ESPP Lookback Provision: How It Boosts Your Discount (With Examples)

How the lookback feature can dramatically increase your ESPP discount

Published March 14, 2026 · Updated March 14, 2026

An ESPP lookback provision lets you buy company stock at a discount based on the lower price from either the start or end of the purchase period. This feature can significantly boost your gains, especially when your stock price rises. We'll show you exactly how it works with real dollar examples.

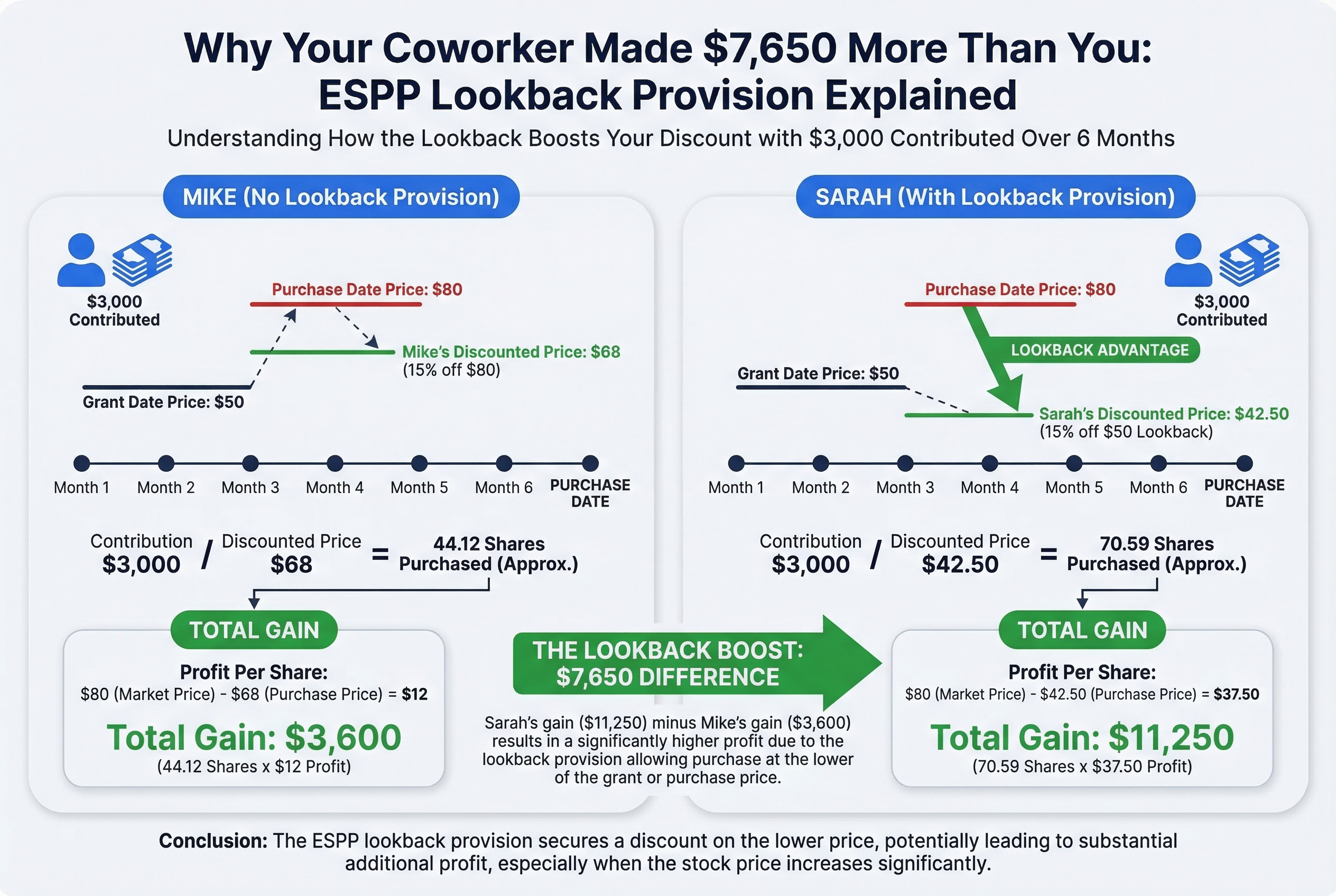

Why Your Coworker Made $3,000 More Than You on the Same ESPP

Sarah and Mike are software engineers at the same tech company. They earn the same salary. They both signed up for their company's ESPP and contribute $500 every month.

Six months later, Sarah made $11,250 when she sold her shares. Mike made $3,600.

Same company. Same contribution amount. Same purchase date. How did Sarah make $7,650 more than Mike?

The difference: Sarah's ESPP has a lookback provision. Mike's doesn't.

Here's what happened. When they enrolled, their company's stock traded at $50 per share. Six months later at purchase time, the stock had climbed to $80.

Mike's ESPP gave him the standard 15% discount off the $80 purchase price. He bought shares at $68 each. His profit: $12 per share when he sold at $80.

Sarah's ESPP looked back to the enrollment date. Her plan let her buy at 15% off the lower price between enrollment and purchase. That meant she bought at $42.50 (15% off the original $50). Her profit: $37.50 per share when she sold at $80.

With $3,000 contributed over six months, Mike bought about 44 shares. Sarah bought about 71 shares. When they sold, Mike pocketed $3,600. Sarah walked away with $11,250.

Think of the lookback provision like a time machine for your discount. It lets you lock in the best possible deal, even when the stock price has already taken off.

Most employees have no idea if their ESPP includes this feature. Let's fix that.

What Is an ESPP Lookback Provision? (The Simple Answer)

Think of a lookback provision as time travel shopping. You walk into a store on June 30th, but you get to pay whichever price is lower: today's price or the price from six months ago on January 1st. You automatically get the better deal.

That's exactly how an ESPP lookback provision works.

Here's the basic definition: A lookback provision lets you buy company stock at a discount from the LOWER of two prices. Those two prices are:

- The stock price on the offering date (when the purchase period starts)

- The stock price on the purchase date (when you actually buy)

This lookback feature works ON TOP OF your standard ESPP discount, which is usually 15%.

Here's a real example with actual dollars:

Your company stock is $100 on January 1 (offering date). By June 30 (purchase date), it has climbed to $130.

With a 15% discount AND lookback, you pay 15% off the LOWER price. That's 15% off $100, which equals $85 per share.

Without lookback, you'd pay 15% off the current price of $130, which is $110.50 per share.

The difference? You save an extra $25.50 per share. If you bought 100 shares, that's $2,550 in extra savings just from the lookback provision.

Important reality check: Not all ESPPs include this feature. Some plans only give you the 15% discount off the purchase date price. You need to check your specific plan documents to know if you have lookback.

Companies offer lookback provisions to make their ESPP more attractive. It's a retention tool. The better the benefit, the more likely you are to stay and participate.

The best part? This benefit is completely automatic. You don't have to do anything special to get it.

Now let's break down exactly how the lookback calculation works step by step.

What Should You Know Before Joining an ESPP?

How the Lookback Calculation Actually Works (Step by Step)

Think of the lookback provision like a price protection guarantee at Best Buy. If the price drops after you order something, they give you the lower price. But ESPP lookback works even better because it protects you if the price goes UP too.

Here's exactly how your company calculates what you pay for shares:

Step 1: Identify the Two Comparison Dates

Your company looks at two specific prices:

- The stock price on the offering date (the first day of your enrollment period)

- The stock price on the purchase date (the last day when shares actually get bought)

Step 2: Pick the Lower Price

The ESPP automatically selects whichever price is lower. This is the lookback magic. You get the better deal no matter which direction the stock moved.

Step 3: Apply Your Discount

Take that lower price and apply your discount (usually 15%). The formula: Lower price x 0.85 = Your purchase price

Step 4: Calculate Your Shares

Divide your total contributions by your purchase price. That's how many shares you get.

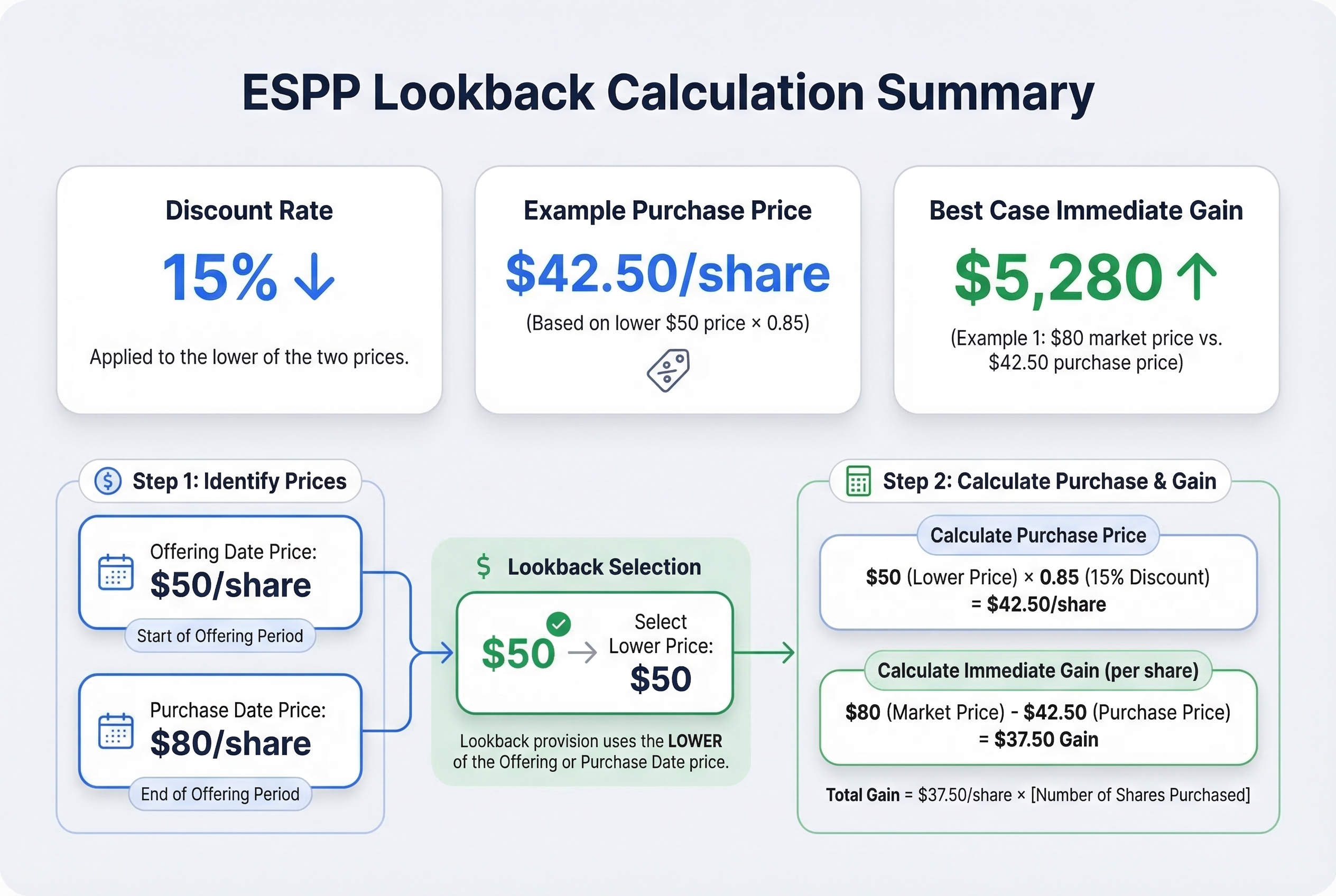

Example 1: When the Stock Goes Up (Best Case)

Your company's stock was $50/share on the offering date. Six months later on purchase date, it's $80/share.

- Lower price:

$50(offering date wins) - Your purchase price:

$50 x 0.85 = $42.50/share - You contributed:

$6,000total - Shares you buy:

$6,000 ÷ $42.50 = 141 shares - Market value:

141 shares x $80 = $11,280 - Your cost:

$6,000 - Immediate gain: $5,280

You just made $5,280 because the lookback let you buy at the old, lower price.

Example 2: When the Stock Goes Down

Same company, but now the stock falls. Offering date: $80/share. Purchase date: $50/share.

- Lower price:

$50(purchase date wins) - Your purchase price:

$50 x 0.85 = $42.50/share - You contributed:

$6,000total - Shares you buy:

141 shares - Market value:

141 shares x $50 = $7,050 - Your cost:

$6,000 - Immediate gain: $1,050

Even when the stock drops, you still profit. The 15% discount protects you.

The lookback provision means you win in both directions. But the real jackpot happens when stock prices climb during your enrollment period.

This UNLOCKs your ESPP

Lookback Provisions When Stock Prices Rise (Your Best-Case Scenario)

This is where lookback provisions really shine. When your company's stock price climbs during your offering period, you're getting what amounts to a discount on a discount.

Think of it like buying a concert ticket at last year's price when this year's price has doubled. You locked in the old price, but you can sell the ticket for today's higher value. That's exactly what lookback does for you.

The Math Gets Really Good

Let's look at three real scenarios to see how this plays out:

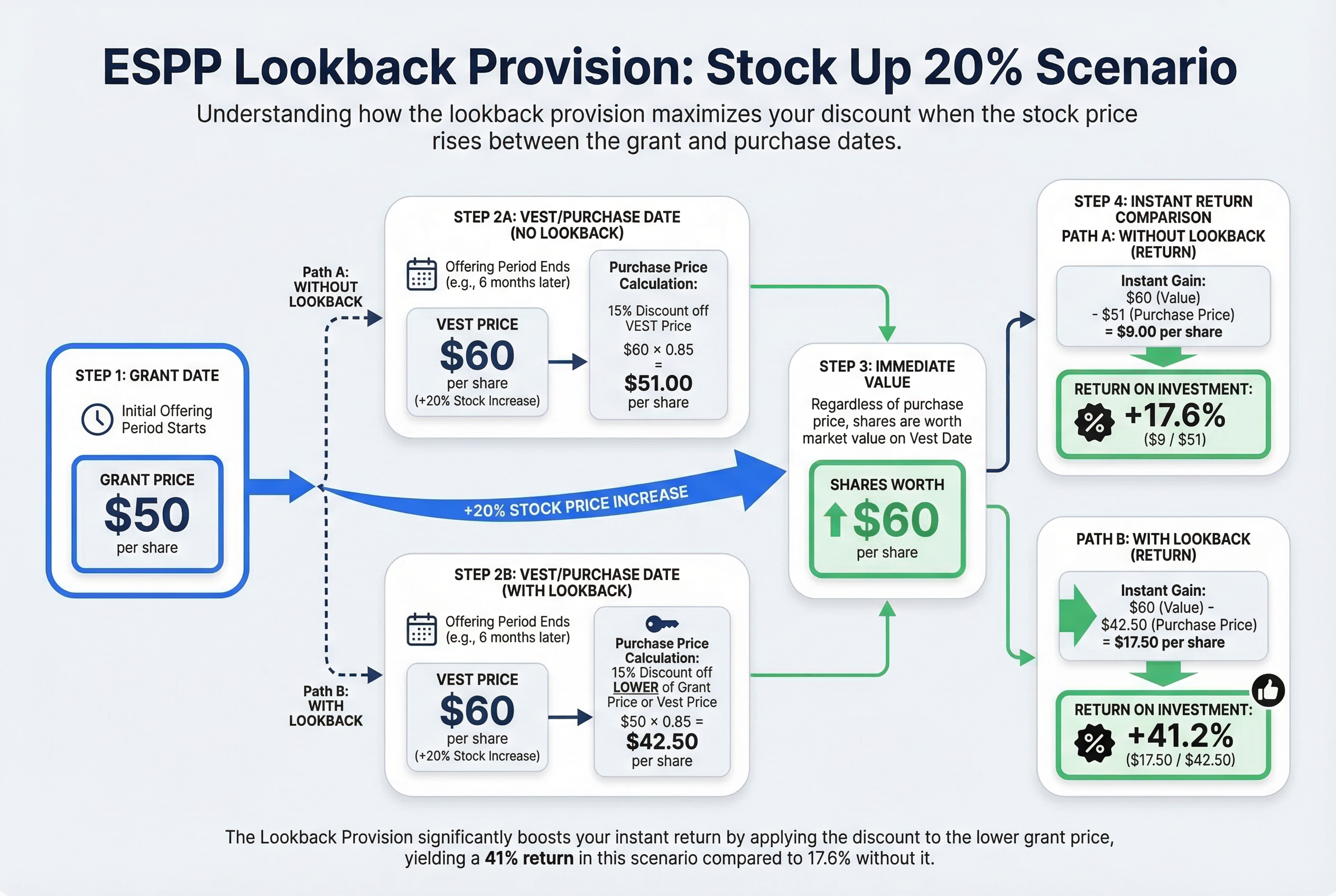

Modest Rise: Stock Up 20%

- Start of period: $50 per share

- End of period: $60 per share

- Without lookback: You pay $51 (15% off $60)

- With lookback: You pay $42.50 (15% off $50)

- Your shares are immediately worth: $60

- Your instant gain: $17.50 per share, or 41% return

Significant Rise: Stock Up 50%

- Start of period: $50 per share

- End of period: $75 per share

- Without lookback: You pay $63.75 (15% off $75)

- With lookback: You pay $42.50 (15% off $50)

- Your shares are immediately worth: $75

- Your instant gain: $32.50 per share, or 76% return

Dramatic Rise: Stock Up 100%

- Start of period: $40 per share

- End of period: $80 per share

- Without lookback: You pay $68 (15% off $80)

- With lookback: You pay $34 (15% off $40)

- Your shares are immediately worth: $80

- Your instant gain: $46 per share, or 135% return

Real Money Example

Say you contributed $10,000 in that last scenario. Here's what happens:

At $34 per share, your $10,000 buys you 294 shares. Those shares are immediately worth $23,529 (294 shares × $80). You just made $13,529 in profit. In six months. While still earning your regular salary.

This is why lookback provisions are so valuable. The bigger the price increase, the bigger your advantage. Your effective discount grows way beyond the stated 15%. In that 100% rise scenario, you're really getting a 57.5% discount off the current price.

The best part? This gain is locked in the moment you purchase. You don't have to hope the stock keeps rising. You already won.

But what happens when the stock price falls instead? That's where lookback proves it's still your friend.

Lookback Provisions When Stock Prices Fall (You Still Win)

Here's the surprising truth: even when your company's stock drops, you still make money with a lookback provision. It's like having a safety net that catches you before you hit the ground.

Think of the lookback as insurance. No matter what happens during the offering period, you're protected. The provision picks the lower of two prices (offering start or purchase date), then applies your 15% discount to that lower price. You still buy below market value.

The Math Still Works in Your Favor

Let's say your stock drops from $100 to $60 over six months. That's a brutal 40% decline.

Here's what happens:

- Offering start price: $100

- Purchase date price: $60

- Lookback selects: $60 (the lower price)

- Your purchase price: $60 x 0.85 = $51

- Immediate value: $60

- Your instant gain: $9 per share (17.6% return)

If you contributed $6,000 over those six months, you'd buy shares worth $7,059. You still made $1,059 in profit despite the stock tanking.

Real Examples at Different Decline Levels

Modest 10% drop ($100 to $90):

- You buy at: $76.50 (15% off $90)

- Immediate gain: $13.50 per share (17.6%)

Significant 30% drop ($100 to $70):

- You buy at: $59.50 (15% off $70)

- Immediate gain: $10.50 per share (17.6%)

Major 50% drop ($100 to $50):

- You buy at: $42.50 (15% off $50)

- Immediate gain: $7.50 per share (17.6%)

Notice the pattern? Your percentage gain stays the same (17.6%) because you're always buying at 15% below current market price.

When You Actually Lose Money

You only lose money if the stock falls after the purchase date. Using our example, if you buy at $51 and the stock drops to $45 the next week, you're down $6 per share.

Your breakeven point: The stock would need to fall below your purchase price ($51 in our example) for you to have a loss. As long as you sell at or above $51, you're profitable.

This is why many people sell immediately after purchase, even in falling markets. They lock in that guaranteed discount before the stock can drop further.

Now that you understand how lookback works in both rising and falling markets, you need to know the timing mechanics that make it all possible.

Offering Periods, Purchase Periods, and How Lookback Timing Works

Think of an ESPP like a subscription box service. You sign up for a membership period (the offering period), but you actually receive boxes at regular intervals during that membership (the purchase periods). The lookback provision always compares prices back to when you first signed up, not to when you got your last box.

The offering period is your overall enrollment window. It typically runs 6 to 27 months. When you enroll, the company records the stock price on that first day. This becomes your "offering date price," and it's locked in for the entire period.

Purchase periods are when you actually buy stock. These happen inside the offering period. Most companies have purchase periods every 6 months, but some do 3-month or 12-month intervals. On the last day of each purchase period (the "purchase date"), your accumulated paycheck contributions buy shares.

Here's where the lookback magic happens: the lookback always goes back to the offering date, not the previous purchase date. This is crucial.

A Real Example: The 24-Month Offering Period

Your company starts a 24-month offering period on January 1, 2024. Stock price: $50. The plan has four 6-month purchase periods.

First purchase (June 30, 2024): Stock is now $60. You buy at $42.50 (15% off the lower of $50 or $60).

Second purchase (December 31, 2024): Stock climbs to $70. You STILL buy at $42.50 (15% off the original $50). The lookback doesn't reset to the June price.

Third purchase (June 30, 2025): Stock hits $80. You STILL buy at $42.50. Same original lookback price.

Fourth purchase (December 31, 2025): Stock reaches $90. Final purchase at $42.50.

You bought shares at $42.50 four separate times while the actual stock price climbed from $50 to $90. That's a 52% discount on your last purchase ($42.50 vs $90).

What About Reset Provisions?

Some plans include a "reset" feature. If the stock price drops below the original offering date price during the enrollment period, the plan automatically starts a new offering period at the lower price. This protects you from being stuck with a high starting price. Not all plans have this, check your plan documents.

Now that you understand the timeline, what happens if you leave your job before a purchase date?

What Happens to Your ESPP Money If You Leave Before Purchase Date

Think of your ESPP contributions like money sitting in a savings account at a store. You've been setting cash aside to buy something at a big discount. But if you walk away before the sale happens, you get your cash back. You just miss out on the deal.

Here's what actually happens when you leave your job before the purchase date:

Your accumulated contributions come back to you in full. The company returns every dollar you've put in, usually in your final paycheck or shortly after. This money was always yours. You don't forfeit it.

But you lose the opportunity to buy shares at the discounted price. And if your plan has a lookback provision, this loss can be massive.

The Painful Math of Leaving Early

Let's say you've contributed $500 per month for 5 months. That's $2,500 total sitting in your ESPP account.

The stock price was $50 at the start of the offering period. Today it's at $80. Your purchase date is in 2 weeks.

You decide to resign now. Here's what happens:

What you get: Your $2,500 back.

What you miss: With a 15% discount and lookback, you would have purchased at $42.50 (85% of the $50 starting price). Your $2,500 would have bought about 59 shares worth $4,720. That's a $2,220 instant gain, gone.

If you'd waited just 2 more weeks, you could have resigned the day after the purchase date with that profit in hand.

It Doesn't Matter Why You're Leaving

The rules are the same whether you quit, get laid off, or are fired for cause. No purchase happens if you're not employed on the purchase date. It's all or nothing.

Some companies (very few) allow an immediate purchase when you terminate. Your plan documents will say if this applies to you. Most don't offer this.

When Timing Is Everything

Leaving 1 day before the purchase date costs you the entire discount and lookback advantage. Leaving 1 day after means you keep the shares you just bought at a discount.

The lookback provision makes this timing even more critical. In a rising market, you're not just losing a 15% discount. You're losing the chance to buy at a price that might be 30%, 40%, or even 50% below current value.

Bottom line: If you're planning to leave your company and a purchase date is coming up, consider your timing carefully. Those extra weeks could mean thousands of dollars in your pocket.

Next, let's make sure your ESPP actually has a lookback provision. Not all plans do, and knowing makes a big difference in your strategy.

Does Your ESPP Have a Lookback? How to Check Your Plan

You wouldn't buy a car without checking what features it has. Same goes for your ESPP. Here's how to find out if you've got the lookback feature.

Check Your Plan Documents (5-Minute Search)

Step 1: Log into your stock plan account (Fidelity, E*TRADE, Schwab, Morgan Stanley, etc.)

Step 2: Look for a section called "ESPP" or "Employee Stock Purchase Plan"

Step 3: Download these documents:

- Summary Plan Description (SPD)

- Plan Prospectus

- Employee Enrollment Guide

Step 4: Open the PDF and hit Ctrl+F (or Command+F on Mac). Search for these exact phrases:

lookbacklook-backlesser oflower ofoffering date

What the Language Actually Means

You HAVE a lookback if you see: "Purchase price is 85% of the lower of the fair market value on the offering date or purchase date."

That "lower of" phrase is your green light. It's like getting a rain check at the grocery store that locks in the sale price, even if the sale ended months ago.

You DON'T have a lookback if you see: "Purchase price is 85% of the fair market value on the purchase date" with no mention of the offering date.

Still Can't Tell? Ask Directly

If the documents are confusing (they often are), contact your HR benefits team. Here's an email template:

Subject: Question about ESPP lookback provision

Hi [HR contact],

I'm enrolled in our ESPP and want to confirm: Does our plan use a lookback provision? Specifically, is my purchase price based on the lower of the stock price at the start of the offering period OR the purchase date?

Thanks, [Your name]

One More Clue: Your Last Purchase Statement

Already made an ESPP purchase? Look at your confirmation statement. If the "purchase price" is lower than the stock price on the actual purchase date, you've got a lookback.

For example, say your statement shows you bought shares at $85 on June 30, but the stock was trading at $120 that day. That $85 came from applying the 15% discount to the $100 offering date price. That's lookback in action.

Now that you know if you have this feature, let's talk about what it means for your taxes.

Tax Treatment: How Lookback Provisions Affect Your Tax Bill

Here's the hard truth: the IRS wants a piece of your discount, not just your profit.

That amazing lookback benefit you got? The government considers it compensation income, just like your salary. You'll pay ordinary income tax on it, not the lower capital gains rate.

Think of it like a work bonus that comes in the form of stock instead of cash. The IRS taxes it the same way.

The Tax Bite on Your Lookback Discount

Let's see exactly what this means with real numbers.

You buy 100 shares at $42.50 using the lookback provision. The stock was $50 on the offering date and $80 on the purchase date. You sell immediately at $80.

Here's what happens on your taxes:

Your W-2 shows $3,750 in compensation income. That's the discount you received: $80 minus $42.50 equals $37.50 per share, times 100 shares.

You have $0 capital gain. You bought at $80 (the fair market value on purchase date) and sold at $80. No profit beyond the discount.

You owe about $900 in taxes if you're in the 24% tax bracket. That's 24% of your $3,750 discount.

Your net profit: $2,850. Still great, but not the full $3,750.

The bigger your lookback benefit, the bigger this tax bite. A 15% discount creates less taxable income than a 35% discount from lookback.

Qualifying vs Disqualifying Dispositions

The IRS gives you two paths, and they tax your shares differently.

Disqualifying disposition means you sell before meeting the holding requirements:

- You must hold 2 years from the offering date AND

- You must hold 1 year from the purchase date

If you sell before hitting both deadlines, it's disqualifying. Your employer reports the full discount as ordinary income on your W-2 that year.

Qualifying disposition means you hold long enough to meet both requirements.

Here's where it gets tricky. With a qualifying disposition, you still pay ordinary income tax on part of the discount. But it might be a smaller amount. The rest becomes long-term capital gain, which is taxed at a lower rate.

Let's use the same example. You bought 100 shares at $42.50 (with lookback) when the stock was $50 on offering date.

Disqualifying disposition (sell immediately at $80):

- Ordinary income: $3,750 (the full discount)

- Short-term capital gain: $0

- Tax at 24% bracket: about $900

Qualifying disposition (hold 2+ years, sell at $90):

- Ordinary income: $750 (the smaller of: actual discount OR 15% of offering date price)

- Long-term capital gain: $4,000 (the rest of your profit)

- Tax at 24% bracket + 15% long-term rate: about $780

The qualifying disposition might save you some tax. But you took on two years of risk holding the stock.

How Your Employer Reports This

Your company tracks everything and reports it to the IRS.

For a disqualifying disposition, the bargain element (your discount) shows up in Box 1 of your W-2 as wages. It's already included in your taxable income. You don't add it again when you file.

Your broker sends you Form 1099-B showing the stock sale. But the cost basis might look wrong. The broker often shows what you paid ($42.50 per share), not the fair market value on purchase date ($80 per share).

You need to adjust this on your tax return. Otherwise, you'll pay tax twice on the same discount.

For a qualifying disposition, you report the ordinary income portion on your Form 1040. Your company doesn't put it on your W-2 because you sold after the tax year ended.

A Simple Decision Tree

Ask yourself these questions:

- Can you afford the tax bill? If you sell immediately, you'll owe taxes on the discount by April 15.

- Do you want to hold company stock for 2+ years? That's a long time to have money tied up in one stock.

- Will the tax savings from qualifying treatment be worth the risk? Usually, the answer is no.

Most people choose the disqualifying disposition. They sell immediately, pay the higher tax rate, and take their guaranteed profit.

Important: This is complicated stuff. The lookback provision makes it even more complex because your discount is larger. Talk to a tax professional before making big decisions.

Now that you understand the tax impact, let's tackle the biggest question: should you sell your ESPP shares right away or hold them?

ESPP Taxation

Should You Sell ESPP Shares Immediately or Hold? (When You Have Lookback)

You just bought ESPP shares at a huge discount. Now comes the big question: do you sell right away and lock in your profit, or hold the shares for better tax treatment?

This is the classic "bird in hand versus two in the bush" decision. With a lookback provision, though, you often have a pretty fat bird already in your hand.

The Case for Selling Immediately

When you sell your ESPP shares right after purchase, you lock in a guaranteed profit. No waiting. No risk. No wondering if the stock will tank next month.

Here's what that looks like with real numbers:

You bought 200 shares at $42.50 (thanks to your lookback provision). The stock is trading at $80 today. You sell immediately.

- Your profit: $37.50 per share

- Total gain: $7,500 in just 6 months

- Return on your money: roughly 88%

That's an incredible return for half a year. You'd struggle to find a savings account or bond that comes close.

Selling immediately also solves the concentration risk problem. Think of it like keeping all your eggs in one basket. If you already get your paycheck from this company, do you really want your savings tied up in the same company's stock? If the business hits trouble, you could lose your job AND watch your stock value crater at the same time.

The Case for Holding

If you hold your ESPP shares for at least two years from the offering date AND one year from the purchase date, you qualify for better tax treatment. This is called a "qualifying disposition."

The tax savings can be real. But here's where the math gets tricky.

Using the same example:

You bought at $42.50, stock is now $80. If you hold for 18 more months to hit the qualifying period, you might save around $600 in taxes (depending on your tax bracket).

But what if the stock drops during those 18 months? Let's say it falls to $60.

- Your loss in stock value: $20 per share x 200 shares = $4,000

- Your tax savings from holding: $600

- Net result: You're down $3,400 compared to selling immediately

The $600 tax savings doesn't justify the $4,000 risk for most people.

How to Decide What's Right for You

Ask yourself these questions:

1. How much company stock do you already own? If you have RSUs or other ESPP shares, you might already have too much concentration. Selling immediately makes more sense.

2. What's your risk tolerance? Can you stomach watching your $7,500 gain shrink if the stock drops? If that would keep you up at night, sell now.

3. How bullish are you on your company? If you genuinely believe the stock will keep climbing AND you don't have much company stock exposure, holding might work. But be honest with yourself. Most employees are overly optimistic about their own company's stock.

4. What are your financial goals? Need money for a down payment next year? Sell. Building long-term wealth and can afford the risk? Maybe hold a portion.

A Simple Decision Framework

Here's a quick way to think through this:

- High company stock concentration (more than 10-15% of your portfolio): Sell immediately

- Need the money soon (within 2 years): Sell immediately

- Low company stock concentration AND long time horizon AND bullish on company: Consider holding some or all

- Unsure about any of the above: Sell immediately (you can always buy the stock back later if you want exposure)

What Most Financial Advisors Recommend

Many financial advisors suggest selling ESPP shares immediately, especially when you have a lookback provision. Why? Because you've already won. You got your discount, you got your lookback bonus, and you have a guaranteed profit sitting there.

Holding means gambling that guaranteed profit on a single stock. That's speculation, not investing.

With lookback provisions, your immediate gains are often so substantial (30% to 50%+) that the tax benefits of holding pale in comparison to the risk you're taking.

The Middle Ground Approach

Can't decide? You don't have to pick all or nothing.

Sell 75% immediately and hold 25% for the tax benefits. This way you lock in most of your profit while keeping some upside potential. If the stock tanks, you protected most of your gain. If it soars, you still benefit.

Now that you know when to sell, there's one more timing issue to consider: what if you CAN'T sell right away?

Blackout Periods and Insider Trading: What If You Can't Sell After Purchase?

Here's a frustrating scenario: you just bought ESPP shares at a huge discount, the stock is up, and you're ready to lock in your profit. But your hands are tied. You can't sell.

Welcome to blackout periods.

What Are Blackout Periods?

Most public companies restrict when employees can trade company stock. These blackout periods typically happen around earnings announcements, usually four times a year.

Think of it like being locked out of your own house. You own the shares, but you can't touch them for weeks.

The problem? ESPP purchase dates don't care about blackout periods. Your shares might get purchased on July 15, right in the middle of a blackout that runs July 1 to July 25.

The Real Risk: Watching Your Profit Disappear

Let's see how this plays out with real numbers.

Your ESPP purchase date is July 15. Thanks to the lookback provision, you buy 150 shares at $42.50 each. The stock is trading at $80 today. You're sitting on a profit of $5,625 ($80 minus $42.50 = $37.50 per share × 150 shares).

You want to sell immediately. But you can't. Your company has an earnings blackout from July 1 to July 25.

On July 20, the company reports disappointing earnings. The stock drops hard. By July 26, when you can finally sell, the stock is at $55.

Your profit? Now just $1,875 ($55 minus $42.50 = $12.50 per share × 150 shares).

You still made money, but you lost $3,750 of gains because you were forced to hold during the blackout. That hurts.

This Changes Your Strategy

The "sell immediately" strategy works great when you can actually sell immediately. Blackout periods add real risk.

The stock can move a lot in two or three weeks. It can go up (great for you) or down (not so great). You're basically gambling with your profit during the blackout period.

What You Can Do

First, check your company's insider trading policy. Know exactly when blackout periods happen. Most companies publish a calendar.

Second, look at when your ESPP purchase dates fall. Do they land during typical blackout windows? If your purchase date is always mid-July and mid-January, and those are blackout months, you'll face this issue every single time.

Third, ask HR about 10b5-1 plans. These are pre-scheduled trading plans that let you sell during blackouts. You set up automatic sales in advance, before you have any inside information. Not all companies allow them for ESPP shares, but some do.

The Bottom Line

Blackout periods are a hidden risk that nobody talks about when they're selling you on the ESPP. You might plan to sell immediately, but the company might not let you.

Factor this into your decision about how much to contribute. If you know you'll be forced to hold shares for weeks after each purchase, you're taking on more stock price risk than you might want.

Now that you understand all the benefits and risks of your ESPP lookback provision, let's pull everything together into a clear action plan.

Your Action Plan: Making the Most of Your ESPP Lookback

You've learned how lookback provisions work. Now let's turn that knowledge into money in your pocket.

Think of this action plan like a recipe. You need the right ingredients (information), the right timing (deadlines), and the right steps (in order). Miss one step and you might miss out on thousands of dollars.

Your Quick Wins (Do These Today)

Step 1: Confirm your lookback provision

Log into your stock plan portal right now. Look for your plan document or summary. Search for "lookback" or "lower of." You learned how to do this in Section 8. If you can't find it, email your stock plan administrator. This takes 10 minutes.

Step 2: Find your next enrollment deadline

While you're logged in, write down the deadline for the next offering period. Put it in your phone calendar with an alert for one week before. Missing this deadline means waiting 6 months for the next chance.

Your Weekly Action Checklist

Step 3: Calculate your contribution amount (this week)

Pull up your last pay stub. Calculate 10% and 15% of your take-home pay.

Example: You earn $6,000 per month after taxes. 10% equals $600 per month. 15% equals $900 per month.

Ask yourself: Can I live without this money for 6 months? Will it affect my emergency fund? Start with a comfortable amount. You can always increase it next offering period.

Step 4: Review your budget (this week)

If you contribute $600 per month, that's $3,600 over six months locked away. Make sure you have enough cash for rent, bills, and emergencies. The ESPP discount is great, but not if it forces you to rack up credit card debt.

Before Next Enrollment Deadline

Step 5: Enroll for your chosen amount

Go back to your stock plan portal. Select your contribution percentage. Most people start with 10% to 15% of pay. You can change this each offering period, so don't stress about getting it perfect.

Step 6: Set up your brokerage account

Your company will tell you which brokerage holds your ESPP shares. Create your login credentials now. You'll need this access on purchase date to see your shares and execute your sell strategy.

Step 7: Mark all important dates

Add these to your calendar:

- Offering period start date

- Purchase date (usually 6 months later)

- Next enrollment deadline

Set alerts for one week before each date.

One Week Before Purchase Date

Step 8: Check the blackout period calendar

Log into your company's insider trading policy portal or ask HR. If purchase date falls during a blackout period and you can't sell immediately, you learned your options in Section 11. You might need to hold shares longer than planned.

Step 9: Decide your sell strategy

Before purchase date arrives, decide: Will you sell immediately or hold?

If you're selling immediately, make sure you're not in a blackout period. Have your brokerage login ready. Know how to place a sell order.

If you're holding, review the tax implications from Section 9. Understand that you're taking on market risk.

On Purchase Date

Step 10: Review your account

Log into your brokerage account. You'll see your new shares and the purchase price. Check that the lookback provision applied correctly.

Example: Stock started the offering period at $100 and ended at $120. With a 15% discount and lookback, you should see a purchase price of $85 ($100 minus 15%).

Calculate your instant gain: If you bought 100 shares at $85 and current price is $120, you're up $3,500 before taxes.

Decision Day (Immediate or Within Days)

Step 11: Execute your sell strategy

If selling immediately: Place your sell order. The proceeds will hit your account in 2-3 business days.

If holding: Move on to Step 12.

After Your First Purchase

Step 12: Evaluate and adjust

How did it feel to have that money locked up for 6 months? Was it stressful or easy?

Did you sell immediately or hold? If you held, are you comfortable watching the stock price move?

Use these answers to adjust your contribution for the next offering period. Maybe you go from 10% to 15%. Maybe you drop to 5% because you need more cash flow.

Important Reminders

Review every offering period: Your financial situation changes. Your company's stock price changes. Re-evaluate your ESPP participation every 6 months.

Tax withholding: Your company might not withhold enough taxes on ESPP purchases. Set aside 25% to 35% of your gains for tax time. Talk to a tax professional about your specific situation.

This isn't financial advice: Your situation is unique. Consider talking to a financial advisor or tax professional about your specific circumstances. They can help you make decisions based on your complete financial picture.

The Bottom Line

The lookback provision is like a loyalty bonus that rewards you automatically. But you only get it if you enroll.

Start with a contribution amount that won't stress your budget. Mark your deadlines. Make a sell decision before purchase date. Then repeat every offering period.

Thousands of employees miss out on this benefit simply because they never take the first step. Don't be one of them.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis