How to Donate Appreciated Stock: A Simple Guide to Maximizing Your Charitable Impact

Why giving stock instead of cash could save you thousands in taxes

Published March 14, 2026 · Updated March 14, 2026

When you donate stock that has grown in value, you can avoid capital gains taxes and get a bigger tax deduction than if you sold the stock and donated cash. This guide explains how it works, who benefits most, and exactly how to do it.

Why Your Financial Advisor Keeps Telling You to Donate Stock

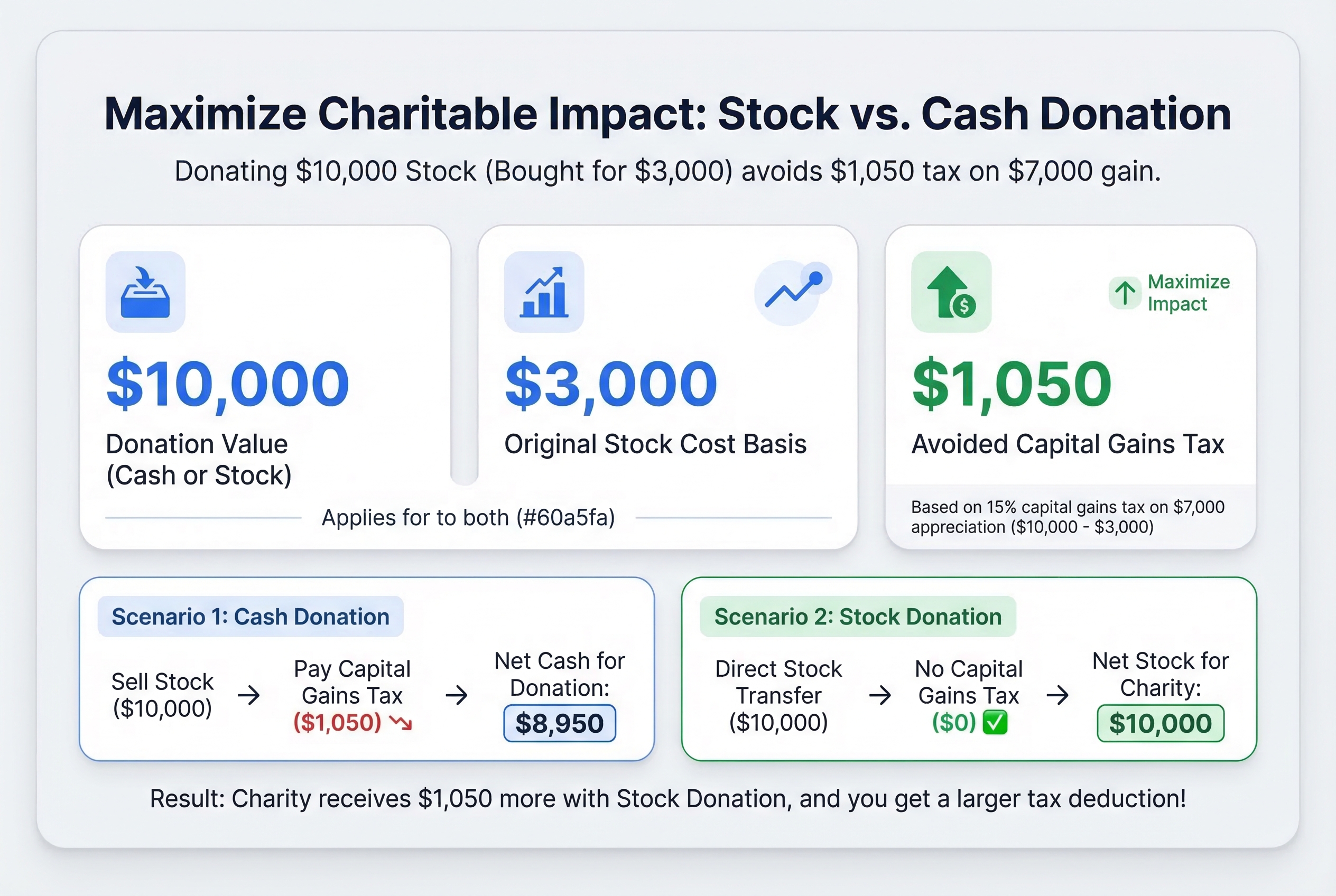

Meet Sarah. She wants to donate $10,000 to her favorite animal shelter this year. She has the cash sitting in her checking account, ready to write a check.

But Sarah also owns company stock worth $10,000. She bought those shares years ago for just $3,000. Her financial advisor keeps bugging her: "Donate the stock, not the cash."

Here's why that advice is worth listening to.

The cash donation path: Sarah writes a $10,000 check. Simple enough. She gets a $10,000 tax deduction. The charity gets $10,000. Done.

The stock donation path: Sarah transfers her $10,000 worth of stock directly to the charity. The charity still gets $10,000. Sarah still gets a $10,000 tax deduction. But here's the magic: she never pays the $1,050 in capital gains tax she would have owed if she'd sold that stock first (that's 15% tax on her $7,000 gain).

Think of it like this: why give the IRS a cut of your charitable donation? When you donate stock directly, you skip the tax bill entirely. The charity gets $1,050 more, and it doesn't cost you an extra penny.

This strategy works because you get two tax benefits at once. You avoid paying capital gains tax on the stock's growth, AND you get a deduction for the stock's full current value.

You don't need to be wealthy to use this strategy. If you own company stock that's gone up in value and you donate to charity anyway, you're leaving money on the table by donating cash instead.

This guide will show you exactly who benefits from donating stock, how the tax rules work, and how to actually do it. First, let's make sure you understand what "appreciated stock" really means.

The immediate benefit: Avoiding capital gains tax by donating appreciated assets.

The immediate benefit: Avoiding capital gains tax by donating appreciated assets.

What Appreciated Stock Actually Means (And Why It Matters for Donations)

Think of appreciated stock like a car you bought for $20,000 that's now worth $35,000. You made a profit without doing anything. That's appreciation.

Appreciated stock simply means stock that's worth more today than when you got it. The difference between what you paid and what it's worth now is your gain. And normally, Uncle Sam wants a cut of that gain when you sell.

The Three Numbers You Need to Know

Cost basis is what you originally paid for the stock. For RSUs, your cost basis is the stock's value on the day it vested (that's when you paid income tax on it). For shares you bought, it's what you paid.

Current value is what the stock is worth today. Check your brokerage account or look up the current price.

Capital gain is the profit in between. Current value minus cost basis equals your gain.

A Real Example

You received 100 RSU shares that vested when the stock was $50/share. Your cost basis is $5,000 (100 shares × $50).

Today those shares are worth $100/share, or $10,000 total.

Your stock has appreciated by $5,000. That's your capital gain.

Here's the key: If you sell those shares, you'll owe capital gains tax on that $5,000 profit. Depending on your tax bracket, that could be $750 to $1,000 going to the IRS.

But if you donate the stock instead? You never pay that tax. The charity gets the full $10,000, and you get a $10,000 tax deduction.

The One-Year Rule (Quick Preview)

To get these benefits, you must hold the stock for more than one year before donating. We'll cover this requirement in detail later, but it's worth noting now.

Now that you understand what appreciated stock is, let's look at exactly how much money those two tax benefits can save you.

Donating Appreciated Stock To Charity: A Win-Win Strategy for You and The Nonprofit

The Two Tax Benefits That Make Stock Donations Powerful

Donating appreciated stock isn't just good, it's like getting a two-for-one deal at your favorite store. You get two separate tax breaks that work together to multiply your savings.

Let's break down each benefit with real numbers.

Benefit #1: You Skip the Capital Gains Tax

When you sell stock that has grown in value, the IRS wants a cut of your profit. That cut is called capital gains tax.

For most people with significant stock holdings, the rate is steep:

- 20% federal capital gains tax on long-term gains

- 3.8% Medicare surtax on investment income for higher earners

- Total: 23.8% of your profit goes to taxes

But here's the magic: when you donate stock directly to charity, you never sell it. You never trigger that tax. The gain disappears.

Think of it like this: you're passing the stock to someone (the charity) who doesn't have to pay taxes on it. Nonprofits are tax-exempt, so they can sell your stock and keep 100% of the proceeds.

Benefit #2: You Deduct the Full Current Value

When you donate stock, you get to deduct what it's worth today, not what you originally paid for it.

If you bought stock for $10,000 and it's now worth $50,000, you deduct $50,000. You get credit for the full gift without paying tax on your $40,000 profit.

The Math: Why These Benefits Create Massive Savings

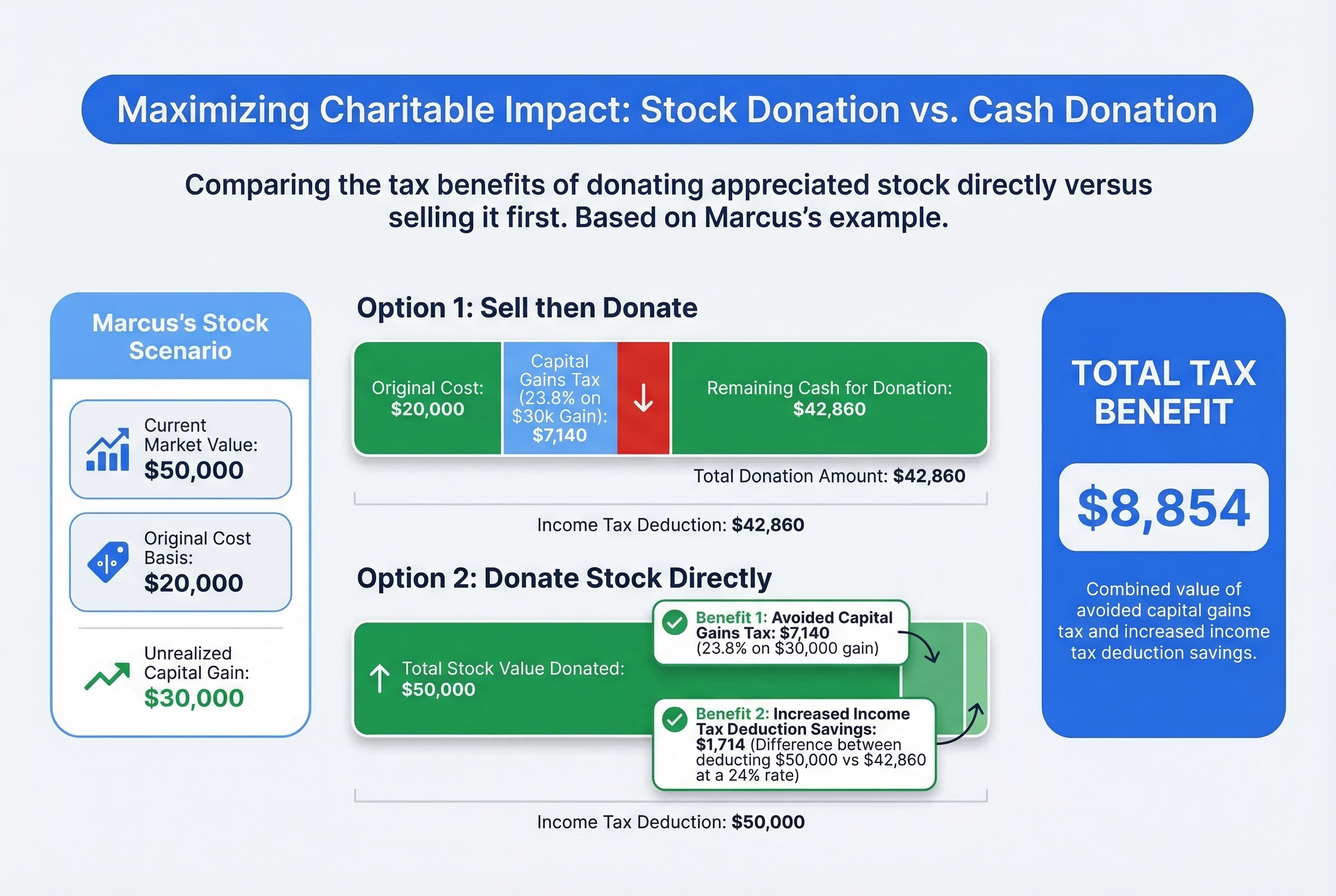

Let's see how this works for Marcus, who wants to donate $50,000 to his favorite charity.

Marcus owns stock worth $50,000 that he bought years ago for $20,000. That's a $30,000 gain.

Option 1: Sell the stock, then donate cash

- Marcus sells the stock

- He pays capital gains tax: $30,000 gain × 23.8% = $7,140 in taxes

- He has $42,860 left to donate

- He deducts $42,860, saving $10,286 in income tax (at his 24% rate)

- His real cost: $32,574

Option 2: Donate the stock directly

- Marcus transfers the stock to charity

- He pays $0 in capital gains tax

- The charity receives the full $50,000

- He deducts $50,000, saving $12,000 in income tax

- His real cost: $38,000

By donating stock instead of cash, Marcus gives $7,140 more to charity. Yes, his out-of-pocket cost is $5,426 higher, but the charity receives dramatically more.

Here's another way to think about it: Marcus avoided $7,140 in capital gains tax and gained an extra $1,714 in deductions ($50,000 vs $42,860 × 24%). That's $8,854 in total tax benefits compared to selling first.

Both Benefits Work at the Same Time

You don't choose between these benefits. You get both automatically when you donate appreciated stock:

- Zero capital gains tax on the profit

- Full deduction for today's value

This is why your financial advisor keeps bringing it up. These twin benefits make stock one of the most tax-efficient assets to donate.

Of course, not everyone benefits equally from this strategy. In the next section, we'll look at who saves the most and when you should just stick with donating cash.

E281: How Donating Appreciated Stock to Charity Can Save You Thousands in Taxes

The two-for-one deal: Deducting the full value while skipping the capital gains tax.

The two-for-one deal: Deducting the full value while skipping the capital gains tax.

Who Benefits Most From Donating Stock (And Who Should Just Donate Cash)

Here's the simple rule: the bigger the gap between what you paid and what it's worth now, the bigger your tax savings.

Think of it like upgrading a plane ticket. If you paid $200 for a ticket now worth $250, upgrading costs you $50. Not a huge deal. But if you paid $200 for a ticket now worth $1,000? That $800 gap makes upgrading incredibly valuable. Same logic applies to donating stock.

The Sweet Spot: When Stock Donations Make Perfect Sense

You're an ideal candidate if you check these boxes:

- Your stock has gained 50% or more since you bought it

- You're in the 24% tax bracket or higher ($100k+ income for single filers)

- You itemize deductions on your tax return

- Your gain is at least $1,000 (below this, the hassle often isn't worth it)

Example: Lisa bought ESPP shares 5 years ago for $15,000. They're now worth $60,000. That's a $45,000 gain. She's in the 32% tax bracket and itemizes deductions.

If Lisa donates the stock:

- She avoids $10,710 in capital gains tax (23.8% of $45,000)

- She gets a $19,200 income tax deduction (32% of $60,000)

- Total tax savings: nearly $30,000

If she sold the stock and donated cash instead, she'd lose that $10,710 to capital gains tax. That's money that could have gone to charity.

Marginal Cases: When It's a Coin Flip

Stock donations still work but offer smaller benefits if:

- Your stock gained less than 20%

- You're in the 12% or 22% tax bracket

- Your gain is under $2,000

You'll still save some tax dollars, but the advantage isn't dramatic. If the charity prefers cash or your brokerage makes stock transfers difficult, just donate cash.

Red Flags: When You Should Absolutely Donate Cash Instead

Don't donate stock if:

-

You have a loss. Sell the stock first, claim the loss on your taxes, then donate the cash. If you donate losing stock, you waste the tax loss.

-

You've held it less than one year. Short-term holdings don't qualify for the full fair market value deduction. You'll only deduct what you paid, not what it's worth now.

-

You don't itemize deductions. You won't benefit from the charitable deduction anyway. Just donate cash.

-

The gain is tiny (under $500). The paperwork and hassle outweigh the tax savings.

Example: James received RSUs 3 months ago. They were worth $10,000 at vest and are now worth $10,500. That's only a $500 gain, and he hasn't held them for a year yet.

James should donate cash or wait. If he donates the stock now, he'll only get a $10,000 deduction (what he paid in taxes at vest), not the full $10,500 value. Plus, the $500 gain barely moves the needle on his taxes.

Special Guidance for People with Equity Compensation

Your situation depends on timing and gains:

Great candidates:

- ESPP shares held 2+ years with big discounts (often 30%+ gains)

- Old stock options exercised years ago (potentially massive gains)

- RSUs vested 3+ years ago that have doubled or tripled

Poor candidates:

- RSUs that vested in the past year (little to no gain)

- Stock options exercised less than a year ago

- Any equity comp with losses

Here's why this matters: when your RSUs vest, you already paid income tax on their full value. If they haven't grown much since then, you're donating stock that's mostly "basis" (what you paid tax on). You might as well donate cash.

But if you have old ESPP shares or stock options from years ago? Those often have enormous gains. That's when stock donations become incredibly powerful.

Now that you know whether stock donations make sense for you, let's cover the rules you must follow to actually claim these tax benefits.

The One-Year Rule and Other Requirements You Must Know

Think of the one-year holding period like a maturity date on a savings bond. The IRS wants to see that you actually invested in the stock, not just bought it to immediately donate for a tax break.

Here's the rule that catches most people: You must hold the stock for more than one year to deduct its current market value. If you held it for one year or less, you can only deduct what you originally paid (your cost basis).

The Real Cost of Donating Too Soon

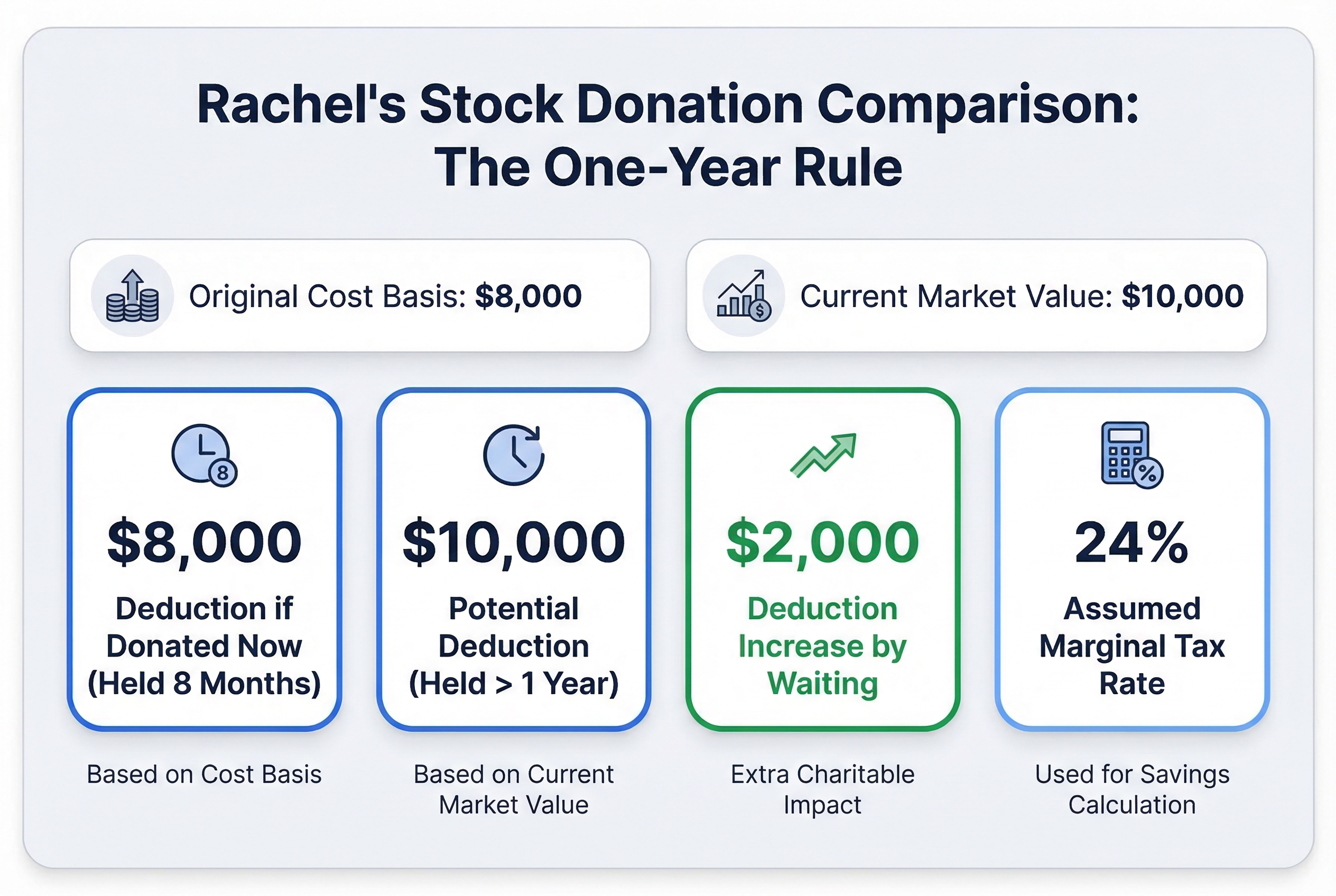

Rachel received 200 RSU shares that vested 8 months ago at $40/share ($8,000 cost basis). They're now worth $50/share ($10,000 value).

If she donates now, she can only deduct $8,000 because she hasn't held them for over a year. If she waits 5 more months, she can deduct the full $10,000.

That's a $2,000 difference in deduction, worth $480 in tax savings at a 24% tax rate. For most people, it's worth waiting.

Three More Requirements You Can't Skip

The charity must be a qualified 501(c)(3) organization. Your kid's sports team or a GoFundMe campaign doesn't count. Churches, universities, hospitals, and major charities like the Red Cross all qualify. When in doubt, check the IRS Tax Exempt Organization Search tool online.

You must itemize deductions to benefit. If you take the standard deduction ($14,600 for single filers, $29,200 for married couples in 2024), donating stock gives you zero extra tax benefit. You need enough itemized deductions (charitable gifts, mortgage interest, state taxes) to exceed the standard deduction.

The charity must actually receive the stock. A verbal promise doesn't count. The transfer must complete before December 31st if you want the deduction for that tax year.

The Prearranged Sale Trap

Never tell a charity "donate this stock and use the money for X specific purpose" if that requires them to sell immediately. The IRS may treat this as if you sold the stock yourself, meaning you owe capital gains tax. Let the charity decide when to sell.

Now that you know the basic rules, there's one more limit that might affect how much stock you can donate in a single year.

The cost of impatience: How the one-year holding rule impacts your deduction amount.

The cost of impatience: How the one-year holding rule impacts your deduction amount.

AGI Limits: How Much Stock You Can Actually Deduct Each Year

Think of the IRS like a highway patrol officer. They put a speed limit on your deductions each year. Even if you donate $500,000 of stock, you can't deduct it all at once.

The 30% Speed Limit

When you donate appreciated stock, you can only deduct up to 30% of your Adjusted Gross Income (AGI) per year. Your AGI is basically your total income: salary, bonuses, RSU income, investment gains, and other earnings.

This is different from cash donations, which have a higher 60% limit. Stock donations hit the lower ceiling because you're getting a bigger tax benefit (you skip capital gains taxes entirely).

What Happens When You Exceed the Limit

Let's say David earns $200,000 a year (his AGI). He wants to donate stock worth $100,000 to his favorite charity.

Here's the math:

- His 30% limit: $200,000 × 30% = $60,000

- Amount he can deduct this year: $60,000

- Leftover amount: $100,000 - $60,000 = $40,000

That extra $40,000 doesn't disappear. It carries forward to next year. David can use it on next year's tax return, as long as he has enough AGI to support it.

If David's AGI next year is $150,000, his new limit is $45,000 (30% × $150,000). He can deduct the full $40,000 carryforward because it's under his limit.

The Five-Year Carryforward Rule

You get up to five years to use any excess deduction. After that, you lose it. This is rare, but it can happen if your income drops significantly or you donate a massive amount.

Planning Strategy: Bunch Your Donations

If you regularly donate $20,000 a year, consider bunching multiple years into one. Donate $100,000 this year instead of $20,000 over five years. You'll use your full 30% limit now and potentially hit a higher tax bracket where the deduction is worth more.

This is where donor-advised funds become incredibly useful. You can dump all the stock into the fund this year, take the full deduction (up to your limit), and then distribute the money to charities over the next several years.

Donor-Advised Funds: The Secret Weapon for Stock Donations

Think of a donor-advised fund (DAF) as a charitable savings account you control. You deposit money or stock now, get an immediate tax deduction, and then recommend grants to charities whenever you want over months or years.

Here's the magic: you get the full tax benefit the year you contribute, but you don't have to decide which charities get the money right away.

How DAFs Work in Three Steps

- You contribute appreciated stock (or cash) to your DAF account. You get an immediate tax deduction for the full market value.

- The DAF sells the stock tax-free and holds the cash in your account. You can invest it to potentially grow the balance.

- You recommend grants to any IRS-approved charity whenever you want. Most DAFs process grants within days.

The catch? Once you contribute to a DAF, that money must eventually go to charity. You can't take it back for personal use.

Why DAFs Are Perfect for Stock Donations

Problem: You want to donate to five different charities, but transferring stock five times sounds like a nightmare.

Solution: Transfer stock to your DAF once. Then recommend grants to all five charities from your DAF account. The DAF handles the paperwork.

Problem: You're in the 12% tax bracket most years, so itemizing doesn't beat the standard deduction.

Solution: Use a DAF to "bunch" multiple years of donations into one high-income year.

Real Example: Handling a Big RSU Vesting

Emma usually earns $150,000 and donates $10,000 yearly to various charities. In 2024, a large RSU vesting pushes her income to $400,000.

Instead of her normal $10,000 donation, Emma contributes $50,000 of appreciated stock to a DAF. She avoids $11,900 in capital gains tax and deducts the full $50,000 in 2024 when her tax rate is highest.

Over the next five years, she recommends $10,000 grants annually from her DAF to her favorite charities. She's pre-funded five years of giving while maximizing her tax benefit in a single high-income year.

When to Use a DAF vs. Direct Donation

Use a DAF when:

- You want to bunch multiple years of donations into one year

- You're donating to several different charities

- You need time to research which charities to support

- You have a one-time income spike (RSU vesting, bonus, stock sale)

Donate directly when:

- You're only giving to one charity

- You want the charity to get the money immediately

- Your donation is small (under $5,000)

Most major investment firms offer DAFs. They charge small annual fees (typically 0.6% to 1% of your balance), but the tax savings usually dwarf these costs.

Now that you understand the strategy, let's walk through the actual mechanics of donating your stock.

Donating Stock Explained: Maximize Your Impact and Minimize Taxes | Ep. 7

Step-by-Step: How to Actually Donate Your Stock

Donating stock is like transferring money between banks, but instead of cash, you're moving shares. The process takes a few extra steps, but it's straightforward once you know what to do.

Here's exactly how to make it happen:

Step 1: Get the Charity's Brokerage Information

Call or email the charity's development office. Ask for their brokerage account details. You need three pieces of information:

- DTC number (a code that identifies their brokerage firm)

- Account number (the charity's specific account)

- Account name (usually the charity's legal name)

Most established charities have this information ready to share. If they seem confused, they might not have a brokerage account set up. We'll cover that situation below.

Step 2: Log Into Your Brokerage Account

Find the transfer or gift section. Look for options like "Transfer Shares," "Gift Stock," or "Charitable Transfer." Every brokerage platform looks different, but the basic process is the same.

Enter the charity's brokerage information and specify which stock you want to donate and how many shares. Double-check everything before submitting.

Step 3: Tell the Charity to Expect Your Transfer

This step is critical. Stock transfers don't include your name automatically. The charity will receive shares from an anonymous account if you don't notify them.

Send an email or call the charity right after you initiate the transfer. Tell them: "I've transferred 500 shares of ABC Company stock to your account. It should arrive by [date]."

Step 4: Get Written Acknowledgment

Once the transfer completes, the charity must send you a written receipt. This document is essential for your tax deduction.

The receipt should include:

- The charity's name and tax ID

- The date they received the shares

- The number of shares and company name

- A statement that you received no goods or services in return (if true)

Important: The charity does NOT need to state the dollar value. You determine that based on the stock price on the transfer date.

Step 5: Document the Stock's Value

Save your brokerage statement showing the transfer date. Look up the stock's closing price on that date. This price determines your tax deduction.

Keep these records with your tax files: the charity's acknowledgment letter, your brokerage statement, and proof of the stock's value on the transfer date.

Real Example: Tom's Food Bank Donation

Tom wants to donate 500 shares of his company stock to his local food bank. The shares are worth $50 each, so his total donation is $25,000.

On November 15, he calls the food bank and gets their brokerage info. On November 18, he logs into his Fidelity account, selects "Transfer Shares," chooses "Gift to Charity," and enters the food bank's brokerage details.

He immediately emails the food bank: "I've initiated a transfer of 500 shares of XYZ Corp, should arrive by November 25."

On November 23, the transfer completes. The food bank sends him a letter acknowledging receipt of 500 shares (worth $25,000 on November 23). Tom saves this letter plus his brokerage statement showing the transfer for his tax records.

Timing Matters

Stock transfers typically take 1-2 weeks to complete. During busy periods (like December), they can take longer.

For year-end donations: Initiate your transfer by mid-December. If you wait until December 28, your donation might not complete until January, which means you can't deduct it until next year's taxes.

The IRS counts your donation on the date the charity receives the shares, not the date you initiate the transfer.

Common Problems and Solutions

Problem: The charity doesn't have a brokerage account.

Solution: Small charities might not have the infrastructure for stock donations. You have two options. First, open a donor-advised fund (covered in Section 7) and donate your stock there, then grant cash to the charity. Second, sell the stock yourself, pay the capital gains tax, and donate cash. The first option is better if your donation is large enough to justify the setup.

Problem: Your transfer is delayed or missing.

Solution: Contact your brokerage's transfer department. Have the charity's account information and your transfer confirmation number ready. Most delays happen because of incorrect account details or missing information.

Problem: You want to donate fractional shares.

Solution: Most brokerages only transfer whole shares. If you own 150.5 shares and want to donate them all, you'll need to donate 150 shares and sell the 0.5 shares separately. Or round up and donate 151 shares if you own enough.

Problem: The stock price drops between when you initiate the transfer and when it completes.

Solution: This is just bad timing. Your deduction is based on the stock price when the charity receives the shares, not when you started the transfer. If you're worried about price volatility, initiate the transfer when you're comfortable with the current price.

Now that you know how to execute the transfer, let's talk about what your tax preparer needs from you to claim your deduction properly.

What Your Tax Preparer Needs (And What Forms You'll File)

Think of your stock donation paperwork like building a tax defense file. You're creating proof that you donated what you say you donated, when you say you donated it, and what it was worth at that moment.

The good news? For most people donating publicly traded stock, the paperwork is straightforward.

The Basic Documentation (Everyone Needs This)

Every stock donation requires a written acknowledgment from the charity. This letter must show:

- The date they received your stock

- A description of what you donated (like "100 shares of Apple stock")

- A statement that you received no goods or services in return

You also need your brokerage statement showing the transfer and the stock's value on the transfer date.

When You Need IRS Form 8283

The IRS requires different levels of documentation based on how much you donate:

Under $500: Just keep the charity's acknowledgment letter. Your tax preparer includes the deduction on Schedule A, no special forms needed.

$500 to $5,000: Your tax preparer files Form 8283 Section A with your tax return. This is a simple form listing what you donated and its value.

Over $5,000: Your tax preparer files Form 8283 Section B. This requires more detail, including your original cost basis and when you bought the stock.

The Appraisal Question

Here's where it gets easier for most people. If you donate publicly traded stock (like shares of Microsoft, Amazon, or any company on a major stock exchange), you never need an appraisal. The stock price on the transfer date is your proof of value, no matter how much you donate.

Appraisals only matter for non-publicly traded stock worth over $5,000. That's private company shares, which most people don't have.

Real Example: Sarah's $15,000 Donation

Sarah donates $15,000 of publicly traded stock to her local food bank in November. Here's what she keeps in her tax defense file:

- The charity's acknowledgment letter stating they received 50 shares of Tesla stock on November 20

- Her brokerage statement showing the transfer and that those shares were worth $15,000 on November 20

- Her original purchase records showing she bought the shares for $6,000 two years ago

In April, she gives these three documents to her tax preparer. He files Form 8283 Section B with her return because the donation exceeded $5,000. No appraisal needed because Tesla is publicly traded.

Your Tax Preparer Checklist

Hand your tax preparer this complete package:

- Charity acknowledgment letter (showing date and description)

- Brokerage statement (showing transfer and value on transfer date)

- Purchase records (showing your original cost basis and purchase date)

- Any correspondence about the donation (emails confirming the transfer)

Keep copies of everything for at least three years. The IRS can audit returns within three years of filing, and you'll want that tax defense file ready.

One Important Timing Note

The charity's acknowledgment letter must be dated before you file your tax return. If you donate stock in December but don't get the letter until February, that's fine. Just make sure you have it before your tax preparer files in April.

Most charities send acknowledgment letters within a few weeks. If you haven't received yours within 30 days, follow up. You can't claim the deduction without it.

Now that you know what paperwork to expect, let's look at special situations. What if you want to donate shares from your employee stock purchase plan or incentive stock options? Those require extra attention.

Special Situations: ESPP Shares, ISOs, and Other Equity Compensation

Different types of stock have different tax rules when donated. Think of it like different types of tickets at an arcade. Some you can cash in immediately, others have waiting periods, and some have special restrictions. Your equity compensation works the same way.

ESPP Shares: Watch Out for Disqualifying Dispositions

ESPP shares come with a catch. To get favorable tax treatment, you need to hold them for 2 years from the offering date AND 1 year from the purchase date. Donate before meeting both requirements, and you trigger what's called a "disqualifying disposition."

Here's what that means in practice:

Mike's ESPP Example: Mike bought ESPP shares at a 15% discount. He paid $8,500 for shares worth $10,000. To get favorable tax treatment, he needs to hold them 2 years from offering date and 1 year from purchase.

If he donates the shares before meeting these requirements, he'll owe ordinary income tax on the $1,500 discount, even though he donated the shares. He loses the tax benefit he was hoping for.

Better options for Mike:

- Wait until the holding period is met, then donate

- Donate other stock instead

- Donate cash and keep the ESPP shares

ISO Shares: The AMT Problem

Donating ISO shares doesn't eliminate your AMT (Alternative Minimum Tax) liability. The AMT calculates based on the spread when you exercised, not when you donated.

Best practice: Exercise your ISOs and hold them for at least one year. Then donate them. This way, you avoid AMT issues and get the full charitable deduction.

RSU Shares: Simple, But Timing Matters

RSUs are straightforward. Once they've been vested for over a year, you can donate them freely with no special tax complications.

Wait for long-term status: If your RSUs vested 6 months ago, wait another 6 months before donating. This ensures you get the full fair market value deduction.

NSO Shares: No Special Rules

Non-qualified stock options follow the same rules as regular stock. Once you've held the shares for over a year after exercising, you're good to go.

Decision Matrix

| Equity Type | Can Donate Immediately After Vesting/Purchase? | Special Considerations |

|---|---|---|

| ESPP | No | Wait for 2-year + 1-year holding periods |

| ISO | Not recommended | Exercise and hold 1 year first to avoid AMT |

| RSU | Yes, but wait 1 year | Need long-term capital gains status |

| NSO | Yes, after 1 year | Same as regular stock |

Bottom line: With equity compensation, timing is everything. Donate too early, and you might trigger taxes you were trying to avoid. When in doubt, wait for the full holding period.

Now let's look at situations where donating stock might actually be the wrong move.

When Donating Stock Is the Wrong Move

Donating appreciated stock is like having a powerful tool in your toolbox. But sometimes you need a different tool entirely.

Here are five situations where donating stock actually costs you money.

Your Stock Has Losses

This is the biggest mistake people make.

Example: Jessica bought stock for $20,000 that's now worth $15,000. She lost $5,000.

If she donates the stock directly:

- She gets a $15,000 charitable deduction

- At 24% tax rate, that saves $3,600

- But she loses the $5,000 capital loss forever

Better move:

- Sell the stock and claim the $5,000 capital loss (saves $1,190 at 23.8% capital gains rate)

- Donate the $15,000 cash (saves $3,600 at 24% rate)

- Total tax benefit: $4,790 instead of $3,600

Think of it like this: you can't use a coupon after you've already paid. Claim your loss first, then donate.

You've Held the Stock Less Than One Year

Short-term holdings get no special treatment. You can only deduct your cost basis, not the current value.

If you bought stock for $10,000 six months ago and it's now worth $12,000, you only deduct $10,000. You might as well donate cash.

You Don't Itemize Your Deductions

If you take the standard deduction ($14,600 single, $29,200 married in 2024), charitable donations don't reduce your taxes at all.

Donating stock just adds paperwork with zero benefit. Donate cash if you want to give.

The Stock Is Still Growing Fast

You bought stock at $50 that's now $200. But you think it's heading to $500 in two years.

Donating now means you miss that future growth. Sometimes the best move is to hold the stock and donate cash instead. Or donate different shares you're less excited about.

You Need to Rebalance Anyway

If your portfolio is out of whack and you planned to sell shares anyway, donating doesn't add much value. You were going to pay the capital gains tax as part of rebalancing.

Exception: if you have multiple lots, donate the highest-basis shares and sell the lowest-basis ones.

The Gain Is Too Small

Donating $2,000 of stock with a $500 gain saves you maybe $119 in taxes. Is the paperwork and transfer process worth two hours of your time?

For small amounts, just write a check.

Simple decision rule: If your stock has losses, you've held it less than a year, or you don't itemize, donate cash instead. If you love the stock's future or the gain is tiny, donate cash. Otherwise, stock donations usually win.

Now let's pull everything together with a clear action plan based on your specific situation.

Your Action Plan: Next Steps Based on Your Situation

Think of this like creating your personal game plan. Different situations need different plays.

If You Have Appreciated Stock and Donate Regularly

Your next steps:

- Review your portfolio this week for stocks you've held over 1 year that have gained value

- Calculate your potential tax savings (use the example from Section 2: donate $10,000 in stock, save $3,700 in taxes)

- Contact your favorite charities and ask for their brokerage transfer instructions

- Initiate the transfer at least two weeks before you need it completed

Reality check: If you donate $5,000+ per year and have any stock gains, you're probably leaving money on the table by donating cash instead.

If You're Facing a High-Income Year

Maybe you sold a business, exercised ISOs, or got a big RSU vest. You need a bigger tax strategy.

Your next steps:

- Calculate your expected AGI for this year

- Open a donor-advised fund (DAF) account this month

- Transfer appreciated stock up to 30% of your AGI into the DAF

- Take the full deduction this year, then distribute to charities over the next 5-10 years

Think of a DAF as your charitable savings account. You get the tax break now but can spread out the actual donations.

If You're Not Sure This Applies to You

Run this quick checklist:

- Do I donate $1,000+ per year to charity?

- Do I have stock, mutual funds, or RSUs worth more than when I got them?

- Have I held these investments for over 1 year?

- Am I in the 22% tax bracket or higher (single: $47,000+, married: $94,000+)?

If you checked three or more boxes, donating stock probably saves you money.

Year-End Donation Timeline

November 1-15:

- Review your portfolio for appreciated stock held over 1 year

- Calculate potential tax savings

- Decide between direct donation and DAF

November 15-30:

- Contact charities for brokerage information

- Gather your cost basis records (purchase date and price)

December 1-15:

- Initiate stock transfers (don't wait until the last week)

- Stock transfers take 3-7 business days, sometimes longer during holidays

December 15-31:

- Confirm transfers completed

- Get acknowledgment letters from charities

January-February:

- Organize documentation for your tax preparer

- File Form 8283 if you donated over $5,000 in stock

If you're reading this in March thinking "I should have done this": Don't worry. Start planning now for next year's donations. Set a calendar reminder for November 1.

When to Consult Professionals

Talk to a tax professional if:

- You're donating stock worth over $50,000

- You have complex equity compensation (ISOs, ESPP, restricted stock)

- Your donation exceeds 30% of your AGI

- You're in AMT territory

Talk to a financial advisor if:

- You're not sure which appreciated stock to donate

- You need help setting up a DAF

- You want to create a multi-year donation strategy

Think of professionals like having a coach. You can learn the basics yourself, but a coach helps you execute a winning strategy.

The Bottom Line

Donating appreciated stock isn't just for wealthy people with million-dollar portfolios. If you have $5,000 in stock that's doubled in value and you donate $2,500 per year, you could save $500+ in taxes. That's real money.

The mechanics are simple: check your holding period, get the charity's brokerage info, initiate the transfer. The hardest part is just getting started.

Your move: Open your brokerage account right now. Look for stocks or funds you've held over a year that show gains. That's your donation fund. Next time you write a charity check, donate that stock instead.

You'll give more to causes you care about. You'll pay less in taxes. And you'll wonder why you didn't do this years ago.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

ESPP Tax Rules: A Simple Guide to What You'll Owe (With Examples)

ESPP taxes confuse even smart employees because the rules change based on how long you hold your shares. This guide walks you through the two types of sales (qualifying vs. disqualifying), shows you exactly what you'll owe with real examples, and helps you avoid the most common costly mistakes.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

ESPPHow ESPP Works: Your Complete Guide to Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) lets you buy your company's stock at a discount, usually 10-15% off. This guide explains how ESPP works from enrollment through selling shares, including the tax rules that determine how much money you keep. You'll learn the exact steps, see real dollar examples, and discover strategies competitors don't share.

Not sure what to do with your equity?

Get a free personalized analysis