Free equity analysis

Complete guide to understanding your Morgan Stanley equity compensation, including RSU, ISO, NSO, ESPP, vesting schedules, and tax strategies.

Employees

88.9K

Worldwide

Equity Programs

4

programs

Vesting Period

3 years

RSU vesting

Morgan Stanley offers 4 equity compensation programs to employees. Click on each program to learn more about eligibility, vesting, and tax implications.

Standard RSU program with 4-year vesting and 1-year cliff. Annual refresh grants available for eligible employees.

Learn about Morgan Stanley's Incentive Stock Options program, including vesting schedules and tax treatment.

Learn about Morgan Stanley's Non-Qualified Stock Options program, including vesting schedules and tax treatment.

Learn about Morgan Stanley's Employee Stock Purchase Plan program, including vesting schedules and tax treatment.

Morgan Stanley offers a comprehensive equity compensation package designed to align employee interests with the firm's long-term success. As a major financial services institution, the company provides multiple equity vehicles including Restricted Stock Units (RSUs), Performance Stock Units (PSUs), Restricted Stock Awards (RSAs), stock options (both Incentive Stock Options and Non-Qualified Stock Options), and an Employee Stock Purchase Plan (ESPP).

Equity compensation represents a significant component of total compensation at Morgan Stanley, particularly as you advance in your career. These awards give you direct ownership in the company's stock, allowing you to benefit from the firm's financial performance and market valuation. As a publicly traded financial services leader, Morgan Stanley's stock (ticker: MS) provides employees with exposure to the company's growth trajectory.

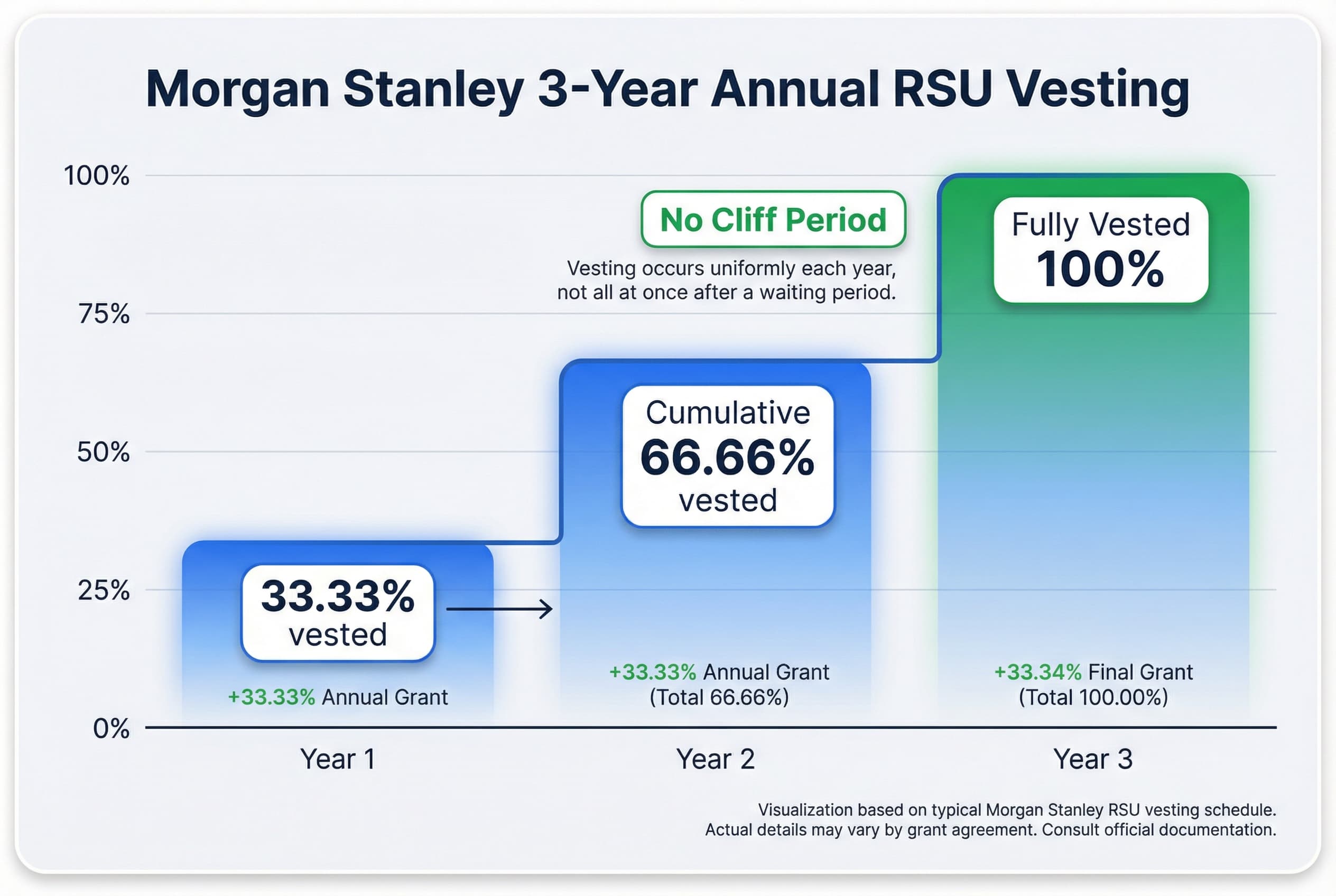

For RSU grants, Morgan Stanley typically uses a three-year uniform vesting schedule, with one-third of your award vesting on each anniversary of the grant date. This annual vesting structure means you'll receive roughly 33% of your shares each year over three years, encouraging long-term retention while providing regular liquidity events.

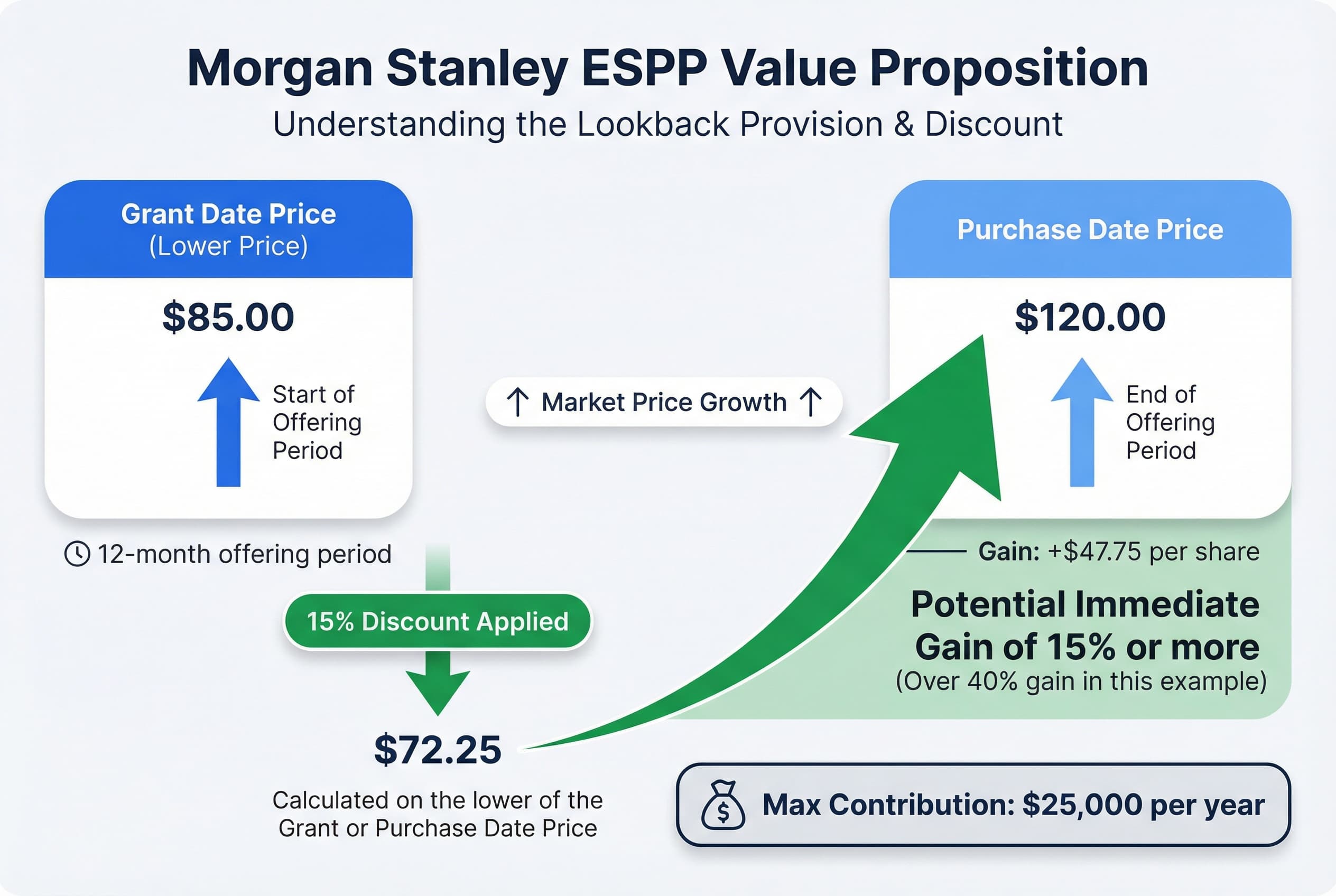

The ESPP offers a compelling opportunity to purchase company stock at a 15% discount with a lookback feature and a 12-month offering period. Contributions are capped at $25,000 annually, allowing you to build equity ownership through regular payroll deductions.

Understanding these programs is essential for maximizing your total compensation and building long-term wealth at Morgan Stanley.

Morgan Stanley typically grants Restricted Stock Units (RSUs) with a three-year vesting schedule. Unlike many technology companies that use four-year schedules, Morgan Stanley's equity awards vest over a shorter timeframe, which is common in the financial services industry.

Your RSU grant follows a uniform vesting pattern, meaning shares vest in equal installments throughout the vesting period. Specifically, one-third of your total grant vests on each anniversary of your grant date:

Shares vest annually on the anniversary of your grant date, not monthly or quarterly. This means you'll receive your vested shares once per year until the grant is fully vested.

Morgan Stanley's standard RSU vesting schedule does not include a cliff period. A cliff would require you to remain employed for a minimum period (commonly one year) before any shares vest. Instead, you'll receive your first vesting installment on your first anniversary, assuming you remain employed with the company.

This is an important distinction: you begin earning equity immediately, but you must wait a full year to receive the first portion of your grant. If you leave Morgan Stanley before your first anniversary, you would forfeit the entire unvested grant.

The uniform vesting structure means you receive equal value each year throughout the three-year period. This differs from "backloaded" schedules where more shares vest in later years, or "frontloaded" schedules that accelerate vesting upfront. With Morgan Stanley's approach, your equity compensation is distributed evenly, providing consistent annual value as long as you remain with the firm.

Remember that when your RSUs vest, they're treated as ordinary income for tax purposes. Morgan Stanley typically withholds 22% for federal taxes by default, though you can adjust this rate. Depending on your total compensation and tax bracket, this standard withholding may be insufficient to cover your full tax liability.

Morgan Stanley offers an Employee Stock Purchase Plan that provides employees with an attractive opportunity to purchase company stock at a discount. The plan features a 15% discount on the stock price, allowing you to buy Morgan Stanley shares at 85% of their fair market value.

The ESPP includes a lookback provision, which significantly enhances the plan's potential value. With this feature, your purchase price is based on the lower of two prices: the stock price at the beginning of the offering period or the price at the end of the offering period when shares are purchased. This means if the stock price rises during the 12-month offering period, you benefit from purchasing at the lower starting price with the 15% discount applied.

The plan operates on a 12-month offering period. You can contribute up to $25,000 per year to the ESPP, allowing you to maximize your discounted stock purchases within IRS limits.

The combination of the 15% discount and lookback provision can generate substantial returns. For example, if Morgan Stanley's stock price increases during the offering period, you could purchase shares at 85% of the lower beginning price - potentially resulting in an immediate gain of 15% or more, depending on stock performance.

Understanding the tax implications of your ESPP shares is important. A qualifying disposition occurs when you sell shares more than one year after the purchase date AND more than two years after the offering period began. Qualifying dispositions receive more favorable long-term capital gains treatment. Sales that don't meet both criteria are disqualifying dispositions and result in ordinary income recognition for the discount amount.

The ESPP represents a valuable benefit that can complement your overall compensation package at Morgan Stanley.

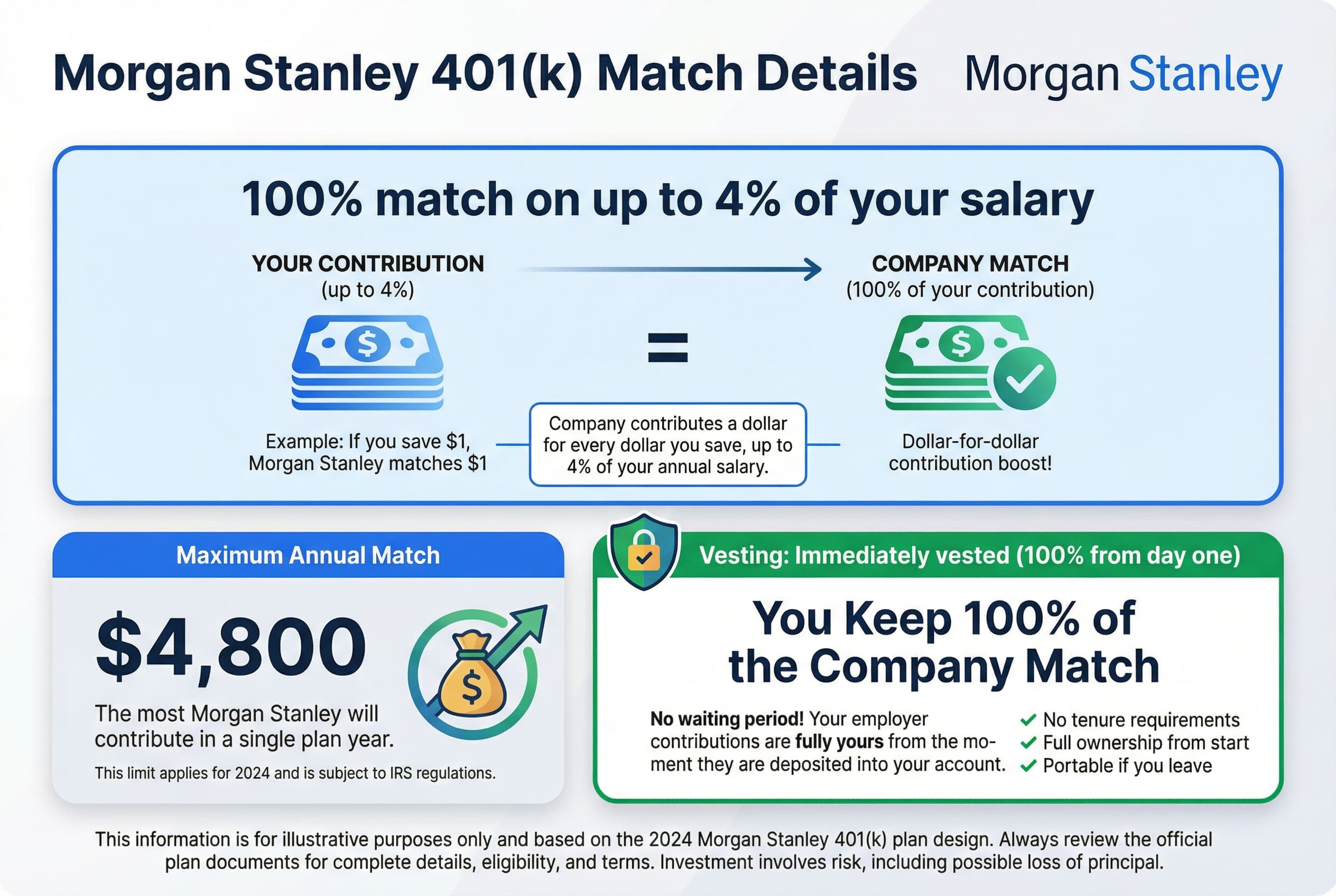

Morgan Stanley offers a competitive 401(k) plan with an attractive employer match to help you build retirement savings alongside your equity compensation.

Morgan Stanley provides a 100% match on up to 4% of your salary, with a maximum annual match of $4,800. This means if you contribute at least 4% of your gross pay, the company will match that contribution dollar-for-dollar up to the cap. This is one of the more generous matching formulas in the financial services industry.

The employer match is immediately vested, meaning you own 100% of the company contributions from day one. This is a significant advantage if you're considering a job change, as you won't forfeit any matched funds regardless of your tenure.

Morgan Stanley offers both traditional pre-tax and Roth 401(k) contributions, giving you flexibility in your tax planning strategy. The plan also supports after-tax contributions, which can be valuable for high earners who've maxed out their standard 401(k) limits.

Note that contribution percentages are calculated based on your gross (before-tax) pay, so plan accordingly when setting your deferral rate.

While after-tax contributions are available, information about mega backdoor Roth conversion capabilities and brokerage window options wasn't specified in the available plan details. Contact HR or your 401(k) plan administrator to confirm whether these features are available to you.

Understanding the tax treatment of your equity compensation is essential for effective financial planning. Different equity awards trigger taxes at different times and rates.

RSUs and PSUs: You owe taxes at vesting, when shares are delivered to you. This is treated as ordinary income, just like your salary. Morgan Stanley withholds taxes at a default rate of 22%, which you can adjust if needed.

Stock Options (ISOs and NSOs): NSOs trigger ordinary income tax when you exercise. ISOs receive preferential treatment - no ordinary income tax at exercise (though AMT may apply), with taxes deferred until you sell the shares.

ESPP: Tax treatment depends on how long you hold the shares. For a qualifying disposition (holding more than one year after purchase AND more than two years after the offering date), you'll pay ordinary income tax on the discount and capital gains on any additional profit. Disqualifying dispositions are taxed less favorably.

A common issue with the 22% default withholding rate: if your marginal tax rate is higher (which it likely is for many Morgan Stanley employees), you'll owe additional taxes when filing your return. Consider increasing your withholding rate or setting aside cash to cover the shortfall.

Income from vesting RSUs and exercising NSOs is taxed as ordinary income at your marginal rate. However, if you hold shares after they vest or after exercising options, any subsequent appreciation is taxed as capital gains - long-term rates apply if you hold for more than one year, which are typically lower than ordinary income rates.

Exercising ISOs may trigger Alternative Minimum Tax, even though you don't owe regular income tax at exercise. The spread between the exercise price and fair market value counts as an AMT preference item, potentially creating a significant tax liability.

Morgan Stanley is headquartered in New York, which has high state and local income taxes. If you work in New York, you'll face additional state and city taxes on your equity compensation income.

Disclaimer: This information is educational only and not tax advice. Equity compensation taxation is complex and depends on your individual circumstances. Consult a qualified tax professional for personalized guidance.

While Morgan Stanley equity compensation can be valuable, concentrating too much of your wealth in a single stock - even your employer's - creates significant financial risk. If Morgan Stanley's stock price declines, you could face a double impact: reduced portfolio value and potential job insecurity during the same downturn.

As a financial services company, Morgan Stanley faces specific risks that could affect your equity value:

Financial advisors commonly recommend limiting single-stock exposure to 10-20% of your total net worth. This becomes especially important when your income and equity are tied to the same company. Consider your complete Morgan Stanley exposure: RSUs, ESPP shares, stock options, and any PSUs or RSAs you hold.

Develop a diversification strategy as your equity vests. You might sell a portion of vested shares systematically or use 10b5-1 trading plans to automate sales during compliant periods, helping you build a balanced portfolio across different sectors and asset classes.

As your RSUs vest annually over three years (one-third each anniversary), each vesting event creates a decision point. Consider selling some or all vested shares if Morgan Stanley stock represents more than 10-15% of your total investment portfolio. This is particularly important for financial services employees, as your career success is already tied to the industry's performance.

Working in financial services means both your salary and equity are concentrated in a single sector. When RSUs vest, you're not "leaving money on the table" by selling - you've already earned the compensation. Diversifying into other sectors, asset classes, or index funds reduces risk without sacrificing the value you've earned.

Morgan Stanley's ESPP offers a 15% discount with a lookback provision, capped at $25,000 in contributions. To achieve a qualifying disposition and receive favorable long-term capital gains treatment, hold shares for more than one year after purchase and more than two years after the offering date. However, evaluate whether the tax savings justify the concentration risk of holding company stock longer.

View your equity grants as part of your total compensation package, not just "bonus" money. RSUs vest with 22% default tax withholding, which may be insufficient if your marginal tax rate is higher. You can adjust withholding or set aside additional funds to avoid surprises at tax time.

Morgan Stanley offers 10b5-1 plans, which allow you to establish predetermined selling schedules. These plans are particularly valuable in financial services, where trading windows may be restricted. A 10b5-1 plan lets you systematically diversify regardless of blackout periods or market timing concerns.

Remember: This is educational information, not personalized financial advice. Consider consulting a financial advisor for your specific situation.

Let's walk through a typical RSU grant to see how vesting works in practice.

Sarah, a Vice President at Morgan Stanley, receives a grant of 300 RSUs as part of her annual compensation. Morgan Stanley uses uniform vesting over three years, with one-third vesting on each anniversary of the grant date.

Year 1 Anniversary:

Year 2 Anniversary:

Year 3 Anniversary:

Over three years, Sarah received 234 shares (78 + 78 + 78) with a current value of $32,760 at the final $140 price. The remaining 66 shares were withheld to cover federal tax obligations totaling $8,690.

Important note: If Sarah's actual marginal tax rate exceeds 22%, she may owe additional taxes when filing her return. Morgan Stanley allows employees to adjust their withholding rate or pay taxes directly from their paycheck to avoid selling shares.

Even experienced financial services professionals can stumble when managing their own equity compensation. Here are key mistakes Morgan Stanley employees should avoid:

The default withholding rate of 22% on RSUs often falls short if you're in a higher tax bracket. Since you can adjust your withholding rate, review your overall tax situation annually to avoid surprise tax bills. This is especially critical for higher earners who may face marginal rates well above the default.

Morgan Stanley's ESPP offers a 15% discount with a lookback provision, yet many employees don't participate. This benefit can generate immediate returns, though remember to plan for the complex tax treatment - especially the distinction between qualifying and disqualifying dispositions based on holding periods.

Holding too much company stock ties your financial future to a single employer. While Morgan Stanley is a major financial institution, diversification remains a fundamental principle. Consider selling vested shares systematically to rebalance your portfolio.

If you receive incentive stock options, exercising them may trigger Alternative Minimum Tax (AMT), even without selling shares. This often-overlooked tax consequence can create unexpected liabilities.

For employees receiving RSAs, failing to file a Section 83(b) election within 30 days means paying taxes on appreciation during vesting rather than at grant. This election isn't available for RSUs, so understand which equity type you hold.

Understanding how your equity compensation is affected when you leave Morgan Stanley is crucial for financial planning around any career transition.

When you leave Morgan Stanley, unvested RSUs are typically forfeited, regardless of whether you resign or are terminated. Since Morgan Stanley RSUs vest uniformly over three years (one-third annually), any shares that haven't reached their vesting anniversary will be lost upon your departure. Your termination date matters significantly - leaving even a day before a vesting anniversary means forfeiting that entire tranche.

Morgan Stanley employees may receive both Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs). However, specific post-termination exercise windows are not publicly documented. You should review your individual grant agreements carefully, as these will specify how long you have to exercise vested options after leaving the company. This window is typically much shorter than the original option expiration date.

If you leave during an active ESPP offering period, your participation will generally end, and accumulated contributions may be returned to you. You won't receive shares for a partial period. Any shares already purchased in previous periods remain yours to hold or sell.

There's typically no difference in equity treatment between voluntary and involuntary termination for standard separations. However, specific circumstances like retirement, disability, or executive-level agreements may have different rules. Always consult your grant documents and HR before making departure decisions.

Morgan Stanley offers a non-qualified deferred compensation (NQDC) plan, sometimes referred to as Executive Services, available to employees at the Director level and above.

The deferred compensation program allows eligible employees to defer a portion of their current income to a future date, typically retirement or separation from the company. This gives you greater control over the timing of your taxable income and potential tax planning opportunities.

Benefits:

Risks:

Before participating, consider your current and expected future tax rates, your confidence in the company's long-term financial stability, and your overall retirement savings strategy. Consult with a tax advisor to understand how deferral fits into your comprehensive financial plan, especially given the irrevocable nature of most deferral elections.

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Helpful videos explaining Morgan Stanley equity compensation, vesting, and tax strategies.

Stop Paying Double Tax on Your RSUs (Common 1099-B Mistake) | McCarthy Tax Preparation

RSU Tax Tips: Avoid Double Taxation

RSUs at Morgan Stanley typically vest uniformly over three years, with one-third vesting on each anniversary of your grant date. This means you'll receive 33.33% after year one, 33.33% after year two, and the final 33.34% after year three. There is no initial cliff period, so you'll start receiving shares after your first anniversary.

Morgan Stanley withholds at a default rate of 22% for federal taxes when your RSUs vest, and you can adjust this rate if needed. However, if your actual marginal tax rate is higher than 22%, the standard withholding may be insufficient and you could owe additional taxes at year-end. You can cover the tax withholding through share surrender or direct payment from your paycheck.

Morgan Stanley's ESPP offers a 15% discount on stock purchases with a lookback provision over a 12-month offering period. You can contribute up to $25,000 per year to the plan. The lookback feature means you'll purchase shares at 85% of the lower price between the offering date and purchase date, maximizing your potential discount.

To achieve a qualifying disposition for your ESPP shares at Morgan Stanley, you must hold the shares for more than one year after the purchase date AND more than two years after the offering date. Meeting both requirements allows you to receive more favorable long-term capital gains tax treatment on a portion of your gain.

Morgan Stanley offers limited tax deferral options depending on the equity type and your level. Section 83(i) election may allow you to defer federal income taxes on RSUs or PSUs in certain circumstances. Additionally, if you're at Director level or above, you may be eligible for the non-qualified deferred compensation (NQDC) plan, sometimes called Executive Services.

Generally, unvested RSUs are forfeited when you leave the company, though specific terms depend on your grant agreement and reason for departure. Since RSUs vest annually over three years at Morgan Stanley, any shares that haven't reached their vesting anniversary will typically be lost upon termination. Review your specific equity award documents for details about your grants.

Yes, Morgan Stanley offers both Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) as part of its equity compensation program. However, be aware that exercising ISOs may trigger Alternative Minimum Tax (AMT), which is a common concern for employees. Consult with a tax advisor to understand the implications before exercising.

Yes, Morgan Stanley makes 10b5-1 trading plans available to employees. These pre-arranged trading plans allow you to sell shares on a predetermined schedule, which can help you diversify your holdings and avoid concerns about trading during blackout periods or while in possession of material non-public information.

Get a free personalized analysis from our equity compensation experts