How Much Should You Contribute to Your ESPP? A Complete Guide

Find your ideal contribution amount based on your financial situation

Published March 14, 2026 · Updated March 14, 2026

Your ESPP offers guaranteed discounts on company stock, but figuring out how much to contribute requires looking at your whole financial picture. This guide walks you through a simple decision framework with real dollar examples so you can choose the right contribution amount for your situation.

The ESPP Contribution Dilemma: Sarah's Story

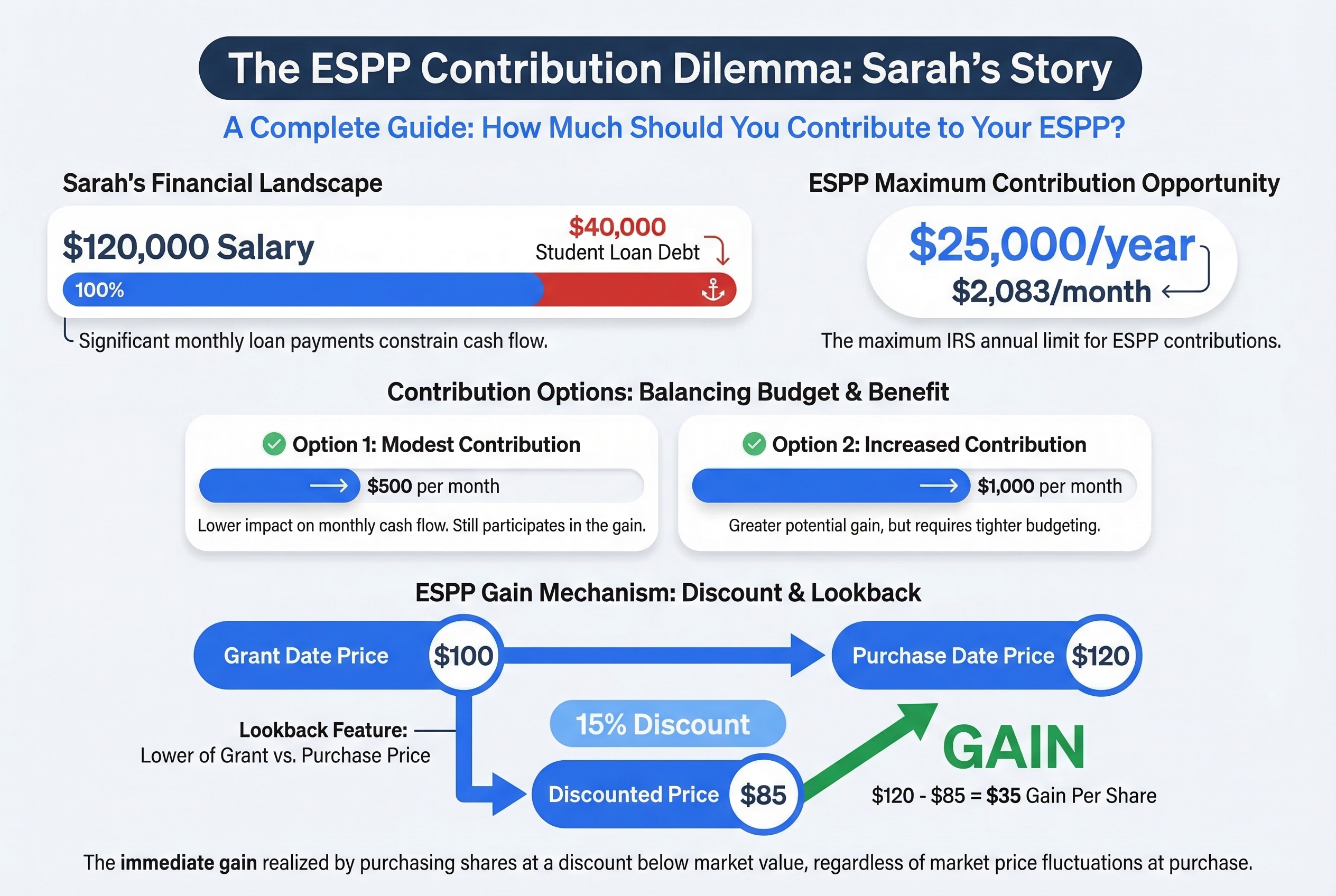

Sarah just got the email she'd been waiting for. After six months at her tech company, she finally qualifies for the Employee Stock Purchase Plan (ESPP). The offer sounds amazing: buy company stock at a 15% discount, up to $25,000 per year.

But then she opens the enrollment form and freezes.

Sarah earns $120,000 as a software engineer. Contributing the full $25,000 means $2,083 comes out of her paycheck every month. That's more than her rent. She has $40,000 in student loans. She's trying to save for a house down payment. And honestly, she's nervous about tying so much money to one company, especially after watching her dad lose his savings when his employer's stock crashed in 2008.

Maybe she should start with just $500 per month? Or $1,000? How do other people decide this?

If you're reading this, you're probably asking the same questions. The ESPP contribution decision feels like a high-stakes guess. Contribute too little and you leave free money on the table. Contribute too much and you might squeeze your budget or take on too much risk.

Here's the good news: this isn't actually a guessing game. By the end of this guide, you'll have a clear framework for choosing your contribution amount. One that fits your specific financial situation, not just a one-size-fits-all rule.

First, let's make sure we're all speaking the same language about how ESPPs actually work.

Sarah's dilemma: Maxing out the $25,000 annual ESPP contribution ($2,083/month) versus her existing financial obligations.

Sarah's dilemma: Maxing out the $25,000 annual ESPP contribution ($2,083/month) versus her existing financial obligations.

ESPP Basics: How the Discount Machine Works

Think of your ESPP as a six-month shopping window where you buy company stock at a guaranteed discount. Here's how the machine works.

The Shopping Window (Offering Period)

Your ESPP runs in cycles called offering periods. Most companies use six-month windows, though some run three or twelve months. During this period, money automatically comes out of your paycheck (after taxes are taken out). This cash sits in a holding account, waiting for purchase day.

Let's say your offering period runs from January 1 to June 30. Every two weeks, $200 gets deducted from your paycheck. By June 30, you've saved $2,600.

Checkout Day (Purchase Date)

On the last day of the offering period, all that saved-up money converts to company stock. But here's the magic: you don't pay full price. Your company gives you a discount, typically 5% to 15%. Most companies offer 15%.

Your Instant Discount

With a 15% discount, you pay $42.50 for a share that everyone else pays $50 for. That's an immediate $7.50 gain per share, or a 17.6% return the moment you buy.

Using our example: Your $2,600 buys stock at $42.50/share. You get 61 shares worth $3,050. You just made $450 instantly.

The Time Machine Discount (Lookback Provision)

Many ESPPs include a lookback feature. This is like a "best price guarantee" that compares two prices: the stock price on day one of the offering period and the price on purchase day. You get the 15% discount off whichever price is lower.

Here's where it gets exciting. Say your stock was $40 on January 1 but climbed to $50 by June 30. The lookback lets you buy at $34 (15% off the lower $40 price), not $42.50. Your $2,600 now buys 76 shares worth $3,800. That's a $1,200 gain, or a 46% return in six months.

Even if the stock drops from $50 to $40, you still win. You'd pay $34 (15% off $40), getting shares worth $40 each.

The Bottom Line

The discount alone guarantees a return. The lookback provision can turn that return into something spectacular. But before you max out your contributions, you need to know if you're financially ready to use this discount machine.

What Should You Know Before Joining an ESPP?

The Financial Prerequisites: When NOT to Contribute

Think of your finances like the airplane safety demonstration. You need to put on your own oxygen mask before helping others. Some financial foundations matter more than even a guaranteed 15% ESPP discount.

Emergency Fund Comes First

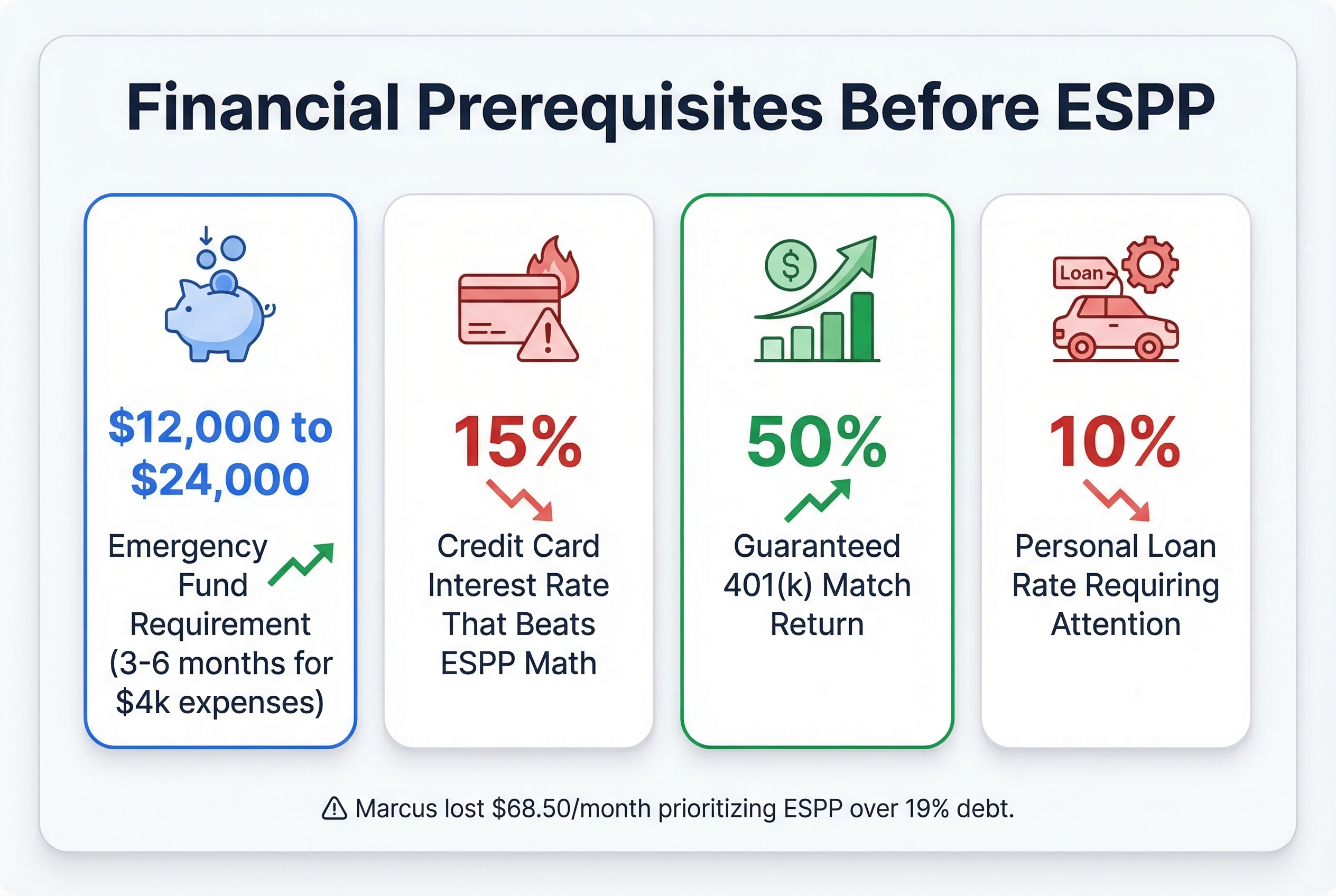

Before contributing to ESPP, you need 3-6 months of expenses in a savings account. Here's why: if you lose your job, you lose both your paycheck AND your ESPP contributions for that period. You're doubly exposed.

If your monthly expenses are $4,000, you need $12,000 to $24,000 saved first. No emergency fund? Skip ESPP for now and build that cushion. This isn't forever, just 6-12 months while you get stable.

High-Interest Debt Kills Your Returns

Credit card debt above 15% interest beats ESPP math every time. Here's the real-world calculation:

Marcus has $8,000 in credit card debt at 19% interest. That costs him $127/month in interest charges alone. His ESPP offers a 15% discount, but after paying 22% in taxes, his actual gain is 11.7%.

If Marcus puts $500/month into ESPP instead of debt payoff:

- He gains $58.50/month from the ESPP discount (11.7% of $500)

- He loses $127/month to credit card interest

- Net result: He's $68.50 worse off each month

Marcus should attack that credit card first. In 6 months, the debt is gone and he can start ESPP contributions with a clean slate.

Capture Your 401(k) Match

If your company matches 401(k) contributions, max that out before ESPP. A 50% match on 6% of salary is a guaranteed 50% return. No ESPP discount beats that.

Example: You earn $80,000. Contributing 6% ($4,800/year) gets you $2,400 free from the match. That's a $2,400 guaranteed gain versus maybe $702 from ESPP (15% discount on $4,800). The 401(k) wins by $1,698.

Personal Loans Above 10% Need Attention

Car loans or personal loans charging more than 10% interest should typically be paid down first. Run the math: compare your loan's interest rate to your after-tax ESPP discount.

Your after-tax ESPP discount = (Discount percentage) × (1 - Your tax rate)

If that number is lower than your loan rate, pay the loan first.

This Is Temporary

Here's the good news: this waiting period doesn't last forever. Once you've handled high-interest debt and built your emergency fund, ESPP becomes a powerful wealth-building tool. You're not missing out, you're sequencing smart.

Now let's figure out exactly how much you should contribute once these foundations are in place.

Prioritizing financial health: The required emergency fund range ($12k-$24k for $4k expenses) outweighs the immediate ESPP discount.

Prioritizing financial health: The required emergency fund range ($12k-$24k for $4k expenses) outweighs the immediate ESPP discount.

Your ESPP Contribution Sweet Spot: The Decision Framework

Think of your first ESPP contribution like test-driving a car. You don't commit to the most expensive model right away. You start with something manageable, see how it feels, and adjust from there.

Here's your step-by-step process for finding your perfect contribution amount.

Step 1: Know Your Monthly Take-Home

Calculate what hits your bank account each month after taxes, 401(k), and health insurance. This is your real spending power.

If you're paid bi-weekly, multiply one paycheck by 2.17 to get your monthly average. Don't use your gross salary for this calculation.

Step 2: Add Up Your Fixed Expenses

List everything you must pay each month:

- Rent or mortgage

- Car payment and insurance

- Utilities and phone

- Minimum debt payments

- Groceries and gas

Be honest. Use your actual spending from the last 3 months, not what you wish you spent.

Step 3: Find Your Discretionary Income

Subtract your fixed expenses from your take-home pay. What's left is your discretionary income. This is money for dining out, entertainment, savings, and yes, your ESPP.

Your ESPP contribution should come from this bucket, not your fixed expense money.

Step 4: Start with 5% of Take-Home

For your first ESPP enrollment period, contribute 5% of your monthly take-home pay. This gives you a meaningful discount without straining your budget.

Calculate it: Monthly take-home × 0.05 = First ESPP contribution

Step 5: Live with It for One Full Period

Go through an entire purchase period (usually 6 months) at this level. Pay attention to how it feels. Are you stressed about money? Or did you barely notice the deduction?

Step 6: Adjust Based on Comfort

After your first ESPP purchase, evaluate:

- Did you miss the money?

- Did you have to dip into savings?

- Could you handle more?

If you felt comfortable, increase by 2-3% of take-home for the next period. If it felt tight, stay at 5% or drop to 3%.

The Real-World Example

Jennifer takes home $5,500 per month after taxes and her 401(k) contribution. Her fixed expenses total $4,200, leaving $1,300 in discretionary income.

For her first ESPP period, she starts with $275 per month. That's 5% of her take-home and 21% of her discretionary budget.

After 6 months, she gets her first ESPP purchase. The process felt easy, and she didn't miss the money. She increases to $440 per month (8% of take-home).

A year later, Jennifer settles at $550 per month. That's 10% of her take-home, and it feels sustainable. She's not sacrificing her lifestyle, and she's building a nice discount on company stock.

The Beginner's Rule of Thumb

Don't exceed 10-15% of take-home pay until you've completed at least two full ESPP periods. This protects you from overcommitting before you understand how the program works.

Remember: You can always increase your contribution. It's much harder to decrease mid-period without losing money.

One More Critical Check

Add up all your company stock. Include:

- Vested RSUs you haven't sold

- Unvested RSUs

- Stock from previous ESPP purchases

- Your planned ESPP contributions

If this total exceeds 15-20% of your net worth, pump the brakes. You're getting too concentrated in one company, even if the ESPP discount looks tempting.

Now that you know your personal contribution sweet spot, let's explore when it makes sense to contribute more than the baseline.

How Much Money Should You Contribute To Your ESPP?

Maximizing Your Discount: When to Contribute More

If you've checked all the boxes (emergency fund, no high-interest debt, retirement on track), it's time to think bigger. Contributing the maximum to your ESPP is like finding a coupon that gives you 15% off everything. You'd use that coupon as much as possible, right?

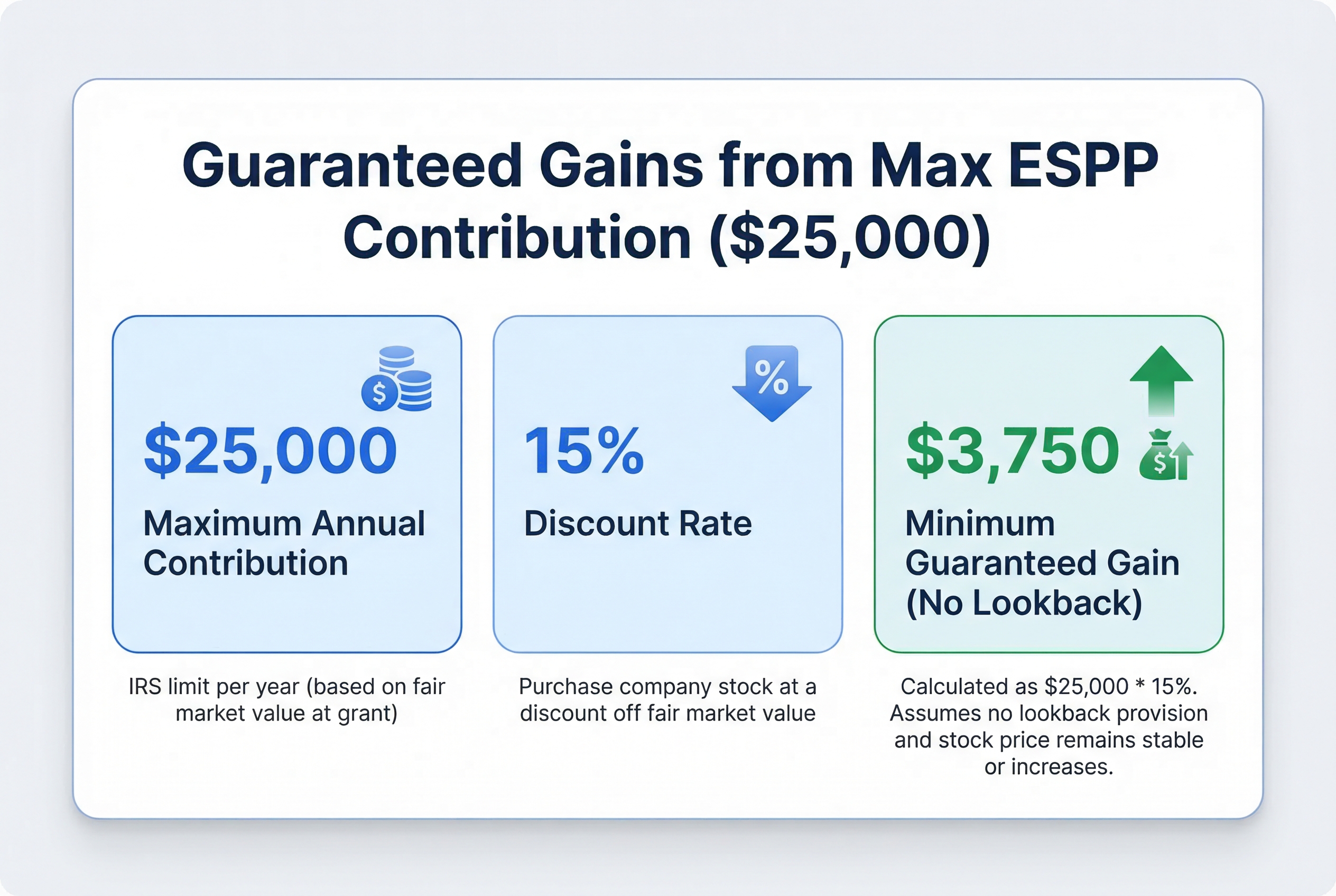

The maximum contribution is $25,000 per year. That's $2,083 per month. Many companies cap it lower, usually at 10-15% of your salary. Check your plan rules to see your actual limit.

The Math on Maximum Contributions

Let's say you contribute the full $25,000 over a year. With a 15% discount and no lookback, you're guaranteed to capture at least $3,750 in gains. That's free money for filling out an enrollment form.

With a lookback provision, your gains jump higher. The stock price usually moves up or down during the offering period. When it goes up, you buy at the lower starting price. Your annual gains often hit $6,000 to $11,750 instead.

Think of it this way: you're getting a 15-47% return on money that's only tied up for 6 months. No other investment offers that guarantee.

Who Should Max Out Their ESPP

David's situation shows when maxing out makes sense. He earns $180,000 with $10,500 in monthly take-home pay. He has no debt, 8 months of emergency savings, and already maxes his 401(k).

His company ESPP has a 15% discount with lookback. He contributes the maximum $2,083 per month. Every 6 months, he captures at least $1,875 in discount. With the lookback feature, he often makes $3,000 or more per purchase.

Over a year, David makes $6,000 to $8,000 in guaranteed gains. That's like getting a 4-5% raise for doing nothing. He sells shares immediately after each purchase to lock in the discount.

The Profile for Maximum Contributions

You're a good candidate for maxing out if you:

- Earn enough that $2,083/month (or your plan's limit) doesn't strain your budget

- Have 6+ months of emergency savings

- Carry no high-interest debt

- Already contribute enough to get full 401(k) match

- Can handle seeing a big chunk leave each paycheck

The key question: Can you afford to have this money tied up for 6 months? If yes, contribute as much as your plan allows.

The Immediate Sale Strategy

Contributing the maximum works best when you sell shares right after purchase. You capture the discount without betting on your company's future stock price.

This matters even more if you already have RSUs. Those shares already give you plenty of exposure to your company's success. Your ESPP should be about harvesting the discount, not doubling down on company stock.

One warning about concentration risk: If your total compensation is heavily weighted toward company stock (salary + bonus + RSUs + ESPP), you need to be extra careful. We'll dig into this critical issue next.

Employee Stock Purchase Plans Explained: How to Maximize Your ESPP and Build Flexibility

The guaranteed minimum return: $3,750 in gains from a full $25,000 contribution with a 15% discount.

The guaranteed minimum return: $3,750 in gains from a full $25,000 contribution with a 15% discount.

The Concentration Risk Nobody Talks About

Here's something most ESPP guides won't tell you: your paycheck already ties your financial life to your company. Adding more company stock on top creates a dangerous double risk.

Think of it like this: you're already betting on your company every two weeks when you show up for work. Your salary, health insurance, and career growth all depend on the company doing well. Piling more company stock into your portfolio is like doubling down on that same bet.

Your Company Exposure Is Bigger Than You Think

Most people only count their ESPP shares. But you need to add up everything:

- RSUs that have vested (current value)

- ESPP shares you're holding (current value)

- Stock options that are in the money

- Your salary dependency (yes, this counts)

Then divide by your total net worth. The result might shock you.

Real example: Priya has $80,000 in net worth: $30,000 in her 401(k), $15,000 emergency fund, $25,000 in RSUs vesting this year, and $10,000 in ESPP shares from previous purchases. Her company stock is $35,000 of her $80,000. That's 44% of her net worth in one company.

If her company hits trouble, Priya faces a nightmare scenario. She could lose her job while watching 44% of her wealth evaporate. Her income disappears at the exact moment her savings crater.

The Enron Warning

Remember Enron? Employees lost their jobs and their retirement savings simultaneously. They had loaded up on company stock, thinking it was safe because they "knew" the company. When Enron collapsed in 2001, workers lost everything at once.

You don't need a fraud scandal for this to hurt you. Even good companies hit rough patches. Tech layoffs in 2022-2023 happened while stock prices dropped 40-60%. Employees got hit twice.

What's a Safe Amount?

Most financial advisors say no single stock should exceed 10-15% of your investment portfolio. Some stretch this to 20% if you're young and have time to recover.

Quick check: Calculate your company exposure right now:

(RSU value + ESPP shares + options) ÷ total net worth = your %

If you're above 20%, you're in the danger zone. Above 30%? You need to act fast.

Why This Matters for Your ESPP

Here's the key insight: your ESPP should be a discount capture tool, not an investment strategy.

The safest approach? Contribute to your ESPP, grab the discount, then sell immediately. You pocket the 15% gain without adding concentration risk. The discount is your reward. Holding the shares hoping they'll go up is speculation.

If you already have RSUs (and most tech workers do), this becomes even more critical. Those RSUs already give you plenty of company exposure. Your ESPP contributions should focus on capturing the discount, not building a bigger position.

Priya's fix: She should sell her ESPP shares right after each purchase period. That $10,000 goes into her 401(k) or a diversified brokerage account. When her $25,000 in RSUs vest, she should sell at least half. These moves would drop her company exposure from 44% to around 15%, a much safer level.

The Math on Double Risk

Your company stock can hurt you in ways other investments can't. If Apple stock drops, it doesn't affect your job at Microsoft. But if your own company stock drops, you might be facing layoffs at the same time.

This "correlation risk" means company stock is riskier than the same amount in any other single stock. You need to count it as extra risky when planning your portfolio.

Now that you understand concentration risk, what happens if you need to leave your company mid-year? The next section covers the tricky timing of ESPP when you exit.

What Happens When You Leave: The Mid-Period Exit

Leaving your job mid-ESPP period feels like abandoning a layaway plan at the store. You've been putting money aside, but you haven't actually bought anything yet. Here's exactly what happens to your money and shares.

If You Leave Before the Purchase Date

Your contributions sit in a holding account, like money in escrow. When you leave, the company returns this money to you, usually within 30 to 60 days.

Here's the catch: You get back exactly what you put in. No interest. No discount. Just your original contributions.

Let's look at Tom's situation:

- He contributes $500 per month to his ESPP

- Four months into a 6-month offering period, he accepts a new job

- He has contributed $2,000 so far

- His company returns his $2,000 within 45 days (no interest, no discount)

- He misses out on the $300 discount he would have earned by staying 2 more months

The timing matters hugely. If Tom had left just 2 weeks AFTER the purchase date, he would have received shares worth $2,300 (with his 15% discount) and could sell them immediately at his new job.

If You Leave After Purchase

You keep all shares you already own. They're yours, period.

Most companies let you sell these shares right away, even if you just left. You don't lose access to your brokerage account. The shares simply transfer to a personal account.

Important: Some plans let you stay enrolled through your current offering period even after giving notice. Check your plan document. This could mean finishing out that 6-month period and getting your discount before you leave.

The Holding Period Continues

If you're aiming for a qualifying disposition (lower taxes), the holding period clock keeps ticking after you leave.

You bought shares on March 1st. You need to hold them until March 2nd two years later. Leaving your job in June doesn't reset this clock. The dates stay the same.

Three Exit Scenarios

Scenario 1: Leave Before Purchase

- You get: Your contributions back (no interest)

- You lose: The discount on that period's purchase

- Timeline: Refund in 30 to 60 days

Scenario 2: Leave Right After Purchase

- You get: Your shares with full discount

- You can: Sell immediately if needed

- You keep: Access through your brokerage

Scenario 3: Leave During Holding Period

- You keep: All purchased shares

- Your holding period: Continues unchanged

- Tax treatment: Still based on how long YOU hold shares

Action Steps for Each Scenario

If you're leaving before purchase date:

- Check if you can stay enrolled through current period

- Calculate whether waiting for purchase date is worth it

- Request refund confirmation in writing

- Watch for refund within 60 days

If you're leaving after purchase:

- Log into your brokerage account

- Note your purchase dates for tax planning

- Decide whether to sell now or hold

- Keep all purchase confirmations for tax time

Your Plan's Specific Rules

Company policies vary. Most return contributions within 30 to 60 days, but some take longer. Some let you finish the current offering period, others cut you off immediately.

Where to find your rules: Look for your Summary Plan Description (SPD) in your benefits portal. Search for "termination of employment" or "leaving the company." If you can't find it, email HR before you give notice.

The bottom line: Your money isn't lost. Contributions come back (just without the discount). Shares stay yours. The main risk is timing, leaving a week before purchase date instead of a week after can cost you hundreds or thousands in lost discount.

Now that you understand what happens when you leave, let's tackle the tax side of ESPP contributions, because keeping more of your discount matters just as much as earning it.

Tax Impact: Keeping More of Your Discount

Your ESPP discount looks great on paper. But the IRS wants their cut. Understanding the tax rules helps you keep more of what you earn.

Think of ESPP taxes like a "patience bonus" at work. Hold your shares longer, and you might get a tax break. But that bonus comes with a big catch: your stock could drop while you wait.

The Two Tax Paths

Disqualifying Disposition (Sell Fast)

You trigger a disqualifying disposition when you sell before meeting both holding requirements:

- 2 years from the offering date (when the purchase period started)

- 1 year from the purchase date (when you actually bought shares)

Sell before hitting both dates? Your discount gets taxed as ordinary income, just like your salary. Any additional gains get taxed as short-term capital gains (also ordinary income rates if you held less than a year).

Qualifying Disposition (Hold Long)

Meet both holding periods and you unlock the patience bonus. Part of your discount converts to long-term capital gains, which get taxed at lower rates (0%, 15%, or 20% depending on your income).

Sounds great, right? Here's the problem: you're betting your company stock won't drop for two years.

The Real Numbers

Let's look at Aisha's situation. She buys $10,000 of company stock through her ESPP at a 15% discount. She pays $8,500 and immediately owns shares worth $10,000. Her discount: $1,500.

Scenario 1: Sell Immediately

Aisha sells right away for $10,000. The $1,500 discount gets taxed as ordinary income at her 24% tax rate. She pays $360 in taxes.

Her after-tax gain: $1,140

That's an 11.4% return on her $10,000 investment in six months. Guaranteed.

Scenario 2: Hold for Qualifying Disposition

Aisha holds for two years, hoping to save on taxes. If the stock stays flat at $10,000, she converts some discount to long-term capital gains (taxed at 15% instead of 24%). She saves roughly $135 in taxes.

Her after-tax gain: $1,275

But what if the stock drops 10% to $9,000? She loses $1,000 of value. Even with the $135 tax savings, she's down $865 total. The patience bonus cost her money.

After-Tax Return: The Only Number That Matters

Here's the simple formula:

After-tax return = (Sale price - Purchase price - Taxes) / Purchase price

For Aisha's immediate sale:

($10,000 - $8,500 - $360) / $8,500 = 13.4%

For her two-year hold at flat price:

($10,000 - $8,500 - $225) / $8,500 = 15.0%

For her two-year hold with 10% drop:

($9,000 - $8,500 - $225) / $8,500 = 3.2%

The immediate sale captures most of the benefit without the risk.

Should You Ever Hold?

Most financial advisors recommend selling immediately. Here's why:

The math rarely works out. Your stock needs to stay flat or rise just to break even after tax savings. A 10% drop wipes out years of potential tax benefits.

You're already concentrated. You work there. Your salary depends on company performance. Why bet your ESPP gains too?

Guaranteed returns are rare. An 11% return in six months, locked in, beats hoping for a 2% tax savings two years later.

Simple Decision Tree

-

Do you believe your stock will rise 20%+ over two years? If yes, maybe hold. If no or unsure, sell now.

-

Can you afford to lose the discount if the stock drops? If no, sell now.

-

Do you already own company stock (RSUs, options)? If yes, sell now to reduce concentration.

For 95% of employees, "sell immediately" is the right answer.

Now that you understand the tax impact, let's look at the mistakes that cost employees thousands in ESPP gains.

Common Contribution Mistakes to Avoid

Think of these mistakes as potholes on your ESPP journey. You can avoid every single one if you know where to look.

Mistake 1: Maxing Out Without Testing Your Cash Flow

The error: You see the 15% discount and immediately contribute the maximum $25,000. Then you realize you're living paycheck to paycheck.

Real impact: Emma earns $120k and maxes out her ESPP at $2,083/month. Three months in, her car needs $2,000 in repairs. She has no emergency fund left and puts it on a credit card at 22% interest. The credit card interest eats up more than her ESPP discount.

The fix: Start at 5% of your salary for one purchase period. If your budget feels comfortable, increase to 10% next period. Work up to your target contribution slowly.

Mistake 2: Never Selling Your ESPP Shares

The error: You buy discounted shares every 6 months and hold them all. After 3 years, 40% of your net worth is in your employer's stock.

Real impact: Think of this like keeping your entire emergency fund in lottery tickets from the same gas station. If that station closes, you lose everything at once.

The fix: Sell most or all shares immediately after each purchase period. Your paycheck already depends on this company. Your investment portfolio shouldn't.

Mistake 3: Forgetting ESPP When Planning Big Purchases

The error: Carlos contributes $800/month to his ESPP and plans to buy a house in 8 months. He forgets this reduces his take-home by $800/month.

Real impact: When applying for a mortgage, his debt-to-income ratio is higher than expected because his take-home is lower. He either needs to reduce his mortgage amount or pause ESPP contributions for 6 months before applying.

The fix: When planning major purchases, account for ESPP contributions in your cash flow analysis 6 to 12 months ahead. Pause contributions if you need to show higher take-home income.

Mistake 4: Contributing While Carrying High-Interest Debt

The error: You contribute to ESPP while paying 20% interest on credit cards. You're earning 15% (maybe) while losing 20% guaranteed.

The fix: Pay off any debt above 7% interest before contributing to ESPP. The math is simple: guaranteed 20% loss beats potential 15% gain.

Mistake 5: Set It and Forget It

The error: You set your contribution rate 3 years ago. Since then, you got a 30% raise and had a baby. Your contribution rate hasn't changed.

The fix: Review your ESPP contribution every 6 months. Life changes fast. Your contribution should keep up.

Mistake 6: Chasing the Qualifying Disposition

The error: You hold ESPP shares for 2 years to get "better" tax treatment, even though your stock is volatile.

Real impact: Your 15% discount can disappear in a single bad earnings report. The tax savings from a qualifying disposition might save you 5%, but the stock could drop 30%.

The fix: For most people at most companies, sell immediately. The guaranteed 15% discount beats the potential tax savings.

Mistake 7: Ignoring Your Total Company Stock

The error: You contribute to ESPP, hold RSUs, and have 401k money in company stock. You think these are separate.

Real impact: Marcus has $50k in ESPP shares, $80k in unvested RSUs, and $30k of his 401k in company stock. That's $160k tied to one company. If the stock drops 40%, he loses $64k across all accounts.

The fix: Add up ALL your company stock exposure: ESPP shares, RSUs (vested and unvested), 401k company stock, and stock options. If the total exceeds 20% of your net worth, you have concentration risk.

Now that you know what to avoid, let's create your personal action plan to start using your ESPP effectively.

Your ESPP Action Plan: What to Do This Week

Think of this like a pilot's pre-flight checklist. You don't need to do everything at once, but you do need to do these steps in order.

This Week: The Essential Three

Action 1: Find Your Plan Details (15 minutes)

Log into your HR portal (Workday, ADP, Fidelity, E*TRADE, or wherever your benefits live). Search for "ESPP" or "Employee Stock Purchase Plan."

Download the plan document and write down three numbers:

- Discount percentage: Usually 15%

- Lookback provision: Yes or no

- Contribution limit: Usually 15% of pay or $25,000 per year

Can't find it? Email your HR benefits team. Use this exact subject line: "Request: ESPP Plan Document."

Action 2: Calculate Your Starting Amount (10 minutes)

Open your most recent paystub. Find your take-home pay after taxes and deductions.

Let's say you take home $5,000 per month. Multiply by 5%: $5,000 x 0.05 = $250 per month.

That's your starting contribution. It's small enough that you won't miss it, but big enough to build the habit.

Action 3: Enroll or Adjust (10 minutes)

Go back to your HR portal. Find the ESPP enrollment section. Enter your contribution as a percentage (probably 5%) or dollar amount ($250 per month).

Hit submit before the enrollment deadline. Most companies have enrollment windows at the start of each offering period (usually January 1 and July 1).

Before Your First Purchase Date: The Next Two

Action 4: Set Your Calendar Reminders

Create three calendar events:

- Purchase date (6 months from enrollment): Review how the contribution felt

- One week before purchase: Decide whether to sell immediately or hold

- Quarterly review: Check if you want to increase, decrease, or pause

Action 5: Pick Your Sell Strategy Now

Before you own a single share, decide: Will you sell at purchase or hold?

Write it down. Seriously. Studies show people who decide in advance make better decisions than people who decide in the moment.

If you're not sure, default to selling immediately. You can always change your mind later.

Next Enrollment Period: The Growth Step

Action 6: Review and Adjust (Quarterly)

Every three months, ask yourself:

- Did the contribution hurt my budget?

- Am I still debt-free with a 3-month emergency fund?

- Do I own too much company stock now (more than 10% of investments)?

If you answered yes, yes, and no, consider increasing your contribution by 2-3%.

If any answer is no, keep your contribution the same or decrease it.

Your Safety Net

Bookmark these resources on your phone right now:

- Your company's ESPP administrator website (Fidelity, E*TRADE, Morgan Stanley, etc.)

- Your HR benefits contact email

- This article (for when you forget the framework in 6 months)

You've got this. The hardest part is starting, and you're about to do that this week. Even a 5% contribution with a 15% discount puts you ahead of the 70% of employees who never enroll at all.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis