Should You Sell or Hold Your RSUs? A Clear Guide for Employees

How to decide what to do with your vested shares (with real examples and decision frameworks)

Published March 1, 2026 · Updated March 1, 2026

Deciding whether to sell or hold your RSUs is one of the most common questions employees face. This guide walks you through the key factors, tax implications, and practical decision frameworks to help you make the right choice for your financial situation.

The $50,000 Question: What Just Landed in Your Account?

Sarah works at a public tech company. Last Tuesday, 200 RSUs vested on her 1-year anniversary. The stock price was $250 per share. That means $50,000 worth of stock just landed in her brokerage account.

Now she's stuck. Her coworker Jake sold all his RSUs the day they vested and put the money in index funds. "Never keep all your eggs in one basket," he says. But her college friend Emily works at another tech company and held all her shares. They doubled in 18 months. Emily thinks Sarah would be crazy to sell.

Sarah feels paralyzed. She's heard both sides, and both make sense.

Here's what makes this decision so hard: It's like receiving a $50,000 bonus, except instead of cash, you got paid entirely in your company's stock. You believe in your company (you work there, after all). But you also know that tying your paycheck AND your savings to the same company is risky.

This is the core tension every employee faces: potential growth vs. concentration risk. Your company's stock might keep climbing. But if it drops, you lose twice - your net worth shrinks AND your job might be at risk.

You've probably heard conflicting advice from coworkers, friends, and random internet forums. Some people swear by selling immediately. Others insist you should hold for the long-term gains.

Here's the truth: there's no single right answer that works for everyone. But there ARE clear frameworks that help you make the right decision for YOUR situation. That's what this guide will give you.

First, let's clear up the biggest misconception about RSU taxes.

The Most Important Thing to Understand: You Already Paid Taxes

Here's what most employees miss: you already paid taxes on your RSUs the day they vested. The IRS treats vested RSUs exactly like a cash bonus. Not "sort of like" a bonus. Exactly like one.

Think of it this way: Imagine your company gave you a $50,000 cash bonus, then immediately used that cash to buy company stock for you. That's what RSUs are. The IRS sees that $50,000 as ordinary income, just like your salary.

The Real Numbers

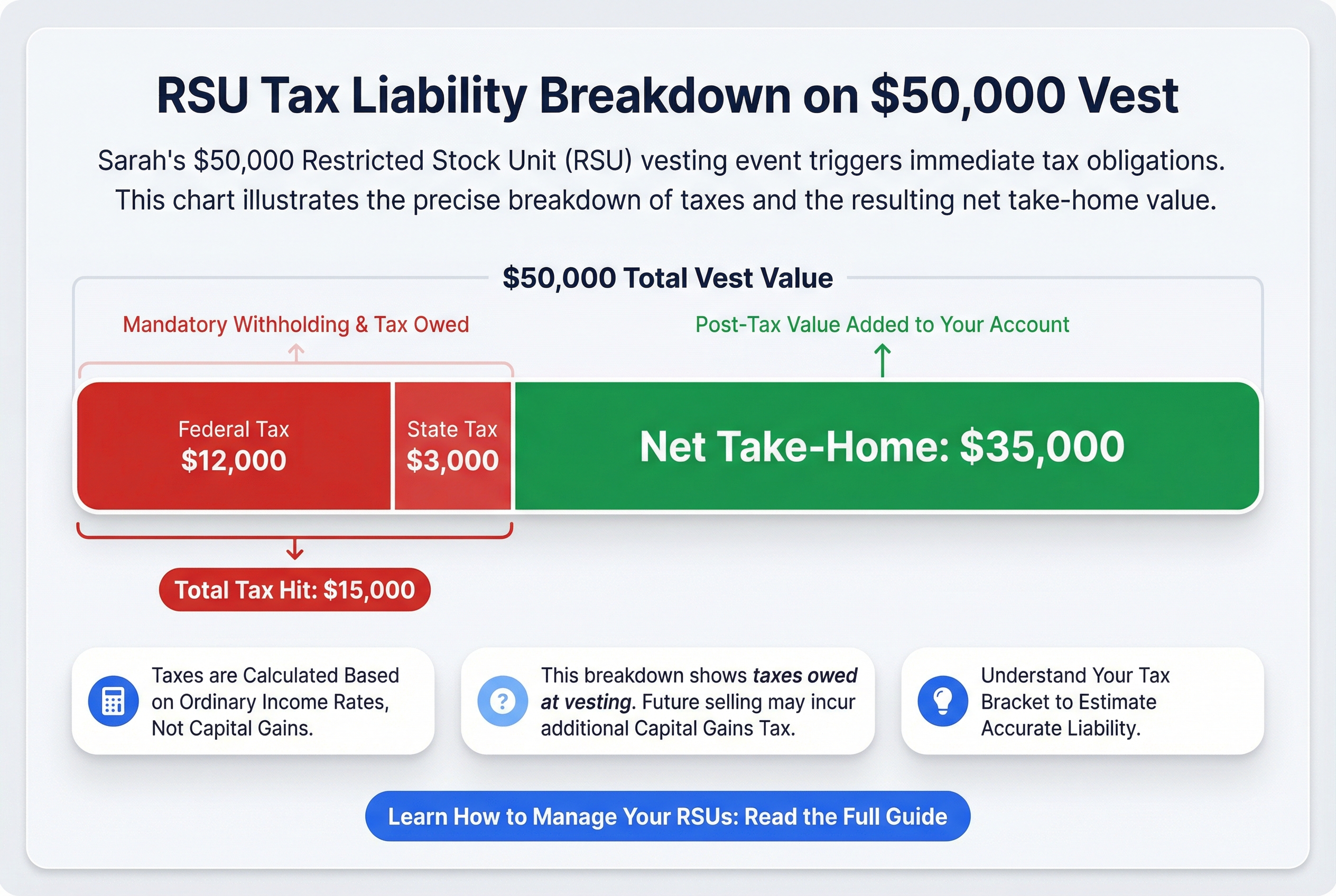

Let's look at Sarah's situation. When her 200 RSUs vested at $250 per share:

- Total value: 200 shares × $250 = $50,000

- Reported on her W-2: $50,000 (same as a cash bonus)

- Federal taxes owed (24% bracket): About $12,000

- State taxes: Another $3,000 (varies by state)

- Total tax hit: $15,000

Her company probably withheld some shares to cover taxes (called "sell to cover"). So she might only receive 150 shares in her account. But here's the key: she already paid taxes on the full $50,000 value.

Why This Changes Everything

This one fact reframes your entire decision. You're not deciding "should I sell my RSUs?" You're deciding "would I take $50,000 of my own money and buy this stock today?"

Because that's exactly what holding means. You've already cashed out from a tax perspective. The money is yours. You just happen to be holding it in company stock instead of cash.

Most employees think holding RSUs is different from buying stock. It's not. Once they vest, you own shares you've already paid for with tax dollars.

Now let's look at exactly how those taxes work, so you can see the real numbers in your situation.

The immediate tax hit: How $50,000 in vested RSUs is reduced by ordinary income taxes.

The immediate tax hit: How $50,000 in vested RSUs is reduced by ordinary income taxes.

How RSU Taxes Actually Work: The Numbers You Need to Know

Here's what catches most people off guard: your RSUs get taxed twice. Once when they vest, and again if you hold them and sell later at a profit.

Let's break down exactly what happens to your money.

When Your RSUs Vest: The First Tax Hit

The day your RSUs vest, the IRS treats them exactly like a cash bonus. If 100 shares vest at $150 each, you just earned $15,000 of ordinary income. You'll pay the same tax rate on this as you do on your salary.

Think of RSU tax withholding like the taxes taken from your paycheck. It's an estimate, and it might not be exact.

Your company typically withholds 22% for federal taxes automatically. They do this through "sell-to-cover," which means they sell some of your shares before you ever see them.

Here's how the math works:

- 200 RSUs vest at $250/share = $50,000 value

- Company withholds 22% = $11,000 in taxes

- They sell 44 shares to cover that $11,000

- You receive 156 shares in your account

The Problem: 22% Often Isn't Enough

Sarah from our example actually earns $180,000 per year. That puts her in the 32% federal tax bracket. She'll owe an extra $5,000 when she files her taxes ($50,000 × 32% = $16,000 total tax, minus the $11,000 already withheld).

This surprises a lot of people. The 22% withholding is a flat default rate. If you're in a higher tax bracket, you'll get a tax bill in April.

If You Hold Shares: The Second Tax Hit

Let's say Sarah keeps those 156 shares instead of selling them immediately. Six months later, the stock hits $300/share. She sells for $46,800 total.

Now she owes capital gains tax on her profit:

- Cost basis: $250/share (the price when they vested)

- Sale price: $300/share

- Gain: $50 per share × 156 shares = $7,800

Because she held for less than a year, this $7,800 counts as short-term capital gains. That gets taxed at her ordinary income rate (32% again). She'll owe about $2,500 more in taxes.

If she'd held for over a year, it would be long-term capital gains. That's taxed at 15% for most people, which would only be $1,170 in taxes on that same $7,800 gain.

The Tax Timeline in Plain English

- Vesting day: You owe ordinary income tax on the full value. Your company withholds 22% (usually not enough).

- Tax filing season: You might owe more if you're in a higher bracket.

- If you sell later: You owe capital gains tax on any increase in value since vesting.

The key insight: the longer you hold, the more tax complexity you add. And if the stock drops after vesting, you still paid that first round of taxes on the higher value.

Now let's talk about the biggest risk that comes with holding those shares, something that wrecked thousands of employees at companies like Enron and Lehman Brothers.

How to Strategically use RSUs to Save Tax

The Biggest Risk Nobody Talks About: The Enron Effect

In 2001, Enron employees lost everything. They had retirement accounts stuffed with company stock. When Enron collapsed, their jobs disappeared and their savings evaporated overnight. The same thing happened at Lehman Brothers in 2008.

You might think, "My company isn't Enron." You're probably right. But here's the thing: you don't need a total collapse to get hurt badly.

Your Paycheck and Your Portfolio Shouldn't Depend on the Same Thing

Think of it like this: having all your money in one stock is like being a farmer who only grows corn. One bad season and you're in serious trouble. You need to grow different crops.

Right now, your company already controls your biggest asset: your ability to earn money. Your paycheck depends on your company doing well. When you hold company stock, you're doubling down on that same bet.

Here's what that looks like in real life:

Mark's story: Mark worked at a fast-growing tech company. Over 5 years, he accumulated $300,000 in company stock. He kept holding because the stock kept going up. Why sell a winner?

Then 2022 hit. The stock market turned. His company's stock dropped 60% to $120,000. Mark thought, "It'll bounce back." Three months later, his company announced layoffs. Mark lost his job.

In six months, Mark lost his income AND $180,000 in stock value. The double hit was devastating. If he'd sold shares as they vested and put that money in a diversified portfolio, he'd have protected most of that wealth.

Even Great Companies See Massive Drops

You don't need to work at a failing company to lose big. In 2022, Meta's stock dropped 64%. Amazon fell 50%. Netflix lost 51%. These are world-class companies, and their employees who held too much stock watched their net worth get cut in half.

During the 2008 financial crisis, even Apple dropped 60%. Google fell 65%. If your entire portfolio drops that much while you're also worried about layoffs, you'll lose sleep.

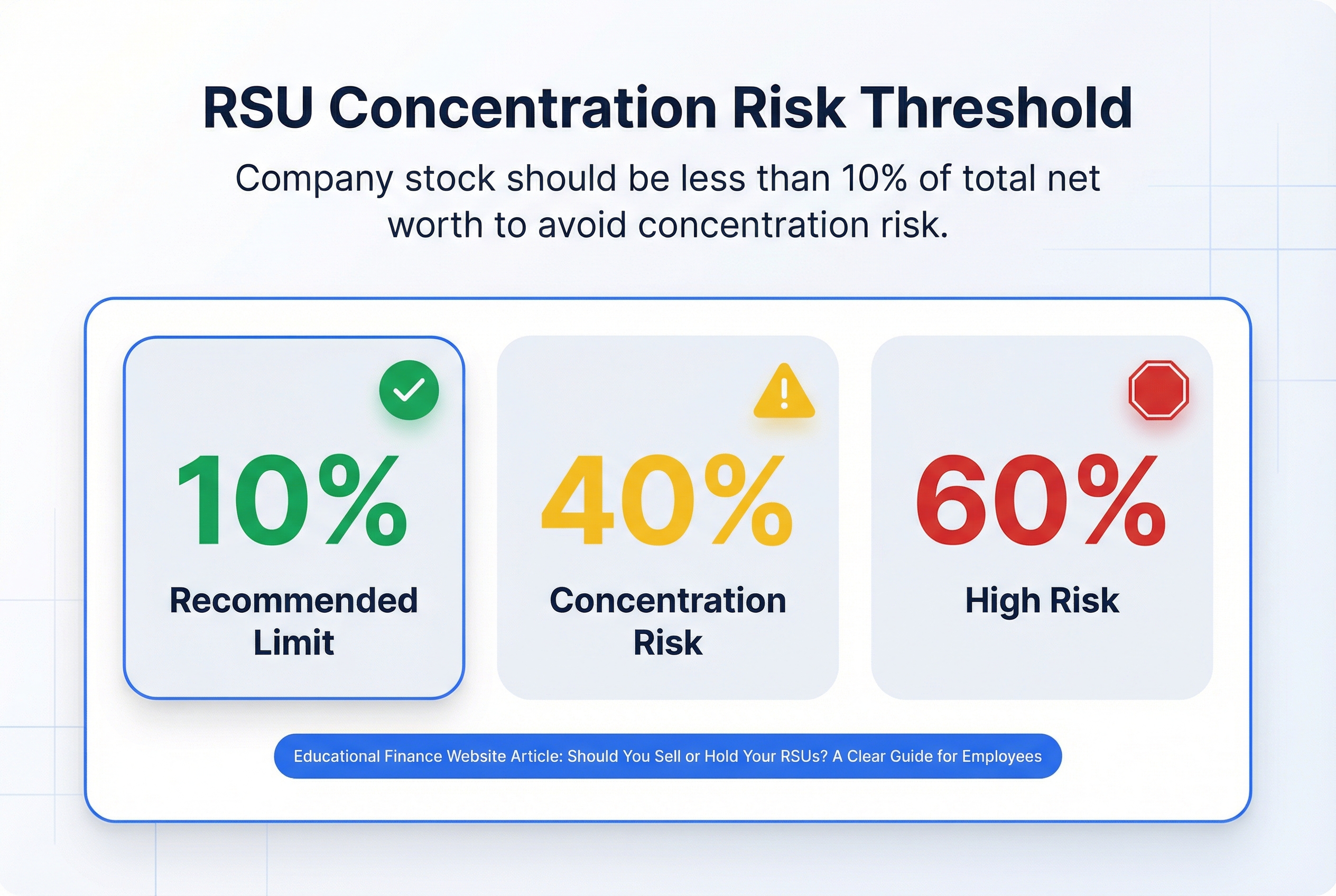

The 10% Rule

Many financial advisors use a simple guideline: no single stock should be more than 10% of your investment portfolio. Some say 5%. Almost no one recommends 30% or 40%, which is where many tech employees end up if they hold all their vested RSUs.

Why 10%? Because at that level, even if your company stock drops 50%, you only lose 5% of your total portfolio. That's manageable. If your company stock is 40% of your portfolio and drops 50%, you just lost 20% of everything you own.

The bottom line: Your job already ties your financial future to your company's success. Your investment portfolio shouldn't make that risk even bigger.

Now, does this mean you should always sell immediately? Not necessarily. Let's look at why most financial advisors recommend selling, and then we'll cover when holding might make sense.

The Case for Selling Immediately: Why Most Financial Advisors Recommend This

Here's the advice most financial professionals give: Sell your RSUs the day they vest.

This feels wrong, especially if you work at a hot company where everyone talks about the stock price. But there's solid math behind this recommendation.

You're Already Betting Everything on Your Company

Think about it this way. Your paycheck comes from your company. Your health insurance comes from your company. Your career growth depends on your company doing well.

If your company hits hard times, you could lose your job AND watch your stock portfolio crash. That's a double hit you want to avoid.

Selling immediately is like taking your paycheck and depositing it in your bank account instead of investing it all back into one stock. You've earned the money. Now protect it.

The Math: Most Individual Stocks Lose to Index Funds

Here's what the data shows. Over any 10-year period, about 60% of individual stocks underperform a simple S&P 500 index fund. Some go to zero.

Your company might be the exception. But do you want to bet your financial future on it?

A Real Example: The Power of Diversification

Jennifer works at a large tech company. Every quarter when her RSUs vest, she sells all shares immediately (about $40,000 per quarter). She invests the proceeds in a mix of index funds:

- 60% total stock market

- 30% international stocks

- 10% bonds

Over 3 years, she built a diversified $480,000 portfolio. Her company's stock went up 30% during this time. Her diversified portfolio went up 22%, with much less volatility.

The key difference: Jennifer sleeps well at night. A bad quarter at work won't devastate her savings. If her company stumbles, she still has a solid nest egg.

The Peace of Mind Factor

When you hold your company stock, you check the price. Every day. Sometimes multiple times per day.

That's exhausting. It also creates an emotional connection to something you can't control.

Selling immediately removes this burden. You've already gotten the bonus (the RSUs). Now you're converting it into stable, diversified wealth.

This Works No Matter What Happens Next

The beauty of selling immediately: it works whether the stock goes up or down after you sell.

Stock goes up? You still built diversified wealth and avoided concentration risk.

Stock goes down? You protected yourself from a loss.

You're not trying to time the market. You're following a consistent strategy that reduces risk.

That said, selling immediately isn't the only reasonable choice. Some situations might justify holding at least some shares. Let's look at those next.

Should I hold or sell my RSUs upon vest?

The Case for Holding: When It Might Make Sense to Keep Some Shares

Let's be clear: holding company stock isn't always wrong. It's just wrong for most people in most situations.

Think of it like keeping money in your hometown's local bank because you believe in the community. That's fine if you only keep 5-10% of your savings there. It's a disaster if that's where ALL your money lives.

When Holding Some Shares Makes Sense

Here are the conditions where holding a portion of your RSUs might be reasonable:

1. Your company stock is a small slice of your wealth

If company stock represents less than 10% of your total net worth, you have room to take some risk. Above 10%? You're in concentration risk territory.

2. You have strong, informed conviction

This means you've studied the company's financials, understand the competitive landscape, and have specific reasons to believe in growth. "My manager says we're doing great" doesn't count. Neither does "the stock has been going up."

3. You already have a diversified portfolio

You own index funds, maybe some real estate, maybe bonds. Your company stock is extra, not the foundation of your wealth.

4. You can afford to lose this money

If the stock dropped 50% tomorrow, your retirement plans wouldn't change. Your kids' college fund would be fine. You'd be disappointed but not devastated.

5. Tax timing matters to you

If you're planning to sell in 6 months anyway, holding until you hit long-term capital gains (one year after vest) might save you money. But only if points 1-4 above are true.

A Real Example of Calculated Risk

David works at a growing software company. He has $800,000 in diversified investments: $500,000 in index funds, $200,000 in a rental property, and $100,000 in bonds.

When his RSUs vest each quarter ($30,000 worth), he sells 70% immediately and keeps 30%. His total company stock holdings: about $80,000, which is 8% of his $1 million net worth.

David believes in his company's 5-year expansion plan. He's read the earnings reports. He understands the risks. If the stock drops 50%, he'd lose about $40,000. That would sting, but it wouldn't wreck his financial future.

This is calculated risk, not concentration risk.

The Key Difference: Hope vs. Strategy

Employees who successfully held shares usually had three things in common:

- Company stock was under 10% of their total wealth

- They had specific, informed reasons to believe in growth

- They could afford to be wrong

Compare that to most employees who hold:

- Company stock is 40-60% of their net worth

- They're holding because "it might go up" or "I'd feel stupid if I sold and it doubled"

- A big drop would seriously hurt their financial goals

See the difference? One is strategic. The other is gambling with money you can't afford to lose.

What About Short-Term vs. Long-Term Capital Gains?

You've heard that holding shares for over a year gets you better tax rates. That's true. Long-term capital gains are taxed at 0-20% (depending on your income). Short-term gains are taxed as regular income (potentially 22-37%).

But here's the math that matters: Would you rather pay 15% tax on a $10,000 gain, or 25% tax on a $5,000 gain because the stock dropped while you waited?

Tax savings only help if the stock doesn't tank while you're holding it.

Some Employees Did Get Rich by Holding

We can't ignore this: some people held their company stock and made life-changing money. Early Amazon employees. Early Google employees. Early Netflix employees.

But here's what you don't hear: for every employee who got rich holding, there are dozens who lost significant wealth when their "sure thing" company crashed.

The employees who won big usually got in very early (when the stock was cheap) and had other sources of income and savings. They could afford the risk.

The Bottom Line on Holding

Holding some shares can make sense if:

- You're already financially secure

- Company stock is a small percentage of your wealth

- You have specific, informed reasons to believe in growth

- You can afford to lose this money

If any of those conditions aren't true, you're not making a calculated bet. You're hoping. And hope is not a financial strategy.

Now that you've seen both sides, the case for selling and the case for holding, how do you actually decide what's right for you? That's what we'll tackle next with a clear decision framework.

The Complete Guide to RSUs | 15 Common Questions ❓Answered | What People Get Wrong...

The 10% Rule: The threshold where company stock begins to represent an unacceptably high concentration of personal wealth.

The 10% Rule: The threshold where company stock begins to represent an unacceptably high concentration of personal wealth.

Your Personal Decision Framework: The Questions to Ask Yourself

Think of this like a flight pre-check checklist. You go through each item before deciding to take off. This framework helps you make a smart decision based on YOUR situation, not general advice.

Question 1: What percentage of your net worth is in company stock?

Here's how to calculate it:

- Add up the current value of your company stock (all vested shares)

- Add up everything else you own (401k, savings, other investments, home equity)

- Divide company stock by total assets

Formula: Company stock value ÷ Total assets = Concentration percentage

The 10% Rule: If your company stock exceeds 10% of your net worth, you're too concentrated. This is the threshold where most financial advisors start waving red flags.

Question 2: What are your financial goals in the next 1-3 years?

Be specific:

- Buying a house? How much do you need for a down payment?

- Paying off student loans or credit cards? What's the balance?

- Building an emergency fund? How much do you need?

If you have concrete goals with dollar amounts, selling RSUs gives you guaranteed money to hit those targets. Holding means gambling that the stock goes up enough to cover your needs.

Question 3: Do you have 6+ months of expenses saved outside of company stock?

Calculate your monthly expenses (rent, food, insurance, everything). Multiply by 6. Do you have that much in savings or other liquid investments that AREN'T company stock?

If no, you need to sell some RSUs to build this cushion. Your emergency fund can't be in company stock because emergencies don't wait for stock prices to recover.

Question 4: How diversified are your other investments?

Look at your 401k and other accounts. Are they spread across different companies and industries? If yes, you have a buffer. Your company stock is just one piece.

If your other investments are small or non-existent, holding company stock means putting all your eggs in one basket.

Question 5: Can you afford to lose 50% of your company stock value?

Be honest. If your company stock dropped 50% tomorrow, would it:

- Delay your house purchase?

- Force you to work longer before retirement?

- Create financial stress?

If yes to any of these, you're holding too much.

Real Example: Rachel's Decision

Let's work through this with Rachel, a software engineer:

Her situation:

- Company stock:

$80,000(just vested) - 401k:

$120,000 - Savings:

$40,000 - Other investments:

$60,000 - Total net worth:

$300,000

Her calculation:

$80,000 ÷ $300,000 = 27% of her net worth is company stock

That's nearly 3x the 10% threshold. Way too concentrated.

Her goals:

- Buy a house in 2 years (needs

$60,000down payment) - Build emergency fund (needs

$30,000for 6 months expenses)

Her answers:

- Emergency fund outside company stock? No, only

$40,000total savings - Can afford 50% loss? No, she needs this money for her house

- Other investments diversified? Yes, her 401k is spread across index funds

Rachel's decision: Sell at least 75% of her company stock immediately.

This gives her $60,000 for the house and brings her company stock down to $20,000 (about 7% of net worth, under the 10% threshold). She keeps $20,000 in company stock for potential upside.

Creating Your Personal Policy

Once you've worked through these questions, create a standing policy for future vests. This removes emotion from the decision.

Rachel's policy: "I will automatically sell 80% of all future RSU vests the day they vest. I'll hold 20% for growth potential, but never let company stock exceed 10% of my net worth."

Your policy might be different. Maybe you sell 100% every time. Maybe 50%. The key is deciding NOW, not when emotions are high after a big vest or stock price swing.

Now that you have a framework for today's decision, let's talk about creating a long-term strategy for all your future RSU vests.

The Standing Strategy: Creating Your Personal RSU Policy for Future Vests

Here's the thing about RSU vests: they keep happening. Every quarter or every year, you'll face the same decision. Should I sell? Should I hold? What about this time?

This gets exhausting fast.

The better approach: decide once, then automate. Think of this like setting up automatic 401k contributions. You make the hard choice one time, then it happens without emotional interference. No more agonizing every quarter when shares vest.

Why You Need a Standing Policy

Decision fatigue is real. When you're deciding fresh each quarter, you're vulnerable to:

- Selling after the stock drops (panic mode)

- Holding after the stock soars (greed mode)

- Doing nothing because you're too busy or overwhelmed

A standing policy removes emotion from the equation. You decide your strategy when you're thinking clearly, not when you're reacting to stock movements.

Three Policy Templates (Pick One)

Conservative Policy: Sell 100% Immediately

Best for most people. Every vest, you sell everything and diversify.

Example: Conservative Chris earns $90k and gets $25,000 in RSUs quarterly. His policy: sell 100% at vest, invest in a target-date fund. He never thinks about it. His brokerage executes the trade automatically. Four times a year, $25,000 moves from company stock to diversified investments.

Moderate Policy: Sell 70-80%, Hold 20-30%

For employees who want some company exposure but know diversification matters.

Example: Moderate Maria earns $120k with $25,000 quarterly vests. Her policy: sell 75% ($18,750) immediately into index funds, hold 25% ($6,250) in company stock. She sets a calendar reminder each January to rebalance. If company stock grows beyond 10% of her net worth, she sells the excess.

Aggressive Policy: Sell 50% (Only If Already Well-Diversified)

For employees with significant wealth outside their company stock.

Example: Aggressive Alex has $2 million net worth and gets $50,000 in RSUs quarterly. His policy: sell 50% ($25,000) immediately, hold 50%. He reviews quarterly to ensure company stock stays under 8% of total wealth. If it creeps higher, he sells shares to rebalance. This only works because company stock is a small slice of his total pie.

How to Set Up Your Policy

Step 1: Choose your percentage. Most people should start with 100%. If you're already well-diversified and want company exposure, consider 70-80%.

Step 2: Set up automatic trades. Most brokerages (E*TRADE, Schwab, Fidelity) let you create automatic sell orders that trigger when RSUs vest. You set it once, it runs forever.

Step 3: Decide where the money goes. Don't let cash sit in your brokerage account. Set up automatic transfers to your target investments (index funds, target-date funds, whatever matches your overall strategy).

Step 4: Create review reminders. Set a calendar reminder for one year from now. Label it "Review RSU Policy."

When to Revisit Your Policy

Your standing policy isn't forever. Review it:

- Annually (minimum)

- After major life changes (marriage, home purchase, job change)

- If company stock concentration creeps up (check quarterly)

- As your net worth grows (you might shift from conservative to moderate)

If you started with "sell 100%" at $200k net worth, you might shift to "sell 75%" when you hit $1 million. More wealth means you can afford more company stock risk.

The Relief of Automation

Once your policy is set, you stop wrestling with the decision every quarter. Your RSUs vest. The trades execute. The money diversifies. You focus on your actual job and life.

This doesn't mean you stop paying attention. You still check quarterly to make sure your policy is working. But you're checking the system, not making emotional decisions about individual vests.

Now, let's talk about what your HR department probably hasn't told you about RSUs.

What Your HR Department Won't Tell You: The Hidden Considerations

Think of these as the fine print in your equity compensation. Not secret, but easy to miss. And missing them can cost you real money.

You Can't Always Sell When You Want

Most companies have trading windows. You can only sell during specific periods, usually a few weeks after earnings announcements.

Here's what this looks like: Tom's 500 RSUs vest on March 15 at $180/share ($90,000 value). His company has a trading window that closes March 20 before Q1 earnings on April 5. If Tom wants to sell, he has exactly 5 days. If he misses that window, he's stuck holding until the next one opens (probably late April).

Blackout periods are even more restrictive. If you're an executive or work in finance, you might not be able to trade for weeks before earnings. Check with your stock admin team before planning any sales.

The Cost Basis Mistake That Costs Thousands

This is where employees overpay taxes. Your cost basis is the value at vest, not $0.

Back to Tom: His 500 RSUs vest at $180/share. That $90,000 shows up on his W-2. He already paid income tax on it (roughly $32,000 if he's in the 35% bracket).

He sells a week later at $185/share for $92,500 total. He owes capital gains tax only on the $2,500 gain (500 shares × $5 increase). That's about $375 in taxes.

Many employees think their cost basis is $0. They'd calculate taxes on the full $92,500 and panic. Or worse, they file incorrectly and overpay by thousands.

Your cost basis = the stock price on the day your RSUs vested. Write this down.

What Happens If You Leave

Unvested RSUs usually disappear when you quit or get laid off. Some companies have exceptions (retirement provisions, layoff packages), but the default is: you lose them.

If Tom has 1,000 RSUs vesting in 6 months and leaves next month, those shares vanish. That's $180,000 of future compensation gone.

This changes the math on job offers. A new job offering $20k more in salary might actually pay less if you're walking away from $100k in unvested RSUs.

Vesting Schedules Aren't Always Equal

Some companies backload vesting. You might get 5% in year one, 15% in year two, 30% in year three, and 50% in year four.

Tom's schedule works this way. His next vest is 1,000 shares in 6 months (double what just vested). His concentration risk is about to jump. He needs to plan now, not wait until that vest date.

Coordinating With Other Equity

If you have an ESPP (employee stock purchase plan), you're buying company stock at a discount. If you also hold vested RSUs, you now have company stock from two sources.

This doubles your concentration risk. Many employees don't realize they're overexposed until it's too late.

Now let's look at how to handle multiple types of equity compensation at once.

Special Situations: When You Have Multiple Types of Equity Compensation

Think of your equity compensation like having multiple bank accounts at the same company. You need to look at the total balance across all of them, not each one individually.

Here's what trips people up: You check your RSU balance and think "that's only 15% of my net worth, I'm fine." But you forget about the stock options you exercised last year. And the ESPP shares you've been accumulating. When you add it all up, you might be sitting on 50% company stock without realizing it.

Calculate Your Real Company Stock Exposure

Add up everything:

- Vested RSUs (current market value)

- Exercised stock options you still own (current market value)

- ESPP shares you haven't sold yet (current market value)

- Unvested RSUs if they vest within 12 months (estimated value)

This total is your concentration risk. Not the pieces. The whole thing.

The Priority Framework: What to Sell First

When you have multiple equity types, here's the general order to consider:

1. RSUs first (you already paid taxes, no special tax benefits) 2. ESPP shares next (after you meet the holding period for better tax treatment) 3. Non-qualified stock options (NSOs) when you exercise them 4. Incentive stock options last (ISOs have special tax benefits if you hold longer)

Why this order? RSUs give you no tax advantage for holding. You already got taxed. ISOs, on the other hand, can qualify for lower capital gains rates if you hold them long enough.

A Real Example: Lisa's Multiple Equity Problem

Lisa works at a tech company. She just added up her equity:

- Vested RSUs:

$100,000 - Vested ISOs she exercised:

$80,000 - ESPP shares held 6 months:

$30,000 - Total company stock:

$210,000

Her other assets: $140,000 in savings and retirement accounts.

Company stock is 60% of her $350,000 net worth. Way too concentrated.

Her strategy:

- Sell all RSUs immediately:

$100,000 - Sell ESPP shares:

$30,000(she met the holding period) - Keep ISOs for now (better tax treatment if held longer)

This gets her to $80,000 company stock, which is 23% of her net worth. Still high, but manageable.

Her new policy: Sell all future RSU vests and ESPP purchases immediately until she's under 10% company stock.

The ESPP Trap

Don't buy ESPP shares AND hold your RSUs. That's doubling down on concentration. If you participate in ESPP, sell those shares right after purchase. Then decide separately what to do with RSUs.

When to Get Professional Help

Talk to a tax professional if:

- Your total equity value is over

$200,000annually - You have ISOs worth more than

$100,000 - You're considering exercising options early

- You have AMT (Alternative Minimum Tax) concerns with ISOs

The tax rules for ISOs are complicated. The concentration risk calculation is simple, but the tax optimization isn't.

Your Combined Policy

Create one policy that covers all your equity types. Not separate rules for each.

Example: "I will keep no more than 10% of my net worth in company stock total. This means selling RSUs at vest, selling ESPP shares at purchase, and trimming exercised options when they push me over 10%."

Review this total every quarter. Company stock prices change. Your net worth changes. What was 10% in January might be 25% by June.

Now let's look at what other employees actually did when they faced these same decisions.

Real Scenarios: What Other Employees Actually Did (And What Happened)

These stories are like case studies from real employees. Each person made a choice that was right (or wrong) for their specific situation. The lesson isn't about who picked the winning strategy. It's about matching your decision to your actual financial needs.

Scenario 1: Amy Sold Everything and Bought a House

Amy worked at a tech company for three years. Every time her RSUs vested, she sold immediately. Over those three years, she collected $300,000 after taxes.

She used $100,000 for a down payment on a house. The rest went into boring index funds.

Here's the twist: her company's stock went up 80% after she sold. If she'd held, she'd have $540,000 instead of $280,000 in her investment account.

Did she make a mistake? Absolutely not.

Amy owns her house. She sleeps well at night. Her money is spread across hundreds of companies, not just one. She didn't "miss out" because she met her actual goal. The stock going up doesn't change the fact that she made the right choice for her situation.

Scenario 2: Brian Held Everything and Lost $220,000

Brian believed in his company. Every time RSUs vested, he kept them. "Why would I sell? I work here. I know we're doing great things."

Over five years, he accumulated $400,000 in company stock. That was 75% of everything he owned.

Then his company missed earnings by 10%. The stock dropped 55% in three months. Brian's net worth fell from $530,000 to $310,000.

He lost $220,000 in 12 weeks.

Brian's problem wasn't that the stock went down. Markets do that. His problem was concentration. Think of it like putting 75% of your savings in your neighbor's restaurant. Even if it's the best restaurant in town, that's too much risk in one place.

Scenario 3: Maria Held 10% and Got Lucky

Maria followed a simple rule: sell 90%, keep 10% as her "lottery ticket."

Over four years, she sold $270,000 worth of RSUs and invested in index funds. She kept $30,000 worth of company stock.

Her company's stock tripled. That $30,000 became $90,000.

This worked because Maria treated it like a calculated bet. She could afford to lose that $30,000. It was 10% of her equity comp, not her entire financial future. When it paid off, great. If it hadn't, she'd still be fine.

Scenario 4: David's 80/20 Split Matched His Risk Tolerance

David sold 80% of his RSUs immediately and held 20%. This wasn't based on stock predictions. It was based on his personality.

He wanted some upside exposure but couldn't handle the stress of watching all his wealth swing with one stock. The 80/20 split let him sleep at night.

His company's stock went up 40%. His held shares gained $48,000. His sold shares (now in index funds) gained $60,000. Total gain: $108,000.

The "perfect" choice would have been holding everything for a $150,000 gain. But David would have been a nervous wreck. The 80/20 split worked because it matched his actual risk tolerance.

The Real Lesson: Your Situation Matters More Than the Stock

Notice something about these stories? We can only judge them now because we know what happened to the stock.

Before the stock moved, nobody knew. Amy didn't know her stock would double. Brian didn't know his would crash. That's hindsight bias, it's easy to judge decisions after you know the outcome.

The right choice depends on your financial situation, not your ability to predict stock prices. Amy needed a house. Brian was over-concentrated. Maria could afford to gamble with 10%. David needed to match his stress tolerance.

What's your situation? That's what matters.

Now let's build your actual action plan for this week.

Your Action Plan: What to Do This Week

Think of this as your equity compensation to-do list. You don't need to tackle everything at once. Just start with Action 1 today.

Action 1: Calculate Your Current Concentration (Do Today, 15 Minutes)

Pull up your bank accounts, retirement accounts, and brokerage statements. Add up everything you own. Then calculate:

Company stock value ÷ Total net worth = Your concentration percentage

Example: You have $40,000 in company stock, $60,000 in your 401(k), and $20,000 in savings. That's $40,000 ÷ $120,000 = 33% concentration.

If you're over 20%, you're taking on more risk than most financial advisors recommend.

Action 2: Review Your Vesting Schedule (Do Today, 10 Minutes)

Log into your equity compensation portal (E*TRADE, Fidelity, Schwab, or wherever your company holds your RSUs). Look for these details:

- How many shares vest in the next 12 months?

- What are the specific vest dates?

- What's the current share price?

- Multiply shares × price to see the dollar amounts coming

Write these dates down. You need to know what's ahead.

Action 3: Decide Your Personal Policy (Do This Week, 30 Minutes)

Using the framework from earlier, pick your rule:

- Sell 100% at vest (lowest risk, maximum diversification)

- Sell 80%, keep 20% (mostly safe, small upside bet)

- Sell 50%, keep 50% (balanced approach)

- Keep 100% (only if you answered yes to all the "hold" questions)

Write it down. Make it your standing rule for all future vests.

Action 4: Check Trading Windows (Do This Week, 10 Minutes)

Before you sell anything, confirm:

- Are you in a blackout period right now?

- When is the next open trading window?

- Do you need pre-clearance to trade?

Your HR department or equity portal will have this information. Don't accidentally break insider trading rules.

Action 5: Set Up Your System (Do This Week, 30 Minutes)

If you're selling immediately:

- Check if your brokerage offers automatic sell-at-vest

- If not, set calendar reminders for each vest date

- Add a reminder for 2 days after each vest (to execute your sell order)

If you're holding:

- Set a calendar reminder to review your concentration quarterly

- Pick a maximum percentage (like 25%) where you'll force yourself to sell

Action 6: Schedule Your Annual Review (Do This Month, 5 Minutes)

Pick a date one year from now. Put it in your calendar with the note: "Review RSU policy and concentration percentage."

Your life changes. Your company changes. Your policy should too.

When to Get Professional Help

Consider hiring a financial advisor if:

- Your total equity compensation exceeds $200,000 per year

- You have multiple types of equity (RSUs, stock options, ESPP)

- Your concentration is over 30% and you're not sure how to fix it

- You're facing a major tax bill (over $50,000) from a large vest

Consider a tax professional if:

- You're in a high tax state (California, New York, New Jersey)

- You're planning to move states soon

- You have AMT concerns with ISOs

- Your total income (salary + RSU vesting) pushes you over $200,000

Here's What Sarah Did This Week

Remember Sarah from the beginning? She had $50,000 worth of RSUs vest and didn't know what to do.

Monday: She calculated her concentration. Company stock was 35% of her net worth. Way too high.

Tuesday: She logged into her equity portal. Three more vests this year totaling $150,000. That would push her concentration even higher.

Wednesday: She decided on a policy. Sell 80% of all vests immediately. Keep 20% as a small bet on the company.

Thursday: She checked her trading window. Open until next Friday. No blackout period.

Friday: She placed a sell order for 80% of her current shares ($40,000). She set calendar reminders for her next three vest dates. She scheduled her annual review for next January.

Total time: 3 hours spread over a week.

Sarah told us she feels relieved. She's not checking the stock price every day anymore. She's not lying awake wondering if she should sell. She has a plan.

The Most Important Thing

Making an imperfect decision is better than making no decision at all.

Holding your RSUs because you "haven't decided yet" IS a decision. It's a decision to stay concentrated in one stock. It's a decision to take on extra risk.

You don't need the perfect answer. You need YOUR answer. Pick a policy that lets you sleep at night. Then stick to it unless your situation changes.

You've got this. Start with Action 1 today.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

What Are RSUs? A Complete Guide to Restricted Stock Units

Restricted Stock Units (RSUs) are a type of stock compensation where your company promises to give you shares after you meet certain conditions, usually working there for a set period. Unlike stock options, RSUs always have value as long as the company's stock has value. This guide explains how RSUs work, when you'll owe taxes, and how to make the most of this benefit.

TaxHow RSUs Are Taxed

RSUs are taxed as ordinary income when they vest, but there's more to the story. Learn about withholding, the tax gap, and strategies to manage your RSU tax bill.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

Not sure what to do with your equity?

Get a free personalized analysis