The ISO AMT Trap: How Exercising Stock Options Can Cost You Thousands in Unexpected Taxes

Why exercising your incentive stock options could trigger a massive tax bill - even if you haven't sold anything yet

Published March 14, 2026 · Updated March 14, 2026

The ISO AMT trap catches thousands of employees off guard every year. When you exercise incentive stock options, you might owe Alternative Minimum Tax on paper gains you haven't actually received - sometimes tens or hundreds of thousands of dollars. This guide explains exactly how the trap works and how to avoid it.

The Story of Sarah: How a $200,000 Tax Bill Appeared Out of Nowhere

Sarah was living the startup dream. She joined a promising tech company in 2020 as employee #47, with 50,000 stock options at a $1 strike price. By 2023, the company had raised a massive Series C round. Her options were now worth $5 per share on paper.

She did the math. If she exercised all 50,000 options, it would cost her $50,000 (50,000 shares × $1 strike price). But the shares were worth $250,000 (50,000 shares × $5 current value). A $200,000 gain, all locked in before the company went public.

Sarah pulled money from her savings and exercised everything in November 2023. She didn't sell a single share. The stock sat in her account, waiting for the eventual IPO.

Here's where everything went wrong.

In April 2024, Sarah sat down with her accountant to file her taxes. "You owe $56,000 in Alternative Minimum Tax," he told her. "It's due by April 15th."

Sarah was confused. "But I didn't sell anything. I never got any money."

"Doesn't matter," her accountant explained. "The IRS sees that $200,000 spread between your strike price and the fair market value. They want their cut now."

Sarah had to drain what was left of her savings to pay taxes on shares she couldn't sell. Her money was locked up in private stock that might be years away from liquidity.

This nightmare is called the ISO AMT trap. It happens to smart, well-meaning employees every single day. Let's break down what went wrong and how you can avoid Sarah's mistake.

What Is the Alternative Minimum Tax (AMT)?

Here's the frustrating truth: every April, you actually calculate your taxes twice. Once using the regular tax system you know. And once using a completely separate system called the Alternative Minimum Tax.

Think of it like having two scorekeepers at a basketball game. One uses the normal rules. The other uses a different rulebook where certain plays count for more points. At the end of the game, you have to accept whichever scorekeeper says you scored higher.

How the two-system approach works:

- You calculate your tax bill using regular income tax rules

- You calculate it again using AMT rules

- You pay whichever amount is higher

The AMT system was created in 1969 after Congress discovered 155 millionaires had paid zero income tax. The idea was simple: create a backup tax system that limits deductions and adds back certain income that regular tax ignores.

For decades, AMT mostly hit wealthy people. But the income thresholds haven't kept pace with inflation, and now middle-class folks with ISOs get caught in the trap.

Here's a concrete example:

You're a software engineer earning $120,000. Under regular tax rules, your federal bill is $15,000. But you also exercised some ISOs this year. When you run the AMT calculation, it says you owe $18,000. You pay $18,000. That $3,000 difference is your AMT liability.

The key difference? AMT adds back the "bargain element" from your ISO exercise. That's the spread between what you paid for the shares and what they're worth. Regular tax ignores this. AMT treats it as income.

This is why exercising ISOs can trigger a massive, unexpected tax bill even though you haven't sold anything yet. Let's look at exactly how AMT rates work.

Demystifying the AMT & ISOs | The Breakdown Lane

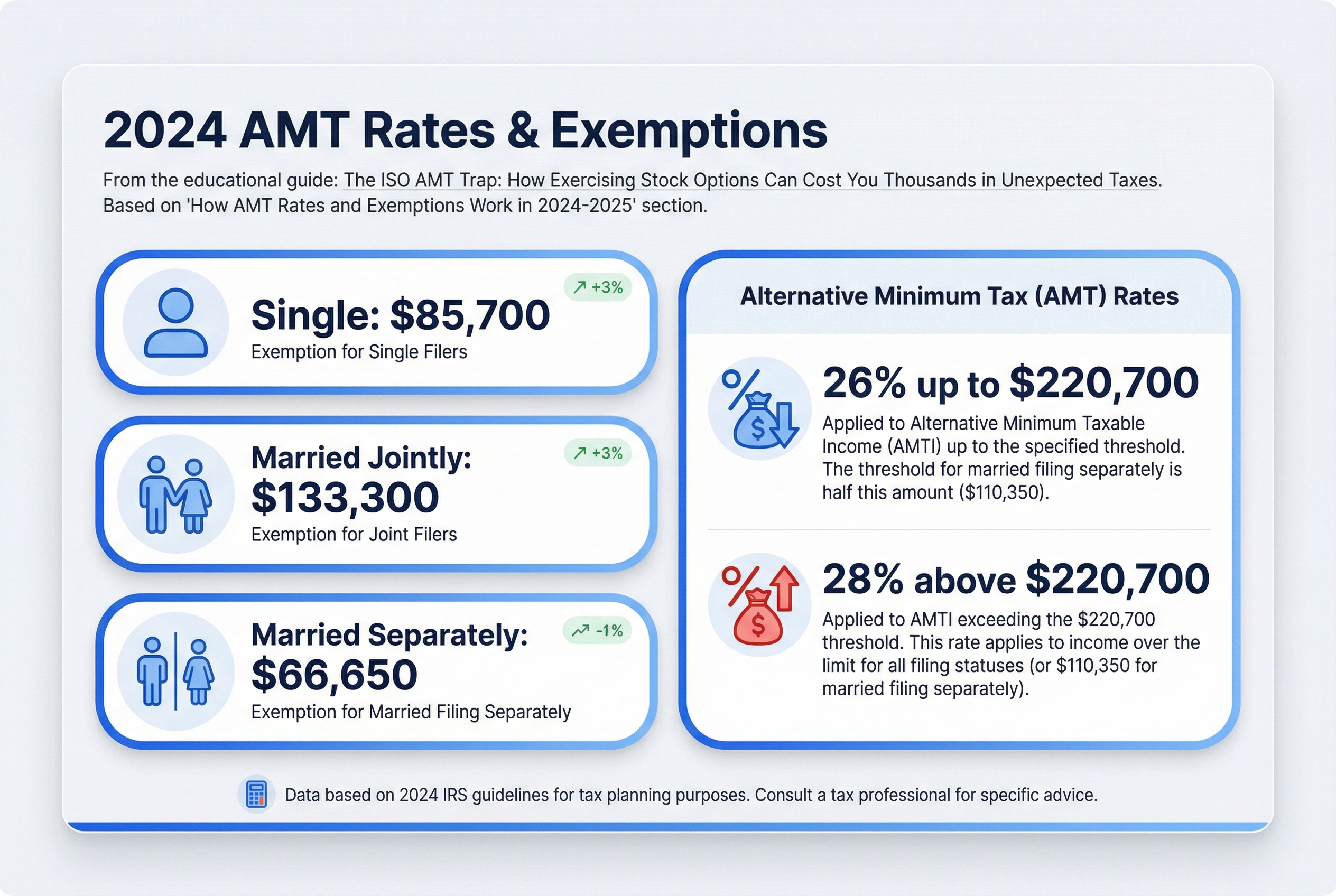

How AMT Rates and Exemptions Work in 2024-2025

AMT has its own tax rates and a built-in "tax-free zone" called an exemption. Think of the exemption like a buffer that protects your first chunk of income from AMT. The problem? This buffer shrinks as you make more money, and it can disappear entirely.

The Two AMT Tax Rates

AMT uses a two-tier system:

- 26% on AMT income up to $220,700

- 28% on AMT income above $220,700

These rates apply after you subtract your exemption (we'll get to that next).

The AMT Exemption: Your Tax-Free Zone

The exemption is like a coupon that reduces your AMT income. For 2024, here's what you get:

| Filing Status | Exemption Amount |

|---|---|

| Single | $85,700 |

| Married filing jointly | $133,300 |

| Married filing separately | $66,650 |

If your AMT income is below the exemption, you owe zero AMT. Simple.

When the Exemption Disappears

Here's the trap: the exemption phases out at higher income levels. It shrinks by 25 cents for every dollar you earn above these thresholds:

- Single filers: Phase-out starts at $609,350

- Married filing jointly: Phase-out starts at $1,218,700

Once your AMT income exceeds these amounts by enough, your exemption vanishes completely.

A Real Example: How ISOs Change Everything

Maria is single and earns $120,000 in salary. Let's see what happens with and without an ISO exercise.

Without ISOs:

- AMT income: $120,000

- Minus exemption: $85,700

- Taxable for AMT: $34,300

- AMT owed: $34,300 × 26% = $8,918

- Regular tax: $18,000

- She pays regular tax (the higher amount)

With a $300,000 ISO exercise:

- AMT income: $120,000 + $300,000 bargain element = $420,000

- Exemption phases out partially

- Remaining exemption: ~$43,000

- Taxable for AMT: $377,000

- AMT owed: ($220,700 × 26%) + ($156,300 × 28%) = $101,166

- Regular tax: still $18,000

- She pays AMT: $101,166

- Extra tax bill: $83,166

Maria went from owing zero AMT to owing over $80,000 in extra taxes. The ISO bargain element pushed her income high enough to trigger AMT and partially erase her exemption.

The Key Takeaway

The exemption protects you when your income is moderate. But ISO exercises add "phantom income" (the bargain element) that can blast you past the exemption and into AMT territory.

Next, we'll break down exactly what this "bargain element" is and why it creates such a massive tax bill.

Understanding the AMT structure: Tax rates and exemption buffers vary based on your filing status.

Understanding the AMT structure: Tax rates and exemption buffers vary based on your filing status.

Why ISOs Trigger AMT: The Bargain Element Explained

Here's the cruel twist that creates the AMT trap: when you exercise ISOs, the IRS treats you differently depending on which tax system it's using.

The bargain element is the gap between two prices:

- Strike price: What you pay to buy the shares (locked in when you got the options)

- Fair Market Value (FMV): What the shares are worth today

Think of it like finding a designer handbag at a garage sale for $100 that's actually worth $500. You got a $400 bargain. The IRS says that $400 bargain is income, but only for AMT purposes.

How the Bargain Element Works

Let's use real numbers. You have 10,000 ISOs with a $2 strike price. Your company just raised money, and the new valuation sets the FMV at $10 per share.

You decide to exercise all 10,000 shares:

- You pay: $20,000 (10,000 shares x $2 strike price)

- The shares are worth: $100,000 (10,000 shares x $10 FMV)

- Your bargain element: $80,000 ($100,000 minus $20,000)

The Double Standard

Here's where it gets weird:

For regular income tax: You pay $0. Exercising ISOs creates no taxable income under normal tax rules. This is the whole point of ISOs, they're supposed to be tax-advantaged.

For AMT: The IRS adds that entire $80,000 bargain element to your income. At the 26% AMT rate, you could owe $20,800 in taxes.

The Phantom Income Problem

This is phantom income. You're paying tax on paper gains you can't access. You spent $20,000 cash to exercise. Now you owe $20,800 in taxes. But if your company is private, you can't sell the shares to pay that bill.

You're out $40,800 in cash, holding illiquid stock, hoping it's worth something someday.

Now let's walk through exactly how to calculate your AMT exposure, step by step.

Don’t Exercise ISOs Before Watching This - AMT Math Explained

Step-by-Step: Calculating Your ISO AMT Exposure

Think of calculating AMT like following a recipe. You need to do each step in order, and skipping one will mess up your final result. Here's how to estimate what you might owe before you exercise those ISOs.

The Six-Step AMT Calculation

Step 1: Calculate your bargain element

This is the "paper profit" the IRS sees when you exercise. Take the fair market value (FMV) minus your strike price, then multiply by the number of shares.

Formula: (FMV - Strike Price) x Number of Shares = Bargain Element

Step 2: Add the bargain element to your regular income

Your AMT income is your salary plus that bargain element. This is why ISOs can push you into AMT territory.

Formula: Regular Salary + Bargain Element = AMT Income

Step 3: Subtract the AMT exemption

For 2024, single filers get an $85,700 exemption. Married couples get $133,300. But here's the catch: this exemption phases out if you make too much. At incomes above $609,350 (single) or $1,218,700 (married), the exemption starts disappearing.

Formula: AMT Income - AMT Exemption = Taxable AMT Income

Step 4: Multiply by the AMT rate

The AMT rate is 26% on the first $220,700 of taxable AMT income, then 28% above that. Most people fall in the 26% bracket.

Formula: Taxable AMT Income x 26% = Tentative AMT

Step 5: Calculate your regular tax

Figure out what you'd pay in normal federal income tax on just your salary (without the ISO exercise).

Step 6: Find the difference

If your tentative AMT is higher than your regular tax, you owe the difference. That's your AMT bill.

Formula: Tentative AMT - Regular Tax = AMT Owed (if positive)

Real Example: James's $21,118 Surprise

James earns $150,000 as a software engineer. He wants to exercise 20,000 ISOs with a $1 strike price. His company just got a 409A valuation at $8 per share.

Step 1: Bargain element = ($8 - $1) x 20,000 = $140,000

Step 2: AMT income = $150,000 + $140,000 = $290,000

Step 3: Minus exemption = $290,000 - $85,700 = $204,300 taxable

Step 4: Tentative AMT = $204,300 x 26% = $53,118

Step 5: His regular tax on $150,000 salary = approximately $32,000

Step 6: AMT owed = $53,118 - $32,000 = $21,118

James owes an extra $21,118 in April just because he exercised his ISOs. He didn't sell anything. He didn't make any cash. But the tax bill is very real.

Your Quick Estimate

Want a rough ballpark? Multiply your bargain element by 26%. That's often close to your AMT exposure, especially if you're a typical tech employee earning $100,000 to $300,000.

Important Warnings

This calculation is simplified. It doesn't include state taxes (which can add another 5% to 13%). It assumes you're taking the standard deduction. It doesn't account for other AMT preference items you might have.

Use this as a starting point to understand your risk. Before exercising a large number of ISOs, get exact numbers from a CPA or tax software.

The good news? You don't lose this AMT payment forever. The AMT credit system lets you recover it in future years, which we'll explain next.

The AMT Credit: Getting Your Money Back (Eventually)

Here's the good news: AMT you pay on ISO exercises isn't lost forever. It's more like a forced loan to the IRS.

Think of it like store credit. You paid extra at checkout this year, but you get a credit to use later when the regular tax system charges you more than AMT would. The bad news? You might wait years to use that credit, and you're out the cash the whole time.

How the AMT credit works:

When you pay AMT from exercising ISOs, the IRS gives you a tax credit for the difference. You can use this credit in future years when your regular tax exceeds your AMT. You recover the credit when you return to the regular tax system.

This often happens when you sell your ISO shares. The sale removes the ISO bargain element from your AMT calculation, which usually pushes you back to regular tax.

Here's a real example:

In 2024, you exercise ISOs and pay $30,000 in AMT. This creates a $30,000 AMT credit on your tax return.

In 2025, your regular tax is $45,000 and your AMT is $40,000. You owe $45,000 in regular tax, but you can apply $5,000 of your AMT credit. You pay $40,000 instead. Your remaining credit is $25,000.

In 2026, you can use more of it. Maybe another $8,000. Then $10,000 in 2027. Eventually, over several years, you recover the full $30,000.

The catch: You've been out that $30,000 the whole time. If it takes five years to recover, that's five years you couldn't invest that money or use it to pay off debt.

What if the stock crashes?

If your ISO shares become worthless before you sell them, you might never recover the full credit. The credit carries forward indefinitely, but you need enough regular tax liability to use it. If you stay in AMT territory year after year, recovery can take a very long time.

The AMT credit provides eventual relief, but it doesn't solve the immediate cash flow problem. Let's look at real scenarios where this timing mismatch creates serious financial stress.

Real AMT Trap Scenarios: When Good Decisions Go Wrong

These scenarios show how smart, well-intentioned employees get caught in the AMT trap. Think of it like planning a road trip based on today's gas prices, only to find out you have to pay based on last year's prices instead.

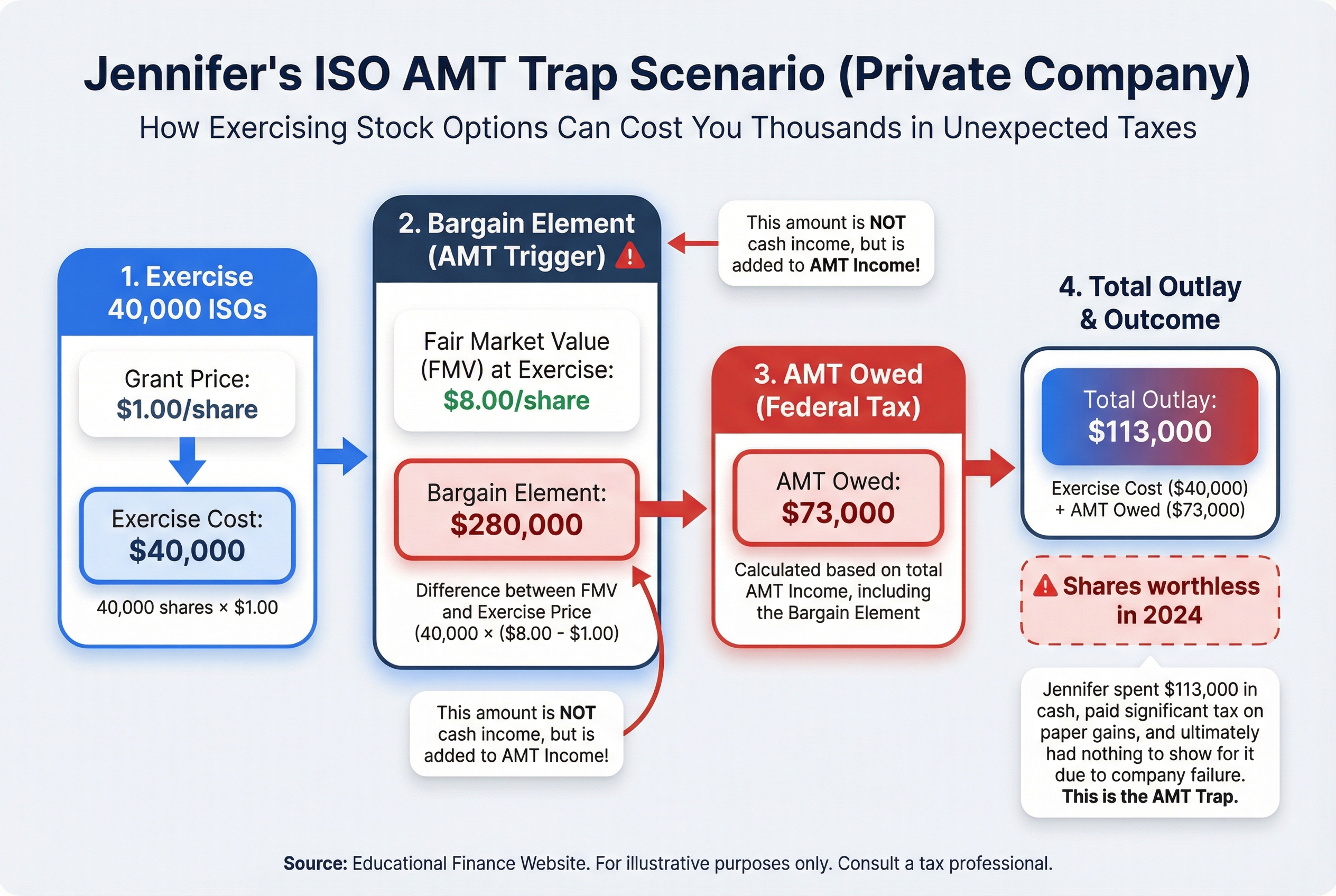

Scenario 1: The Pre-IPO Exercise That Never Paid Off

Meet Jennifer, Senior Engineer at a Promising Startup

Jennifer exercised 40,000 ISOs in 2022 when her company's FMV was $8 per share. Her strike price was $1.

The math:

- Exercise cost: 40,000 x $1 = $40,000

- Bargain element: 40,000 x ($8 - $1) = $280,000

- AMT owed: $73,000

Jennifer paid $113,000 total ($40,000 exercise + $73,000 AMT). She believed in the company. The IPO seemed 18 months away.

What happened: The company ran out of runway in 2024. No IPO. No acquisition. Her shares are worthless. She's out $113,000 with nothing to show for it. The AMT credit sitting on her tax return is useless because she doesn't make enough to ever use it.

Scenario 2: The Down Round Trap

Meet Marcus, Engineering Manager

Marcus exercised 30,000 ISOs in 2023 when FMV was $12 per share. His strike price was $2.

The math:

- Exercise cost: 30,000 x $2 = $60,000

- Bargain element: 30,000 x ($12 - $2) = $300,000

- AMT owed: $78,000

- Total paid: $138,000

What happened: The company had a rough 2024. They raised a down round at $3 per share. Marcus's shares are now worth $90,000 (30,000 x $3). He paid $138,000 for stock worth $90,000. He's $48,000 in the hole, and the stock is still illiquid. He can't sell to recover his losses.

The AMT was calculated on the $12 valuation. That number is locked in, even though the real value dropped to $3.

Scenario 3: The All-at-Once Mistake

Meet Priya, Product Manager

Priya had 50,000 vested ISOs. She exercised them all in one year.

Option A (what Priya did):

- Exercised all 50,000 ISOs in 2024

- Bargain element: $400,000

- AMT owed: $104,000

Option B (what she could have done):

- Exercised 12,500 ISOs per year for four years

- Bargain element per year: $100,000

- AMT owed per year: $0 (stayed under exemption)

- Total AMT over four years: $0

By exercising everything at once, Priya paid $104,000 in AMT that she could have avoided entirely by spreading exercises across multiple years.

Scenario 4: The High Earner's Double Hit

Meet David, VP of Engineering

David earns $350,000 in salary. He exercised 20,000 ISOs with a $150,000 bargain element.

The problem: High earners lose AMT exemption benefits. For every dollar you earn above $609,350 (married filing jointly), you lose 25 cents of your AMT exemption.

David's math:

- Regular AMT exemption: $133,300

- His reduced exemption: $0 (income too high)

- AMT on $150,000 bargain element: $39,000

- Plus he's already paying high regular taxes on his salary

David got hit twice. His high salary eliminated his AMT protection, then his ISO exercise triggered AMT anyway.

The Common Thread

Notice the pattern? Every scenario involves paying real money for stock you can't sell. You're locked in twice: once by the illiquid stock, once by the tax timing.

The next section shows you how to avoid these traps before you fall into them.

AMT Tax Trap: How Stock Options Can Cost You $50,000+ | Startup Finance Explained

Jennifer's story highlights the risk of exercising ISOs in private companies when the IPO fails to materialize.

Jennifer's story highlights the risk of exercising ISOs in private companies when the IPO fails to materialize.

How to Avoid the AMT Trap: Exercise Strategies That Work

Good news: you don't have to fall into the AMT trap. Think of AMT like portion control at a buffet. You can pile your plate sky-high, but you'll pay for it later. Better to make multiple trips with smaller portions.

Here are five strategies that actually work:

Strategy 1: Stay Under the AMT Exemption Amount

How it works: Exercise only enough ISOs each year to keep your bargain element under $85,700 (single filers) or $133,300 (married filing jointly) for 2024.

Example: Your ISOs have a strike price of $10 and current FMV is $20. You can exercise up to 8,570 shares and stay under the single filer exemption. Bargain element: 8,570 shares x $10 spread = $85,700. AMT owed: $0.

Best for: People with large ISO grants who can be patient.

Tradeoff: Takes multiple years. Stock price might go up (good) or down (bad) while you wait.

Strategy 2: Spread Exercises Over Multiple Years

How it works: Break one big exercise into several smaller ones across 3-4 years.

Example: You want to exercise 40,000 ISOs with a $320,000 bargain element. Instead of doing it all at once (triggering $83,200 in AMT), spread it over four years.

- Year 1: Exercise 10,000 shares, $80,000 bargain element, $0 AMT

- Year 2: Exercise 10,000 shares, $80,000 bargain element, $0 AMT

- Year 3: Exercise 10,000 shares, $80,000 bargain element, $0 AMT

- Year 4: Exercise 10,000 shares, $80,000 bargain element, $0 AMT

Total AMT paid: $0 instead of $83,200. You've saved $83,200 by being patient, though you take on more risk of stock price changes over time.

Best for: Anyone who can afford to wait and has years left before ISOs expire.

Tradeoff: More time in the market means more uncertainty. If the stock tanks in year 3, you might regret not exercising earlier.

Strategy 3: Exercise During Low-Income Years

How it works: Time your ISO exercise for years when your regular income drops, like during a sabbatical, parental leave, or between jobs.

Example: You normally earn $200,000. You take a 6-month sabbatical and earn only $100,000 that year. Your AMT exemption phases out more slowly with lower income, giving you more room to exercise ISOs without triggering AMT.

Best for: People with planned career breaks or income fluctuations.

Tradeoff: Requires flexibility and planning. You can't always control when low-income years happen.

Strategy 4: Same-Year Sale (Exercise and Sell Immediately)

How it works: Exercise your ISOs and sell the shares in the same calendar year. This disqualifies them from ISO tax treatment, so they're taxed like regular income instead.

Example: Exercise 10,000 ISOs at $10 strike price when FMV is $30. Sell immediately. You pay regular income tax on the $20 spread ($200,000), but zero AMT.

Best for: People who need cash now and don't want AMT risk.

Tradeoff: You lose the potential long-term capital gains tax benefit of ISOs. You'll pay 35-37% federal tax instead of 20% if you'd held the shares long enough.

Strategy 5: Model Before You Move

How it works: Use AMT calculators to test different exercise scenarios before you commit. Plug in various numbers of shares, timing, and your income to see the AMT impact.

Best for: Everyone. This should be step one, not step five.

Tradeoff: Takes time and effort. You might need to run 10-20 scenarios to find the sweet spot.

Where to start: IRS Form 6251 instructions, TurboTax's AMT calculator, or a tax professional who specializes in equity compensation.

The key insight: you have control here. AMT isn't something that just happens to you. With planning, you can exercise your ISOs and keep your tax bill manageable.

But what if you work at a private company? The rules change completely, and not in a good way. Let's look at why private company ISOs create an even nastier version of the AMT trap.

The Public vs. Private Company AMT Difference (What Your HR Won't Tell You)

Here's the thing your HR department probably won't mention: exercising ISOs at a public company versus a private startup is like comparing cash in your wallet to equity in your house. Both are valuable, but only one can pay for groceries today.

The public company advantage is huge. You can sell your shares the same day you exercise them. This means you can cover your AMT bill immediately, even if you need to dig into your savings first.

Let's see how this plays out:

David at Public Company XYZ:

- Exercises 15,000 ISOs

- Bargain element: $150,000

- AMT bill due: $39,000

- His solution: Immediately sells 4,000 shares at market price for $40,000

- Pays the $39,000 AMT from the sale proceeds

- Keeps 11,000 shares for potential long-term gains

David had options. He could sell just enough to cover taxes. He could sell everything. He could hold everything and pay from savings. The key word is could.

Rachel at Private Startup ABC:

- Exercises 15,000 ISOs

- Bargain element: $150,000

- AMT bill due: $39,000

- Her reality: Cannot sell any shares (no public market exists)

- Must pay $39,000 from personal savings

- Holds illiquid stock that might be worth $0 or $1 million someday

- Won't know the outcome for years

Rachel has no options. She needs $39,000 in cash, period.

This is the AMT trap at its worst. Private company employees face two risks: paying AMT on paper gains and the possibility their stock becomes worthless before they can ever sell it. You're betting real cash today on uncertain value tomorrow.

Most employees don't grasp this difference until they're sitting across from their accountant, staring at a five-figure tax bill they can't avoid. HR departments rarely explain it clearly. They'll walk you through how to exercise your options, but they won't tell you that you're about to write a check for taxes on money you haven't actually made yet.

The bottom line: Public company ISOs carry AMT risk. Private company ISOs carry AMT risk plus total liquidity risk. It's the difference between a calculated bet and a blind gamble.

Fortunately, you're not completely stuck if you're at a private company. Let's look at ways to finance your ISO exercise and AMT bill.

Liquidity Solutions: Financing Your ISO Exercise and AMT Bill

You want to exercise your ISOs, but you don't have $100,000 sitting in your checking account. You're not alone. Most people need to find creative ways to pay for the exercise cost plus the AMT bill.

Think of it like buying a car. You can pay cash, take out a loan, or lease. Each option gets you the car, but the costs and risks are completely different.

Non-Recourse Loans: Borrow Against Your Stock

A non-recourse loan is money borrowed specifically to exercise ISOs. The loan is secured only by the stock itself. If the stock becomes worthless, you walk away. You don't owe the money back.

Here's how it works:

The good scenario: You want to exercise 25,000 ISOs. Exercise cost is $50,000. The bargain element is $200,000, so your AMT bill is $52,000. Total cash needed: $102,000.

You take a non-recourse loan for $102,000 at 10% annual interest. Three years later, your company goes public. The stock is worth $750,000. You sell, repay the loan ($102,000) plus interest ($33,000), and keep $615,000 in profit.

The bad scenario: Same setup, but the company fails. Your stock is worth $0. You walk away from the loan. You owe nothing. But you've lost three years of potential returns on $33,000 in interest payments.

Typical interest rates: 7% to 15% depending on how risky lenders think your company is. Safer companies (close to IPO) get lower rates.

Personal Loans: You're on the Hook

Regular personal loans use your credit score, not your stock. You borrow $100,000, you owe $100,000 back no matter what happens to your shares.

Interest rates are typically lower (5% to 10%), but the risk is all yours. If your company tanks, you still make monthly payments.

Secondary Sales: Sell Shares for Cash

Some private companies allow employees to sell shares to private buyers before an IPO. You sell 5,000 shares at $20 each, get $100,000 in cash, use it to exercise more options.

The catch: You pay taxes immediately on the sale. And you give up future upside on those shares.

Tender Offers: Company-Sponsored Sales

Occasionally, companies run tender offers where they buy back employee shares or arrange sales to investors. These are rare and usually limited (you might only sell 10% to 20% of your holdings).

The bottom line: These aren't free money. Each option has significant costs. Non-recourse loans protect you from total loss but charge high interest. Personal loans are cheaper but riskier. Secondary sales mean paying taxes now and giving up growth.

Before you borrow six figures to exercise options, you need expert guidance on whether the math makes sense for your situation.

When to Get Professional Help: Tax Planning for Large ISO Exercises

Think of ISO tax planning like home repairs. You can change a lightbulb yourself. But when you need to rewire the entire house? You call an electrician. The same logic applies here.

Here's when the stakes are high enough to need professional help:

If your potential AMT exceeds $10,000, consider getting professional advice. If it exceeds $50,000, definitely get help. And if your bargain element (spread between strike price and FMV) exceeds $200,000? Don't even think about going it alone.

Red Flags You Need Help Now

You should talk to a professional if you have:

- Multiple types of equity compensation (ISOs, NSOs, RSUs all at once)

- High regular income (over $200,000)

- Complex family situations (dependents, divorce, estate planning)

- A major life change coming (sabbatical, home purchase, career change)

- ISOs at multiple companies

Who to Hire and What to Ask

Look for a CPA with equity compensation experience. Not just any tax preparer. Ask them:

- "How many ISO clients do you work with each year?"

- "What strategies do you typically recommend?"

- "What's your fee structure for tax planning versus tax preparation?"

You might also consult a Certified Financial Planner (CFP) for broader financial planning or a tax attorney if you're dealing with very large amounts (over $1 million in bargain element).

What It Costs (And What You Get)

Typical costs run $500 to $3,000 for tax planning and modeling. Tax preparation adds another $200 to $500.

Here's why it's worth it: You're considering exercising ISOs with a $400,000 bargain element. Your potential AMT? $104,000. Ouch.

You hire a CPA specializing in equity compensation for $2,500. They model multiple scenarios. They recommend spreading your exercise over three years, with specific timing around your planned sabbatical when your income will be lower.

This strategy reduces your total AMT to $28,000. You just saved $76,000. That $2,500 fee returned 30x its value. Plus, you sleep better knowing you have a solid plan instead of guessing.

A good professional doesn't just calculate numbers. They model different scenarios. They show you the tradeoffs. They help you understand what happens if the stock price moves up or down.

Getting help isn't a sign of weakness. It's the smart move when thousands of dollars are on the line.

Now that you know when to call in the experts, let's wrap up with a clear action plan you can start using today.

Your ISO AMT Action Plan: What to Do Right Now

Think of this action plan like a flight pre-check. Do these things before takeoff, and you'll avoid major turbulence with the AMT.

This Week: Get Your Facts Straight

You need three numbers to start planning:

- Find your ISO grant documents. Look for strike price and vest dates. Check your email for "stock option grant" or ask HR.

- Get current fair market value (FMV). Public company? Check today's stock price. Private company? Ask HR for the latest 409A valuation.

- Calculate your bargain element. Multiply (FMV minus strike price) times number of vested shares.

Example: You have 10,000 vested ISOs with a $5 strike. Current FMV is $15. Your bargain element is ($15 - $5) x 10,000 = $100,000.

This Month: Model Your Risk

- Use an online AMT calculator. Input your salary, filing status, and bargain element. You'll get a rough AMT estimate.

- Is your AMT over $10,000? Time to find professional help. Research CPAs or tax attorneys who specialize in equity compensation.

- Under $10,000? You might handle this yourself, but a one-time consultation ($500-$1,000) can save you much more.

This Quarter: Build Your Strategy

- Model 2-3 exercise scenarios. What happens if you exercise 25% of your options this year? 50%? All at once?

- Compare total AMT across scenarios. Spreading exercises over multiple years almost always wins.

Real Example: Marcus Avoids the Trap

Marcus works at a private company. He has 40,000 vested ISOs with a $3 strike price. Current FMV: $9.

This week: Marcus confirmed the $9 FMV and calculated his bargain element: ($9 - $3) x 40,000 = $240,000.

This month: He used an AMT calculator. Exercising all 40,000 shares at once would trigger $62,400 in AMT. He scheduled consultations with two CPAs who specialize in startup equity.

Next month: His CPA recommended a three-year plan:

- Year 1: Exercise 14,000 shares (stays under AMT exemption)

- Year 2: Exercise 13,000 shares

- Year 3: Exercise 13,000 shares

Total AMT with this plan: $0 instead of $62,400.

Marcus now has a clear roadmap and saved over $60,000.

This Year: Lock In Your Plan

- Create a multi-year exercise strategy. Write down how many shares you'll exercise each year and why.

- Set calendar reminders. Review your plan every December before the year ends.

- Track your AMT credit. If you do pay AMT, you'll get it back eventually. Keep records.

Ongoing: Stay Alert

Review your strategy when:

- Your company's valuation changes significantly (up or down)

- You get promoted or your salary increases substantially

- Tax laws change (rare, but it happens)

- You're within 12 months of a potential IPO or acquisition

Quick Decision Flowchart

Are you at a public or private company?

- Public: You can sell shares immediately. AMT risk is lower, but still calculate it.

- Private: You cannot sell. AMT risk is higher. Spread exercises over multiple years.

Have you already exercised ISOs this year?

- Yes: Calculate your current AMT exposure now. You might need to adjust withholding or make estimated tax payments.

- No: You have time to plan. Use it.

Is your potential AMT over $10,000?

- Yes: Get professional help. The cost of a CPA ($1,500-$3,000) is tiny compared to the AMT you'll avoid.

- No: You can probably manage this yourself with online tools and calculators.

You Now Have the Knowledge

The ISO AMT trap catches people who don't know it exists. You know better now. You understand how the bargain element creates phantom income. You know AMT rates and exemptions. You've seen real scenarios where people lost six figures.

Most importantly, you have a concrete action plan. Start this week. Get your numbers. Model your scenarios. Build your strategy.

The difference between getting trapped and staying free is simple: planning ahead. You're already ahead of 90% of people with ISOs just by reading this far.

Now go execute your plan.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis