How RSU Refresher Grants Work: Your Guide to Understanding Refresh Equity

Why companies give you more stock after your initial grant, and what it means for your paycheck

Published March 1, 2026 · Updated March 1, 2026

RSU refresher grants are additional equity awards companies give you after your initial stock package starts running out. They're designed to keep your total compensation steady and retain talented employees. This guide explains when you'll get refreshers, how much to expect, and what to do with them.

The Refresher Problem: Why Your Paycheck Drops in Year 5

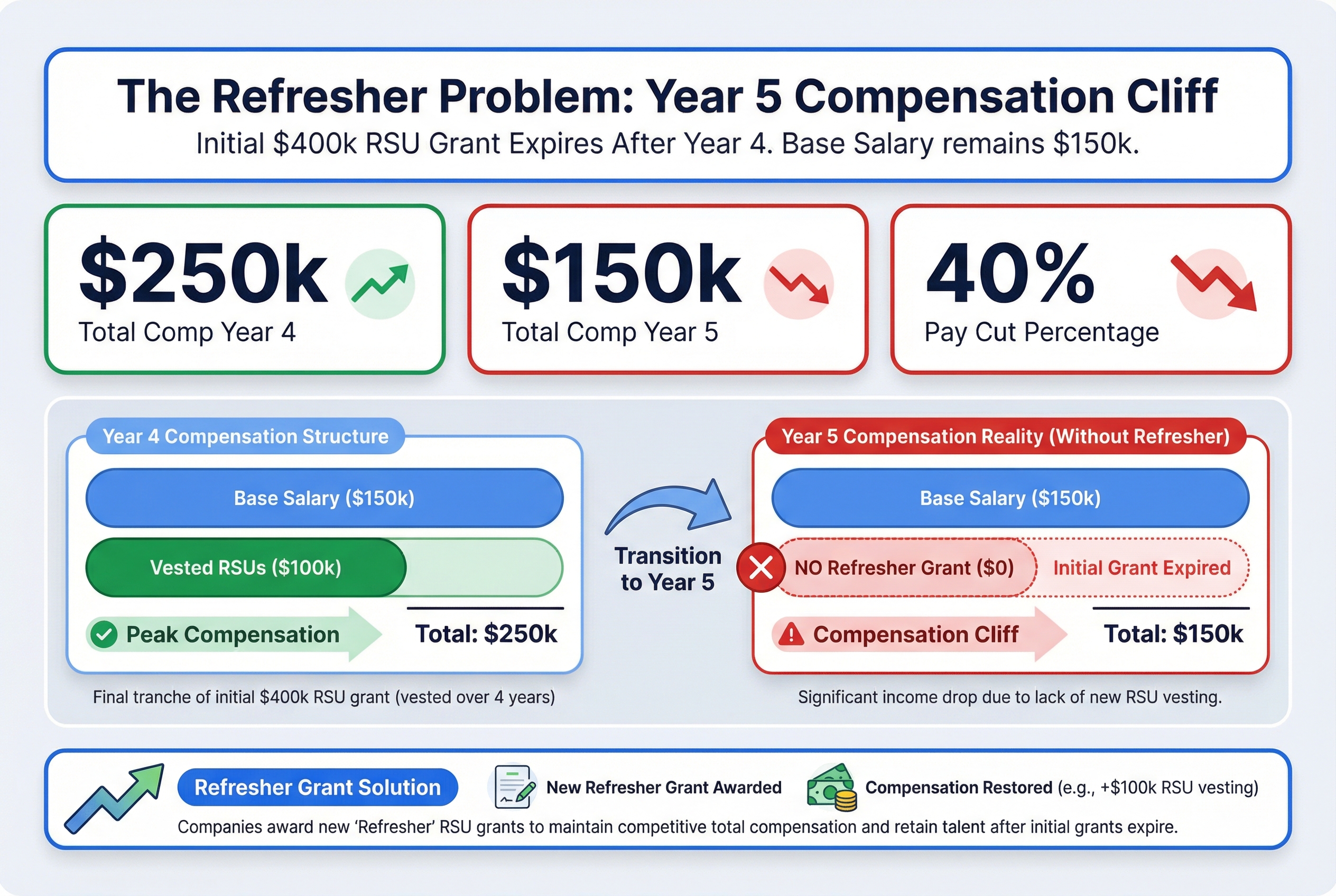

Meet Sarah, a software engineer at a big tech company. She makes $150k in base salary and got a $400k RSU grant when she started. That grant vests over 4 years at $100k per year.

For her first four years, life is good. Her total compensation looks like this:

| Year | Base Salary | RSUs Vesting | Total Comp |

|---|---|---|---|

| 1 | $150k | $100k | $250k |

| 2 | $150k | $100k | $250k |

| 3 | $150k | $100k | $250k |

| 4 | $150k | $100k | $250k |

| 5 | $150k | $0 | $150k |

See the problem? In Year 5, Sarah's total compensation drops to $150k. That's a 40% pay cut, even though she's doing the exact same job.

Think of your initial RSU grant like a Netflix subscription that expires. For four years, you're getting the full package. Then suddenly, the subscription ends. You're back to basic cable.

This compensation cliff is why your inbox fills up with recruiter emails around Year 4. Other companies know you're about to take a huge pay cut. They're ready to offer you a fresh RSU grant to jump ship.

Sarah isn't getting lazy. She isn't worth less to her company. But without new equity grants, her paycheck says otherwise.

This is exactly the problem that refresher grants solve. Let's look at how they work.

The 'Refresher Problem': Sarah's total compensation drops 40% in Year 5 when her initial $400k RSU grant fully vests.

The 'Refresher Problem': Sarah's total compensation drops 40% in Year 5 when her initial $400k RSU grant fully vests.

What RSU Refresher Grants Actually Are

Think of refresher grants like a phone company giving you credits to keep you from switching carriers. Every year or two, they sweeten the deal to make leaving harder.

A refresher grant is bonus equity on top of your original grant. When you joined your company, you got an initial RSU package. That might have been 1,000 shares vesting over four years. A refresher is a new grant of additional RSUs they give you later, while you're already working there.

Companies give refreshers for two big reasons:

Reason 1: Keeping you from leaving. Your initial grant runs out. Without new equity, you might jump to another company offering fresh stock. Refreshers are literally called "golden handcuffs" because they tie you to the company with money that only comes if you stay.

Reason 2: Preventing pay cuts. As your initial grant runs out, your total compensation drops. Hard.

Here's how that works. Let's say Sarah earns:

- Base salary: $150,000

- Initial RSU grant: $200,000 (vesting $50,000 per year for 4 years)

- Year 1-4 total comp: $200,000 per year ($150k + $50k)

- Year 5 without refreshers: $150,000 (just her base salary)

That's a 25% pay cut just for staying loyal. Ouch.

Now add a refresher. If Sarah gets a $200,000 refresher grant in Year 3 that vests over four years at $50,000 per year, her Year 5 compensation stays at $200,000 ($150k base + $50k from the refresher). The company just prevented a massive pay cut.

Important reality check: Refreshers aren't guaranteed. Your company decides whether to give them, when to give them, and how much. This is totally different from your initial grant, which was part of your signed offer letter.

Most large public tech companies give regular refreshers. Smaller companies or non-tech companies might not. We'll cover who gets what in a later section.

Now let's look at the specific types of refreshers you might receive.

Restricted Stock Units: The Basics of RSUs and How to Use Them

The Three Types of Refresher Grants You Might Get

Think about how your parents gave you money growing up. There was your regular allowance for just being part of the family. Extra cash for good grades. And a bigger allowance when you became a teenager. Companies hand out refresher grants the same way.

Time-Based Refreshers (Your Regular Allowance)

These are the most common type. You get them just for staying at the company.

Most big tech companies give time-based refreshers every year or every two years. No special performance needed. You're breathing and still employed? Here's your grant.

Example: Sarah is a Product Manager at Meta. Every year in March, she gets a refresher grant. This year: $120,000 in RSUs. Next year, assuming she's still there: another $120,000 grant.

These grants keep your total compensation steady as your original hire grant runs out.

Performance Refreshers (Your Good Grades Bonus)

These depend on your performance review rating or hitting specific goals.

If you get "Exceeds Expectations" or "Outstanding," you get extra equity on top of your regular refresher. Meet your quarterly targets? Bonus grant.

The amounts vary wildly. A "Meets Expectations" rating might mean no performance grant at all. "Exceeds" could mean $50,000 to $100,000 extra. "Outstanding" could double that.

The catch: These aren't guaranteed. Bad year or just okay performance? You might get zero.

Promotion Refreshers (Your Teenager Upgrade)

When you move up a level, your equity compensation needs to match your new role. That's where promotion grants come in.

These are usually larger than annual refreshers and they happen immediately when you get promoted, not at the regular refresh cycle.

Real example: Marcus is a Senior Engineer (L5) at Google. Here's what happened in his promotion year:

- Annual time-based refresher:

$150,000in RSUs - Gets promoted to Staff Engineer (L6):

$100,000promotion grant immediately - Also rated "Exceeds Expectations": additional

$75,000performance grant - Total new equity that year:

$325,000

Most People Get Multiple Types

Here's the key thing: these aren't mutually exclusive. High performers often get all three in the same year. Average performers typically just get the time-based refresher.

Now, there's one more refresher structure that works completely differently. Instead of getting grants every year, some companies give you one massive grant every few years. Let's look at how those boxcar grants work.

Traditional Annual Refreshers vs. Boxcar Grants

Companies give refreshers on two different schedules. Think of it like getting paid. Some people get a paycheck every week. Others get a bigger check once a month. Both can add up to the same amount, but the timing feels very different.

Traditional annual refreshers work like weekly paychecks. You get a smaller grant every single year. Meta, Google, and most big tech companies use this approach.

Here's what it looks like:

- Year 1: $100k grant

- Year 2: $100k grant

- Year 3: $100k grant

- Year 4: $100k grant

- Year 5: $100k grant

- Year 6: $100k grant

- Total: $600k in grants

Boxcar grants work like monthly paychecks. You get a much bigger grant, but only every 2-3 years. Amazon and some startups use this structure.

Same total value, different timing:

- Year 1: $300k grant

- Year 2: Nothing

- Year 3: Nothing

- Year 4: $300k grant

- Year 5: Nothing

- Year 6: Nothing

- Total: $600k in grants

Why the Difference Matters

Boxcar grants create their own mini compensation cliffs. In years 2, 3, 5, and 6, you get zero new equity. Your income relies entirely on older grants still vesting.

Traditional refreshers give you smoother, more predictable pay. Every year brings new equity. Your compensation doesn't swing as wildly.

Stock price risk hits harder with boxcar grants. Imagine the stock drops 30% right before your Year 4 grant. That $300k grant is now worth $210k. You just lost $90k in potential equity. With annual grants, you'd only lose $30k on that year's grant. You'd still get grants in the other years at different prices.

The boxcar structure also means more of your wealth gets locked to the stock price on just two specific dates over six years. Traditional refreshers spread that risk across six different grant dates.

Now that you understand the two main structures, let's talk about when companies actually give these refreshers.

When You'll Actually Get Refreshers (and When You Won't)

Think of refreshers like airline status. You don't get lounge access on day one. You need to fly with them for a while first.

Most companies follow the same pattern: your first refresher grant comes in year 2 or year 3 of employment. You won't see one after your first year. Companies want to see you stick around and perform before they invest more equity in you.

Who Actually Gets Refreshers?

The numbers tell a clear story:

Large public tech companies: Almost everyone gets them. Meta, Google, Amazon, Microsoft, and similar companies treat refreshers as standard. Over half of employees at public companies receive refreshers by year 2.

Startups and private companies: Only 30-40% give regular refreshers. Many treat your initial equity grant as a one-time bonus. They might promise refreshers "after the IPO" or "when we raise our next round." That might never happen.

When Refreshers Stop

Even companies that normally give refreshers will skip them during:

- Hiring freezes or layoffs. No new money means no new equity grants.

- Poor stock performance. When the stock tanks, companies often pause refreshers.

- Performance issues. If you're on a performance improvement plan, don't expect a refresher grant.

Real example: Elena joins a Series C startup in 2022 with $200k initial RSUs. She's a solid performer, but the company freezes refreshers in 2024 due to market conditions. She gets nothing in years 2-3.

Meanwhile, her friend at Google gets $120k annual refreshers starting year 2. By year 4, the Google friend has $360k more in equity grants despite similar initial offers.

Quick Decision Guide

You'll likely get refreshers if:

- You work at a large public company

- You meet or exceed performance expectations

- The company is growing or stable

You probably won't get refreshers if:

- You're at an early-stage startup

- The company is struggling financially

- You're underperforming

Now that you know when refreshers happen, let's talk about how much you can actually expect to receive.

How Much to Expect: Refresher Grant Sizes by Company Type

Think of refreshers like tips at restaurants. A fancy steakhouse (Meta, Google) means bigger tips than your local diner (early-stage startup). The service matters too. Great performance gets you a 25% tip, average performance gets 15%.

Here's what you can actually expect:

Large Public Tech Companies

At FAANG and similar companies, refreshers typically range from 50% to 100% of your annual equity target. Sometimes more if you crush it.

Real Meta numbers:

- Mid-level engineer (E5) with "Meets Expectations": $180k in annual refreshers

- Same E5 with "Greatly Exceeds": $300k

- Staff Engineer (E6) with top rating: $400k+

- Senior Staff (E7): Up to $500k or more

Google and Amazon follow similar patterns. A Google L5 might see $150k-250k depending on performance. Amazon L6 engineers often get $200k-350k in refreshers.

Your performance rating is huge. Top performers can get 200% of target. Low performers might get zero.

Startups: It Depends on Stage

Startups allocate a chunk of their equity pool to refreshers every year:

- Early-stage (Series A/B): 35-37% of equity pool

- Later-stage (Series C+): 40-50% of equity pool

What does this mean for you? At a Series B startup, a senior engineer might get $50k-80k in refreshers every 2 years (not annually). That's way less frequent and smaller than public companies.

Pre-IPO companies like Stripe or Databricks fall somewhere in between. They often give annual refreshers, but amounts vary wildly based on funding and performance.

Quick Reference Table

| Company Type | Frequency | Typical Amount | Performance Impact |

|---|---|---|---|

| FAANG/Big Tech | Annual | 50-100% of yearly equity target | 0-200% of target |

| Late-stage startup | Annual or bi-annual | 30-60% of initial grant | High variance |

| Early-stage startup | Every 2-3 years | 25-40% of initial grant | Very high variance |

The bottom line: Bigger, more profitable companies give bigger, more predictable refreshers. Your level and performance rating matter more than anything else.

Now that you know how much to expect, let's look at when you'll actually get that money in your account.

Refresher Vesting Schedules: When You Actually Get the Money

Most refresher grants vest over four years at 25% per year. Think of it like a payment plan that splits your bonus into four equal chunks.

Here's the big difference from your initial grant: refreshers usually have no cliff. You start earning shares immediately in year one. Your initial grant probably made you wait a full year before any shares vested. Refreshers don't work that way.

How Multiple Grants Stack Up

The magic happens when multiple grants vest at the same time. You're not replacing old grants with new ones. You're adding layers.

Here's what this looks like in practice:

Sarah's Overlapping Grants

- Year 1: Initial grant vests = $100,000

- Year 2: Initial grant ($100k) + First refresher ($50k) = $150,000

- Year 3: Initial ($100k) + First refresher ($50k) + Second refresher ($50k) = $200,000

- Year 4: Initial ($100k) + First refresher ($50k) + Second refresher ($50k) = $200,000

- Year 5: First refresher ($50k) + Second refresher ($50k) + Third refresher ($50k) = $150,000

- Year 6: Second refresher ($50k) + Third refresher ($50k) + Fourth refresher ($50k) = $150,000

Notice how Sarah has three different grants vesting in year 5. Each grant runs on its own four-year schedule. They don't interfere with each other.

Why Companies Do This

This overlap is intentional. Without refreshers, Sarah's compensation would drop from $100k to zero in year 5. The overlapping grants keep her total vesting amount stable year after year.

You might have 3-4 active grants vesting simultaneously once you've been at the company a few years. Each one ticks along on its own timeline, depositing shares into your account every year.

Now let's talk about what your HR team probably isn't mentioning about refresher strategy.

What Your HR Won't Tell You: The Real Refresher Strategy

Your company is playing a game with your compensation. And they're really good at it.

Think of it like a restaurant with cheap menu prices but expensive drinks. The base salary looks reasonable, but the real money is in the equity. That's not an accident. It's strategy.

The Base Salary Cap Game

Amazon caps every single employee at $160,000 base salary. Even executives. Even the CEO (technically).

Why? Because equity doesn't hit the cash budget the same way salary does. When Amazon gives you 1,000 RSUs, they're not writing a check for $150,000. They're creating shares out of thin air. It affects shareholders through dilution, but it doesn't drain the bank account.

This lets companies pay you more total compensation while managing their cash flow. Your $300k total comp package might be $160k salary + $140k in RSUs. The cash budget only sees $160k.

How Stock Price Makes Refreshers "Cheaper"

Here's the part that might make you angry.

When your company's stock price rises, refreshers become cheaper for them. Not in dollars, but in shares.

Real example: When Amazon's stock was $100, they granted you 1,000 shares ($100,000 value). When the stock hit $150, they granted 667 shares (still $100,000 value).

You got the same dollar amount. But you got fewer shares.

Now here's the kicker. If the stock drops back to $100, those 667 shares are worth $66,700 instead of $100,000. The company saved money by granting during the high. You lost potential upside.

They're not trying to screw you. They're managing their equity budget. But you need to understand this dynamic.

The Performance Rating Calibration Secret

Most companies calibrate performance ratings. That's HR-speak for "we limit how many people can get top ratings."

If everyone performed great, tough luck. Only 20% can get "exceeds expectations." Only 10% can get "outstanding."

Why does this matter? Because refresher amounts are tied to ratings. The calibration system ensures that most people get average refreshers, even in a great year.

The Attrition Bet

Companies know something else: not everyone stays for the full vesting period.

When they grant 10,000 employees refreshers with 4-year vesting, they're banking on maybe 30% leaving before year four. Those unvested shares go back to the company. They just saved millions.

This isn't cynical. It's math. And it's why refreshers often look more generous than they actually are.

Now that you understand the game, let's talk about how refreshers fit into your total compensation picture.

How to Think About Refreshers in Your Total Compensation

Your total compensation is like a phone bill. You can't just look at one line item. You need to add up everything to see what you're really getting.

Here's the formula that actually matters:

Total Annual Compensation = Base Salary + Cash Bonus + Value of All Equity Vesting That Year

Most people only think about their base salary. That's a mistake. At big tech companies, equity often makes up 30-50% of your total pay.

Calculate What You're Really Making

Let's say you're in Year 3 at your company. Here's how to find your true compensation:

Step 1: Write down your base salary and any cash bonuses.

Step 2: List every RSU grant you have and when shares vest.

- Initial grant: 25 shares vesting this year

- Year 2 refresher: 15 shares vesting this year

- Year 3 refresher: 10 shares vesting this year

Step 3: Multiply total vesting shares by current stock price.

- 50 shares total × $200 per share = $100,000

Step 4: Add it all up.

- $150k base + $20k bonus + $100k equity = $270k total comp

You need to track all your grants in one place. Use a spreadsheet or your company's equity portal. Update it every time you get a new grant.

Why This Matters When Comparing Job Offers

Total comp is everything when you're looking at offers. A lower base salary with better refreshers often wins.

Here's a real example:

Job Offer A:

- Base: $180k

- Initial RSUs: $400k (vesting over 4 years = $100k/year)

- Annual refreshers: $100k starting Year 2

Job Offer B:

- Base: $220k

- Initial RSUs: $400k (vesting over 4 years = $100k/year)

- Annual refreshers: None

In Years 1-4, both offers are similar. You're getting around $280-300k total.

But look at Year 5. This is where it gets interesting.

Offer A in Year 5:

- $180k base

- $100k from Year 2 refresher (final vest)

- $100k from Year 3 refresher

- $100k from Year 4 refresher

- Total: $480k

Offer B in Year 5:

- $220k base

- $0 from equity (initial grant finished vesting)

- Total: $220k

Over 6 years, Offer A pays you about $200k more. Even though the base salary is $40k lower.

The Stock Price Reality Check

Remember, equity value changes with stock price. Use today's price to estimate, but know it will fluctuate.

If the stock doubles, your equity is worth twice as much. If it drops 50%, your equity is worth half. This is why you can't just look at grant values from years ago. You need to recalculate based on current prices.

Track your vesting schedule. Know exactly which grants vest when. Then you can make smart decisions about your total compensation picture.

Next, let's talk about what happens when those refreshers actually vest. Spoiler: the IRS takes a big bite.

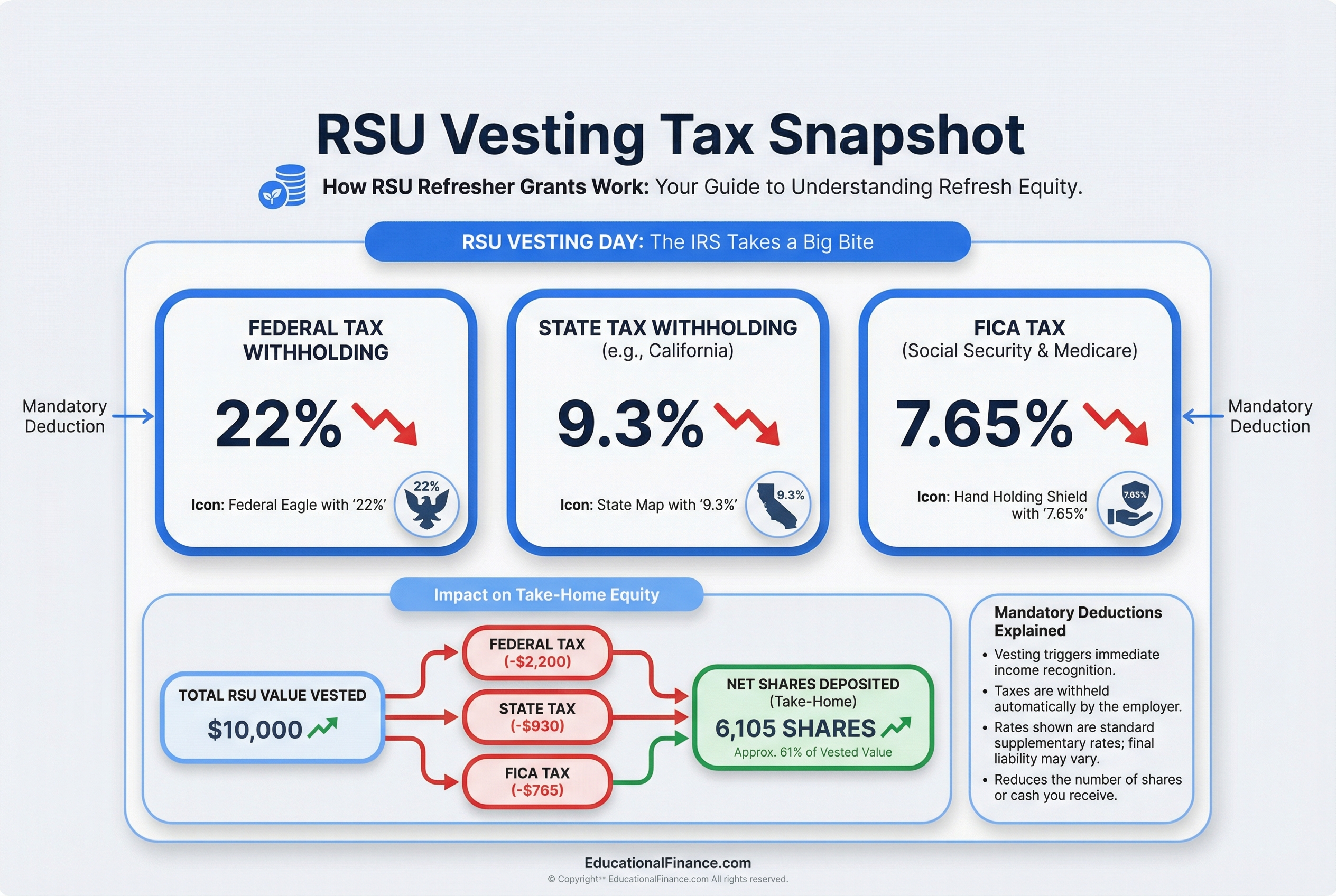

When RSUs vest, expect automatic withholding of 35-40% to cover ordinary income taxes.

When RSUs vest, expect automatic withholding of 35-40% to cover ordinary income taxes.

Taxes on Refresher Grants: What You'll Actually Take Home

Here's the hard truth: when your refresher RSUs vest, the IRS treats them exactly like a cash bonus. Not like an investment that grew over time. Like salary you just earned today.

Think of vesting day as getting a surprise bonus paycheck. The company calculates the total value of your vesting shares and reports it as ordinary income. You pay the same tax rate as your regular salary, not the lower capital gains rate.

How Much Gets Withheld on Vesting Day

Your company will automatically sell some of your shares to cover taxes. Here's what typically gets withheld:

- 22% federal (supplemental withholding rate)

- 7-10% state (varies by location, 0% in states like Texas)

- 7.65% FICA (Social Security and Medicare, up to income caps)

Total withholding: usually 35-40% of your shares disappear immediately.

A Real Example

You have 100 RSUs vesting when the stock is worth $100 per share. That's $10,000 in value.

Your company withholds 35% for taxes by selling 35 shares. You receive 65 shares worth $6,500.

If you sell those 65 shares immediately at the same $100 price: You owe nothing more in taxes. You're done.

If you hold those 65 shares and sell a year later at $120 per share: You now have $7,800 total. You owe long-term capital gains tax on the $1,300 gain ($7,800 minus your $6,500 cost basis). That's typically 15-20% tax on the gain, or about $200-260.

The Withholding Trap

Here's what catches people: that 22% federal withholding often isn't enough.

If you earn $200k in salary and $100k in RSUs vest, you now have $300k in taxable income. That pushes you into the 35% federal bracket. But your company only withheld 22% federal on the RSUs.

You'll owe the difference when you file taxes. This surprises a lot of people in April.

When Multiple Refreshers Hit at Once

This gets messy fast. Say you have three different refresher grants all vesting shares in the same year, plus your original grant still vesting. You could have $200k+ in RSU income hitting in one tax year.

That's like getting three bonus paychecks in one year. It can bump you up one or two tax brackets temporarily. The withholding might only cover 35%, but you could owe 40-45% total when federal, state, and FICA combine.

Some people get hit with $20k-30k surprise tax bills because they didn't plan for multiple grants vesting together.

Setting Yourself Up for Success

Now that you understand the tax hit, let's talk about whether you should actually negotiate for better refreshers in the first place.

Strategies for Restricted Stock Unit Taxes (RSUs)

Should You Negotiate for Better Refreshers?

Here's the hard truth: annual refreshers are like prices at Target. You can't haggle. They're set by formula based on your level and performance rating.

But that doesn't mean you're powerless. You just need to negotiate the right things at the right time.

What You Can't Negotiate

Annual refresher grants follow company formulas. If you're an L5 engineer with a "meets expectations" rating, you get the same refresher target as every other L5 engineer with that rating. HR can't change this for you.

The refresher formula itself is non-negotiable. You can't ask for 25% annual refreshers when the company gives 15%.

What You CAN Negotiate

Your initial equity grant is fully negotiable during hiring. This is your biggest opportunity. A higher initial grant means more total compensation for 4 years.

Your level determines everything. Higher level means larger initial grants AND higher refresher targets forever.

Promotion timing can sometimes be negotiated, especially when changing companies. Get commitments in writing.

Performance expectations that drive your rating (and thus refresher size) are somewhat negotiable with your manager.

The Smart Strategy: Negotiate Level, Not Refreshers

Maya got promoted to Senior Engineer at a big tech company. She was offered an L5 position with a $200,000 promotion grant.

She couldn't negotiate that $200,000 (it's set by level). But she DID negotiate to be hired as L6 instead. That came with:

- A $280,000 initial grant (40% larger)

- Annual refresher targets of $70,000 instead of $50,000

- Higher salary too

She negotiated level, not the refresher formula. That's the move.

When to Push Back

During initial offer: Negotiate hard. Ask for higher level or larger initial grant. This is your only real chance.

At promotion time: If you're being promoted internally, refresher amounts are usually fixed. But if you're changing companies for a "promotion," you can negotiate the offer package.

Performance review time: You can't negotiate the refresher formula, but you CAN work with your manager on performance expectations and ratings.

What to Say

When interviewing, ask: "What's your typical refresher policy for this level? How much equity do high performers usually get annually?"

When getting promoted: "I understand the promotion grant is set by level. Can we discuss whether L6 is appropriate given my scope?"

When reviewing performance: "What specific outcomes would put me in the 'exceeds expectations' category for next cycle?"

The Decision Tree

Joining a new company? Negotiate initial grant size and level aggressively. This is your moment.

Getting promoted internally? Accept the standard promotion grant. Focus energy on negotiating level if you're borderline.

Annual review time? Accept the refresher amount. Focus on setting clear performance goals for next year.

Considering leaving? Use refresher targets at other companies as negotiating leverage for your next offer.

What Actually Works

Don't ask for "better refreshers." That's like asking Target to lower their prices just for you.

Instead, ask for things that indirectly increase your refreshers:

- Higher level (increases all future refreshers)

- Larger initial grant (more total comp now)

- Clear performance metrics (better chance at top ratings)

- Promotion timeline commitments (faster path to higher refresher targets)

The refresher formula won't change for you. But you can change which formula applies to you.

Once you understand what you can and can't negotiate, you need a plan for what to do when those refreshers actually vest. That's where most people make expensive mistakes.

RSU Taxes Explained + 5 Strategies for 2024

What to Do When Your Refreshers Vest: A Decision Framework

Here's the uncomfortable truth: most people should sell their vested RSUs immediately.

Think of it like this. You work at Apple. You get paid in Apple dollars (your salary). You get bonuses in Apple stock (your RSUs). Your career depends on Apple doing well. Now you want to keep all your vested shares too? That's like a farmer who grows only corn, gets paid in corn, and invests all his savings in corn futures. One bad harvest and everything crashes at once.

Your default strategy should be: sell 75-100% when shares vest.

Here's why. Your job and your investments are both tied to the same company. If your company struggles, you might face layoffs AND watch your stock drop 40%. That's a double disaster you can avoid.

The Simple Decision Flowchart

Ask yourself three questions:

1. Do you have a 6-month emergency fund?

- No? Sell 100%. Build that safety net first.

- Yes? Move to question 2.

2. Is more than 20% of your net worth in company stock?

- Yes? Sell immediately until you're under 20%. You're dangerously concentrated.

- No? Move to question 3.

3. Do you need this money in the next 2 years?

- Yes? Sell 100%. Don't gamble with money you need soon.

- No? You can hold 25% if you're bullish. Sell the rest.

Real Scenarios, Real Recommendations

Scenario 1: You have $8,000 in credit card debt

- Refreshers vest: 200 shares at $150 = $30,000

- Recommendation: Sell 100% immediately. Pay off the debt ($8,000). Put $15,000 in emergency fund. Invest $7,000 in diversified index funds.

Scenario 2: You're financially stable, company stock is 5% of your net worth

- Refreshers vest: 100 shares at $200 = $20,000

- Net worth: $400,000 (company stock currently $20,000)

- Recommendation: Sell 75% ($15,000). Keep 25% ($5,000) if you believe in the company. This keeps you under 10% concentration.

Scenario 3: Company stock is 40% of your net worth

- Refreshers vest: 150 shares at $180 = $27,000

- Net worth: $300,000 (company stock currently $120,000)

- Recommendation: Sell 90%+ immediately. You're one bad earnings report away from losing your net worth AND potentially your job. Get to 15% or less.

Scenario 4: You need a house down payment in 6 months

- Refreshers vest: 250 shares at $160 = $40,000

- Down payment needed: $50,000

- Recommendation: Sell 100% today. Lock in that money. The stock could drop 20% before you buy the house.

Why Selling Immediately Makes Sense

When you sell at vest, you avoid three problems:

Problem 1: Capital gains complexity. Sell immediately and you pay zero capital gains. Hold for months and now you're tracking cost basis and short-term vs. long-term gains.

Problem 2: Speculation. Holding shares because "the stock might go up" is gambling. You're betting on your company with money you already earned. Would you take your paycheck and buy more company stock? Probably not.

Problem 3: Concentration risk. Every share you hold increases your risk. Your salary already depends on this company. Don't double down.

What About FOMO?

Yes, you might sell at $150 and watch the stock hit $200. That stings.

But you might also sell at $150 and watch it drop to $90. You just saved yourself from a 40% loss on money you need.

Remember: you're not trying to maximize every dollar. You're trying to build stable wealth while managing risk. Selling at vest does that.

Keep Just Enough to Stay Engaged

Want to keep some skin in the game? Fine. Keep 10-25% of each vest. That's enough to benefit if the stock soars, but not enough to wreck you if it crashes.

The rest? Sell it. Use that money for real goals. Pay off your student loans. Max out your 401(k). Buy a diversified index fund. Save for your kid's college. These are concrete wins, not hypothetical stock gains.

Now that you know when to sell, let's talk about your action plan for managing refreshers going forward.

Your Refresher Action Plan: What to Do This Week

Think of this like a pilot's pre-flight checklist. You don't need to do everything perfectly. You just need to check the important stuff before takeoff.

Here's what to do in the next 7 days:

1. Find all your grants (Monday, 15 minutes)

Log into your equity portal. For most big tech companies, that's E*TRADE, Fidelity, Morgan Stanley, or Schwab. Take screenshots of every grant you have. Look for anything labeled "RSU Grant" or "Equity Award."

2. Build your tracking spreadsheet (Tuesday, 20 minutes)

Open Google Sheets or Excel. Make columns for: Grant Date, Total Shares, Vesting Schedule, and Next Vest Date. List every grant, including your initial hire grant and all refreshers.

Example: "April 2023 Refresher, 200 shares, 25% per year, Next vest: April 2025"

3. Calculate your next 12 months (Wednesday, 10 minutes)

Add up everything that vests in the next year. If your stock is at $150 and you have 300 shares vesting, that's $45,000 before taxes (about $27,000 after).

4. Check your concentration risk (Thursday, 10 minutes)

Is your company stock more than 20% of your total savings and investments? If yes, you're probably too concentrated. That's your signal to sell some at the next vesting.

5. Set your vesting reminders (Friday, 10 minutes)

Put a calendar reminder for one week before each vesting date. Title it: "RSU vesting soon. Decide: sell or hold?" This gives you time to think before the shares hit your account.

6. Pick your sell/hold rule now (Friday, 10 minutes)

Decide your default action before emotions kick in. Many smart employees use: "Sell enough to cover taxes plus 20% more." Write it down.

7. Ask about refresher timing (optional)

If you're approaching year 2 or 3 at your company, ask your manager: "When does our team typically get refresher grants?" Most managers will tell you.

You just did what 80% of employees never do. You know what you have, when it vests, and what you'll do about it. That's huge.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis