Managing RSU Concentration Risk: How to Protect Your Wealth When Your Company Stock Takes Over Your Portfolio

Simple strategies to diversify when your company stock dominates your net worth

Published March 1, 2026 · Updated March 1, 2026

When your RSUs grow to represent a large chunk of your wealth, you're exposed to concentration risk - the danger of having too many eggs in one basket. This guide teaches you how to recognize when you have too much company stock, why it's risky, and practical strategies to diversify without triggering unnecessary taxes or missing out on future growth.

The Day You Realize You're All-In on One Bet

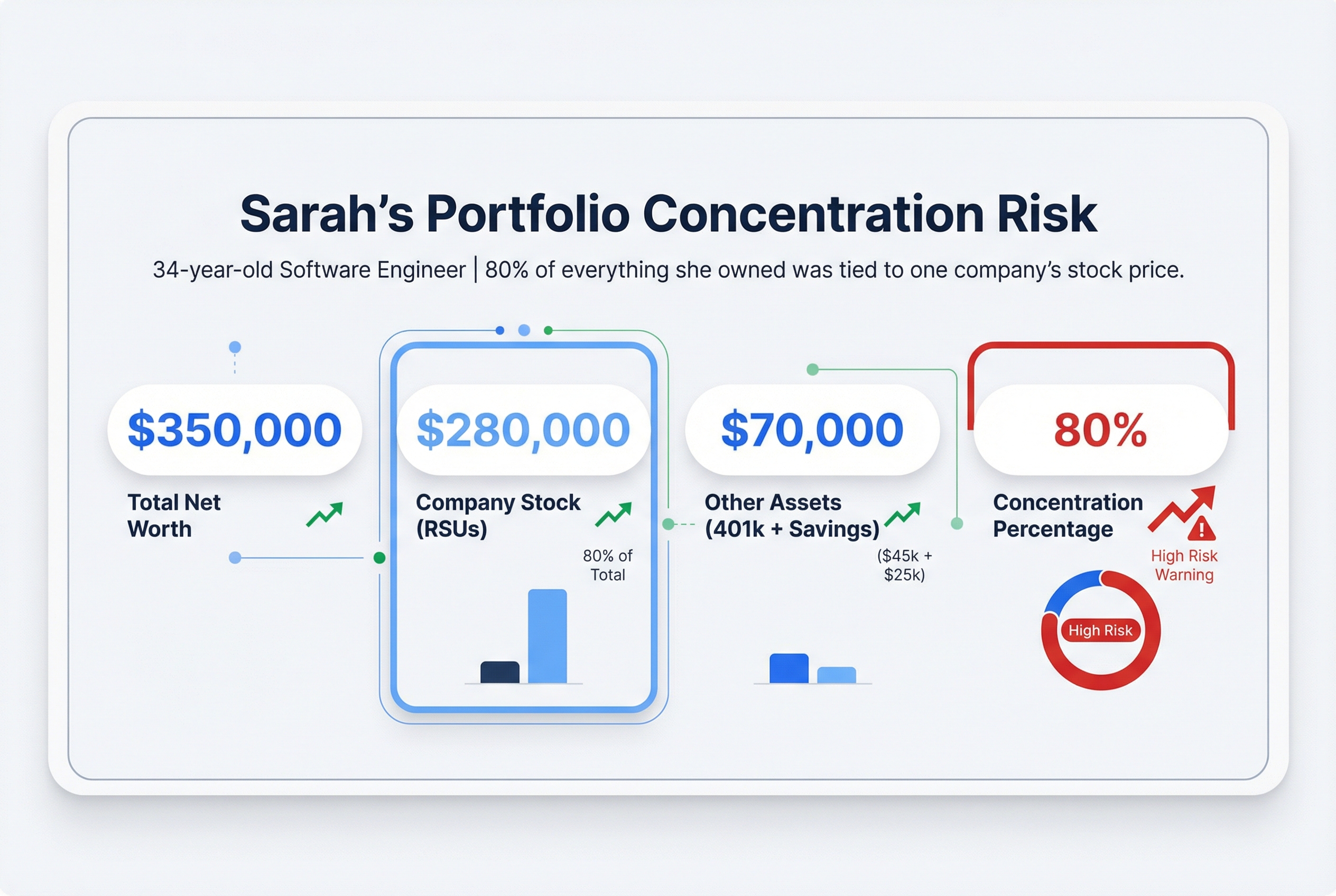

Sarah, a 34-year-old software engineer at a cloud company, logged into her brokerage account on a Tuesday morning. She wanted to check her net worth before talking to a financial advisor.

Here's what she saw:

- Company stock: $280,000

- 401(k): $45,000

- Savings account: $25,000

- Total net worth: $350,000

She stared at the screen. 80% of everything she owned was tied to one company's stock price.

This is the moment most employees discover they have a concentration problem. RSUs vest quietly over years. You don't feel them accumulating the way you feel a paycheck hitting your account. But they pile up, especially when your company's stock keeps climbing.

Here's the real risk: The same company pays your salary AND holds most of your wealth. If something goes wrong, you lose on both fronts. Think of it like keeping 80% of your life savings in a single lottery ticket. You might win big. Or you might lose everything.

When tech stocks dropped 30% in 2022, Sarah would have lost $84,000. That's almost two years of emergency fund savings and her down payment money, gone.

Try this thought experiment: If your company handed you $280,000 in cash today, would you immediately use it to buy $280,000 worth of their stock? Most people say no. But that's exactly the position you're in when RSUs accumulate unchecked.

This isn't about whether your company is good or bad. Great companies have bad years. This is about basic risk management. You need to understand what you actually own. RSUs 101: Guide to Equity, Taxes & Financial Planning

Sarah's portfolio breakdown revealed an 80% concentration risk tied to a single company stock.

Sarah's portfolio breakdown revealed an 80% concentration risk tied to a single company stock.

What Is Concentration Risk? (And Why 10% Is the Magic Number)

Concentration risk means you have too much of your wealth tied to one investment. It's the financial version of carrying all your eggs in one basket. If you trip, you lose everything.

Here's the classic rule: No single stock should make up more than 10% of your investable assets. This isn't some arbitrary number. It comes from decades of research showing that diversification reduces risk without killing your returns. Concentrated stock position? Direct indexing can help.

Think of it like this. Imagine you own a restaurant and you also invest your life savings in restaurant stocks. If a recession hits and people stop eating out, you lose your job AND your savings at the same time. That's concentration risk in action.

Your company stock already controls a huge part of your financial life. It pays your salary. It funds your health insurance. It determines your career growth. When you load up on company shares through RSUs, you're doubling down on the same bet.

Meet James, a software engineer with $400,000 in investable assets (not counting his house). Using the 10% rule:

- Safe concentration = $40,000 in company stock (10% of $400,000)

- James actually has $180,000 in company stock = 45% of his portfolio

- He's 35 percentage points over the recommended threshold

Even if his company is crushing it right now, James is taking unnecessary risk. If he got laid off and the stock dropped 40% at the same time (which often happens when companies announce layoffs), he'd lose both his income and $72,000 in wealth at the worst possible time.

This is exactly why company executives are often required to diversify their holdings. They know something important: the goal isn't zero company stock. It's balanced exposure.

Diversification doesn't mean you hate your company or think it will fail. It means you're spreading your eggs across multiple baskets. You can still believe in your company's future while protecting yourself from the unexpected.

So how do you figure out if you're overexposed? Let's run the numbers.

Should I Sell My Company Stock? The Truth About Concentration Risk

The Two Risks You're Actually Taking (That Most People Miss)

Think about weather risk for a second. There's the general risk that it might rain today (affects everyone in your city). Then there's the specific risk that a tree falls on your house (only affects you). Your company stock works the same way.

Market risk is like the rain. When the economy struggles, interest rates spike, or a recession hits, pretty much all stocks drop together. You can't avoid this risk. Even if you buy an S&P 500 index fund, you're still exposed to market risk.

Company-specific risk is like that tree falling on your house. This is the risk that your specific employer faces problems that other companies don't:

- A product launch flops

- Your CEO gets caught in a scandal

- A competitor releases something better

- Regulatory changes hammer your industry

- The company misses earnings badly

Here's the critical part: your company stock has both risks stacked on top of each other. An index fund spreads company-specific risk across 500 different companies. If one tree falls, you barely notice. But when you hold individual company stock, you're taking the full hit from both risks.

The Double Whammy You Need to Understand

When companies face financial trouble, two terrible things often happen at once. The stock price crashes AND they start laying people off.

Consider two real scenarios from 2022:

Scenario 1: Maria works at a big tech company and holds $200,000 in company stock. The market drops 20%. Her stock drops 20% = $40,000 loss. Painful, but she keeps her job.

Scenario 2: David works at Meta and holds $200,000 in Meta stock. The market drops 20%, but Meta drops 64% due to company-specific problems (metaverse concerns, crashing ad revenue). David loses $128,000. Then Meta announces 11,000 layoffs. Suddenly David faces losing his income right when his savings just got crushed.

Same market conditions. But David's concentration in one company tripled his losses and put his paycheck at risk simultaneously.

Even Great Companies Have Bad Decades

You might think "but my company is different, we're crushing it." Maybe you are. But past performance tells you nothing about the next 10 years.

IBM dominated technology for decades. Then it didn't. General Electric was America's most valuable company. Then it lost 75% of its value over 20 years. Employees at both companies who kept their stock out of loyalty watched their retirement funds evaporate.

The 2022-2023 tech layoffs drove this home. Amazon, Google, Microsoft, Salesforce, all top-tier companies, all cut thousands of workers while their stocks dropped 30-50%. These weren't failing companies. They were industry leaders hitting rough patches.

The most extreme example? Lehman Brothers in 2008. Employees didn't just lose their jobs. They lost an average of 30% of their net worth that was tied up in company stock. Retirement accounts built over 20-year careers vanished in weeks.

You're not being paranoid by diversifying. You're being realistic about how risk actually works.

Now that you understand what you're risking, let's figure out exactly how exposed you are right now.

RSU Tax Trap: The Concentration Mistake That Destroys Wealth

Calculate Your Real Exposure (The 5-Minute Portfolio Checkup)

Think of this like taking inventory before cooking a big meal. You need to know what ingredients you have before you can tell if you're missing something important.

Here's your five-minute portfolio checkup. Grab your phone and pull up your accounts.

Step 1: Add Up Your Company Stock

Count everything you own right now:

- Vested RSUs in your brokerage account

- ESPP shares you've purchased

- Exercised stock options (if you have them)

- Company stock in your 401(k) (yes, this counts)

Write down the total current value. This is your company stock number.

Step 2: Add Up Everything Else You Could Invest

This is your "investable assets." Include:

- 401(k) balance (all of it, not just company stock)

- IRA or Roth IRA

- Taxable brokerage accounts

- High-yield savings or money market funds

- Any cash you're planning to invest

Don't include: Your house, cars, furniture, or anything you can't easily sell and reinvest. Those aren't investable assets.

Step 3: Do the Math

Here's the formula:

(Company Stock Value / Total Investable Assets) x 100 = Your Concentration %

Let's calculate for Rachel, a product manager at a tech company:

- Vested company stock in brokerage:

$120,000 - 401(k) balance:

$85,000 - IRA:

$30,000 - Savings/emergency fund:

$15,000 - Total investable assets:

$250,000

Rachel's current concentration: ($120,000 / $250,000) x 100 = 48%

That puts Rachel in the orange zone. But wait, there's more.

Step 4: Check Your Future Exposure

Rachel has $80,000 in RSUs vesting over the next year. Let's recalculate:

- Future company stock:

$200,000(current plus vesting) - Future total assets:

$330,000(current plus vesting) - Future concentration:

($200,000 / $330,000) x 100 = 61%

Rachel is heading into the red zone. She needs a diversification plan before those RSUs vest, not after.

Your Risk Zones

Green zone (under 10%): You're good. Keep monitoring quarterly.

Yellow zone (10-25%): Elevated risk. Consider diversifying, especially if more RSUs are vesting soon.

Orange zone (25-50%): Significant risk. Make a concrete plan to diversify over the next 6-12 months.

Red zone (over 50%): Urgent. Your financial security depends too much on one company. Diversify as soon as practical.

Most people discover they're in the orange or red zone. If that's you, don't panic. You have options, and we'll cover three proven strategies next.

Strategy 1: The Automatic Diversifier (Sell a Fixed Percentage at Each Vest)

Think of this strategy like a thermostat for your portfolio. You set the temperature once, and it automatically keeps your house comfortable without you constantly fiddling with the dial. That's what selling a fixed percentage at each vest does. It maintains balance without requiring constant decisions.

Here's how it works: Every time RSUs vest, you immediately sell 25%, 50%, or 75% of those shares. You take the cash and invest it in diversified index funds. The rest stays in company stock.

This is the most common strategy financial advisors recommend. Why? It removes emotion from the equation. No more lying awake wondering "Should I sell now? What if it goes up tomorrow?" You've already decided. The rule does the work for you.

The best part: Selling at vest means zero additional capital gains tax. When your RSUs vest, the IRS taxes you on their value that day. If you sell immediately, you're selling at the same price the IRS already taxed you at. No extra tax bill.

How to Pick Your Percentage

Your concentration level tells you how aggressive to be:

- Under 20% concentrated? Sell 25% at each vest. You're in decent shape already.

- 20% to 40% concentrated? Sell 50% at each vest. This is the sweet spot for most people.

- Over 40% concentrated? Sell 75% at each vest. You need to diversify faster.

Real Example: Tom's Salesforce Strategy

Tom works at Salesforce. Every quarter, $20,000 worth of RSUs vest. He calculates his concentration and finds he's at 35%. Yikes. He decides on a 50% automatic sell rule.

Quarter 1: $20,000 vests. He immediately sells $10,000 (50%) and invests it in a total market index fund. He keeps $10,000 in Salesforce stock.

Quarter 2: Another $20,000 vests. Same drill. Sells $10,000, keeps $10,000.

After one year, Tom has sold $40,000 and diversified it. He still holds $40,000 in company stock. His concentration has dropped from 35% to 28%. He's on track to reach the 20% yellow zone within 18 months.

The kicker: If Salesforce stock goes up, Tom still benefits from the 50% he kept. He's not leaving all the upside on the table.

Making It Truly Automatic

Most brokers (E*TRADE, Fidelity, Schwab) let you set up automatic sales. You configure it once: "Sell 50% of shares immediately when they vest." Then you forget about it. The system handles everything.

This removes FOMO (fear of missing out) and analysis paralysis. You're not checking stock prices daily. You're not second-guessing yourself. The plan runs on autopilot.

One warning: This strategy works great in normal times. But what about blackout periods when you can't trade? That's where Strategy 3 comes in. First, though, let's talk about the tax impact of selling, because that's what stops most people from pulling the trigger.

Understanding the Tax Impact of Your Diversification Strategy

Think of RSU vesting like buying a car. The moment you drive it off the lot, the IRS decides what it's worth and sends you a tax bill. That value is locked in. If you sell the car immediately for the same price, no extra tax. If you hold it and the price changes, that's when new tax consequences kick in.

Here's the part most people miss: you already paid tax when your RSUs vested. Selling immediately doesn't create additional taxes.

How RSUs Get Taxed at Vest

When your RSUs vest, the IRS treats them as ordinary income. Just like your salary.

Let's say 500 shares vest when your stock is trading at $100. That's $50,000 of income. If you're in the 32% tax bracket, you owe $16,000 in taxes.

Your company automatically withholds shares to cover this tax bill. They typically withhold 22% for federal taxes, but that might not be enough if you're in a higher bracket. In our example, they'd withhold 110 shares (worth $11,000) for the standard 22%, leaving you short $5,000 that you'll owe at tax time.

The key insight: The IRS has already decided your shares are worth $100 each. That's your cost basis, the price you "paid" for tax purposes.

Why Selling at Vest Is Tax-Neutral

If you sell those shares immediately at $100, you're selling them for exactly what the IRS said they're worth. No gain. No additional tax.

It's like selling that car for the exact price you paid. The dealership already collected sales tax. Selling it immediately doesn't trigger another tax event.

This surprises people. They think, "If I sell, I'll get hit with huge taxes." But you were already hit. Selling at vest just converts shares to cash without adding to your tax bill.

What Happens If You Hold

Holding shares after they vest creates new tax events based on price changes.

Short-term capital gains (held less than 1 year): Taxed as ordinary income, same as your salary. If you're in the 32% bracket, you pay 32% on any gains.

Long-term capital gains (held more than 1 year): Taxed at lower rates of 0%, 15%, or 20%, depending on your income. Most people pay 15%.

Here's where the math gets interesting.

Jessica's Three Scenarios

Jessica works at a tech company. Her RSUs vest: 500 shares at $100 each = $50,000 worth of stock.

The IRS taxes this as $50,000 of ordinary income at her 32% tax rate = $16,000 in taxes.

Her company withholds 160 shares (worth $16,000) to cover the tax bill.

Jessica receives 340 shares in her brokerage account, worth $34,000.

Scenario A: Sell immediately

- She sells all 340 shares at $100 = $34,000

- Capital gains = $0 (sold at same price as vest)

- She invests $34,000 in a diversified index fund

- Total after-tax: $34,000

Scenario B: Hold for 2 years, stock rises

- Stock climbs to $130

- She sells 340 shares = $44,200

- Capital gains = $10,200 ($130 - $100 per share × 340 shares)

- Long-term capital gains tax at 15% = $1,530

- Total after-tax: $42,670

Scenario C: Hold for 2 years, stock drops

- Stock falls to $70

- She sells 340 shares = $23,800

- Capital loss = $10,200

- She can use this loss to offset other investment gains

- Total after-tax: $23,800

Jessica chose Scenario A. She accepted that she might miss out on gains, but she also avoided the risk of a $10,200 loss. More importantly, she eliminated her concentration risk immediately.

The Tax-Loss Harvesting Safety Net

Here's a silver lining: losses can offset gains.

If you hold company stock and it drops, you can sell at a loss and use that loss to cancel out gains from other investments. You can deduct up to $3,000 of excess losses against ordinary income each year.

Think of it as a partial refund on a bad investment. It doesn't eliminate the pain of losing money, but it softens the blow.

Don't Let Tax Fears Paralyze You

Many people hold concentrated positions because they're afraid of the tax hit. But here's the reality: you already took the tax hit when shares vested.

The question isn't "Should I pay taxes?" You already did.

The real question is: "Should I hold a concentrated position in my company stock, hoping for gains that will be taxed at 15%, while risking significant losses?"

That's an investment decision, not a tax decision.

Tax considerations matter. But concentration risk, the risk of having 40% or 60% of your wealth in one stock, usually matters more. A 30% drop in your company's stock will hurt far worse than paying 15% long-term capital gains tax on a diversification strategy.

As the saying goes: don't let the tax tail wag the investment dog.

Now that you understand the tax mechanics, let's look at practical strategies for gradually reducing your concentration over time.

Strategy 2: The Gradual Glide Path (Spreading Sales Over Time)

Selling all your RSUs the day they vest feels like ripping off a Band-Aid. It's quick, it's decisive, and it's over. But what if you're not ready for that? What if you want to leave the party gradually, saying goodbye to a few people at a time instead of bolting for the door?

That's where the gradual glide path comes in.

How the Glide Path Works

Instead of selling 100% at vest, you spread your sales over 3, 6, or 12 months. You're still diversifying, just more slowly.

Here's a typical setup:

- Month 0 (vest date): Sell 30-50% immediately

- Months 1-6: Sell the rest in equal chunks each month

- Result: You're fully out within 6 months instead of on day one

Think of it as dollar-cost averaging in reverse. When you buy into a 401(k), you invest a little each month to smooth out market ups and downs. With a glide path, you're selling a little each month. You exit at different prices, which averages out the volatility.

The Real-World Math

Marcus has $60,000 in RSUs vest. He's at 40% concentration and knows he should diversify. But he's worried about selling right before a potential stock run-up. He chooses a 6-month glide path:

- Month 0 (vest date): Sell

$20,000at$100/share= 200 shares - Month 1: Sell

$8,000at$105/share= 76 shares - Month 2: Sell

$8,000at$98/share= 82 shares - Month 3: Sell

$8,000at$103/share= 78 shares - Month 4: Sell

$8,000at$107/share= 75 shares - Month 5: Sell

$8,000at$102/share= 78 shares

Total sold: $60,000 across 6 months, average exit price of $102.50/share.

Marcus captured some upside when the stock hit $107. He avoided some downside when it dipped to $98. Most importantly, he felt less emotional stress than if he'd sold everything on day one. His concentration dropped from 40% to 22% over 6 months.

Comparing Your Options

Here's how immediate selling stacks up against a glide path:

| Factor | Immediate Sale (100% at vest) | 6-Month Glide Path |

|---|---|---|

| Risk reduction | Instant (40% to 22% on day one) | Gradual (40% to 22% over 6 months) |

| Emotional difficulty | High (all at once decision) | Lower (spread out) |

| Upside capture | None after sale | Possible during glide path |

| Downside protection | Complete after sale | Partial (still exposed for 6 months) |

| Discipline required | Low (one decision) | High (must follow through monthly) |

When the Glide Path Makes Sense

This strategy works best if:

You're emotionally stuck. You know you should diversify, but you can't bring yourself to sell everything at once. A glide path gets you moving instead of staying frozen at 40% concentration.

You want to test the waters. Selling 50% immediately, then 10% monthly for 5 months, lets you capture some potential upside while still reducing risk.

You're moderately bullish. You think the stock might run up over the next few months. The glide path lets you participate in some of that gain while still exiting your position.

You have multiple vests. If RSUs vest quarterly, you can set up a glide path for each vest. This creates a natural rhythm of regular selling.

The Honest Drawbacks

Let's be clear: the glide path is a compromise, not an optimization.

You maintain concentration risk longer. For 6 months, you're still overexposed to your company stock. If the stock drops 30% in month two, you'll wish you'd sold everything at vest.

It requires discipline. You need to actually follow through on the monthly sales. If the stock goes up 20% in month one, you'll be tempted to skip month two. That's how people end up back at 40% concentration.

You might capture downside instead of upside. Marcus got lucky with his timing. But if the stock had dropped from $100 to $80 over those 6 months, he would have been better off selling everything at vest.

Making It Work

If you choose a glide path, set it up like a bill on autopay. Decide your schedule now, write it down, and commit to it. Don't check the stock price before each monthly sale. Just execute.

You can also combine strategies. Sell 50% at vest (immediate diversification), then use a 5-month glide path for the other 50%. This gives you some protection right away while leaving room for potential upside.

The glide path is still better than holding 100% indefinitely. You're moving in the right direction, just at a slower pace.

But what if you're in a blackout period when your RSUs vest? Or what if you want to lock in your selling schedule months in advance? That's where 10b5-1 plans come in, and they deserve their own deep dive.

6 Tax-Efficient Strategies to Diversify Your Investments - Don't Get Trapped By Your Company Stock

Strategy 3: The Rule 144 and Blackout Period Workaround (Setting Up a 10b5-1 Plan)

If you're an executive, director, or insider at your company, you face a frustrating problem. You want to diversify, but you're blocked from trading for huge chunks of the year.

Think of a 10b5-1 plan like setting an auto-responder for your email before vacation. You program it in advance to handle things automatically when you're "unavailable" to trade.

Who Gets Blocked from Trading (and Why)

Rule 144 restrictions apply to company insiders. This includes executives, board members, and anyone who owns more than 10% of the company. If you're unsure whether you're an insider, ask your HR or legal team.

Blackout periods are mandatory quiet times when you can't trade company stock. These typically happen:

- 4-6 weeks before quarterly earnings (that's potentially 24 weeks per year)

- During mergers, acquisitions, or major announcements

- When the company has material non-public information

Add it up, and you might be locked out 40-50% of the year. That makes diversifying nearly impossible without a plan.

How a 10b5-1 Plan Works

A 10b5-1 plan lets you pre-schedule stock sales that execute automatically, even during blackout periods. You set specific rules like:

- Sell 500 shares on the 15th of every month

- Sell 1,000 shares when the price hits $200

- Sell 25% of vested shares quarterly

The key: you must set up the plan when you don't have material non-public information. You can't use insider knowledge to time the market.

The Setup Process

Cooling-off period: After you establish the plan, there's typically a 30-90 day waiting period before the first trade executes. This proves you weren't trying to exploit insider information.

Costs: Expect to pay $500-2,000 to set up through your broker or attorney. Some brokers include it free for high-net-worth clients.

Modifications: You can change or cancel the plan, but only outside blackout periods and with a new cooling-off period.

Real Example: Breaking Free from Blackout Jail

Lisa is a VP at her company, making her a Rule 144 insider. She has $300,000 in company stock, which is 55% of her total investments. She wants to diversify, but her company has 6-week blackout periods before each quarterly earnings. That's 24 weeks per year she can't trade, nearly half the year.

In January, Lisa sets up a 10b5-1 plan with two rules:

Rule 1: Sell 1,000 shares on the 15th of every month for 12 months.

Rule 2: Sell an additional 500 shares if the stock price exceeds $150.

The plan has a 60-day cooling-off period, so her first sale happens in March. Over the next year, the plan automatically executes sales during blackout periods when Lisa couldn't trade manually. She sells $120,000 worth of stock and reduces her concentration to 38%.

Without the 10b5-1 plan, she would have missed half the trading windows and stayed stuck at dangerous concentration levels.

When You Need This Strategy

If you're subject to trading restrictions, a 10b5-1 plan isn't optional. It's the only reliable way to diversify systematically. Yes, it's more complex than the other strategies we've covered. Yes, you'll want to consult an attorney or financial advisor. But for insiders, it's essential.

(Note: Blind trusts are another option for executives, but they're significantly more complex and expensive. Most people start with a 10b5-1 plan.)

Now let's talk about the uncomfortable truths your HR department probably hasn't shared with you about managing your RSUs.

What Your HR Department Won't Tell You (The Unspoken Realities of RSU Management)

Your RSU grant paperwork is like the terms and conditions on a software install. The information is technically there, but nobody reads it. And your company isn't exactly eager to highlight the parts that might make you uncomfortable.

Here's the harsh reality: unvested RSUs are golden handcuffs. They're designed to keep you at the company. If you quit, get fired, or take another job, you forfeit every dollar of unvested equity. All of it.

Let's say you have $150,000 in unvested RSUs sitting in your account. You get a job offer for $20,000 more in base salary. Sounds great, right? But if you leave before those RSUs vest, you're walking away from $150,000 to gain $20,000. That's a terrible trade.

What happens to your RSUs when you leave:

- You quit voluntarily: Unvested RSUs disappear. Gone. You keep only what already vested.

- You're laid off (terminated without cause): Same result in most cases. Unvested RSUs are forfeited.

- You're fired for cause: Definitely forfeited. Some companies even claw back recently vested shares.

- Garden leave period: A few companies (mostly in tech) let you keep vesting for 30 to 90 days after termination. This is rare. Don't count on it.

The difference between "with cause" and "without cause" matters. Getting laid off in a restructuring (without cause) sometimes comes with severance that includes a few extra months of vesting. Getting fired for poor performance (with cause) usually means you get nothing extra.

The acquisition wildcard:

When your company gets bought, your unvested RSUs might suddenly become very interesting. This depends on whether your plan has single-trigger or double-trigger acceleration.

Single-trigger acceleration means all your unvested RSUs vest immediately when the acquisition closes. The company gets bought, you get paid. Simple.

Double-trigger acceleration means you need two things to happen: the company gets acquired AND you get terminated within a certain period (usually 12 to 18 months). If you keep your job after the acquisition, your RSUs typically convert to the acquiring company's stock and keep vesting on the original schedule.

Most companies use double-trigger these days. Acquirers don't want everyone cashing out and leaving immediately.

Here's what this looks like in real life:

Kevin works at Company A. He has $150,000 in unvested RSUs. He gets a job offer from Company B for $20,000 more in base salary.

Kevin digs up his RSU plan document (found it in his equity portal under "Plan Documents"). He learns that if he quits, he forfeits everything unvested. But his next vest is in 2 months, worth $40,000.

Kevin negotiates with Company B to start in 3 months instead of immediately. This lets him capture that $40,000 vest before leaving. He's still walking away from $110,000 in unvested RSUs, but at least he grabbed what was closest to vesting.

Meanwhile, Sarah works at Company C. She also has $150,000 unvested. Company C gets acquired by Big Tech.

Sarah finds her plan document and discovers she has single-trigger acceleration. All $150,000 vests immediately when the acquisition closes.

Sarah sells 75% ($112,500) right away to diversify. She knows this might be her only chance at this kind of liquidity. She only learned about single-trigger acceleration by reading her plan document. HR never mentioned it proactively.

What your company wants vs. what you need:

Your employer loves when you hold company stock. It "aligns your interests with shareholders." That's corporate speak for "we want you thinking like an owner."

But here's the thing: executives who preach alignment often sell their own shares regularly through pre-planned trading programs. They diversify. They manage their concentration risk.

You should too.

Other fine print worth knowing:

- Vesting schedules can change for future grants, but your existing grants are usually protected

- Some companies (rare, mostly for executives) let you defer RSU settlement to delay taxes

- A few companies allow you to donate unvested RSUs to charity (check your plan)

- If your company goes private or gets delisted, your RSUs might convert to cash or private shares with complex restrictions

Where to find the truth:

Your RSU plan document is the source of truth. Not your offer letter. Not what your manager said. The actual plan document.

Look for it in your equity compensation portal (E*TRADE, Fidelity, Schwab, Morgan Stanley, etc.). Usually under "Plan Documents," "Prospectus," or "Legal Documents."

Can't find it? Email HR and ask: "Can you send me the RSU plan document and summary plan description?" They have to provide it.

Read the sections on vesting, termination, and change of control. Yes, it's boring. Yes, it's full of legal language. But you're reading the contract that controls potentially hundreds of thousands of dollars of your wealth.

Think of it like reading your mortgage paperwork. Nobody enjoys it, but you'd never sign a home loan without understanding the terms.

Now that you understand what you're actually holding and what could happen to it, let's talk about the rare situations where keeping concentrated in company stock actually makes sense.

When Holding Makes Sense (The Rare Cases Where Concentration Is Acceptable)

Let's be honest: sometimes going all-in on your company stock actually makes sense.

Think of it like a poker player pushing all their chips to the center of the table. It's a high-risk move, but it's not always stupid. The key difference? A smart poker player only goes all-in when they're playing with money they can genuinely afford to lose.

Here's the truth most financial advisors won't say: holding a concentrated position can be acceptable if you meet very specific criteria.

When Concentration Risk Is Actually Acceptable

You're early in your career with small absolute amounts. Even if company stock is 80% of your net worth, if that net worth is only $50,000, you have decades to rebuild. A 28-year-old can recover from a total loss. A 52-year-old cannot.

You're already financially independent. If you could retire comfortably today without this company stock, then holding it is playing with house money. You're betting on upside without risking your lifestyle.

You're close to a major liquidity event. If your company is going public in 6-12 months and you want to maximize that outcome, holding through the IPO can make sense. But only if you can afford to wait and potentially lose.

This is truly 'extra' money. You have other substantial assets that are properly diversified. Your emergency fund is solid. Your retirement accounts are on track. This company stock is the cherry on top, not the whole sundae.

The One Question That Matters

Here's your test: If this stock went to zero tomorrow, would it meaningfully change your life plans?

If the answer is yes, you cannot afford to hold a concentrated position. Period.

If the answer is no, and you truly mean it, then holding might be reasonable.

Real Examples: When It Works and When It Doesn't

Acceptable Hold: Jake's Calculated Bet

Jake is 28 and works at a hot AI startup that's planning to go public in 8 months. He has $80,000 in unvested RSUs, which is 90% of his $90,000 net worth. His situation:

- No kids, rents an apartment, minimal obligations

- Has $25,000 in emergency savings (separate from investable assets)

- Makes $120,000 salary and can save aggressively

- Early in his career with 35+ working years ahead

Jake decides to hold everything through the IPO, hoping for a 3-5x return. If the company fails and his RSUs become worthless, he's set back a few years. That's painful but not devastating. He can rebuild.

This is a calculated risk with money he can afford to lose.

NOT Acceptable Hold: Patricia's Dangerous Gamble

Patricia is 52 and works at an established public tech company. She has $600,000 in company stock, which is 70% of her $850,000 total net worth. Her situation:

- Plans to retire in 8 years

- Needs this money to fund retirement

- Cannot easily replace losses at this career stage

- Has limited time to recover from a major drop

Patricia is holding because the stock has performed well and she's optimistic about the company's future. She thinks, "I work here, I know the business, we're doing great."

This is dangerous. If the stock drops 50%, her retirement gets pushed back years or she has to dramatically cut her lifestyle. Patricia should immediately diversify to under 25% concentration, even if it means missing potential upside.

Her retirement security is more important than potential gains.

What About Those Early Google Employees?

Yes, some early employees at Google, Apple, and Amazon became incredibly wealthy by holding concentrated positions. Those stories are real.

But for every Google, there's a WeWork. A Theranos. A Pets.com. Dozens of once-promising companies that cratered.

Survivorship bias is powerful. You hear about the winners because they're still around to tell their stories. The losers quietly rebuild their careers and don't write books about it.

The Smart Middle Ground

Even if you meet all the criteria for holding, consider selling some of your position to lock in gains.

Going back to Jake, our 28-year-old startup employee: he could hold 80% through the IPO and sell 20% now. That gives him both upside exposure and some guaranteed money in the bank.

This isn't about timing the market. It's about acknowledging that even calculated bets can go wrong.

What Doesn't Count as a Good Reason

Let's be clear about what is NOT a legitimate reason to hold concentrated positions:

- "The stock has been going up" (past performance means nothing)

- "I have inside knowledge that we're doing well" (you don't know the future)

- "I'd feel stupid if I sold and it doubled" (FOMO is not a financial strategy)

- "Everyone else at the company is holding" (their risk tolerance isn't yours)

- "I believe in our mission" (company optimism is not financial planning)

Loving your job and believing in your company's product is wonderful. It makes work meaningful. But it's not a reason to concentrate your financial future in one stock.

The Bottom Line

Holding concentrated positions is acceptable only when you genuinely, honestly, truly can afford to lose 100% of that money without changing your life plans.

If you're not sure, you can't afford it. Diversify.

Now that you know when concentration might be acceptable, let's create your specific action plan to manage your RSU concentration risk, starting this week.

Your Diversification Action Plan (What to Do This Week)

You've got the map. Now you need turn-by-turn directions to actually reach your destination: a diversified portfolio that won't collapse if your company hits a rough patch.

Think of this like setting up autopilot for a road trip. You program the route once, then the car handles the driving. Same with diversification. Set up your rules now, and they'll run automatically every time RSUs vest.

Here's your checklist:

This Week (2 Hours Total)

Step 1: Calculate your exact concentration (15 minutes)

Open your brokerage account and add up:

- Company stock value: $______

- Total investment accounts: $______

- Concentration percentage: _____%

Step 2: Pick your strategy (30 minutes)

Based on your concentration:

- Over 50%? Choose Strategy 1: Sell 75-100% immediately at each vest

- 25-50%? Choose Strategy 1: Sell 50-75% immediately at each vest

- Under 25%? Choose Strategy 2: Gradual glide path to reach 10-15%

- Have blackout periods? Add Strategy 3: Set up a 10b5-1 plan

Write down your decision: "I will sell ___% of shares within 24 hours of each vest."

Step 3: Open an index fund account if needed (1 hour)

If you don't already have one, open an account at Vanguard, Fidelity, or Schwab. You'll invest sale proceeds here.

Pick one simple fund:

- Total stock market index (VTSAX at Vanguard, FSKAX at Fidelity)

- S&P 500 index (VOO, SPY, or similar)

This Month (3 Hours Total)

Step 4: Set up automatic selling rules (1-2 hours)

Call your equity comp broker (E*TRADE, Fidelity, Morgan Stanley, etc.) and say: "I want to set up an automatic sale rule. Sell [your percentage] of shares within 24 hours of each vest."

Most brokers call this "sell to cover plus" or "automatic diversification." They'll walk you through it.

Step 5: Create your tracking spreadsheet (30 minutes)

Make three columns:

- Date

- Company stock value

- Concentration percentage

Update it after each vest and sale.

Step 6: Set quarterly review reminders (5 minutes)

Add calendar reminders for March 1, June 1, September 1, December 1. Label them: "Check RSU concentration and adjust strategy."

Real Examples: Your 12-Month Roadmap

Starting at 60% concentration:

Week 1: You calculate $240k company stock divided by $400k total = 60%. You choose to sell 75% at each vest.

Week 2: You call your broker and set up the automatic rule. You open a Vanguard account.

Month 1: Your first vest happens, $30k worth of shares. The automatic sale triggers within 24 hours. You sell $22.5k (75%), keep $7.5k (25%). You invest the $22.5k in VTSAX.

12-month goal: Reach 30% concentration

24-month goal: Reach 15% concentration

Starting at 25% concentration:

Week 1: You calculate $75k divided by $300k total = 25%. You choose to sell 50% at each vest.

Week 2: You set up automatic rules. You already have an index fund account.

12-month goal: Reach 15% concentration

24-month goal: Reach under 10% concentration (maintenance mode)

Ongoing Maintenance

Every quarter, check three things:

- What's your current concentration percentage?

- Is your automatic selling rule still working?

- Are sale proceeds getting invested in index funds?

If concentration creeps above your target, sell a chunk of existing shares to get back on track.

What Success Looks Like

In 12 months: You should be at 25-30% concentration or lower, down from wherever you started.

In 24 months: You should be at 10-15% concentration. This is maintenance mode. You're diversified enough that a company crisis won't wreck your finances.

Long term: Your concentration stays under 15%. You sleep better knowing one company doesn't control your financial future.

When to Get Help

Consider a fee-only financial advisor if you have:

- More than $500k in company stock

- Complex tax situations (AMT, big capital gains)

- Executive-level equity (options, performance shares, etc.)

They'll charge $200-400 per hour or 0.5-1% of assets annually. Worth it for personalized guidance.

The Most Important Thing

Taking imperfect action beats perfect paralysis. Even if you only sell 25% at your next vest, that's 25% less concentration risk than doing nothing.

Your company might be great. Your stock might keep climbing. But your financial security shouldn't depend on one company's success.

Set up your automatic rules this week. Your future self will thank you.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis