Early Exercising Stock Options: A Complete Guide to Buying Before Vesting

How to buy your shares before they vest and why it might save you thousands in taxes

Published March 14, 2026 · Updated March 14, 2026

Early exercising means buying your stock option shares before they vest, which can unlock significant tax advantages. This guide explains how it works, the benefits and risks, and helps you decide if it's right for your situation.

Why You're Reading This (And What Sarah Learned the Hard Way)

Sarah and Mike joined the same startup on the same day in 2019. They both got 10,000 stock options with a strike price of $0.50 per share.

Four years later, their stock was worth $5 per share. Both had fully vested options worth the same amount on paper. But their tax bills looked completely different.

Sarah's approach: She waited until her options vested, then exercised them all at once. She paid $5,000 to buy the shares ($0.50 × 10,000). But the IRS saw her shares as worth $50,000 ($5 × 10,000). That $45,000 difference? Taxable income. Her tax bill: $18,000.

Mike's approach: He exercised on day one, back when the stock was still worth $0.50. He paid the same $5,000 to buy the shares. But since the strike price and market price were identical, the IRS saw zero profit. His tax bill at exercise: $500 (just AMT on the spread, which was minimal).

Same company. Same options. A $17,500 difference in taxes.

Early exercise means buying your stock options before they vest. Think of it like pre-paying for concert tickets before the artist gets famous. You lock in today's price, even though you can't actually use the tickets yet.

This strategy isn't available at every company. Most large public companies don't allow it. But if you work at a startup or pre-IPO company, your option agreement might give you this choice.

The question is: should you take it? And what happens to your money if you leave before those shares actually vest?

Let's break down exactly how this works.

What Early Exercise Actually Means (The Simple Version)

Early exercise means you buy your stock options before they vest. You pay cash upfront, but you don't fully own those shares yet.

Think of it like buying a car with a payment plan, except backwards. You pay the full price today, but you only truly own the car after making your "payments" by staying at the company through your vesting schedule.

Here's what actually happens:

You get stock options with a vesting schedule (usually 4 years). Let's say 4,000 options at a $0.50 strike price.

You decide to early exercise on day one. You write a check for $2,000 (4,000 shares × $0.50) and buy all the shares immediately.

The shares are still restricted. Your vesting schedule doesn't change. You still need to stay at the company to earn full ownership.

If you leave early, the company buys back your unvested shares at your original strike price. You get your money back for those shares, nothing more.

A Real Example

You join a startup and get 4,000 options vesting over 4 years (1,000 shares per year). You early exercise everything on your first day, paying $2,000 total.

Six months later, you leave for another job. Only 500 shares have vested so far. The company buys back the other 3,500 unvested shares at $0.50 each. You get $1,750 back. You keep your 500 vested shares.

Important: Not all companies offer early exercise. It's most common at early-stage startups where the strike price is still low. Your option grant paperwork will say if early exercise is allowed.

Now that you understand the mechanics, let's talk about why anyone would do this. The answer is taxes, and the potential savings are huge.

Early Exercise Stock Options Explained (Pros, Cons & 83(b) Election)

The Tax Magic: Why People Early Exercise

Early exercise is like freezing your tax bill at today's price instead of paying tomorrow's inflated rate.

Here's the core idea: When you exercise stock options, you pay taxes based on the "spread." That's the difference between your strike price (what you pay) and the fair market value (what the stock is worth today). The smaller that spread, the smaller your tax bill.

The Freezing Effect

When you early exercise, you're trying to catch that spread at $0 or close to it. This does three powerful things:

- Minimizes your immediate tax hit. Less spread = less tax now.

- Starts the capital gains clock ticking. Hold for a year, and future gains get taxed at lower capital gains rates (15-20%) instead of ordinary income rates (22-37% for most people).

- Locks in your tax basis. All future growth becomes capital gains, not ordinary income.

The Real Numbers: Two Scenarios

Let's say you have 1,000 options with a $1 strike price.

Scenario A: Exercise at grant (early exercise)

- Fair market value: $1

- Spread: $0 ($1 FMV - $1 strike)

- Tax on exercise: $0

- You pay: $1,000 to buy the shares

Two years later, the stock hits $50. You sell for $50,000.

- Your gain: $49,000 ($50,000 - $1,000)

- Tax type: Long-term capital gains (you held over a year)

- Tax bill: $7,350 (15% rate)

- You keep: $41,650

Scenario B: Exercise after 2 years (standard approach)

- Fair market value: $10

- Spread: $9 ($10 FMV - $1 strike)

- Tax on exercise: $3,330 (37% ordinary income rate on $9,000 spread)

- You pay: $1,000 for shares + $3,330 in taxes = $4,330 total

Stock immediately hits $50. You sell for $50,000.

- Your gain: $40,000 ($50,000 - $10,000 basis)

- Tax type: Short-term capital gains (ordinary income, 37%)

- Tax bill: $14,800

- You keep: $31,870

The difference? $9,780 more in your pocket with early exercise.

The ISO Bonus

If you have ISOs (incentive stock options), early exercise has an extra superpower. Exercise at grant when the spread is $0, and you avoid the dreaded Alternative Minimum Tax (AMT) entirely. That's a tax trap that can cost you thousands.

The Catch

This tax magic requires paying cash upfront for shares that might become worthless. You're betting $1,000 today to save $9,780 later. But if the company fails, that $1,000 is gone.

The earlier you exercise, the more potential tax savings. But you're also taking on more risk because there's more time for things to go wrong.

Now let's look at how this works differently depending on whether you have ISOs or NSOs.

ISOs vs NSOs: How Early Exercise Works Differently

Think of ISOs and NSOs as two different board games with the same goal but totally different rules. Both let you early exercise. Both help you start the capital gains clock sooner. But the tax consequences play out in completely different ways.

ISOs: The "No Tax Now" Option (With a Catch)

When you early exercise ISOs at their strike price, you typically pay zero ordinary income tax right away. Here's why: the IRS only cares about the spread between what you pay (strike price) and what the stock is worth (fair market value). If those numbers match, the spread is zero.

Example: You have 2,000 ISOs with a $0.50 strike price. You early exercise when the FMV is still $0.50. You pay $1,000 total. No ordinary income tax due at exercise.

The catch? Alternative Minimum Tax (AMT). If there IS a spread when you exercise (FMV is higher than strike price), that spread counts as income for AMT purposes. You might owe AMT even though you don't owe regular income tax. This is why early exercise works best for ISOs when FMV equals strike price.

To get the best tax treatment (long-term capital gains rates on all your profit), you must hold the shares for 2 years from the grant date AND 1 year from the exercise date. Miss either deadline and your ISOs turn into NSOs for tax purposes.

NSOs: Always Taxed, But You Control When

NSOs always create ordinary income tax on the spread between strike price and FMV. Always. No exceptions.

Same example with NSOs: You have 2,000 NSOs with a $0.50 strike price. You early exercise when FMV is $0.50. You file an 83(b) election (more on this next section). You report $0 of ordinary income because there's no spread. You pay nothing in taxes.

Now compare that to waiting. If you exercise those same NSOs when FMV hits $8.00, you pay ordinary income tax on $7.50 per share. That's $15,000 in taxable income at your regular tax rate (potentially 35% or more with federal and state taxes combined).

The Key Difference in Action

Here's what happens with both types if the company goes public at $20 per share:

ISO path (early exercised at $0.50):

- Paid $1,000 to exercise

- Held for required periods

- Sell at $20: entire $19.50 gain taxed as long-term capital gains (typically 15-20%)

- Profit after taxes: roughly $32,000

NSO path (early exercised at $0.50 with 83(b)):

- Paid $1,000 to exercise

- Reported $0 ordinary income

- Sell at $20: $19.50 gain taxed as long-term capital gains

- Profit after taxes: roughly $32,000 (same result!)

NSO path (waited, exercised at $8.00):

- Paid $16,000 to exercise

- Reported $15,000 ordinary income (taxed at ~40% = $6,000 in taxes)

- Sell at $20: $12 gain taxed as long-term capital gains

- Profit after taxes: roughly $19,000

Both ISOs and NSOs benefit hugely from early exercise. ISOs just have a cleaner path if you meet all the holding requirements.

Next, we'll cover the 83(b) election, the paperwork that makes early exercise work for tax purposes. You have exactly 30 days to file it, and missing that deadline costs you thousands.

The 83(b) Election: Your 30-Day Deadline That Changes Everything

Think of the 83(b) election as tax insurance. You're locking in today's tax bill to protect yourself from a much bigger one later.

Here's the deal: When you early exercise, the IRS normally wants to tax you when your shares vest, not when you buy them. That's a problem. If your stock price jumps from $1 to $15 by vesting day, you'd owe taxes on that $14 gain even though you already own the shares.

The 83(b) election tells the IRS: "Tax me now on what I'm buying, not later when it vests."

Why This Matters (A Real Example)

You early exercise 5,000 NSO shares at $1 per share when the fair market value is also $1. No spread, so no immediate tax bill. You file an 83(b) election.

Two years later, those shares vest. The stock is now worth $15.

Without 83(b): You owe ordinary income tax on $70,000 ($14 spread × 5,000 shares). At a 35% tax rate, that's $24,500 in taxes. You didn't sell anything, but you owe $24,500 in cash.

With 83(b): You owe nothing at vesting. Zero. The IRS already taxed you when you exercised (when there was no spread). You only pay capital gains tax later when you actually sell.

That's $24,500 saved because you filed a one-page form.

The 30-Day Deadline (No Exceptions)

You have 30 calendar days from your early exercise date to file the 83(b) election. Not 30 business days. Not "about a month." Exactly 30 days.

Miss this deadline by one day, and you lose the benefit forever. The IRS doesn't grant extensions. They don't care if you were on vacation or didn't know about it.

Real horror story: Mike early exercised 10,000 shares at his Series A startup. His lawyer mentioned the 83(b) but Mike forgot to file it. Three years later at IPO, his shares were worth $50 each. He owed ordinary income tax on $500,000 at vesting. His tax bill: $175,000. All because he missed a deadline.

Why ISOs and NSOs Are Different Here

For NSOs, the 83(b) election prevents double taxation. Without it, you get taxed at exercise AND at vesting. That's brutal.

For ISOs, the 83(b) prevents AMT (Alternative Minimum Tax) from hitting you at vesting instead of at exercise. You still want to file it, but the consequences of missing it are usually less severe.

Bottom line: File the 83(b) for both ISO and NSO early exercises. Always.

How to File (Your Checklist)

Filing an 83(b) is simple, but you need to do it right:

-

Get the form. Download IRS Form 83(b) or have your company provide a template. It's one page.

-

Fill it out. You need basic info: your name, address, number of shares, price paid, fair market value, and exercise date.

-

Make three copies. One for the IRS, one for your company, one for your records.

-

Mail to the IRS via certified mail. Send it to the IRS Service Center where you file your tax return. Get a tracking number and delivery confirmation.

-

Give a copy to your company. They need it for their records.

-

Attach a copy to your tax return. When you file taxes for the year you exercised.

-

Keep your proof of mailing forever. That certified mail receipt is gold. If the IRS ever questions your filing, it's your only proof.

The whole process takes 30 minutes and costs about $8 for certified mail. That's the best $8 you'll ever spend.

What If You're Close to the Deadline?

If you're on day 28 and just realized you need to file, don't panic. But move fast.

Fill out the form immediately. Drive to the post office. Send it certified mail with return receipt. Get your tracking number. You're good as long as the postmark is within 30 days.

Some people send it overnight or express mail just to be safe. That's fine, but the postmark date is what matters, not when it arrives.

The Bottom Line

The 83(b) election is not optional if you early exercise. It's mandatory for the strategy to work. Set a calendar reminder the day you exercise. File within a week if possible. Keep proof forever.

This one form is the difference between paying taxes on phantom gains and building real wealth from your equity.

Now that you understand the 83(b), let's talk about another tax benefit that makes early exercise even more powerful: the QSBS exclusion that could save you millions.

83(b) Election Explained: Avoid Massive Taxes with ISO Stock Options

The QSBS Superpower: Why Startup Employees Care About Early Exercise

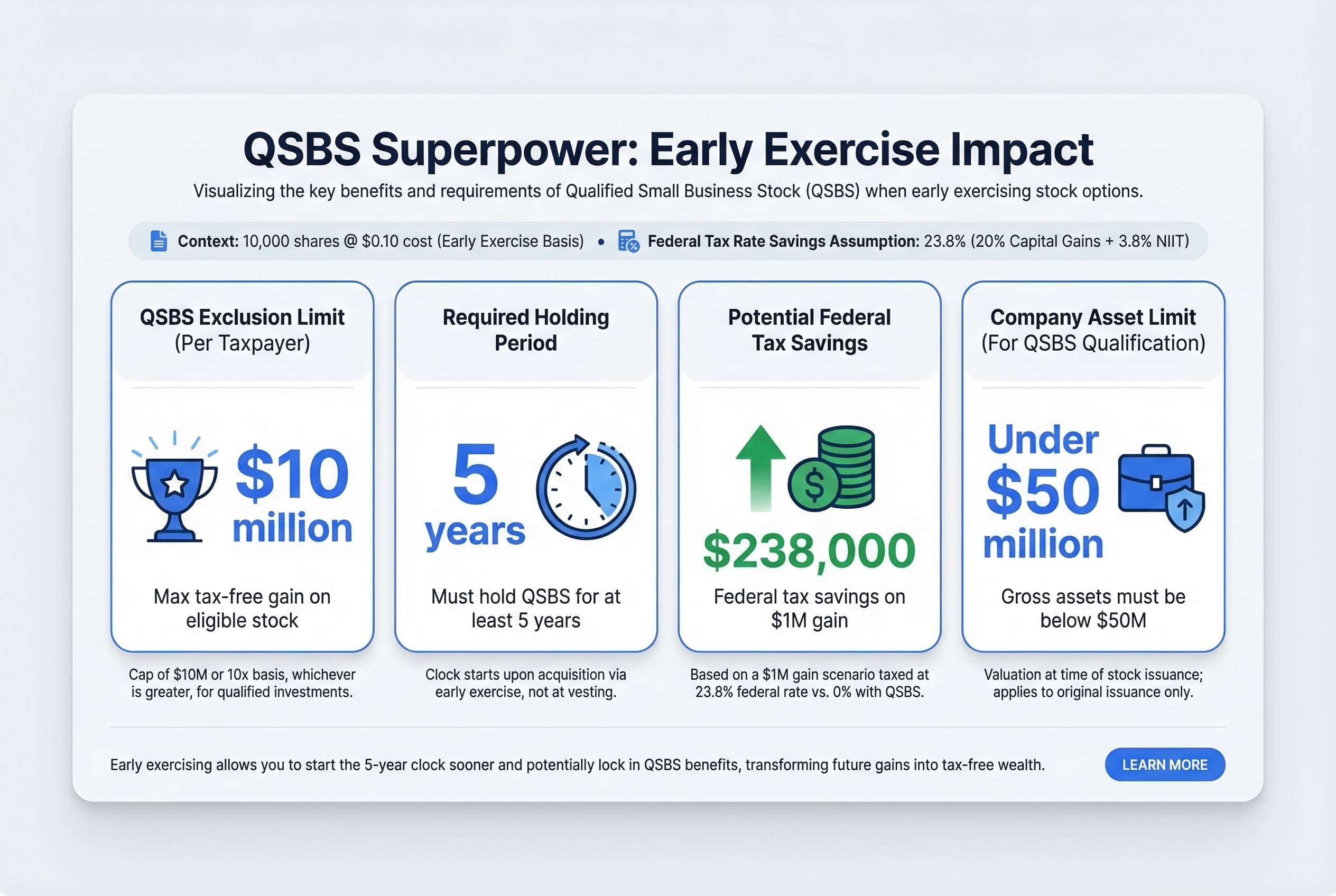

Early exercise has a secret weapon called QSBS. It stands for Qualified Small Business Stock, and it could save you millions in taxes.

Here's the big prize: If your shares qualify as QSBS and you hold them for 5 years, you can exclude up to $10 million in gains from federal taxes. That's right, $10 million tax-free.

Think of QSBS like planting an apple tree. You need to own the tree for 5 full years before you can harvest tax-free fruit. Early exercise lets you plant that tree on day one of your job, not years later when your options vest.

Here's why the timing matters so much:

Let's say you join a startup at founding as employee number 5. You early exercise 10,000 shares at $0.10 each (total cost: $1,000). Seven years later, the company goes public at $100 per share. Your shares are now worth $1 million.

With QSBS, you pay $0 in federal taxes on your $999,000 gain. You just saved about $238,000 in federal capital gains taxes (at 23.8% rate).

Now imagine you didn't early exercise. You waited and exercised your shares after 2 years when they vested. The company IPOs 5 years after you joined. You've only held the shares for 3 years, not 5. No QSBS benefit. You owe that $238,000 to the IRS.

The catch: Your company must qualify

Not every company's stock counts as QSBS. The company needs to be a C-corporation with under $50 million in assets when you buy your shares. Most early-stage startups qualify. Later-stage companies usually don't.

This is why QSBS matters most for the first 10-50 employees. If you join when the company is tiny, you're more likely to qualify and hit that 5-year mark before a big exit.

Even if you never reach $10 million in gains, QSBS still helps. Excluding $500,000 in gains saves you about $119,000 in taxes. That's real money.

The bottom line: Early exercise starts your QSBS clock immediately. Waiting to exercise means waiting to start that 5-year countdown, and you might run out of time before your company exits.

Now let's talk about the risks nobody mentions in those exciting equity offer letters.

The QSBS superpower: Early exercise allows employees to start the 5-year holding clock immediately to potentially exclude up to $10 million in gains.

The QSBS superpower: Early exercise allows employees to start the 5-year holding clock immediately to potentially exclude up to $10 million in gains.

The Real Risks: What Your Company Won't Tell You

Early exercising is like buying concert tickets six months in advance. If the show happens and it's amazing, you got a great deal. But if the concert gets cancelled? Your money is just gone.

Here's what most companies won't emphasize when they offer early exercise: you're betting real cash on an uncertain outcome.

Most Startups Fail (And Your Shares Go With Them)

The numbers are brutal. About 90% of startups fail. Even companies that seem promising can shut down.

Let's say you early exercise 8,000 shares for $4,000. The company has great energy. Smart people. Exciting product. You feel good about it.

Two years later, the company runs out of money and shuts down. Your shares are worth $0. That $4,000 is gone forever.

The opportunity cost hurts even more. If you'd put that $4,000 in an S&P 500 index fund instead, it might be worth $5,200 by now. Your real loss isn't just $4,000. It's $5,200 in potential value.

Your Cash Is Locked Up for Years

When you early exercise, your money disappears into a black box. No public market exists to sell your shares. You can't access that cash until the company goes public or gets acquired.

That typically takes 7-10 years. Sometimes it never happens.

The Company Can Take Back Unvested Shares

Most companies include repurchase provisions. If you leave before your shares fully vest, the company can buy back the unvested portion at your original exercise price.

You paid $4,000 for 8,000 shares. Only 2,000 have vested when you leave. The company can repurchase the other 6,000 shares for $3,000. You lose any appreciation those shares gained.

The AMT Trap (For ISOs)

With ISOs, you might owe AMT even though you haven't sold anything or received any cash. We covered this in the tax section, but it's worth repeating: you can owe tens of thousands in taxes on shares you can't sell.

If the company later fails, you paid real tax money on worthless shares. The IRS doesn't give refunds.

Real Story: Tom's $15,000 Lesson

Tom joined a hot AI startup in 2021. He early exercised 10,000 shares for $15,000. The company had just raised a big funding round. Everyone was optimistic.

By 2023, the funding environment had changed. The company couldn't raise more money. It shut down.

Tom's shares: worthless. His $15,000: gone. His AMT bill from the early exercise: $4,200 that he still had to pay.

Total loss: $19,200 for shares worth zero.

Why This Matters

Early exercise isn't just a tax strategy. It's a concentrated bet on one company with money you might need for other things.

You're trading guaranteed cash today for uncertain equity tomorrow. Sometimes that bet pays off spectacularly. Sometimes you lose everything.

Now that you understand the risks, let's talk about what happens if you leave your company before your shares vest.

What Happens to Your Money If You Leave Before Vesting

Here's the good news: if you leave your company before your shares vest, you typically get your money back.

Think of early exercise like a refundable deposit on an apartment. If you move out early, you get the deposit back. You don't keep the apartment, but you're not out the cash.

How the Repurchase Works

Most companies have the right to buy back your unvested shares within 90 days of your last day. They pay you what you originally paid per share. Not the current fair market value. Not zero. Your original exercise price.

This is actually protection for you. With regular stock options, if you leave before vesting, you get nothing. With early exercise, you get a refund.

The Math When You Leave

Let's say you early exercised 4,000 shares at $0.75 each. You paid $3,000 total.

After 18 months, you get a better job offer. Here's what happens:

- Month 18: 1,500 shares have vested (you worked 1.5 years of a 4-year schedule)

- Unvested shares: 2,500 shares still haven't vested

- Company buyback: Company repurchases 2,500 shares at $0.75 each = $1,875

- You keep: 1,500 vested shares (worth whatever the stock is worth)

- Cash returned: $1,875 of your original $3,000

You keep the vested shares forever. They're yours. The company can't touch them. And you got back 62% of your cash for the unvested portion.

It Doesn't Matter Why You Leave

The repurchase right works the same whether you:

- Quit for another job

- Get fired

- Get laid off

- Retire

The company still buys back unvested shares at your original price. The reason for leaving doesn't change the terms.

The Rare Exception

Some companies (maybe 10%) let you keep unvested shares even after you leave. This is unusual but worth asking about before you early exercise. Check your stock option agreement or ask your equity admin team.

Now that you understand the downside protection, let's talk about the actual cash you need upfront.

How Much Cash You Actually Need (The Real Numbers)

Think of early exercising like buying a car. You need cash for the sticker price, plus taxes, plus registration fees, plus insurance. The sticker price alone doesn't tell the full story.

Here's what you actually pay:

The Basic Formula:

- Exercise cost = number of shares × strike price

- Plus: taxes on the spread (if FMV is higher than strike price)

- Plus: 83(b) filing costs (certified mail, copies, maybe legal review)

- Total: anywhere from a few hundred dollars to tens of thousands

Important: You need liquid cash. You can't use the shares as collateral or borrow against them. And you should keep this money separate from your emergency fund.

Scenario 1: The Cheap One (No Spread)

You join a startup on day one. You get 5,000 options at $0.10 strike price. The company just incorporated, so FMV equals strike price.

Your costs:

- Exercise: 5,000 shares × $0.10 = $500

- Taxes: $0 (no spread means no taxable income)

- 83(b) filing: $10 (certified mail)

- Total: $510

This is the sweet spot. You're buying early when it's cheap.

Scenario 2: The Moderate One (Small Spread)

You join after the Series A. You get 5,000 NSOs at $1 strike price. Current FMV is $2 per share.

Your costs:

- Exercise: 5,000 shares × $1 = $5,000

- Taxes: 5,000 shares × $1 spread × 24% tax rate = $1,200

- 83(b) filing: $10

- Total: $6,210

You're paying ordinary income tax on that $1 per share spread right now.

Scenario 3: The Expensive One (Big Spread with AMT)

You join after Series B. You get 5,000 ISOs at $5 strike price. Current FMV is $10 per share.

Your costs:

- Exercise: 5,000 shares × $5 = $25,000

- AMT: 5,000 shares × $5 spread × 28% AMT rate = $7,000

- 83(b) filing: $10

- Total: $32,010

This is where early exercise gets expensive. That AMT bill hits even though you haven't sold anything yet.

Can You Actually Afford It?

Ask yourself: Can I write this check and still sleep at night? Do I have 6 months of living expenses saved separately?

If the answer is no, early exercise might not be right for you, no matter how good the tax benefits look on paper.

Now let's figure out if spending this cash actually makes sense for your situation.

Should You Early Exercise? A Decision Framework

Think of early exercising like buying a lottery ticket, except you're betting on a company you work for instead of random numbers. Before you buy that ticket, you need to check a few things.

Here's the most important question: Can you afford to lose 100% of this money?

If the answer is no, stop reading. Don't early exercise. The risk is too high.

If the answer is yes, keep going through this checklist.

The Green Light Checklist

You should seriously consider early exercising if all of these are true:

- You're very early (employee #1-50)

- Your strike price equals the current FMV (zero spread)

- The exercise cost is under $5,000

- You have at least 6 months of emergency savings left after exercising

- You believe deeply in this company

- You plan to stay at least 5 years

- The company seems financially healthy

Example: Meet Alex. Alex is employee #15 at a startup. Strike price is $0.20. Current FMV is also $0.20. Exercising 5,000 options costs $1,000. Alex has $30,000 in savings and loves the company's mission.

Decision: Strong yes. Alex can afford to lose $1,000. There's no spread, so no immediate tax bill. If the company succeeds, Alex could save tens of thousands in taxes. If it fails, Alex lost $1,000, which is painful but not devastating.

The Yellow Light: Proceed Carefully

Early exercise gets risky when:

- A spread already exists between strike price and FMV

- Exercise costs more than 5% of your net worth

- You're employee #100+

- You're not sure about the company's future

- You might leave in the next 2-3 years

The Red Light: Don't Do It

Stop if any of these are true:

- Exercise costs more than 10% of your savings

- You don't have an emergency fund

- The company seems unstable (layoffs, leadership changes, missed targets)

- You're planning to leave soon

- You need this money for something else (house, wedding, debt)

Example: Meet Jordan. Jordan is employee #500. Strike price is $8. Current FMV is $12. Exercising 5,000 options costs $40,000 (the strike price). Jordan has $50,000 in savings and isn't sure the company will succeed.

Decision: No. The exercise cost is 80% of Jordan's savings. That's way too much risk. Plus, there's a $4 spread per share, which means Jordan would owe AMT on $20,000 of phantom income. If Jordan leaves or the company fails, that's $40,000 gone forever.

The Two-Part Test

Before you decide, answer these honestly:

Part 1: The Money Test

- Can I lose this entire amount and still be okay financially?

- Will I have 6+ months of expenses saved after exercising?

- Is the exercise cost under 5% of my net worth?

Part 2: The Belief Test

- Do I genuinely believe this company will succeed?

- Am I planning to stay at least 4-5 years?

- Is the company's financial health strong?

You need "yes" to all of Part 1 and most of Part 2.

The Stage Matters

Very early (pre-seed, seed): Early exercise makes the most sense. Strike prices are low. Risk is high, but so is potential reward.

Growth stage (Series B+): Less compelling. Strike prices are higher. The company is less likely to fail, but also less likely to 10x.

Late stage (pre-IPO): Usually not worth it. You're probably paying a significant spread. Better to just hold your options and exercise at IPO.

One More Reality Check

Ask yourself: If this company offered me a $10,000 bonus, would I use it to buy company stock?

If the answer is no, don't early exercise. You're essentially doing the same thing.

Now that you know whether early exercise makes sense for you, let's walk through exactly how to do it if you decide to move forward.

How to Actually Do It: The Step-by-Step Process

Early exercising is like following a recipe. Each step matters. Do them in order, and don't skip the 83(b) deadline or you'll ruin the whole dish.

Here's exactly what to do:

Step 1: Confirm Your Company Allows It (Day 1)

Email your HR team or stock admin. Ask: "Does our company allow early exercise of unvested stock options?"

Not all companies offer this. If they say no, you're done here. If they say yes, ask for the early exercise policy document.

Step 2: Get the Current Strike Price (Days 1-3)

You need two numbers:

- Your strike price (on your grant paperwork)

- The current 409A valuation (ask your finance team)

If these match, you owe zero taxes on exercise. If 409A is higher, you might owe AMT on ISOs or regular tax on NSOs.

Step 3: Calculate Your Total Cost (Day 3)

Example: You have 3,000 options at $0.60/share. That's $1,800 to exercise. Add potential taxes if the 409A is higher than your strike price.

Make sure you have this cash available. You can't use a credit card.

Step 4: Complete the Exercise Paperwork (Days 3-5)

Your company will give you forms. These usually live in:

- An equity management portal (like Carta or Shareworks)

- A PDF from HR

Read the repurchase terms carefully. The company can buy back unvested shares if you leave. At what price? Your strike price or current FMV? This matters.

Step 5: Pay the Company (Day 5-7)

Most companies accept:

- Wire transfer

- ACH transfer

- Personal check

Send the money. Get a receipt. Save that receipt forever.

Step 6: File Your 83(b) Election (Days 7-10)

This is the step that ruins people. You have 30 days from exercise to file. Not 31. Not "around a month." Exactly 30.

How to file:

- Complete IRS Form 83(b) (it's one page)

- Make three copies

- Mail one to the IRS via certified mail with return receipt

- Send one copy to your company

- Keep one copy for your records

The certified mail receipt is your proof. Without it, the IRS can claim you never filed.

Step 7: Keep Everything Forever (Literally)

Create a folder called "Stock Options - [Company Name]." Put in it:

- Original grant paperwork

- Exercise confirmation

- Payment receipt

- 83(b) form and certified mail receipt

- All correspondence

You'll need these for taxes when you eventually sell. That might be 10 years from now.

Common Mistakes That Cost People Thousands

Missing the 83(b) deadline: This is the big one. Set three calendar reminders. Tell your spouse. Write it on your bathroom mirror.

Not keeping proof of 83(b) filing: The IRS loses things. Your certified mail receipt is your insurance policy.

Not understanding repurchase terms: Some companies buy back unvested shares at your strike price (you break even). Others at current FMV (you profit even if you leave). Know which you have.

Exercising everything at once: You can exercise in batches. Start small if you're nervous.

If Something Goes Wrong

Can't find the 83(b) form? It's on the IRS website (search "IRS Form 83(b)").

Missed the 30-day deadline? You can't fix this. The tax treatment changes permanently.

Company won't tell you the 409A? That's a red flag. Consider not early exercising.

Guide to Early Exercising Stock Options with an 83(b) Election (Examples)

You've done it. You own shares. Now what? The final section covers your ongoing responsibilities and what to watch for.

What to Do Next: Your Action Plan

You've learned about early exercise. Now what? Think of this like planning a road trip. You need to check your car, map your route, and decide if you're actually going.

Here's your homework for this week:

Monday: Check if it's even possible Email your HR department or stock admin team. Ask: "Does our company allow early exercise of unvested stock options?" If they say no, you're done. If they say yes, keep going.

Tuesday: Find your numbers Dig up your option grant documents. Look for:

- How many options you have

- Your strike price per share

- Your vesting schedule

Write these numbers down.

Wednesday: Do the math Calculate what early exercise would cost you. Multiply your number of options by your strike price. Add a few hundred dollars for potential fees.

Thursday: Check your bank account Can you afford this cost without touching your emergency fund? Be honest. This money could sit locked up for years.

Friday: Gut check Do you believe your company will be worth significantly more someday? Would losing this money hurt you?

Let's see how Maria did this:

Maria emailed HR on Monday. They said yes to early exercise. Tuesday, she found her grant: 6,000 options at $0.80 each. Wednesday, she calculated the cost: 6,000 × $0.80 = $4,800. Thursday, she checked her savings: $22,000 available. Friday, she asked herself the hard question. She believed in her company and could afford to lose $4,800 if things went south. The following Monday, she started the exercise process.

This month: Get professional help If you're seriously considering early exercise, talk to a tax professional. Yes, it costs money. But so does screwing up your taxes.

Remember this: Not deciding is also a decision. Waiting means choosing to wait. That's okay. But make it an active choice, not a passive one.

You now understand something most employees never learn about. You know what early exercise means. You know the tax benefits. You know the risks. You know the 83(b) election exists and why it matters.

That puts you ahead of 95% of people with stock options.

Whatever you decide, you're making an informed choice. That's what matters.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis