ESPP Qualifying vs Disqualifying Dispositions: A Simple Guide to Tax Treatment

How holding periods change your tax bill when you sell ESPP shares

Published March 14, 2026 · Updated March 14, 2026

When you sell ESPP shares, the IRS treats the sale differently based on how long you held them. This guide explains qualifying vs disqualifying dispositions in plain English, shows you exactly how each affects your taxes with real dollar examples, and helps you decide which approach makes sense for your situation.

Why Your ESPP Sale Date Matters More Than You Think

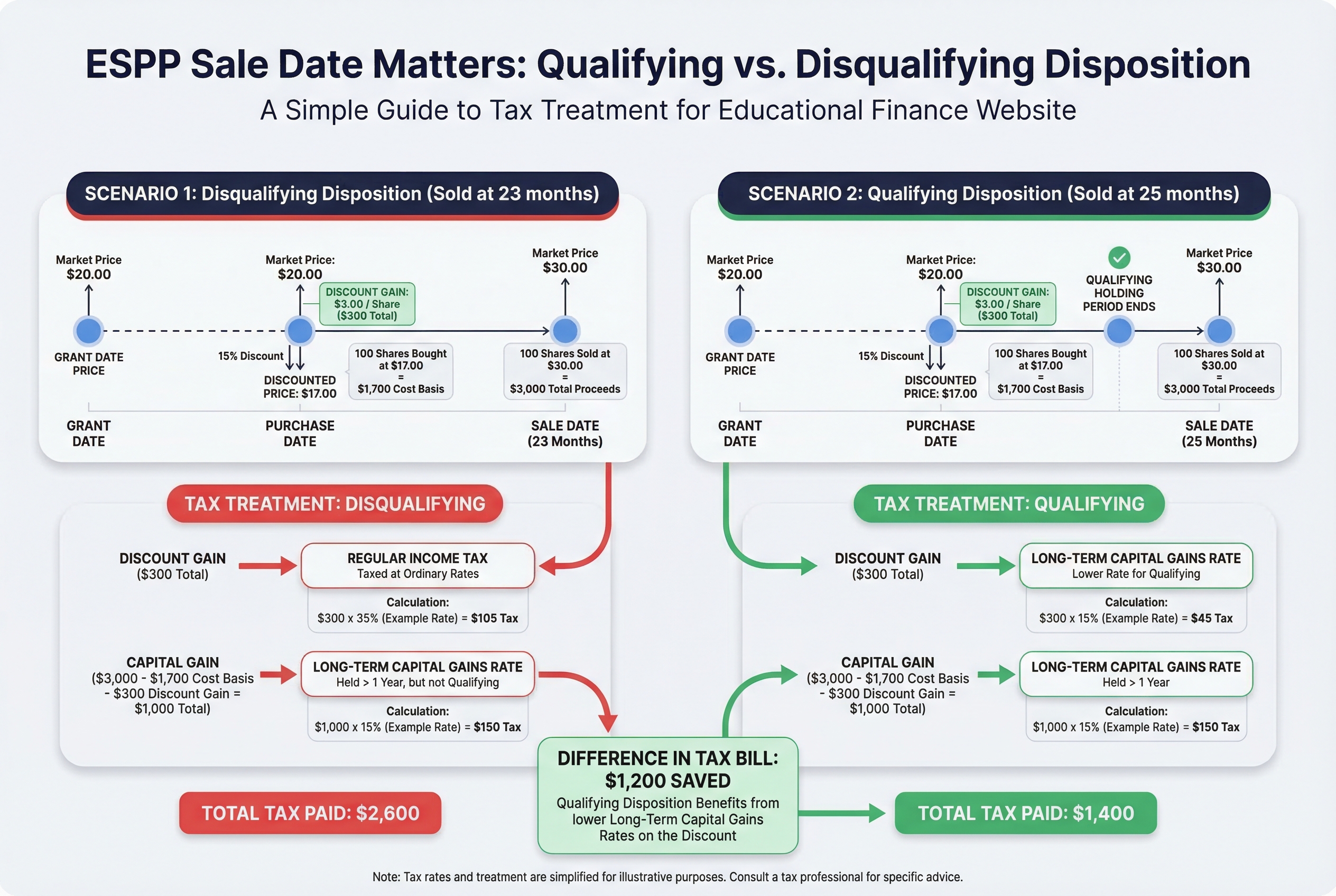

Sarah and Mike work together at the same tech company. Last year, they both bought 100 ESPP shares on the exact same day for $17 each (a 15% discount from the $20 market price). They both sold when the stock hit $30, making the same $1,300 profit.

Sarah sold her shares after 23 months. Mike waited just two more months and sold after 25 months.

The result? Sarah paid $2,600 in taxes. Mike paid $1,400. Same shares, same profit, $1,200 difference in their tax bills.

What happened? The IRS has specific holding period rules for ESPP shares purchased through qualified Section 423 plans (the type most public companies offer). Sell too early, and your discount gets taxed as regular income at your normal rate. Wait long enough, and that same discount gets the lower long-term capital gains rate.

Think of it like aging wine. The wine itself doesn't change, but the right timing unlocks better treatment and more value.

This isn't some obscure tax loophole. It's a straightforward rule that can save you thousands of dollars. The IRS calls these two scenarios "disqualifying dispositions" (selling early) and "qualifying dispositions" (selling after the waiting period).

Most employees have no idea this rule exists. Your HR department probably mentioned it once during onboarding, buried in a 40-page benefits guide you never read.

Here's what you need to know: understanding these two types of sales and their holding periods will help you make smarter decisions about when to sell your ESPP shares.

The difference of just two months in holding time resulted in a $1,200 tax difference between Sarah and Mike.

The difference of just two months in holding time resulted in a $1,200 tax difference between Sarah and Mike.

The Two Types of ESPP Sales: Qualifying and Disqualifying

When you sell ESPP shares, the IRS puts your sale into one of two buckets: qualifying or disqualifying. The difference comes down to how long you held the shares.

Think of it like a video game achievement. You need to unlock two separate milestones to get the "qualifying" badge. Miss either one, and you get "disqualifying" treatment instead.

The Two Holding Periods You Must Meet

For a qualifying sale (the IRS calls it a "qualifying disposition"), you must hold your shares for:

- At least 2 years from the offering date (when your enrollment period started)

- At least 1 year from the purchase date (when you actually bought the shares)

You need to satisfy BOTH requirements. Meeting just one doesn't count.

Here's a Real Example with Dates

Your offering period starts June 1, 2022. You buy shares on December 1, 2022.

For a qualifying sale, you must wait until:

- June 2, 2024 (2+ years from the offering date)

- December 2, 2023 (1+ year from the purchase date)

The later date is June 2, 2024. That's your earliest qualifying sale date.

Sell before June 2, 2024? You have a disqualifying disposition.

What "Disqualifying" Really Means

Don't panic. The term "disqualifying" sounds scary, but you didn't break any rules. It just means you sold before meeting both holding periods. The IRS created these rules to encourage long-term ownership. They give you a tax break if you hold longer.

Many people have disqualifying dispositions. It's a normal choice, not a mistake.

Now that you know the two types, let's look at how taxes work for each one. The tax treatment is where qualifying and disqualifying sales really differ.

Employee Stock Purchase Plans 2026: Section 423 Qualified Dispositions & The 15% Discount

How Taxes Work for Qualifying Dispositions

Think of qualifying disposition as getting a "preferred customer" discount from the IRS. Most of your profit gets taxed at the lower capital gains rate instead of your regular income tax rate.

Here's what happens when you sell ESPP shares as a qualifying disposition:

Only the discount gets taxed as ordinary income. That 15% discount you got when you bought the shares? The IRS treats that like regular wages. But here's the key: they calculate it using the offering date price, not the purchase price.

Everything else is long-term capital gains. Any profit beyond the discount gets the lower tax rate. This is usually where the real tax savings happen.

Step-by-Step Tax Calculation

Let's walk through a real example with actual numbers:

Your ESPP purchase:

- Offering date price:

$20 per share - Purchase price:

$17 per share(15% discount) - Purchase date price:

$25 per share - You bought:

100 shares - Sale price:

$40 per share(qualifying sale after holding periods)

Step 1: Calculate ordinary income (the discount)

- Discount per share:

$20 - $17 = $3 - Total ordinary income:

100 shares × $3 = $300 - This appears on your W-2 like regular wages

Step 2: Calculate long-term capital gains

- Your cost basis:

$20 per share(offering date price) - Gain per share:

$40 - $20 = $20 - Total long-term capital gains:

100 shares × $20 = $2,000

Step 3: Add up your total profit

- Ordinary income:

$300 - Long-term capital gains:

$2,000 - Total profit:

$2,300

What You Actually Pay in Taxes

Let's say you're in the 24% tax bracket for ordinary income and 15% for long-term capital gains:

- Tax on ordinary income:

$300 × 24% = $72 - Tax on capital gains:

$2,000 × 15% = $300 - Total tax bill:

$372

That's an effective tax rate of about 16% on your $2,300 profit. Compare that to ordinary income rates, which can go as high as 37% for top earners. You can see why waiting for qualifying treatment usually saves money.

The math gets different if you sell early. Let's look at disqualifying dispositions next.

How Taxes Work for Disqualifying Dispositions

Think of a disqualifying disposition like the IRS saying "you didn't wait long enough for the special deal, so we're treating part of this as regular income." The tax treatment is more complex than qualifying dispositions, but still manageable once you understand the two-step calculation.

The Bargain Element: Your Discount Becomes Income

Here's the key concept: the discount you got at purchase is called the bargain element. It's always taxed as ordinary income at your normal tax rate, no matter what.

The bargain element is calculated this way:

Bargain Element = (Purchase Date FMV - What You Paid) × Number of Shares

Your employer reports this amount on your W-2, just like your salary. If you're in the 24% tax bracket, you'll pay 24% on this amount.

Additional Gain: It Depends on Your Holding Period

Any profit beyond the bargain element gets taxed based on how long you held the shares after the purchase date:

Held less than 1 year after purchase:

- Short-term capital gains

- Taxed at ordinary income rates (same as your salary)

Held 1+ year after purchase:

- Long-term capital gains

- Taxed at lower capital gains rates (0%, 15%, or 20% depending on income)

Real Example: Disqualifying Sale After 18 Months

Let's use the same scenario as before, but you sell after 18 months (disqualifying):

- Offering date price: $20

- Purchase price (15% discount): $17

- Purchase date price: $25

- Sale price: $40

- Shares: 100

Step 1: Calculate bargain element (ordinary income)

($25 - $17) × 100 shares = $800

Step 2: Calculate additional gain

($40 - $25) × 100 shares = $1,500

Since you held the shares for 1+ year after purchase, the $1,500 qualifies for long-term capital gains treatment.

Your total tax (assuming 24% bracket and 15% capital gains rate):

- Bargain element: $800 × 24% = $192

- Additional gain: $1,500 × 15% = $225

- Total tax: $417

Notice how the holding period after purchase matters. If you'd sold just 11 months after purchase, that $1,500 would be taxed at 24% instead of 15%, costing you an extra $135.

Now that you understand both types of sales, let's put them side by side with real numbers so you can see exactly how much the waiting period affects your tax bill.

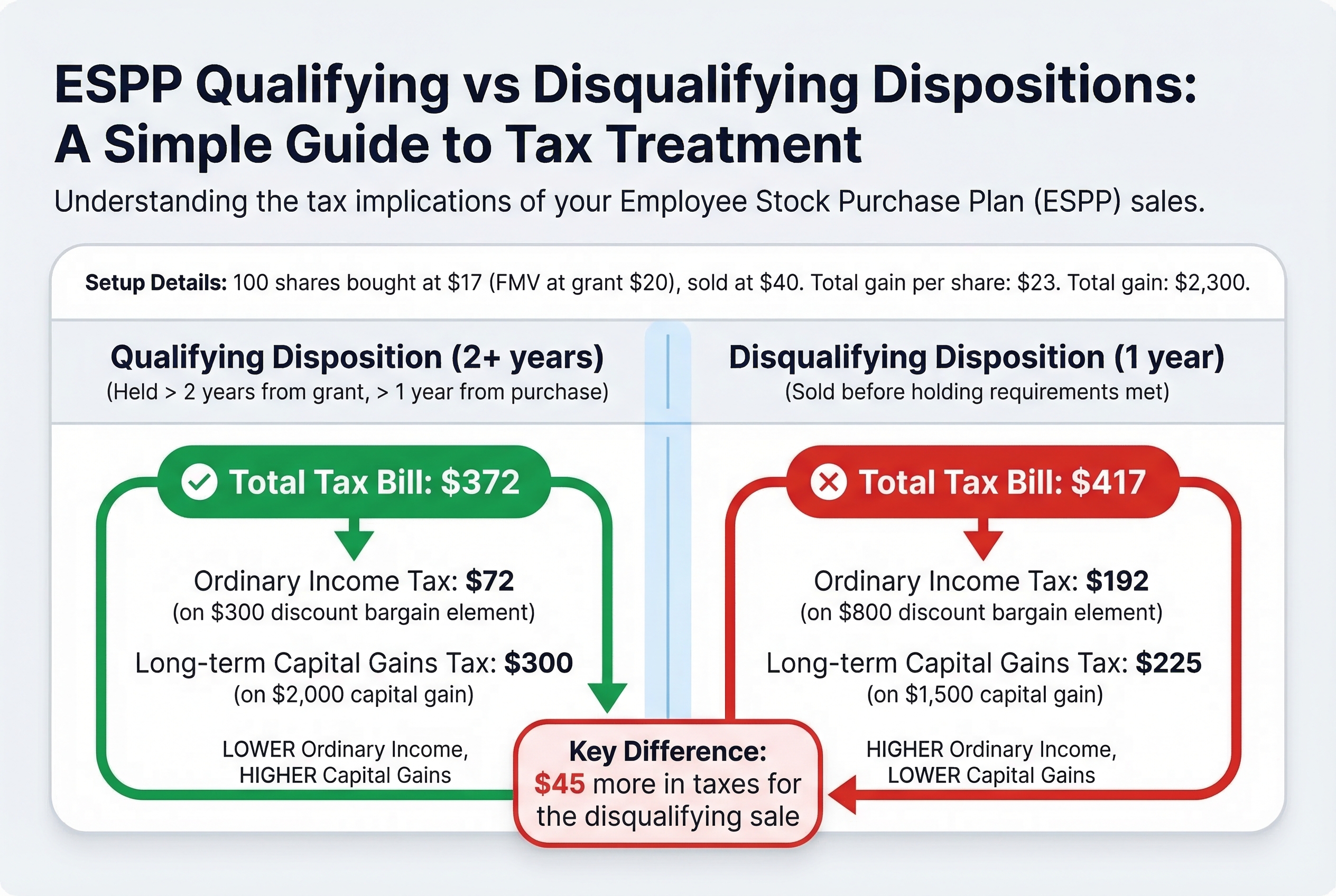

Side-by-Side: Qualifying vs Disqualifying with Real Numbers

Let's watch the same ESPP shares go through both tax treatments. Think of it like choosing between eating a slice of cake now versus waiting for a potentially bigger slice later, but with the risk that the cake might shrink while you wait.

The Setup:

- You buy 100 shares through your ESPP

- Fair market value on offering date: $20

- Your purchase price (with 15% discount): $17

- You sell at: $40 per share

- Your total profit: $2,300

Qualifying Disposition (you waited 2+ years):

You pay ordinary income tax on the smaller of two amounts: your $3 discount per share or your actual $23 gain per share. The discount wins, so you pay ordinary income tax on just $300 total.

- Ordinary income (24% tax bracket): $300 x 24% =

$72 - Long-term capital gains: $2,000 x 15% =

$300 - Total tax bill: $372

Disqualifying Disposition (you sold after 1 year):

You pay ordinary income tax on the full discount plus any gains up to the purchase price.

- Ordinary income (24% tax bracket): $800 x 24% =

$192 - Long-term capital gains: $1,500 x 15% =

$225 - Total tax bill: $417

The difference: $45 more in taxes for the disqualifying sale.

Here's the thing: sometimes paying that extra $45 makes perfect sense. Maybe you needed that $4,000 for a house down payment 18 months earlier. Maybe you wanted to diversify out of company stock sooner. Maybe you believed the stock would drop and you were right.

Lower taxes matter, but they're not everything. You can't spend tax savings if your stock price crashes while you wait.

Next, we'll look at what happens when stock prices move in different directions, because that changes the math in surprising ways.

The ESPP Tax hack you’ll REGRET

Under the specified scenario, waiting for qualifying disposition saved $180 in taxes ($552 vs $372).

Under the specified scenario, waiting for qualifying disposition saved $180 in taxes ($552 vs $372).

What Happens When Stock Prices Move: Scenarios That Change the Math

Stock price movement is like weather during a road trip. Sometimes the sunny route you planned turns stormy, and you need to adjust. The same goes for ESPP sales. Your qualifying vs disqualifying decision depends heavily on where the stock price goes after you buy.

Let's walk through four real scenarios with actual numbers.

Scenario 1: Steady Climb (Qualifying Usually Wins)

You buy 100 shares at $17 (15% discount from $20 offering price). The stock climbs to $28 by the time you hit the qualifying period.

Disqualifying sale at 6 months: You pay ordinary income tax on $1,100 bargain element ($20 - $17 × 100). Then short-term capital gains on $800 ($28 - $20 × 100). Your tax bill is roughly $650 if you're in the 24% bracket.

Qualifying sale at 18+ months: You pay ordinary income tax on just $300 (the discount: $3 × 100). The remaining $1,100 is long-term capital gains at 15%. Total tax: about $240.

When the stock keeps rising, waiting for qualifying treatment saves you real money.

Scenario 2: Spike and Drop (Disqualifying Might Win)

Here's where it gets interesting. Offering price is $20. At purchase, the stock spiked to $30, so your lookback provision gives you 85% of $20 = $17 per share. You buy 100 shares for $1,700.

Six months later, the stock drops to $22. You sell.

Disqualifying sale: Your bargain element is $1,300 (the $30 fair market value at purchase minus your $17 cost). That's ordinary income. But you also have an $800 capital loss ($22 sale price minus $30 FMV at purchase × 100 shares). That loss offsets other investment gains.

If you wait for qualifying: You'd hold through 18 more months of potential drops. The stock could fall to $15. Now you're looking at an actual loss, and you've tied up your money in one company's stock for two years.

Scenario 3: Price Drop After Purchase

You buy at $17 (discounted from $20). The stock falls to $14 before the qualifying period ends.

Disqualifying sale at a loss: You have a $300 capital loss ($17 cost minus $14 sale × 100 shares). No bargain element because you sold at a loss.

Qualifying sale at a loss: Same $300 capital loss. But you waited longer and took on more risk.

When you're sitting on a loss, selling quickly (disqualifying) often makes sense. You free up cash and reduce your concentration risk.

The Lookback Provision Changes Everything

That 85% discount applies to whichever price is lower: offering date or purchase date. Think of it as buying concert tickets at the cheapest price during a six-month window.

If the stock jumps from $20 to $40 during your offering period, you still pay $17 (85% of $20). Your instant gain is huge: $2,300 per 100 shares. This makes the disqualifying vs qualifying math more complex because your bargain element is massive either way.

What This Means for You

Tax savings matter, but they're not the whole story. Holding for qualifying treatment means:

- Market risk: The stock could drop 20% while you wait

- Concentration risk: More of your wealth stuck in one company

- Opportunity cost: That money could be diversified and growing elsewhere

The tax tail shouldn't wag the investment dog. A bird in the hand (selling now with known taxes) often beats two in the bush (waiting for better tax treatment while the stock might crater).

Now that you understand how price movements affect your decision, you need to track the specific dates that determine whether your sale qualifies. Missing a deadline by one day can cost you hundreds or thousands in extra taxes.

How to Track Your Important Dates and Avoid Mistakes

Tracking ESPP dates is like keeping vaccination records. You need them years later, and they're nearly impossible to recreate from memory.

The stakes are real. Sell one day too early, and you lose thousands in tax savings. Lose track of which shares you're selling, and you might owe more than expected.

Find Your Critical Dates First

Your brokerage account holds the information you need. Look for:

- Purchase confirmations (emails or statements showing each ESPP buy)

- Offering period documents (usually in your company HR portal)

- Tax forms from previous years (Form 3922 shows offering and purchase dates)

Important: The offering date is when the offering period starts, not when you enrolled. If you joined mid-period, your offering date is still the period's start date. This matters for your holding period.

Create a Simple Tracking System

Make a spreadsheet with these columns:

- Offering date

- Purchase date

- Number of shares

- Purchase price

- Qualifying sale date (2 years after offering date)

- Status (holding or sold)

Set phone reminders for each qualifying date. Mark them as "ESPP eligible for qualifying treatment."

The FIFO Rule You Must Know

When you sell shares, the IRS assumes you sold your oldest shares first. This is called FIFO (first in, first out).

Example: Maria has three ESPP purchases:

- June 2022 offering, December 2022 purchase (100 shares). Qualifying date: June 2024.

- December 2022 offering, June 2023 purchase (75 shares). Qualifying date: December 2024.

- June 2023 offering, December 2023 purchase (80 shares). Qualifying date: June 2025.

In July 2024, Maria sells 150 shares at $120 each. FIFO means the first 100 shares come from purchase 1 (qualifying disposition, better tax treatment). The next 50 shares come from purchase 2 (disqualifying disposition, higher taxes).

She didn't choose this. FIFO chose for her.

Keep Everything

Save all purchase confirmations, offering documents, and tax forms. You'll need them when filing taxes, sometimes years later.

Some brokerages show holding period information. Most don't. Don't rely on them to track your qualifying dates.

If you have many ESPP purchases across multiple years, consider using tax software designed for stock compensation or working with a tax advisor. The complexity multiplies fast.

Now that you know how to track your dates, let's talk about what your HR department probably hasn't explained about ESPP tax reporting.

What Your HR Department Won't Tell You About ESPP Tax Reporting

ESPP tax reporting is like a relay race. Your company runs the first leg and hands you the baton (tax forms). But you need to run the last leg correctly, or you'll pay taxes twice on the same money.

Here's what actually happens behind the scenes.

The Forms You'll Receive (and When)

Form 3922 arrives after you buy shares, not when you sell them. This is an information form that tells you:

- Your offering date and purchase date

- How much you paid per share

- The fair market value on those dates

- How many shares you bought

Keep this form with your tax records. You'll need it years later when you sell, even for qualifying dispositions.

Your W-2 gets updated in the year you sell shares. For disqualifying dispositions, your company adds the bargain element as ordinary income. For qualifying dispositions, they add the discount (and sometimes additional ordinary income if the stock dropped).

Your 1099-B shows up from your broker. It reports your sale proceeds and cost basis. But here's the catch: the cost basis is almost always wrong for ESPP shares.

Why Your 1099-B Cost Basis Is Incomplete

The 1099-B only shows what you originally paid for the shares. It doesn't include the bargain element that already got taxed as ordinary income on your W-2.

Think of it like buying a discounted laptop at your company store. You paid $800, but your company added $200 to your W-2 as a taxable benefit. Your total tax basis is $1,000, not just the $800 you paid.

Example: John sold 100 ESPP shares (disqualifying) for $4,000. His 1099-B shows proceeds of $4,000 and cost basis of $1,700 (what he paid). His W-2 shows $800 in additional compensation (the bargain element).

When filing taxes, John must adjust his cost basis to $2,500 ($1,700 + $800) to avoid paying tax twice on that $800. If he uses the 1099-B cost basis without adjustment, he'll overpay taxes by about $192.

What to Check Every Year

Compare your W-2 to your records. Did you sell ESPP shares this year? You should see additional compensation on your W-2. No entry there? Contact your stock plan administrator.

Don't trust the 1099-B cost basis blindly. For ESPP shares, you almost always need to adjust it using your W-2 and Form 3922.

Missing forms? Contact your stock plan administrator (not regular HR). They handle equity compensation reporting separately.

Your Responsibility vs Company Responsibility

Your company reports what happened: how much you paid, what the stock was worth, what you sold shares for.

You're responsible for doing the math correctly on your tax return. That means adjusting cost basis and calculating capital gains properly.

The IRS gets copies of all these forms. If your tax return doesn't match what the forms say (after proper adjustments), you'll get a letter asking questions.

Now that you know what forms to expect and why they look the way they do, let's walk through exactly how to report everything correctly on your tax return.

The ESPP Tax Guide Your HR Department Won't Tell You

How to Report ESPP Sales on Your Tax Return Without Losing Your Mind

Filing ESPP taxes is like following a recipe. You need the right ingredients (forms) and steps in the right order. Miss one step, and you might pay taxes twice on the same money.

Here's what you'll actually do when tax season arrives.

The Forms You Need

You'll use two main tax forms:

- Form 8949: This is where you list each stock sale with details

- Schedule D: This summarizes your capital gains and losses from Form 8949

Your broker sends you Form 1099-B showing your sale. Your employer sends Form 3922 showing your ESPP purchase details. Keep both.

The Cost Basis Trick That Saves You Money

This is the most important part. You must adjust your cost basis to avoid double taxation.

For disqualifying sales: Add the W-2 compensation amount to what you paid.

For qualifying sales: Add any ordinary income amount (the discount) to what you paid.

This adjustment prevents the IRS from taxing the same money twice.

Real Example: Disqualifying Sale

You sold 100 shares for $4,000. You originally paid $1,700. Your W-2 shows $800 as ordinary income (the bargain element).

On Form 8949, you enter:

- Proceeds:

$4,000 - Cost basis:

$2,500(that's$1,700+$800) - Capital gain:

$1,500

The $800 is already taxed through your W-2 as ordinary income. By adding it to your cost basis, you only pay capital gains tax on the remaining $1,500.

Without this adjustment, you'd pay tax on $2,300 of gain instead of $1,500. That's paying taxes on $800 twice.

Tax Software Makes This Easier

TurboTax, H&R Block, and other tax software have specific ESPP sections. Answer their questions about your ESPP purchase and sale, and they calculate the adjusted cost basis automatically.

When to hire help: If you made multiple ESPP sales across different years, or you're unsure about qualifying vs disqualifying status, spend $200-400 for a tax professional. It's worth it to get this right.

Keep all your documents: Form 3922, purchase confirmations, sale confirmations, and your brokerage statements. You'll need these if the IRS ever asks questions.

Now that you know how to file, let's talk about whether waiting for qualifying treatment is actually worth the hassle.

Decision Framework: Should You Wait for Qualifying Treatment?

Deciding when to sell your ESPP shares is like deciding when to harvest vegetables from a garden. Waiting might give you a bigger, riper tomato (better tax treatment), but there's always the risk of frost (market crash) or pests (company problems) wiping out your crop. Sometimes the smart move is to pick what you've got.

Here's how to make this decision without losing sleep.

Start With the Actual Dollar Amount

Don't think in percentages. Calculate the real money you'll save.

Quick calculation: Take your ESPP shares' current value, multiply by your tax bracket difference (usually 15-20%), and that's your potential tax savings.

Example: You have $10,000 in ESPP shares. Your tax bracket is 24%. The difference between qualifying (15% long-term capital gains) and disqualifying (24% ordinary income) treatment is 9%. Your tax savings for waiting: $10,000 x 9% = $900.

Now you know what you're deciding about. Is $900 worth the wait and risk?

The Concentration Risk Test

Rule of thumb: Your employer stock should never exceed 10-15% of your total investments.

Calculate this right now:

- Add up all your investments (401k, IRA, taxable accounts, ESPP)

- Divide your ESPP value by that total

- If it's over 15%, you have too many eggs in one basket

Think of it this way: your paycheck already depends on your company. Your health insurance depends on your company. Don't make your retirement depend on them too.

Walk Through This Decision Tree

Question 1: How long until qualifying treatment?

- Less than 2 months away → Easier to wait

- More than 6 months away → Harder to justify waiting

Question 2: How much will you actually save in taxes?

- Less than $500 → Probably not worth the risk

- $500 to $2,000 → Consider other factors carefully

- More than $2,000 → Strong reason to wait (if other factors align)

Question 3: What's your concentration risk?

- Employer stock under 10% of portfolio → Safer to hold

- 10-20% → Yellow flag, be cautious

- Over 20% → Red flag, sell regardless of tax treatment

Question 4: Do you need the money soon?

- Need cash for emergency, down payment, or debt → Sell now

- No immediate need → Can consider waiting

Question 5: How's your company doing?

- Stable company, good news, steady stock → Lower risk to wait

- Industry downturn, layoff rumors, executive departures → Sell now

- Recent major customer loss or bad earnings → Sell now

Real Decision Scenarios

Scenario 1: Don't wait

You have $10,000 in ESPP shares that qualify in 3 months. Tax difference between selling now vs waiting: $300. But employer stock is 40% of your net worth. Your company just lost a major customer. The market has been volatile.

Decision: Sell now. The $300 tax savings isn't worth the concentration risk plus company-specific risk. You're gambling $10,000 to save $300. Bad bet.

Scenario 2: Wait it out

You have $15,000 in ESPP shares that qualify in 1 month. Tax difference: $2,000. Your company is stable with good earnings. Employer stock is 8% of your portfolio. You don't need the cash.

Decision: Wait the month. You're saving $2,000 by waiting 30 days. Your concentration risk is manageable. The company looks solid. This is a reasonable wait.

Scenario 3: Split the difference

You have $20,000 in ESPP shares that qualify in 4 months. Tax difference: $1,200. Employer stock is 18% of your portfolio. Company is stable but you're nervous about concentration.

Decision: Sell half now, wait on the other half. You immediately reduce concentration risk to 9%. You still get $600 in tax savings on the half you wait on. You sleep better at night.

What Matters More Than Tax Savings

Your peace of mind has value. If watching your ESPP balance every day stresses you out, that stress costs you something. Maybe it's worth $500 to not worry.

Immediate financial needs always win. Need money for a medical bill? Down payment on a house? Paying off high-interest debt? Sell the shares. Tax optimization is a luxury problem. Real financial needs come first.

Market timing is impossible. Don't try to predict if the stock will go up or down. Focus on what you can control: your concentration risk and your tax situation.

When Your Tax Bracket Changes Everything

If you're in the 24% or 32% tax bracket, the difference between qualifying and disqualifying treatment is significant (9-17%). For every $10,000 in ESPP shares, that's $900 to $1,700.

If you're in the 12% bracket, the difference is much smaller (0-3% depending on your capital gains rate). For $10,000 in shares, you might save $0 to $300. Probably not worth holding for months.

Higher earners have more to gain from qualifying treatment. But they also have more to lose if the stock tanks.

The Gut Check Question

Ask yourself: "If this stock wasn't my employer's stock, would I buy $X worth of it today with my own money?"

If the answer is no, you shouldn't hold it just for tax treatment. You're essentially making a new investment decision every day you hold.

Red Flags That Mean "Sell Now"

Ignore tax treatment and sell immediately if:

- Employer stock is over 25% of your net worth

- You hear layoff rumors or see executive departures

- Your industry is in serious trouble

- You desperately need the cash

- You can't sleep because you're worried about the stock

No tax savings is worth financial ruin or constant anxiety.

Now that you know how to make this decision, let's create your personal action plan for managing ESPP sales going forward.

Your ESPP Sale Action Plan: Next Steps

Think of this action plan like a pre-flight checklist. Going through each item ensures a smooth journey with no surprises at tax time.

Do This Week

Action 1: Gather your documents. Find your most recent Form 3922 and all purchase confirmations. These show your purchase dates, offering dates, and discount amounts.

Action 2: Create your tracking spreadsheet. Make three columns: Purchase Date, Offering Date, and Qualifying Sale Date (purchase date plus 2 years). Fill it in for every ESPP purchase you own.

Action 3: Set calendar reminders. For each purchase, set a reminder 1 month before the qualifying sale date. This gives you time to decide whether to wait or sell now.

Do Before You Sell

Action 4: Calculate your concentration risk. Add up the value of all your employer stock (ESPP shares plus any RSUs or options). Divide by your total investment portfolio. If it's over 15%, you're taking on extra risk by having too many eggs in one basket.

Action 5: Run the tax numbers. Use the formulas from Section 5 to calculate your tax bill for both qualifying and disqualifying sales. See which makes more sense for your situation.

Action 6: Pick your strategy. Will you sell immediately at every purchase? Wait for qualifying treatment? Use a hybrid approach? Write it down so you're not making emotional decisions later.

Do Annually

Action 7: Review your holdings. Every December, look at all your ESPP shares. Make a plan for the year ahead.

Action 8: Organize for taxes. Keep all your Forms 3922, 1099-B, and sale confirmations in one folder. Your tax preparer (or tax software) will need them.

When to Get Professional Help

You can handle basic ESPP sales yourself. But get help from a CPA or tax advisor if you have:

- Multiple ESPP sales in one year (more than 3-4 transactions)

- Income over $200k (where tax brackets get tricky)

- A complex tax situation (self-employment income, rental properties, etc.)

- Any uncertainty about the tax treatment

Professional help costs $300-$800 for most people. It's worth it to avoid a $2,000 tax mistake.

You're Now Ahead of 90% of Employees

Most people with ESPPs never learn this stuff. They sell shares randomly and hope their broker handles the taxes correctly (spoiler: brokers often get it wrong).

You now understand qualifying vs disqualifying dispositions. You know how to calculate your taxes. You can make informed decisions about when to sell.

That knowledge is worth thousands of dollars over your career. Use it.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis