful. The same goes for your RSU records.

Here's exactly what to do based on where you are right now.

If Your RSUs Haven't Vested Yet

You're in the best position. Set up your system now:

- This week: Bookmark your equity compensation portal (Schwab, E*TRADE, Fidelity, etc.). Save the login.

- Write down your vesting schedule. Know exactly when shares will vest and how many.

- Set calendar reminders for each vesting date with this note: "Save RSU documents today."

When vesting happens, you'll be ready to grab everything while it's fresh.

If RSUs Vested in the Last 6 Months

Do this today. Seriously, today:

- Log into your equity portal and download all vesting confirmations from this year.

- Save your pay stubs from each vesting month (they show the income tax withheld).

- Create a simple spreadsheet: Date, Number of Shares, Price Per Share, Total Value, Taxes Withheld.

Documents get harder to find after six months. Your future self will thank you.

If You're Planning to Sell Soon

Let's say you're selling 100 shares next month to buy a house. Here's your action plan:

- This week: Log into your brokerage account. Find those 100 shares and check what cost basis is listed.

- Compare it to your records from when they vested. If 100 shares vested at $150 each, your cost basis should show $15,000.

- If you see $0 or the wrong number, call your brokerage immediately. Fix it before you sell.

- If your records are incomplete, contact your company's equity team now for historical vesting data.

Don't wait until after you sell. Fixing cost basis beforehand takes one phone call. Correcting your tax return later? That's an amended return, potential penalties, and a headache.

If You Already Sold and Got a 1099-B

Open that 1099-B right now. Look at the cost basis column:

- Shows the right amount? You're good. Just verify it matches your records when you file taxes.

- Shows $0 or way too low? Gather your vesting documents immediately. You'll need them to correct your tax return and prove you already paid income tax.

- Missing some sales? Contact your brokerage. They might have sent multiple 1099-B forms.

If the cost basis is wrong, you have two options: ask your brokerage to issue a corrected 1099-B, or report the correct cost basis on Form 8949 when you file. A tax professional can help you choose.

For Everyone: Set It and Forget It

Create one calendar reminder that repeats on every vesting date: "Download RSU documents and save to Cost Basis folder."

That's it. Five minutes, four times a year (or however often you vest). This simple habit prevents thousands in potential double taxation.

When to Call in a Pro

Consider talking to a tax professional if:

- You have multiple years of RSU sales and messy records

- You've changed jobs and transferred shares between brokerages

- You're dealing with stock splits, mergers, or company acquisitions

- Your 1099-B shows major cost basis errors and you're not sure how to fix them

A CPA who specializes in equity compensation costs $200 to $500 for most situations. That's cheap compared to paying capital gains tax on money you already paid income tax on.

Bottom line: Your cost basis is your proof that you already paid tax once. Track it carefully, save your documents, and you'll never pay the same tax twice. You've got this.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis