Year-End Tax Planning for Equity Compensation: Your Complete Guide

How to avoid surprise tax bills and make smarter decisions before December 31st

Published March 14, 2026 · Updated March 14, 2026

Year-end is when most equity compensation surprises happen - from RSU vesting you forgot about to ISO exercises that trigger unexpected AMT bills. This guide walks you through exactly what to review, when to act, and how to avoid the most common (and expensive) mistakes before the calendar flips.

Why December Decisions Can Make or Break Your Tax Bill

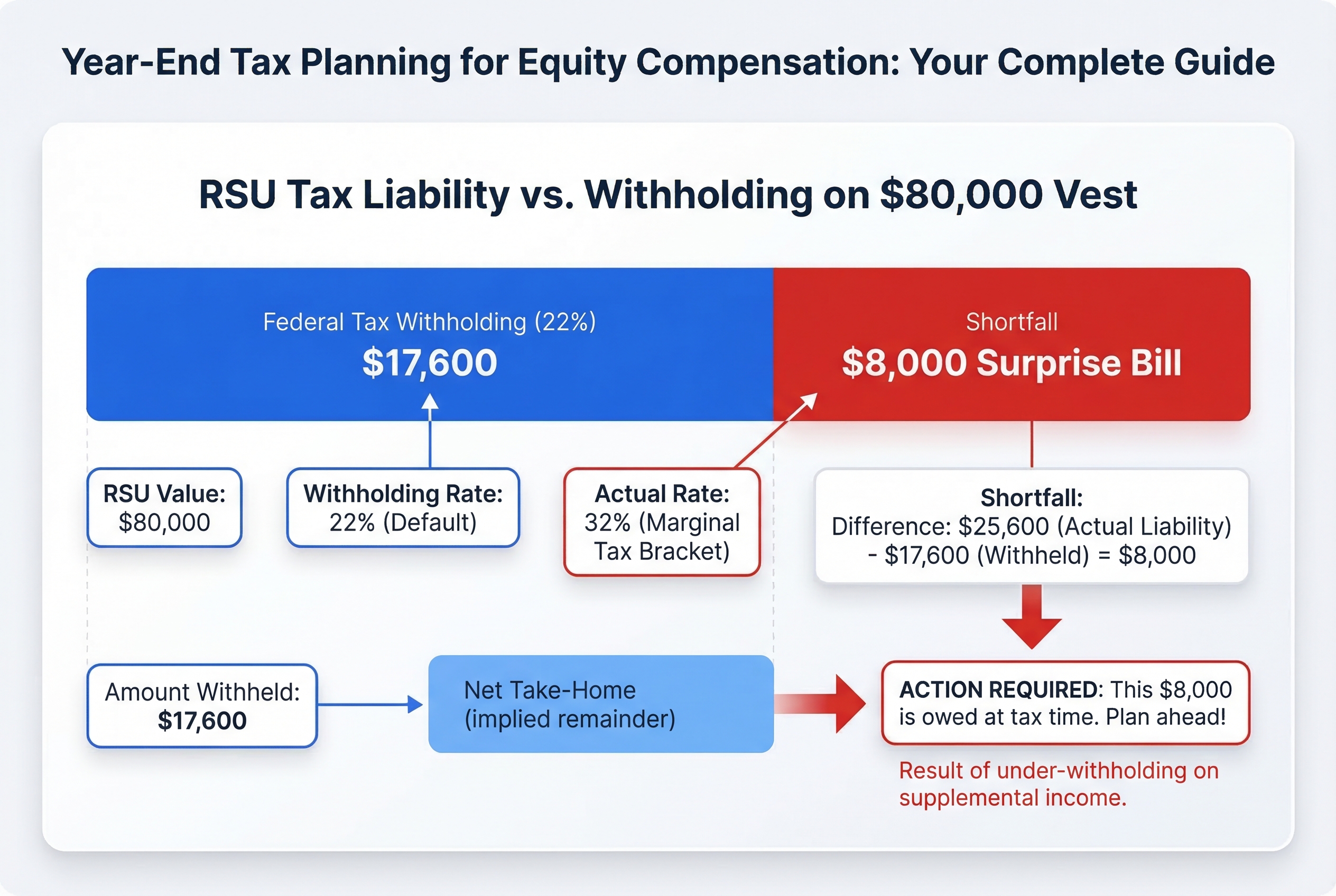

Sarah thought she had her finances figured out. She worked at a tech company, earned $140,000 a year, and watched 100 RSUs vest in March at $800 per share. That's $80,000 in stock compensation.

Her company automatically withheld 22% for taxes ($17,600) and sent the rest to her brokerage account. She sold the shares, paid off her car loan, and moved on with her life.

Then April arrived. Her tax software showed she owed an extra $8,000. Sarah's actual tax rate was 32%, not 22%. She hadn't saved the difference, and now she was scrambling to cover the bill.

Here's what Sarah didn't know: equity compensation is like a tax time bomb with a calendar. Certain dates trigger tax events whether you're ready or not. And once December 31st passes, you can't go back and fix them.

Most Equity Tax Events Run on Autopilot

Unlike your 401(k) contributions or HSA deposits, you don't control when most equity events happen:

- RSUs vest on predetermined dates set by your company

- ESPP purchases happen automatically each purchase period

- Stock sales create taxable gains the day they settle

- ISO exercises can trigger Alternative Minimum Tax in the same calendar year

The calendar doesn't care if you're ready. December 31st is the deadline, and there are no extensions.

The 22% Withholding Trap

When your company withholds taxes on RSUs or ESPP purchases, they typically use 22%. That's the IRS supplemental wage rate. But it's rarely your actual tax rate.

If you earn over $100,000, you're probably in the 24% or 32% bracket. Add state taxes (0% to 13% depending where you live), and the real number could be 35% to 45% total.

The math on Sarah's situation:

- RSU value: $80,000

- Withheld at 22%: $17,600

- Actual federal tax (32%): $25,600

- Surprise bill: $8,000

If she'd reviewed this in December, she could have adjusted her W-4 to withhold more from each paycheck. Or she could have set aside cash in a high-yield savings account. Small planning, big difference.

Small December Decisions, Thousands in Impact

You might think year-end tax planning is for millionaires with fancy accountants. But equity compensation makes it matter for regular employees too.

Here's what you can still control before December 31st:

- Adjust your withholding to cover the gap between 22% and your real rate

- Exercise ISOs strategically to avoid AMT (or trigger it intentionally if you're in a low-income year)

- Sell losing positions to offset gains from equity comp (called tax-loss harvesting)

- Time ESPP sales to qualify for better tax treatment

- Review state tax obligations if you moved or worked remotely this year

Each of these moves can save you hundreds or thousands of dollars. But only if you act before the calendar flips.

Why You Can't Fix This in January

Tax planning is like steering a ship. You need to turn the wheel before you reach the rocks, not after you've hit them.

Once January 1st arrives, your tax year is locked. You can't:

- Change how much was withheld from your March RSU vest

- Undo a stock sale that created a big capital gain

- Exercise ISOs to manage your AMT situation

- Qualify for long-term capital gains treatment on sales that happened too early

The decisions you make (or don't make) this month will show up on your tax return in April. And by then, all you can do is write the check.

Next, let's figure out what equity events actually happened to you this year. You can't plan around what you don't know about.

The Sarah Scenario: How a 22% withholding rate can leave you owing thousands.

The Sarah Scenario: How a 22% withholding rate can leave you owing thousands.

Take Inventory: What Equity Events Happened This Year

Think of this like checking your bank statement before doing your taxes. You can't plan for what you don't know about. Before December gets crazy, spend 30 minutes gathering every equity event from this year.

Here's your detective checklist:

-

Log into your equity portal (E*TRADE, Fidelity, Schwab, etc.). Look for:

- RSU vesting dates and share amounts

- Stock option exercises (both ISOs and NSOs)

- Any shares you sold

-

Pull out your pay stubs. RSU vesting shows up as wages, usually with a note like "RSU Income" or "Stock Comp." The dollars appear right alongside your regular salary.

-

Check your brokerage statements. These show every stock sale you made, including the sale date and proceeds.

-

Review ESPP purchase confirmations. Most companies buy shares every 6 months. Did you have purchases in February and August? June and December?

-

Note which events had taxes withheld. RSUs usually do. ISO exercises usually don't. This matters a lot.

Real example: Marcus logged into his equity portal in early December. He discovered three things he'd half-forgotten:

$50,000of RSUs vested in February (his company withheld 22% for taxes)- He exercised

1,000 ISOsin June at a$20strike price when the stock was$45(no taxes withheld) - His ESPP bought

$8,000of shares in August

He wrote everything down with dates and dollar amounts. That list became his roadmap for the rest of his tax planning.

Why this matters: You might discover equity events that need action before December 31st. Or you might find tax bombs you didn't know were ticking. Either way, you need the full picture first.

Now let's talk about the biggest surprise most people find: that 22% RSU withholding usually isn't enough.

