What Are RSUs? A Complete Guide to Restricted Stock Units

How restricted stock units work, when you get taxed, and what to do with them

Published March 14, 2026 · Updated March 14, 2026

Restricted Stock Units (RSUs) are a type of stock compensation where your company promises to give you shares after you meet certain conditions, usually working there for a set period. Unlike stock options, RSUs always have value as long as the company's stock has value. This guide explains how RSUs work, when you'll owe taxes, and how to make the most of this benefit.

Your Job Offer Includes RSUs - Now What?

Sarah just got a job offer at a tech company. The salary is $120,000, plus something called "10,000 RSUs vesting over 4 years." She has no idea if that's good or what it even means.

If you're reading this, you're probably like Sarah. Your offer letter includes RSUs, and you're wondering what you just signed up for.

Here's the quick version: RSUs are company stock you earn over time, like a loyalty bonus that unlocks in chunks. Think of it as your employer saying "we'll give you shares of our company, but only if you stick around."

The potential value is real. If Sarah's company stock trades at $50 per share today, those 10,000 RSUs could be worth $500,000 total. That's not a typo. Over four years, she could earn an extra $125,000 per year on top of her salary.

But here's the catch: most people don't understand how RSUs actually work. They don't know when they get the shares, how much they'll pay in taxes, or what happens if they leave the company. This confusion costs employees thousands of dollars every year.

This guide will help you:

- Understand exactly what RSUs are and when you get them

- Calculate how much you'll actually take home after taxes

- Make smart decisions when your RSUs vest

- Avoid expensive mistakes that could cost you tens of thousands

Let's start with the basics: what exactly are these RSUs, and how do they turn into real money in your pocket?

RSUs Explained: A Promise of Future Stock

RSU stands for Restricted Stock Unit. Think of it like a gift card your company gives you, but you can't use it until specific dates in the future. When those dates arrive, the gift card turns into real stock you own.

Here's what you need to know: When your company grants you RSUs, you don't own any stock yet. It's a promise. The company is saying "we'll give you this stock later if you stick around."

The "restricted" part means you must meet certain conditions before you actually get the stock. For most people, that condition is simple: stay employed. Work at the company for a set period of time, and the RSUs convert into real shares.

From Promise to Ownership

Let's make this concrete with an example:

January 1, 2024: Your company grants you 1,000 RSUs when the stock price is $50. You don't own any stock yet. You can't sell anything. This is just a promise.

January 1, 2025: 250 of your RSUs vest. Now you own 250 real shares of company stock. If the stock price is now $60, those shares are worth $15,000 ($60 x 250 shares). You could sell them today if you wanted.

Why RSUs Always Have Value

Here's a big difference between RSUs and other equity compensation: RSUs are always worth something as long as the stock has value. If your company's stock is trading at $60, your vested RSUs are worth $60 per share. Period.

Even if the stock drops to $30, your RSUs are still worth $30 per share. They might be worth less than you hoped, but they're never worthless.

Now that you understand what RSUs are, let's talk about how you actually earn them over time.

What Are Restricted Stock Units (RSUs)? | Simple Guide to Equity Compensation 💰📊

How RSU Vesting Works: Earning Your Stock Over Time

Vesting means earning the right to own your stock. When your company grants you RSUs, you don't own them yet. You have to earn them by staying at the company for a set period of time.

Think of vesting like a coffee shop loyalty card. You don't get your free drink on day one. You have to buy 10 coffees first. With RSUs, you don't get your shares on day one. You have to work there for months or years first.

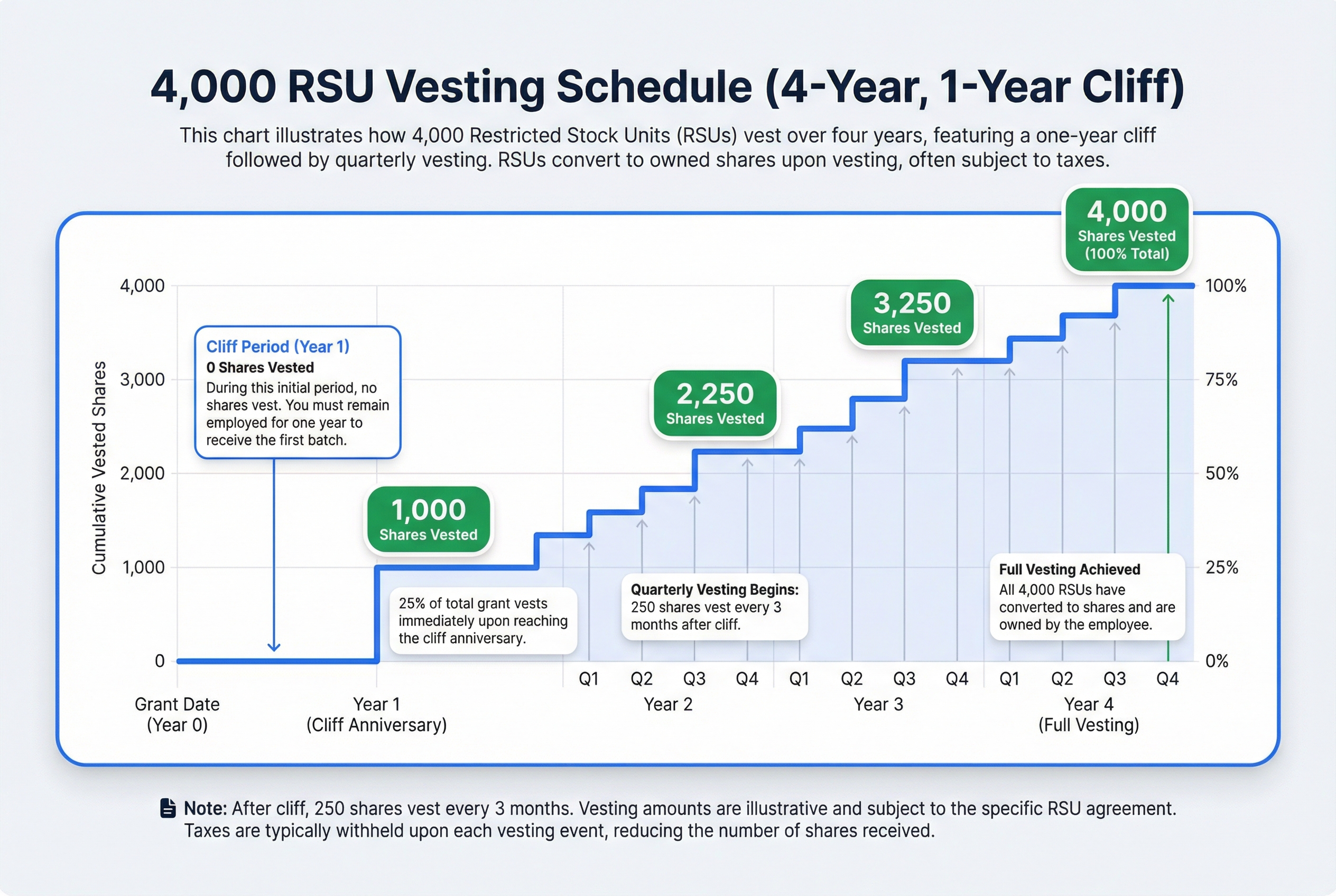

The Most Common Schedule: 4 Years with a 1-Year Cliff

Here's how most tech companies structure RSU vesting:

Total vesting period: 4 years

Cliff period: 1 year (you get nothing if you leave before this)

After the cliff: Shares vest quarterly (every 3 months)

Let's see this in action:

You receive 4,000 RSUs with a 4-year vesting schedule and 1-year cliff.

- Year 1: 0 shares vest. You're waiting for the cliff.

- On your 1-year anniversary: 1,000 shares vest all at once. This is the cliff.

- Years 2-4: 250 shares vest every quarter (every 3 months).

- If you leave after 18 months: You keep the 1,000 from year 1 plus 500 from year 2. You lose the remaining 2,500 unvested RSUs. They disappear.

If the stock price is $150 when you leave, you walk away with $225,000 worth of stock (1,500 shares × $150). The other $375,000 (2,500 shares × $150) evaporates because you didn't stay long enough to earn it.

Understanding the Cliff

A cliff is a waiting period where nothing vests. Then, boom, a big chunk vests all at once.

Why do companies use cliffs? They want to make sure you're committed. If you leave after 11 months, you get zero shares. If you stay one more month, you get 25% of your grant. It's designed to keep you from job hopping.

Other Vesting Schedules You Might See

Not every company uses the 4-year cliff model. Here are other common patterns:

Monthly vesting (no cliff):

You receive 1,200 RSUs vesting monthly over 4 years. That's 25 shares every single month for 48 months. If you leave after 6 months, you keep 150 shares and lose 1,050.

Quarterly vesting (no cliff):

You receive 800 RSUs vesting quarterly over 4 years. That's 50 shares every 3 months for 16 quarters. More common at financial companies than tech companies.

Annual vesting:

You receive 2,000 RSUs vesting 500 shares per year on your anniversary. Rare for new grants, but sometimes used for retention bonuses.

What Actually Triggers Vesting?

Vesting happens on specific calendar dates, not when you hit milestones.

Your grant agreement says something like "25% of shares vest on March 15, 2025, then 1/16th of the total grant vests quarterly thereafter." Mark these dates on your calendar. Some companies send reminders. Many don't.

You must be employed on the vesting date to receive those shares. If you quit or get fired the day before a vesting date, you lose those shares. If you're employed on the vesting date but give two weeks notice the next day, you keep those shares.

The Golden Handcuffs Effect

RSUs are designed to make leaving expensive.

Imagine you have $200,000 in unvested RSUs. Quitting means walking away from that money. A recruiter offers you a new job with a $20,000 raise. Sounds great, except you're leaving $200,000 on the table.

This is intentional. Your company wants you to think twice (or ten times) before leaving. The closer you get to a vesting date, the harder it is to walk away. That's why they're called golden handcuffs.

You Can Have Multiple Grants Vesting at Once

Most people don't just have one RSU grant. You might get:

- Your initial hire grant (4,000 RSUs vesting over 4 years)

- An annual refresh grant in year 2 (1,000 RSUs vesting over 4 years)

- A promotion grant in year 3 (2,000 RSUs vesting over 4 years)

All three grants vest on different schedules. By year 4, you might have shares vesting every month from different grants. This makes the golden handcuffs even tighter. There's always another vesting date around the corner.

What Happens to Unvested RSUs When You Leave

Simple rule: If you haven't vested it, you lose it.

You quit, get fired, or get laid off? Any RSUs that haven't vested yet disappear. They go back to the company. You get nothing for them.

The only shares you keep are the ones that vested before your last day of employment. Those are yours. The company can't take them back.

Exception: Some companies offer severance packages that include accelerated vesting. You might get an extra 3 months of vesting if you're laid off. But this isn't standard. Don't count on it.

Now that you understand when you earn your RSUs, let's talk about the painful part: taxes. You'll get hit twice, and the first hit happens the moment your RSUs vest.

Understanding the 4-year vesting schedule with a 1-year cliff is crucial for maximizing RSU value.

Understanding the 4-year vesting schedule with a 1-year cliff is crucial for maximizing RSU value.

The Two Tax Hits: When You Vest and When You Sell

Here's the painful truth about RSU taxes: you get taxed twice. Once when you receive the shares, and again when you sell them.

Think of it like this: vesting day is like getting a cash bonus. You immediately owe income tax on the full value, just like your regular paycheck. Then, you use that "bonus" to buy stock. When you sell the stock later, any profit or loss gets taxed separately.

Tax Hit #1: Vesting Day (Ordinary Income Tax)

The day your RSUs vest, the IRS treats the full value as salary. If 100 shares vest at $150 each, you just "earned" $15,000 in income. You owe income tax on every dollar.

Your company automatically withholds taxes from your vesting, usually around 22% for federal taxes. But here's the problem: 22% might not be enough.

If you're in a higher tax bracket (like 24%, 32%, or 35%), you'll owe the difference at tax time. Many people get surprised by a big tax bill in April because their company didn't withhold enough.

Here's how the math works:

You have 1,000 RSUs that vest when your stock hits $100 per share.

- Taxable income: 1,000 shares x $100 = $100,000

- Company withholds: 22% federal = $22,000

- But you're in the 32% tax bracket

- What you actually owe: 32% of $100,000 = $32,000

- Shortfall at tax time: $32,000 minus $22,000 = $10,000 you still owe

Your company reports this $100,000 on your W-2, just like your salary. State taxes apply too (we'll skip those details here, but they add another layer).

Tax Hit #2: When You Sell (Capital Gains or Losses)

Now you own 1,000 shares. When you sell them, any price change creates a capital gain or loss.

Let's say six months after vesting, you sell all your shares at $120 each. That's $120,000 total.

- Sale price: $120,000

- Your cost basis: $100,000 (the value on vesting day)

- Capital gain: $20,000

Because you held the shares less than one year after vesting, this is a short-term capital gain. Short-term gains get taxed at your ordinary income rate. In our example, that's 32%.

- Tax on the $20,000 gain: 32% = $6,400

Your total tax bill: $32,000 (from vesting) + $6,400 (from selling) = $38,400 in taxes on your $120,000.

The One-Year Rule: Long-Term vs. Short-Term

Hold your shares for more than one year after vesting? You qualify for long-term capital gains rates. These are much lower: 0%, 15%, or 20% depending on your income. Most people pay 15%.

In our example, if you waited 13 months to sell, that $20,000 gain would be taxed at 15% instead of 32%. You'd pay $3,000 instead of $6,400. That's $3,400 in savings just for waiting.

Of course, the stock price could drop while you wait. There's always a tradeoff between tax savings and market risk.

Now that you understand the tax hits, let's look at how your company handles the first tax bill through something called "sell-to-cover."

Restricted Stock Units Explained: How Do RSUs Work & Taxes

Sell-to-Cover: How Companies Handle Your Tax Bill

When your RSUs vest, you owe taxes immediately. But most people don't have thousands of dollars sitting around to pay the IRS. That's where sell-to-cover comes in.

Sell-to-cover is like a restaurant automatically adding an 18% tip to your bill. It's convenient, but it might not be the right amount for your situation.

How Sell-to-Cover Works

Here's what happens on vesting day:

- Your company calculates the taxes you owe (usually 22% federal + your state rate)

- They automatically sell enough shares to cover that amount

- They send the cash to the IRS and state tax authority

- You receive whatever shares are left

You never see the shares that get sold. They're gone before they hit your brokerage account.

A Real Example: Where Did My Shares Go?

Let's say 1,000 RSUs vest when your stock is trading at $50 per share.

- Total value: 1,000 shares × $50 = $50,000

- Withholding needed: 25% (22% federal + 3% state) = $12,500

- Shares sold: 250 shares × $50 = $12,500

- Shares you receive: 750 shares (worth $37,500)

You expected 1,000 shares. You got 750. The other 250 were sold to pay your taxes.

The Problem: Withholding Usually Isn't Enough

Here's the kicker. That 22% federal withholding? It's just an estimate.

If you earn $150,000 and your RSUs push you into the 35% tax bracket, you actually owe 35% in federal taxes. Using our example above, you'd owe $17,500 total, but only $12,500 was withheld.

You'll owe another $5,000 when you file your tax return.

Your Other Options

You don't have to use sell-to-cover. Most companies let you:

Pay taxes from your bank account: Transfer cash to your employer before vesting day. You keep all 1,000 shares. This works if you have the cash available and want to hold the stock.

Same-day sale: Sell all the shares immediately and pocket the cash after taxes. Simple and clean.

The shares sold through sell-to-cover are gone forever. Choose wisely, because you can't get them back.

Next, we'll look at the hidden costs that catch most employees off guard.

What Your HR Won't Tell You: The Hidden Costs of RSUs

RSUs are like winning a car on a game show. Exciting at first, until you realize you owe taxes on the full value and need actual cash to pay them.

Your HR team will explain how RSUs work. They'll show you the vesting schedule. But they rarely warn you about the financial surprises that catch people off guard.

Hidden Cost #1: The Tax Withholding Shortfall

Your company withholds 22% for federal taxes when your RSUs vest. Sounds reasonable, right?

Here's the problem: that 22% is just a guess. It's often way too low.

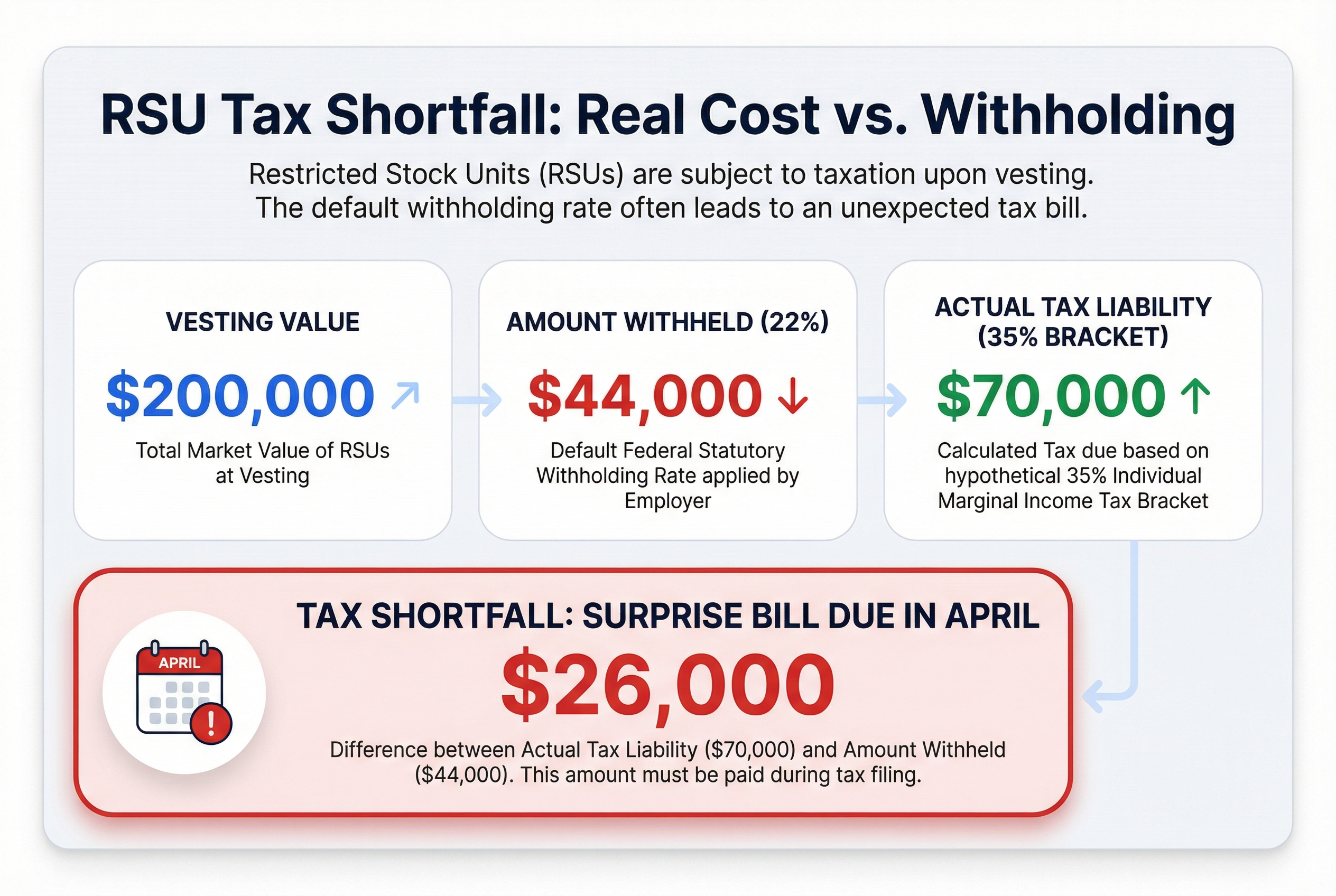

Real example: You have $200,000 of RSUs vesting this year. Your company withholds $44,000 (22%) and you keep $156,000 in stock. But you earn $180,000 in salary, putting you in the 35% tax bracket. You actually owe $70,000 in federal taxes on those RSUs. That's a $26,000 surprise bill when you file your taxes in April.

Thousands of employees get hit with this every year. The bigger your vesting, the bigger the gap.

Hidden Cost #2: Too Many Eggs in One Basket

After that $200,000 vesting, you now own $156,000 of your company's stock. Add your other RSUs and maybe 80% of your savings sits in one stock.

This is concentration risk. If your company's stock drops 30%, you lose $47,000. But you still owe that $26,000 tax bill. And you still work there, so a stock crash might come with layoffs too.

You're betting your savings and your paycheck on the same company. That's risky.

Hidden Cost #3: The Cash Flow Crunch

You need cash to pay that extra $26,000 in taxes. But your RSUs gave you stock, not cash.

Your options: sell some shares to cover it, pull from savings, or scramble to find the money. Many people don't plan for this and end up stressed when tax season arrives.

Hidden Cost #4: Counting Unvested RSUs as 'Yours'

You have 1,000 RSUs granted at $150 per share. That's $150,000, right?

Wrong. Those shares aren't yours until they vest. The stock could drop to $80 by the time you actually get them. Or you might leave the company and forfeit them entirely.

Unvested RSUs are a promise, not a guarantee. Don't spend them in your head before they're real.

What You Can't Do With RSUs

Unlike restricted stock awards (RSAs), you can't file an 83(b) election with RSUs. That's a tax strategy that lets you pay taxes early at a lower value. With RSUs, you're stuck paying taxes at vesting, when the value might be much higher.

The Tax Bracket Bump

Large vesting events can push you into a higher tax bracket for that year. Vest $300,000 of RSUs on top of your $150,000 salary and you're suddenly earning $450,000. Hello, 35% federal bracket (plus state taxes).

Your effective tax rate on those RSUs could hit 40-45% total when you add everything up.

The bottom line: RSUs create real wealth, but they also create real tax bills and real concentration risk. Understanding these hidden costs helps you plan instead of panic.

Now let's compare RSUs to their cousin, stock options, so you understand what makes each one different.

The standard 22% federal withholding often results in a significant tax bill due at filing time.

The standard 22% federal withholding often results in a significant tax bill due at filing time.

RSUs vs. Stock Options: What's the Difference?

Your offer letter mentions both RSUs and stock options. They sound similar, but they work completely differently.

Think of it this way: RSUs are like being given a car. You get it for free, but you pay taxes on its value. Stock options are like getting a coupon to buy a car at today's price in the future. You only profit if the car's price goes up.

The Basic Difference

RSUs give you actual stock after you vest. You don't pay anything for it. The company just hands it to you (minus taxes).

Stock options give you the right to buy stock at a set price called the strike price. This price is locked in on your grant date. You have to pay money to actually get the shares.

When They Have Value

RSUs always have value as long as your company's stock is worth something. If the stock is trading at $100, your RSU is worth $100. If it drops to $30, your RSU is worth $30. It's still worth something.

Stock options only have value if the stock price goes up above your strike price. If your strike price is $50 and the stock is at $45, your options are worthless. You wouldn't pay $50 for something you can buy on the open market for $45.

A Real Example

Your company offers you a choice: 1,000 RSUs or 3,000 stock options. The stock trades at $50 today. If you take options, your strike price is $50.

Here's what happens in three scenarios:

Scenario A: Stock goes to $100

- RSUs: Worth

$100,000(1,000 shares × $100) - Options: Worth

$150,000(you buy 3,000 shares at $50, sell at $100 = $50 profit × 3,000)

Scenario B: Stock stays at $50

- RSUs: Worth

$50,000(1,000 shares × $50) - Options: Worth

$0(no point buying at $50 when market price is $50)

Scenario C: Stock drops to $30

- RSUs: Worth

$30,000(1,000 shares × $30) - Options: Worth

$0(you won't pay $50 for a $30 stock)

Tax Treatment

RSUs get taxed as regular income when they vest. It's like getting a cash bonus. Your company withholds taxes automatically.

Stock options are more complex. You might pay taxes when you exercise (buy the shares), when you sell, or both. The rules depend on whether you have ISOs or NSOs. (We have a separate guide on this.)

Risk and Reward

RSUs are lower risk, lower reward. You always get something of value. But you don't get the massive upside that options can provide.

Stock options are higher risk, higher reward. If the stock price doesn't go up, you get nothing. But if it doubles or triples, your options can be worth way more than RSUs.

Which Is Better?

There's no universal answer. It depends on your situation.

Choose RSUs if you want:

- Guaranteed value (as long as the company doesn't collapse)

- Simpler taxes

- Less risk

Choose options if you:

- Believe strongly in the company's growth

- Can afford to get nothing if the stock doesn't rise

- Want maximum upside potential

Most large public companies grant RSUs to most employees. Stock options are more common at startups where the potential for growth is huge but uncertain.

If you work at a private company that's not yet public, your RSUs work differently. That's what we'll cover next.

Private Company RSUs: When Double-Trigger Vesting Changes Everything

Private company RSUs work like having a winning lottery ticket, but the lottery drawing hasn't happened yet. You've earned the ticket (first trigger), but you can't cash it until the company goes public or gets acquired (second trigger).

Here's what makes private company RSUs different: They need two separate events before you actually own stock.

The Two Triggers Explained

Trigger #1: Time-based vesting (just like public companies)

- You earn RSUs by staying at the company

- Follow a vesting schedule, usually 4 years

- After each vesting period, you've "vested" your shares

- But you don't actually receive anything yet

Trigger #2: Liquidity event (the big difference)

- Company goes public (IPO)

- Company gets acquired

- Company allows a stock buyback

- Until this happens, you own 0 shares

Think of it like a two-part lock on a safe. Time-based vesting opens the first lock. A liquidity event opens the second lock. You need both before you get what's inside.

A Real Example

You join a startup in 2020 with 10,000 RSUs on a 4-year vesting schedule.

By 2024, you've "vested" all 10,000 RSUs time-wise (trigger #1). But the company is still private. You own 0 shares and owe $0 in taxes.

In 2025, the company goes public at $20/share (trigger #2). You immediately receive 10,000 shares worth $200,000. You owe ordinary income tax on the full $200,000 in 2025. All at once.

The Big Risks

Your shares might never become real. If the company doesn't go public or get acquired, your vested RSUs stay worthless. You worked for years, earned the time-based vesting, but never saw a dollar.

You could face a massive tax bill. When trigger #2 finally hits, all your vested RSUs convert to stock at once. If you vested 10,000 RSUs over 4 years and the company IPOs at $50/share, you owe taxes on $500,000 in one year.

You have zero control over timing. The company decides when (or if) to go public. You might vest everything and wait 5+ years for a liquidity event.

Private company RSUs can create life-changing wealth. But they can also leave you with nothing after years of work. Understanding both triggers helps you plan for either outcome.

Now let's look at what happens to your RSUs when you leave your job, whether at a public or private company.

What Happens to Your RSUs When You Leave Your Job

Here's the hard truth: unvested RSUs disappear the day you leave. Vested RSUs stay yours forever.

Think of unvested RSUs like airline miles you haven't earned yet. If you stop flying with that airline, you don't get the miles you would have earned on future flights. They're gone.

The Basic Rule

Unvested RSUs: You lose them. Doesn't matter if you quit, get fired, or take a better job. If the shares haven't vested yet, they vanish.

Vested RSUs: You keep them. They're real shares sitting in your brokerage account. The company can't take them back.

Timing Is Everything

Leaving one day before your vesting date costs you real money.

Example: You have 4,000 RSUs at a company where shares trade at $50. Right now, 2,000 have vested (worth $100,000) and 2,000 are unvested.

You get a job offer. Here's what happens:

- Leave today: Keep 2,000 vested shares ($100,000). Lose 2,000 unvested shares ($100,000).

- Wait 3 months until next vesting: 500 more shares vest. Now you keep 2,500 shares ($125,000) and lose 1,500 ($75,000).

Waiting 3 months = $25,000 more in your pocket.

Quick Decision Guide

Ask yourself three questions:

- When's my next vesting date? Check your equity portal.

- How much am I leaving behind? Multiply unvested shares by current stock price.

- Can I negotiate a later start date? Many new employers will wait 2-3 months if you explain you're waiting for equity to vest.

What About Layoffs or Getting Fired?

Usually the same as quitting. You keep vested shares, lose unvested ones.

Some companies offer severance packages that include extra vesting time. For example, "3 months of severance" might mean your RSUs keep vesting for 3 more months after your last day. But this is rare and must be written in your severance agreement.

Special Situations That Might Save Your RSUs

Retirement: Some companies have "retirement eligible" rules. If you're 55+ with 10 years of service, your unvested RSUs might keep vesting after you leave. Check your equity plan documents.

Disability: Similar to retirement. Some companies continue vesting if you become disabled. Not common.

Death: Most companies immediately vest all your RSUs if you die. Your beneficiaries get the shares. This is the one situation where unvested RSUs don't disappear.

After You Leave: Your Vested Shares

Your vested shares stay in your brokerage account (usually E*TRADE, Fidelity, or Schwab). You can:

- Keep holding them

- Sell them anytime (watch for company trading windows if you're leaving soon)

- Transfer them to your personal brokerage account

The company can't force you to sell. Those shares are yours just like any stock you bought yourself.

The $100,000 Mistake

Real scenario: Sarah had 2,000 unvested RSUs worth $200,000. Her next vesting date was 6 weeks away, when 500 shares ($50,000) would vest.

She accepted a new job and gave 2 weeks notice. She lost all $200,000.

If she'd negotiated a start date 7 weeks out instead of 2, she'd have kept $50,000. Her new employer said yes when she asked.

Always check your vesting schedule before giving notice.

Now that you know what happens when you leave, let's talk about the most important question: what should you actually do when your RSUs vest?

Smart Strategies: What to Do When Your RSUs Vest

Your RSUs just vested. You now own $100,000 worth of company stock. What do you do?

Think of this moment like receiving a big work bonus. You could spend it all, save it all, or do something in between. The right choice depends on your situation.

Here's the reality: There's no perfect answer that works for everyone. But there are smart ways to think through your options.

The Three Basic Strategies

Let's say $100,000 worth of RSUs just vested. Here's what each approach looks like:

Strategy A: Sell Everything Immediately

- You get $100,000 in cash to diversify, pay off debt, or invest elsewhere

- You avoid putting all your eggs in one basket

- You know exactly what you're getting (no surprises)

Strategy B: Hold Everything

- If the stock doubles in 2 years, you have $200,000

- If it drops 50%, you have $50,000

- You're betting your company will keep growing

Strategy C: The Hybrid Approach

- Sell $40,000 to cover taxes and diversify

- Hold $60,000 for potential upside

- You balance risk with opportunity

The Default Smart Move

At minimum, sell enough shares to cover any tax shortfall immediately. If your company didn't withhold enough (common with the 22% federal rate), you'll owe more at tax time. Don't get caught short.

Beyond that? Consider selling more if your company stock represents more than 10-15% of your total net worth.

Why Concentration Risk Matters

You already have huge concentration risk. Your paycheck comes from this company. Your health insurance comes from this company. Your 401(k) match (probably) comes from this company.

Now your savings are in this company's stock too?

If the company hits hard times, you could lose your job AND watch your stock drop. That's a double hit when you need money most.

The One-Year Rule (If You Hold)

Want to hold your shares? Consider waiting at least one year after vesting. Any gains after that qualify for long-term capital gains rates (0%, 15%, or 20%). That's better than ordinary income rates (up to 37%).

But only do this if you can afford the risk.

Questions to Ask Yourself

How old are you?

- In your 20s or 30s? You have time to recover from a stock drop.

- In your 50s or 60s? You might need this money sooner. Diversify more.

What's your risk tolerance?

- Comfortable with volatility? Hold some shares.

- Sleep better with certainty? Sell more.

Do you have other savings?

- Emergency fund covered? You can take more risk.

- Living paycheck to paycheck? Sell and build stability.

Do you believe in your company's future?

- Genuinely optimistic about growth? Hold a portion.

- Uncertain or skeptical? Sell and diversify.

A Simple Decision Framework

Start here:

- Sell enough to cover your tax bill. This is non-negotiable.

- Calculate what percentage of your net worth is company stock. Include all your RSUs, ESPP shares, and stock options.

- If it's over 15%: Sell more to diversify. You're too concentrated.

- If it's under 15%: You have more flexibility. Consider your risk tolerance and belief in the company.

Real Example: Three Employees, Three Choices

Sarah (age 28, $200k net worth, $100k RSUs vest):

- Company stock would be 50% of her net worth

- She sells $80,000 immediately and holds $20,000

- She's still exposed to upside but not overconcentrated

Mike (age 45, $800k net worth, $100k RSUs vest):

- Company stock would be 12.5% of his net worth

- He sells $30,000 to cover taxes, holds $70,000

- He's bullish on the company and can afford the risk

Jennifer (age 35, $50k emergency fund, $100k RSUs vest):

- She sells everything immediately

- Uses $30,000 to max out her IRA and 401(k)

- Puts $40,000 in a diversified index fund

- Keeps $30,000 as extra emergency savings

All three made smart choices for their situations.

The Bottom Line

Holding company stock means betting on your employer. Sometimes that bet pays off big. Sometimes it doesn't.

The safest approach? Sell most or all of your vested RSUs and diversify. You're already dependent on this company for your income. Don't make your savings dependent too.

But if you choose to hold some shares, do it with eyes open. Set a plan for when you'll sell (specific price target or time frame). Don't just hold forever and hope.

Now that you know your options, let's build your personal RSU action plan.

RSU Taxes Explained + 5 Strategies for 2024

Your RSU Action Plan: What to Do Right Now

You've learned the theory. Now it's time to take control of your actual RSUs.

Think of this like checking your bank balance after getting a raise. You need to know what you have, when you'll get it, and what it means for your finances. Here's your step-by-step checklist.

Step 1: Log into your equity compensation portal

Your company uses one of these: Fidelity, E*TRADE, Schwab, Morgan Stanley, or Shareworks. Find the login link in your onboarding email or ask HR.

Step 2: Find your RSU grant details

Click the "Stock Plan" or "Equity Awards" tab. Look for "RSU Holdings" or "Restricted Stock." You should see:

- Grant date

- Number of shares granted

- Vesting schedule

- Shares vested so far

- Shares unvested

Write this down: "I have 5,000 total RSUs. 2,000 vested (worth $80,000 today). 3,000 unvested (worth $120,000 if I stay). Next vesting: 500 shares on June 1, 2024."

Step 3: Calculate your unvested RSU value

Multiply unvested shares by your current stock price. This is money you'll lose if you quit tomorrow.

Step 4: Mark vesting dates on your calendar

Set reminders two weeks before each vesting date. This gives you time to plan.

Step 5: Estimate your tax bill

Take your next vesting value and multiply by 0.4 (40%). That's roughly what you'll owe in taxes. If 500 shares vest at $150 each, that's $75,000 in income and about $30,000 in taxes.

Step 6: Check if you need extra cash

If your company only withholds 22% federal tax, you might owe more at tax time. Set aside the difference.

Step 7: Decide your strategy now

Before RSUs vest, write down: "I will sell 100% immediately" or "I will hold 50% and sell 50%." Don't decide in the moment.

Step 8: Review quarterly

Set a calendar reminder every three months. Check your vesting schedule, update your calculations, and adjust your plan.

Start with Step 1 today. It takes 10 minutes and you'll finally know exactly what you own.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

How RSUs Are Taxed

RSUs are taxed as ordinary income when they vest, but there's more to the story. Learn about withholding, the tax gap, and strategies to manage your RSU tax bill.

StrategyShould You Sell or Hold Your RSUs? A Clear Guide for Employees

Deciding whether to sell or hold your RSUs is one of the most common questions employees face. This guide walks you through the key factors, tax implications, and practical decision frameworks to help you make the right choice for your financial situation.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

Not sure what to do with your equity?

Get a free personalized analysis