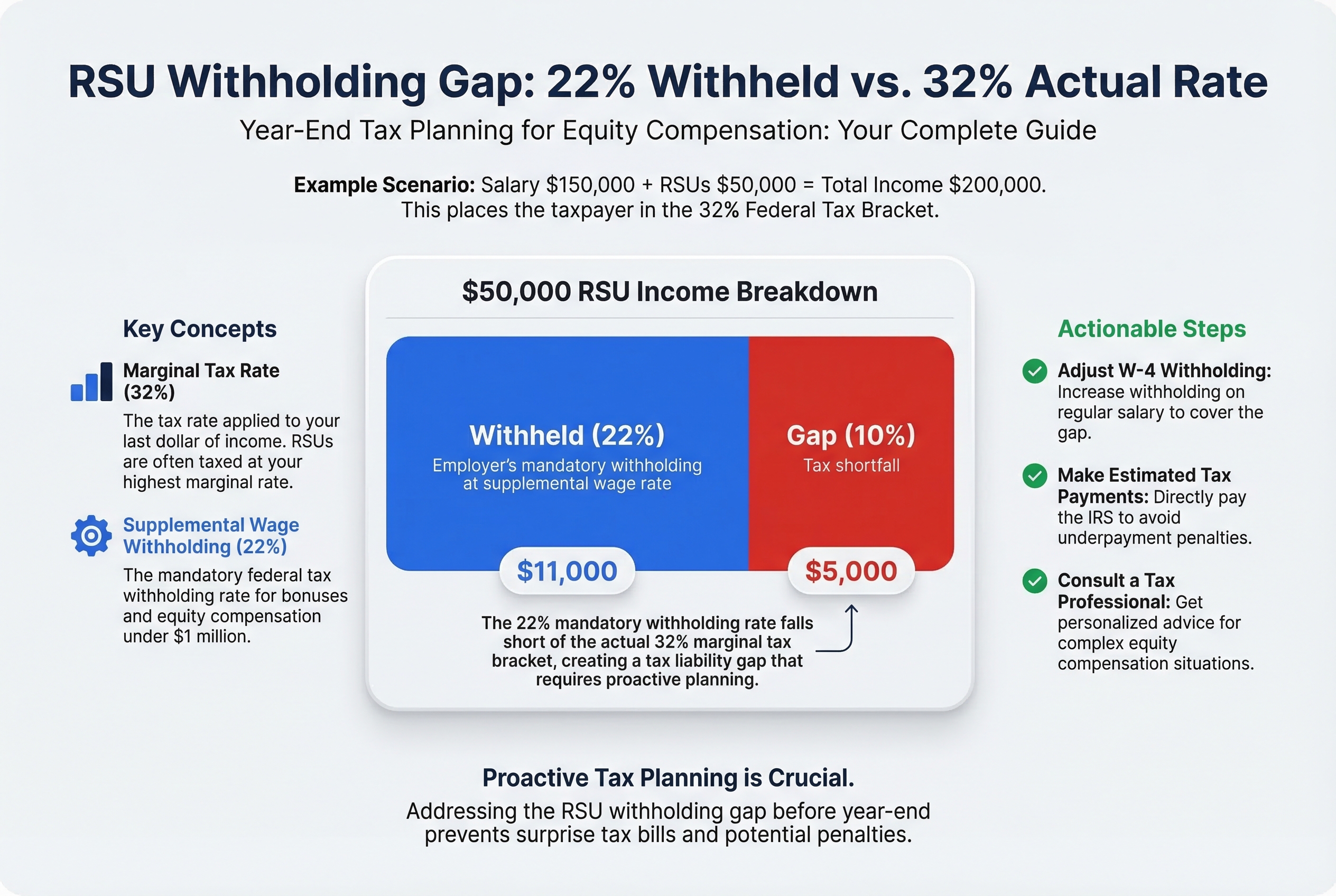

The RSU Withholding Gap: Why 22% Is Usually Not Enough

When your RSUs vest, your company automatically withholds 22% for federal taxes. It's like a restaurant adding an automatic 15% tip to your bill. Sounds convenient, right?

Here's the problem: 22% is almost never enough.

Why the Default Rate Falls Short

The IRS requires companies to withhold 22% on supplemental income like RSUs. But that's just a flat rate for everyone. Your actual tax rate depends on your total income for the year.

Think about it this way. If you earn $150,000 in salary and $50,000 in RSUs vest, your total income is $200,000. That puts you in the 32% federal tax bracket. But your company only withheld 22% on those RSUs.

Someone has to cover that 10% gap. That someone is you.

What's Your Real Tax Rate?

Here's how 2024 federal tax brackets work for single filers:

| Total Income | Tax Rate on RSUs |

|---|---|

| Up to $100,525 | 22% to 24% |

| $100,525 to $191,950 | 24% |

| $191,950 to $243,725 | 32% |

| $243,725 to $609,350 | 35% |

| Over $609,350 | 37% |

Married filing jointly? Double most of these thresholds.

The higher your total income, the bigger the gap between 22% withholding and what you actually owe.

A Real Example of the Gap

Jennifer had $120,000 of RSUs vest this year. Her company withheld $26,400 (that's 22%).

But Jennifer's salary plus RSU income puts her in the 35% tax bracket. She actually owes $42,000 in federal tax on those RSUs.

The gap: $15,600.

If Jennifer does nothing, she'll owe that $15,600 when she files her tax return in April. Plus potential underpayment penalties.

How to Cover the Gap Before Year-End

You have two options to fix this before December 31st:

Option 1: Adjust your W-4 withholding

Tell your payroll department to withhold extra federal tax from your remaining paychecks this year. Use line 4(c) on Form W-4.

Jennifer increased her withholding by $1,300 for her last December paycheck. That covered part of her gap.

Option 2: Make an estimated tax payment

You can send money directly to the IRS by January 15th. Use Form 1040-ES. Pay online at irs.gov/payments.

Jennifer will make an estimated payment for the remaining balance she couldn't cover through payroll.

Do the Math Now

Here's your calculation:

RSU value × your actual tax rate = total tax you oweRSU value × 22% = what was withheldLine 1 minus Line 2 = your gap

For Jennifer: ($120,000 × 35%) minus ($120,000 × 22%) = $15,600 gap.

Don't wait until April to discover you owe thousands. Run this calculation today for every RSU vest that happened this year.

Now let's talk about another year-end trap that catches people off guard: ISOs and the Alternative Minimum Tax.

How to Strategically use RSUs to Save Tax

The 10% RSU Withholding Gap: Comparing the default withholding rate to the actual marginal tax bracket.

The 10% RSU Withholding Gap: Comparing the default withholding rate to the actual marginal tax bracket.

ISO Exercises and the AMT Trap: What You Need to Know Before December 31st

ISOs create a phantom tax problem. You exercise your options and hold the stock, but the IRS treats your paper gain as income for Alternative Minimum Tax (AMT) purposes. You pay real tax on money you haven't actually received yet.

Think of it like this: You buy a house for $200k that's worth $500k, but you don't sell it. For regular tax purposes, no problem. But the AMT system says "you got a $300k bargain, so we're taxing that."

How the AMT Bargain Element Works

When you exercise ISOs, the difference between what you pay and what the stock is worth becomes AMT income.

The formula: (Fair market value - Exercise price) × Number of shares = Bargain element

This bargain element gets added to your income for AMT calculations. The AMT rate is typically 28% on this amount.

A Real Example

David exercised 5,000 ISOs in March. His numbers:

- Exercise price: $15 per share

- Stock value that day: $50 per share

- Bargain element: $35 per share × 5,000 shares = $175,000

That $175,000 gets added to his AMT income. At a 28% AMT rate, he owes about $49,000 in taxes. He didn't sell any shares. He just exercised and held them.

David didn't realize this until December. Now he needs to make an estimated tax payment to avoid penalties. He decides NOT to exercise more ISOs this year because it would make his AMT bill even bigger.

The Good News: AMT Credits

You do get an AMT credit for future years. When your regular tax exceeds your AMT in later years, you can use this credit to reduce your bill. But you need cash now to pay the AMT, and you might wait years to use that credit.

Should You Exercise More ISOs Before Year-End?

Stop and calculate if you already exercised ISOs this year. Use tax software or talk to a CPA to estimate your AMT liability. You need to know this number before December 31st.

Here's a simple decision guide:

- Already facing a big AMT bill? Don't exercise more ISOs this year. Wait until January.

- Haven't exercised any ISOs yet? You might have room to exercise some without triggering AMT, depending on your income and the AMT exemption amount.

- Exercised a small amount? Calculate whether you have room for more before hitting AMT territory.

- Stock price dropped since you exercised? You might be paying AMT on phantom gains that disappeared. This is the worst scenario.

Key factors that affect your decision:

- Your total income from all sources

- Your filing status and AMT exemption amount

- How much the stock has appreciated since your exercise

- Whether you have cash to pay the AMT bill

What to Do This Month

If you exercised ISOs any time this year, don't wait. Calculate your AMT liability now. Use tax software that handles AMT, or pay a CPA for a projection. You may need to make an estimated tax payment by January 15th.

If you're thinking about exercising more ISOs, run the numbers first. The tax surprise isn't worth it.

Your ESPP sales also create year-end tax planning opportunities, but the rules work differently than ISOs.

The Two-Year Rule: How to Get Favorable Tax Treatment on Your ISOs | The Breakdown Lane

ESPP Sales: Timing Matters More Than You Think

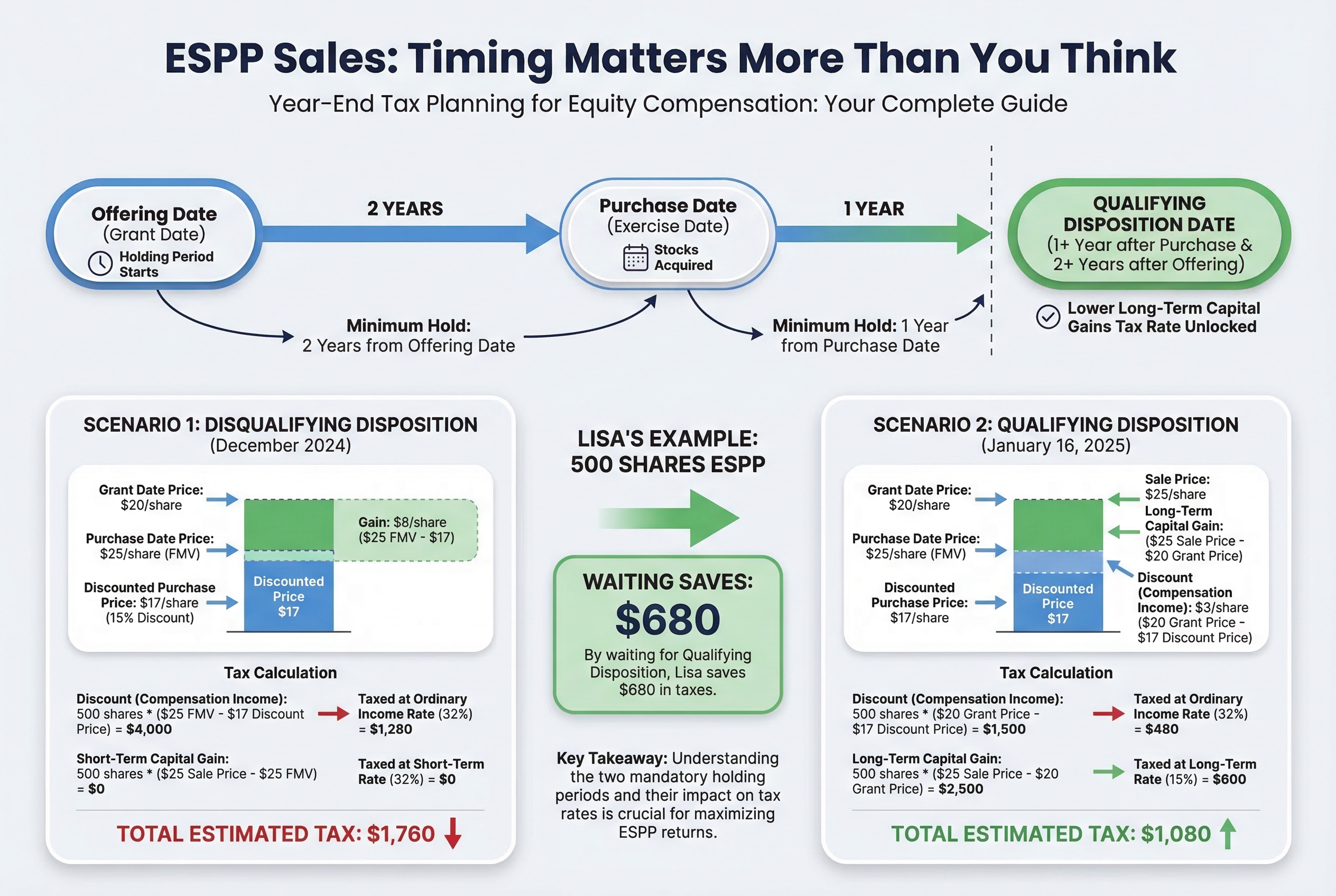

Your ESPP shares have two finish lines you need to cross before you can unlock better tax treatment. Think of it like a relay race where you need to pass both checkpoints to win the prize.

Most employees don't realize that selling ESPP shares a few weeks too early can cost them hundreds or thousands in extra taxes. The difference comes down to something called a "qualifying disposition."

The Two Holding Periods You Need to Know

To get a qualifying disposition, you must hold your ESPP shares for:

- At least 1 year from the purchase date (when you actually bought the shares)

- At least 2 years from the offering date (when the purchase period started)

You need to meet BOTH requirements. Miss either one by even a single day, and you have a "disqualifying disposition."

Why This Matters for Your Tax Bill

Disqualifying disposition (sold too early):

- The discount you got is taxed as ordinary income, just like your salary

- Any additional gain is taxed as capital gains (short-term or long-term depending on how long you held)

Qualifying disposition (met both holding periods):

- The discount is still ordinary income, but capped at the actual discount percentage

- Everything else is taxed as long-term capital gains (usually 15% vs. your higher ordinary rate)

A Real Example: The Cost of Selling Three Weeks Too Early

Lisa bought ESPP shares on January 15, 2024. The offering date for that purchase period was July 15, 2023. She paid $17/share with a 15% discount (fair market value was $20).

In December 2024, her shares are worth $28 and she wants to sell 500 shares.

If she sells in December 2024:

- The

$3discount gets taxed as W-2 income at her 32% rate =$0.96/sharein tax - The

$8gain is short-term capital gains at 32% =$2.56/sharein tax - Total tax:

$3.52/shareor$1,760on 500 shares

If she waits until January 16, 2025:

- It becomes a qualifying disposition (1 year from purchase, 2 years from offering)

- The

$3discount is still ordinary income at 32% =$0.96/share - The

$8gain is now long-term capital gains at 15% =$1.20/sharein tax - Total tax:

$2.16/shareor$1,080on 500 shares

By waiting three weeks, Lisa saves $680 in taxes.

Check Your Dates Before You Sell

Pull up your ESPP purchase confirmations right now. Look for two dates:

- Offering date: When did the purchase period begin?

- Purchase date: When did you actually buy the shares?

Count forward from both dates. If you're close to either deadline, waiting could save you serious money.

The January Strategy

If your shares are approaching the 1-year mark from purchase in December, consider this: Wait until January to sell. You'll likely qualify for long-term capital gains treatment on most of the gain.

The math is simple. Would you rather pay 32% on your gains or 15%? That's the difference between selling in December and waiting a few weeks.

One Big Warning About Cost Basis

Your brokerage will send you a Form 1099-B showing your sale. Here's the problem: They often report the wrong cost basis for ESPP shares. They might not include the discount that already got taxed as income.

This means you could get taxed twice on the same money if you're not careful. Keep your own records. Know what you paid and what discount you received.

Should You Wait? A Quick Decision Tree

Sell now if:

- You need the cash urgently

- You think the stock price will drop significantly

- You're already past both holding periods

Wait until January if:

- You're within weeks of the 1-year purchase date

- The stock price is stable or rising

- You can afford to wait for the tax savings

The tax savings often outweigh a small drop in stock price. Run the numbers for your specific situation.

The Dual Checkpoints: Meeting both the 1-year and 2-year holding periods for favorable ESPP tax treatment.

The Dual Checkpoints: Meeting both the 1-year and 2-year holding periods for favorable ESPP tax treatment.

Now that you understand ESPP timing, let's look at another year-end opportunity: using stock sales strategically to reduce your tax bill through tax-loss harvesting.

Stock Sales and Tax-Loss Harvesting: Your Last Chance This Year

Think of investment losses as tax coupons. You can use them to cut the tax bill on your gains. If you sold company stock this year and made money, those losses sitting in your brokerage account could save you hundreds or thousands in taxes.

Here's how it works: capital losses offset capital gains dollar for dollar. Sell a stock for a $5,000 loss? That wipes out $5,000 of gains from selling your company shares. Even better, if your losses exceed your gains, you can use up to $3,000 to reduce your regular income. Any leftover losses carry forward to next year.

Example: Tom's Tax Savings

Tom sold company stock in June and had a $40,000 capital gain. At the 15% capital gains rate, he owes $6,000 in taxes.

In December, he reviews his brokerage account. He owns Tech Stock XYZ that he bought for $15,000 but is now worth $10,000. That's a $5,000 loss.

He sells Tech Stock XYZ before December 31st. Now his net gain is $35,000 instead of $40,000. Tax savings: $5,000 × 15% = $750.

After waiting 31 days, he buys a similar tech fund to stay invested.

The Wash Sale Rule: No Immediate Buy-Backs

The IRS won't let you sell a stock and immediately buy back the same thing. That's called a wash sale. The rule blocks your loss if you buy the same or a substantially similar security 30 days before or after selling.

Wait 31 days before buying back. Or buy something different, like a mutual fund instead of the individual stock.

Your December Action Plan

Review every position in your brokerage account. Look for stocks or funds worth less than you paid. Those are candidates for tax-loss harvesting.

Key points:

- Sales must settle by December 31st to count this year

- Most stocks settle in 2 business days, so don't wait until the last minute

- Focus on positions with losses that you were planning to sell anyway

- This strategy works best if you had big gains from equity comp this year

Now let's talk about timing constraints you might face when trying to execute these year-end moves.

Trading Windows and Blackout Periods: Planning Around Your Company's Rules

Your company stock is like a store that's only open certain hours. You can't shop when it's closed, no matter how urgently you need something. That's how trading windows work.

Most public companies restrict when employees can buy or sell company stock. You can only trade during "open windows," typically a few weeks after the company releases quarterly earnings. During "blackout periods" (usually 2-4 weeks each quarter), you cannot trade at all.

Here's the problem: December often falls during a blackout period around year-end earnings.

Real Example: Missing Your Window

Rachel realized in mid-December she needs to sell $20,000 of company stock to cover her estimated tax payment due January 15th. But her company has a blackout period from December 15 through January 20.

She can't sell. Her options:

- Sell during the open window in early December (if she plans now)

- Pay the estimated tax from savings and sell in late January

- Set up a 10b5-1 plan in November for future years

This year, Rachel missed her window. She has to use savings and pay the tax bill herself.

How to Find Your Trading Windows

Check these places:

- Your company's insider trading policy (usually on the intranet)

- Your stock plan administrator's website

- Email your HR or legal compliance team

- Look for "trading window calendar" or "blackout period schedule"

Most companies publish trading calendars showing open and closed periods for the entire year.

The 30-60 Day Rule

Plan any equity sale at least 30-60 days before you need the money. This gives you buffer time if a blackout period pops up.

If you need cash for a January tax payment, sell in November, not December.

What About 10b5-1 Plans?

A 10b5-1 plan lets you sell stock during blackout periods, but you must set it up during an open window, typically 30-90 days before the first trade. Think of it as scheduling your trades in advance. We cover this in detail in our separate 10b5-1 planning guide.

Now let's tackle another year-end complication: what happens when you moved states or worked remotely this year.

State Tax Complications: When You Moved or Worked Remotely

Moving states or working remotely can turn your equity comp taxes into a tug of war. Multiple states may claim they deserve a piece of your income. And unlike a regular paycheck, the rules for equity compensation get weird fast.

The Basic Rule (That Gets Complicated)

Your equity comp gets taxed where you performed the work that earned it. Not where you live when it vests. Not where your company is headquartered. Where you physically worked.

For RSUs, most states tax based on where you lived on the vesting date. Simple enough.

For stock options, states look at where you worked during the entire vesting period. That's when it gets messy.

The Moving Trap

Mike lived in California until June 2024, then moved to Texas (which has no income tax). He had $60,000 of RSUs vest in September while living in Texas. He thinks he owes no state tax. Wrong.

His company granted those RSUs 2 years ago when he lived in California. California claims a portion of the RSU value based on how long he worked there during the vesting period. If he worked 18 months in CA and 6 months in TX during the 2-year vesting period, California taxes 75% of the RSU value. That's $45,000 taxable in California at rates up to 13.3%.

Moving from a high-tax state to a no-tax state doesn't erase your past. States remember where you were when you earned that equity.

California's Special Rules

California is particularly aggressive. The state taxes equity based on when you earned it, not when you received it. Even if you moved away years ago, California may claim a piece of your vesting RSUs or option exercises.

Think of it like a loyalty program with a long memory. California gave you the benefit of working there during your vesting period. Now they want their cut, even if you left.

No-Tax States Don't Mean No Taxes

These states have no income tax: Florida, Texas, Washington, Nevada, Tennessee, South Dakota, Wyoming, Alaska, and New Hampshire.

But moving to one doesn't eliminate all state taxes on your equity. Your old state may still claim a portion. And your company might not withhold correctly for your situation, leaving you with a surprise tax bill.

Remote Work Adds Another Layer

Worked remotely from a different state than your company's office? Some states say you owe taxes where you physically sat at your desk. Others say you owe where your company is located. A few want both.

If you worked remotely in multiple states during the year, you might need to file returns in several places. Each state gets a slice based on how many days you worked there.

When to Get Help

You need a CPA who specializes in multi-state equity comp if:

- You moved states during the year and have unvested equity

- You worked remotely in a different state than where you live

- You're leaving California with unvested RSUs or options

- You exercised ISOs while living in multiple states

- You have equity comp over $100,000 and changed states

This stuff gets complex fast. A $500 CPA consultation can save you thousands in taxes or penalties.

Now that you understand the state tax maze, let's pull everything together with a simple checklist you can actually use this month.

Your Year-End Equity Comp Checklist: What to Do This Month

Think of this like a pre-flight checklist. Pilots check every system before takeoff because missing one thing can cause big problems. Your equity compensation deserves the same careful attention before December 31st.

Here's your week-by-week action plan:

Week 1 (Dec 1-7): Gather Everything

Your mission: Create a complete picture of your 2024 equity activity.

- Log into your equity compensation portal (E*TRADE, Fidelity, Morgan Stanley, etc.)

- Download all statements and transaction history for 2024

- List every equity event:

- RSUs that vested

- Stock options you exercised

- ESPP shares you purchased or sold

- Any company stock you sold

- Pull up your pay stubs to see total taxes withheld so far

This takes 30 minutes. Do it first, or nothing else on this list will work.

Week 2 (Dec 8-14): Run the Numbers

Calculate two critical things:

-

Your withholding gap: Add up all RSU income from vesting. Multiply by your tax rate (probably 30-35% if you earn over

$100k). Subtract the 22% already withheld. That's your gap. -

Your AMT liability: If you exercised ISOs, use an AMT calculator or tax software to estimate what you'll owe. The IRS has a free tool on their website.

Check your trading window: Look up when you're allowed to sell stock. Many companies have blackout periods in December. If your window closes soon, you need to act fast.

Week 3 (Dec 15-21): Make Your Decisions

Time to choose your moves:

- Tax-loss harvesting: Sell any losing investments in your regular brokerage account. Those losses offset your equity comp gains.

- W-4 adjustment: If you have one more paycheck coming, increase your withholding to cover some of the gap.

- Estimated tax payment: Calculate if you need to make a payment by December 31st to avoid penalties.

Week 4 (Dec 22-31): Execute and Document

If you're selling stock:

- Place your trades while the window is open

- Save confirmation emails and screenshots

- Note the sale date and amount for your tax records

If you're making an estimated payment:

- Pay online through IRS Direct Pay (it's free and instant)

- Print the confirmation

- Mark it as "4th quarter estimated tax" in your records

Before midnight on December 31st:

- Review your 2025 vesting schedule

- Set calendar reminders for next year's trading windows

- Put all 2024 equity documents in one folder (digital or physical)

Real Example: Alex's December Checklist

Dec 1-7: Alex logs into E*TRADE and finds that 200 RSUs vested in March ($30,000 value) and 150 vested in September ($24,000 value). Total RSU income: $54,000. She also exercised 500 ISOs in June.

Dec 8-14: Alex calculates her withholding gap. Her total tax rate is 32% (24% federal + 8% state). She should pay $17,280 in taxes ($54,000 × 32%), but only $11,880 was withheld ($54,000 × 22%). Gap: $5,400. She also runs TurboTax's AMT calculator and learns her ISO exercise will trigger $8,000 in AMT. She checks her company's trading window and sees it's open until December 15th.

Dec 15-21: Alex sells a tech stock in her brokerage account that's down $3,000 this year. That loss will offset some of her RSU gains. She increases her W-4 withholding by $200 for her final December paycheck.

Dec 22-31: Alex makes a $12,000 estimated tax payment through IRS Direct Pay to cover the withholding gap and part of her AMT bill. She schedules a January call with her CPA to discuss claiming the AMT credit next year and planning her 2025 ISO strategy.

When to Get Professional Help

Stop and call a tax professional if any of these apply to you:

- You moved to a different state this year

- You exercised ISOs (AMT is complex)

- You sold ESPP shares (the tax rules are tricky)

- Your income is over

$200,000 - You're not sure how to calculate estimated taxes

- You feel overwhelmed by any of this

A CPA who specializes in equity compensation costs $300-500 for a consultation. That's cheap compared to the penalties and mistakes you might make on your own.

The Cost of Waiting

Every day you delay in December shrinks your options. If you wait until December 28th and discover you need to sell stock, your trading window might be closed. If you wait until January 2nd to make an estimated payment, you'll owe penalties.

December is your window of control. Use it.

Now that you have your action plan, let's talk about what comes next after you've completed these year-end tasks.

3 Tips for Year End Tax Reporting

What to Do Right Now: Your Next Steps

You've made it through the guide. Now what? Think of this like eating an elephant. You can't do it all at once, but you can take one bite at a time.

If you only have 1 hour today, do this:

-

Log into your equity portal. Write down every equity event from 2024: RSU vests, ISO exercises, ESPP purchases, stock sales. Note the dates and dollar amounts.

-

Calculate your RSU withholding gap. Take your total RSU value (shares times price at vest). Multiply by your tax rate (probably 30-40% if you earn over $100k). Compare that to what was actually withheld. The difference is what you might owe.

-

Check your company's trading window calendar. Note when the next window opens. Mark any blackout dates.

Done. You now know the most critical information.

If you have 3 hours this week, add:

- Calculate your AMT exposure if you exercised ISOs (use the formula from Section 4)

- Review your taxable brokerage account for tax-loss harvesting opportunities

- Adjust your W-4 if you have a big withholding gap

Critical (Must Do by December 31st):

- Make estimated tax payments to cover any withholding gaps

- Execute tax-loss harvesting if you found opportunities

- Sell ESPP shares if you're planning to (check your trading window first)

Important (Next 2 Weeks):

- Adjust your W-4 for 2025 to avoid next year's withholding gap

- Download all equity statements and tax forms from your portal

- Check if you need to make a same-day ISO sale before year-end

Helpful (Before January 15th):

- Find a CPA who understands equity compensation (ask colleagues for referrals)

- Organize all documents: W-2, 1099-B, 3921 forms, 3922 forms

- Set up a spreadsheet to track 2025 equity events as they happen

Where to Get Help:

Your company's HR or equity team can explain your specific plans and vesting schedules. A fee-only financial planner can help with big-picture strategy. A CPA with equity comp experience is essential if you have ISOs or complex situations.

Don't panic. Taking any action is better than taking no action. Even if you only complete the 1-hour task list, you're ahead of most people. Start with what you can do today, then tackle the rest over the next two weeks.

You've got this.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis