Double-Trigger RSUs at Pre-IPO Companies: What You Need to Know Before Your Company Goes Public

Understanding when your equity actually becomes yours and what it means for your taxes

Published March 1, 2026 · Updated March 1, 2026

Double-trigger RSUs require two conditions before you receive actual shares: time-based vesting and a liquidity event like an IPO. This structure helps pre-IPO companies avoid creating tax bills for employees when shares can't be sold, but it also means your equity isn't truly yours until both triggers happen.

The Pre-IPO Equity Puzzle: Why Your RSUs Work Differently

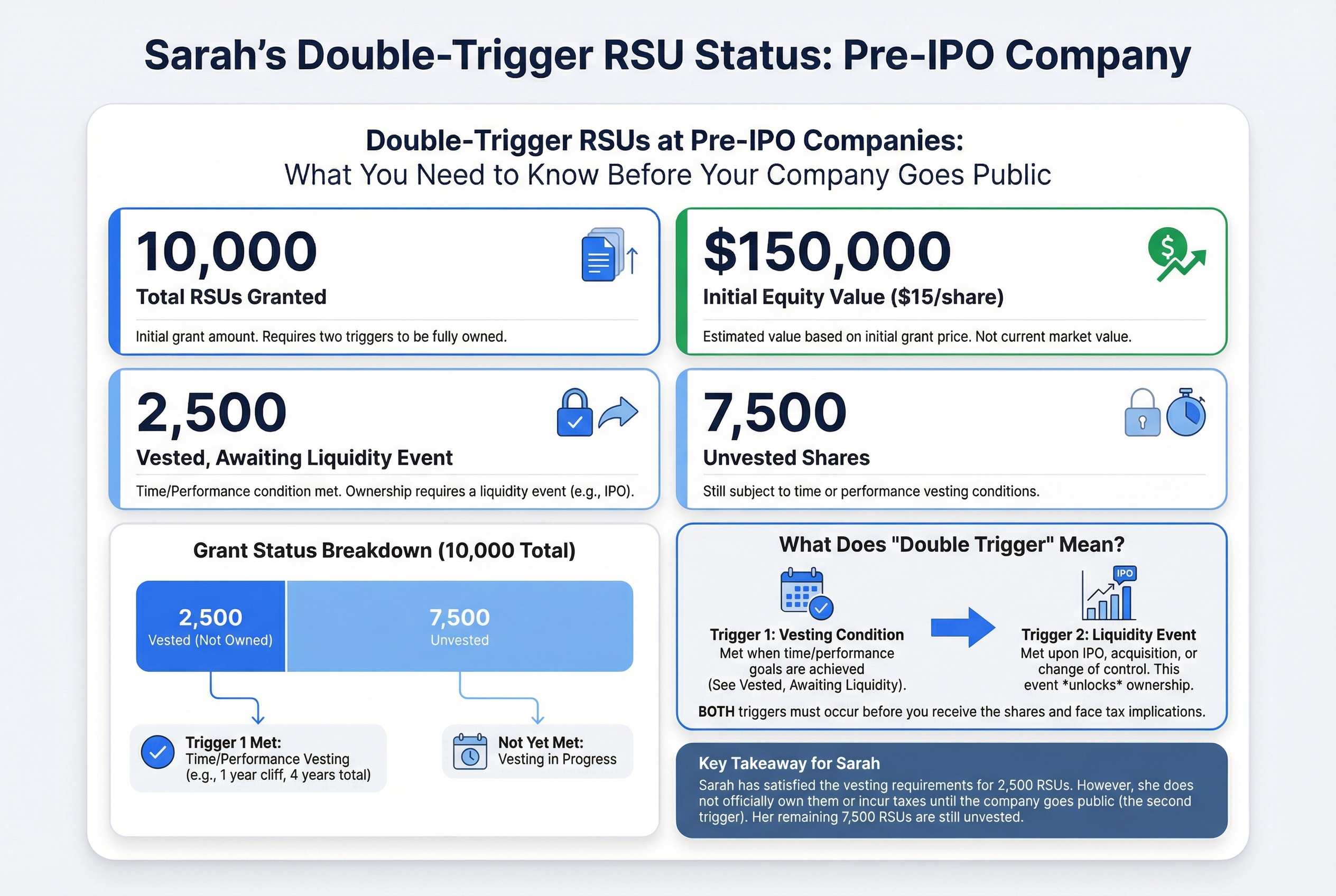

Sarah just joined a Series C startup as a product manager. Her offer letter included 10,000 RSUs valued at $15 per share. On paper, that's $150,000 in equity. She was thrilled.

Fast forward one year. Sarah checks her equity dashboard and sees that 2,500 RSUs have "vested." She waits for something to happen. Nothing does. No shares appear in her account. No tax forms arrive. She emails HR, worried she misunderstood her entire compensation package.

Here's the confusing part: Those RSUs did vest. But Sarah still doesn't own any stock. And she won't until her company goes public or gets acquired.

Think of it like a gift certificate to a restaurant that hasn't opened yet. You earned the certificate. It's yours. But you can't actually use it until the doors open for business.

This is how most pre-IPO companies structure their RSUs. They use something called "double-trigger" vesting. You need two things to happen before you actually receive shares:

- Time passes (you stay at the company long enough)

- A liquidity event occurs (the company goes public or gets acquired)

This setup confuses thousands of employees every year. You watch your RSUs vest on schedule, but you can't touch them. It feels like the company is holding your compensation hostage.

But here's the truth: This structure isn't about being stingy. It's actually protecting you from a massive tax problem that could cost you thousands of dollars in taxes on shares you can't even sell yet.

Let's break down exactly how double-trigger RSUs work and why they exist.

Sarah's initial grant: 10,000 RSUs valued at $150,000, with 2,500 vested but inaccessible due to the second trigger requirement.

Sarah's initial grant: 10,000 RSUs valued at $150,000, with 2,500 vested but inaccessible due to the second trigger requirement.

What Double-Trigger RSUs Actually Are (In Plain English)

Think of double-trigger RSUs like a safe that needs two different keys to open. You need both keys, not just one. Until you have both, the safe stays locked.

Here's what each "key" actually means:

Trigger 1: Time-Based Vesting (The Loyalty Key)

This is straightforward. You earn RSUs by working at the company for a specific period. Most companies use a four-year schedule where you earn 25% of your grant each year.

When you hit your vesting date, you've satisfied trigger one. But you don't get shares yet. You've earned the right to receive them once trigger two happens.

Trigger 2: Liquidity Event (The Cash-Out Key)

A liquidity event is when the company creates a way for you to actually sell shares for real money. The two main liquidity events are:

- IPO: The company goes public and shares trade on the stock market

- Acquisition: Another company buys your company

Until one of these happens, you can't turn your RSUs into cash. The shares aren't tradeable. They're just a promise.

Both Triggers Must Happen

This is the critical part. You need BOTH triggers before you receive actual shares. Time vesting alone doesn't do it. A liquidity event alone doesn't do it. You need both.

Here's How It Works in Real Life

Marcus gets hired and receives 8,000 RSUs vesting 25% per year over four years. After year one, 2,000 RSUs satisfy trigger one. After year two, another 2,000 RSUs satisfy trigger one (4,000 total). But Marcus still has zero actual shares because trigger two hasn't happened.

In year three, the company IPOs. Boom. Trigger two hits. Marcus immediately receives 6,000 shares (years one, two, and three of his time vesting). He'll get his final 2,000 shares when year four hits.

This double-trigger structure is standard at pre-IPO companies. If your company hasn't gone public yet, your RSUs almost certainly work this way.

Now let's talk about why companies use this structure in the first place.

Double Trigger RSUs Basics

Why Companies Use Double-Trigger RSUs (And Why It Actually Protects You)

Double-trigger RSUs feel like a frustrating delay. You've earned the shares, you've worked for years, but you still can't touch them. Here's the thing: this structure actually saves you from a financial nightmare.

The problem it solves: Without the double-trigger protection, you'd owe massive tax bills on shares you can't sell.

Imagine winning a $200,000 house in a contest, but you're not allowed to move in or sell it for two years. The IRS still wants you to pay taxes on that $200,000 this year. You'd owe roughly $70,000 with no way to get the cash. That's what would happen without double-trigger RSUs.

The Real-World Disaster Scenario

Let's look at Jamie's situation. She has 5,000 RSUs at a pre-IPO company. Without double-trigger protection, those RSUs vest based on time alone. After three years, all 5,000 shares vest. The company is now valued at $40 per share.

What happens: Jamie suddenly has $200,000 of taxable income (5,000 shares × $40). She owes approximately $70,000 in federal and state taxes. But she can't sell a single share because the company is still private. She'd need to pay $70,000 out of pocket from her salary or savings.

Thousands of pre-IPO employees faced exactly this problem before double-trigger RSUs became standard. Some had to take out loans. Others sold their cars or dipped into retirement accounts just to pay taxes on stock they couldn't access.

How the IRS Rules Make This Work

The IRS has a simple rule: you only pay taxes when you have real ownership. They call this "substantial risk of forfeiture." As long as there's a real chance you could lose the shares, you don't owe taxes yet.

The second trigger creates that risk. Until the company goes public or gets acquired, there's always a chance it won't happen. The shares could become worthless. This risk is what makes the tax deferral legal and legitimate.

Think of it like this: You don't pay taxes on a lottery ticket until you actually win and collect the money. The second trigger keeps your RSUs in "lottery ticket" status until there's real cash available.

The Company Benefits Too

Double-trigger RSUs also help companies delay SEC reporting requirements. Private companies with too many shareholders face expensive regulatory obligations. By keeping RSUs from fully vesting, companies stay under these thresholds until they're ready to go public.

Facebook pioneered this approach before their 2012 IPO. They had granted thousands of RSUs to employees but didn't want anyone facing tax bills before the company could provide liquidity. The double-trigger structure let them reward employees without creating a tax crisis.

The bottom line: Yes, double-trigger RSUs make you wait longer. But they prevent you from owing five or six figures in taxes on shares you can't sell. It's protection disguised as a delay.

Now that you understand why companies use this structure, let's compare it directly to single-trigger RSUs so you can see exactly what makes them different.

Single-Trigger vs. Double-Trigger RSUs: What's the Difference?

Think of single-trigger RSUs like a regular paycheck. You work for a year, you get paid. Think of double-trigger RSUs like a bonus that only pays out when your company hits a big milestone, like an IPO.

Single-trigger RSUs are the standard at public companies like Google or Microsoft. You only need to satisfy one requirement: stay employed long enough for your shares to vest. Once they vest, you immediately receive actual shares and owe taxes on them. The good news? You can sell those shares right away to cover your tax bill because the stock trades on the public market.

Double-trigger RSUs are the standard at pre-IPO companies. You need to satisfy two requirements: (1) stay employed long enough for time-based vesting, AND (2) wait for a liquidity event like an IPO or acquisition. Until both triggers happen, you get zero shares and owe zero taxes.

Why the Different Structures?

Public companies use single-trigger because their shares are liquid. You can sell them immediately. No problem.

Private companies use double-trigger to protect you from a tax nightmare. Imagine owing $50,000 in taxes on shares you can't sell. That's what would happen with single-trigger RSUs at a private company.

Same Grant, Different Worlds

Let's say you get 4,000 RSUs vesting over 4 years (1,000 per year).

At Google (public company, single-trigger):

- Year one: You receive 1,000 shares worth $150,000

- You owe about $52,500 in taxes (35% combined rate)

- You can sell shares immediately to cover the tax bill

- You walk away with real money

At a pre-IPO startup (double-trigger):

- Year one: You have 1,000 time-vested RSUs

- You receive zero shares

- You owe zero taxes

- You wait for the IPO

The double-trigger structure means everything happens at once when your company finally goes public. That's when things get interesting (and expensive).

Single-Trigger vs. Double-Trigger RSUs: A Critical Guide for Startup Employees | The Breakdown Lane

What Happens When the Second Trigger Finally Hits

Think of your pre-IPO RSUs like water building up behind a dam. You've been earning shares for years, but they've just been sitting there. When your company goes public, the dam breaks. All your time-vested RSUs flood in at once.

Here's exactly what happens on IPO day.

The Settlement Timeline

Your RSUs settle on the IPO date or within a few days after. Settlement means the shares become real stock in your brokerage account. Every RSU that's met the time requirement (usually 25% per year over four years) settles all at the same time.

This is different from your future RSUs. Those will keep vesting quarterly like normal. But everything you've earned up until IPO day hits at once.

The Tax Withholding Process

The moment your RSUs settle, they become taxable income. The company values them at the IPO price, and that full amount goes on your W-2 as ordinary income (just like your salary).

Your company automatically withholds shares to cover taxes. They don't ask for cash. Instead, they keep some of your shares and send the rest to you.

Here's a real example:

Devon has been at her pre-IPO company for three years. She's earned 12,000 RSUs total (all time-vested). Her company goes public at $25 per share.

- Gross value: 12,000 shares × $25 = $300,000

- Tax withholding: Company keeps 3,600 shares (30% for federal and state taxes)

- Net shares Devon receives: 8,400 shares in her brokerage account

- W-2 income added: $300,000

Devon's W-2 at year-end will show her regular salary plus $300,000 from the RSUs. If she's in a higher tax bracket, the 30% withholding might not be enough. She could owe more when she files taxes.

What Shows Up in Your Brokerage Account

A few days after the IPO, you'll see your net shares appear in a brokerage account. Most companies use E*TRADE, Fidelity, Morgan Stanley, or Schwab.

You own these shares. They're real stock. But there's a catch.

The Lockup Period

You typically can't sell for 180 days (six months) after the IPO. This is called a lockup period. It prevents employees from flooding the market with shares right after the company goes public.

Your shares are locked, but they're still yours. The stock price will go up and down during this time. You just have to watch and wait.

The lockup period ends on a specific date (your company will announce it). After that, you can sell whenever you want.

Why This Creates Tax Surprises

The big shock comes at tax time. Many people don't realize that the 30% withholding is just an estimate. If you're in the 35% or 37% tax bracket, you'll owe more. Plus, some states (like California at 13.3%) have higher rates than the standard withholding covers.

You got taxed on $300,000, but you can't sell shares to pay the extra taxes until the lockup ends. This is why tax planning before the IPO matters so much.

Next, we'll break down exactly how to plan for this tax bill before it hits.

The Tax Bill Nobody Warns You About: Planning for Double-Trigger RSU Taxation

Here's the shock that hits employees six months after their company goes public: a massive tax bill they can't pay.

Your company withheld taxes when your RSUs vested at IPO. You thought you were covered. Then April comes, and your CPA says you owe another $60,000. Or $100,000. Sometimes more.

Why does this happen? Think of tax withholding like a down payment on a house. It's just the minimum required upfront, not the full price.

The Withholding Gap That Catches Everyone

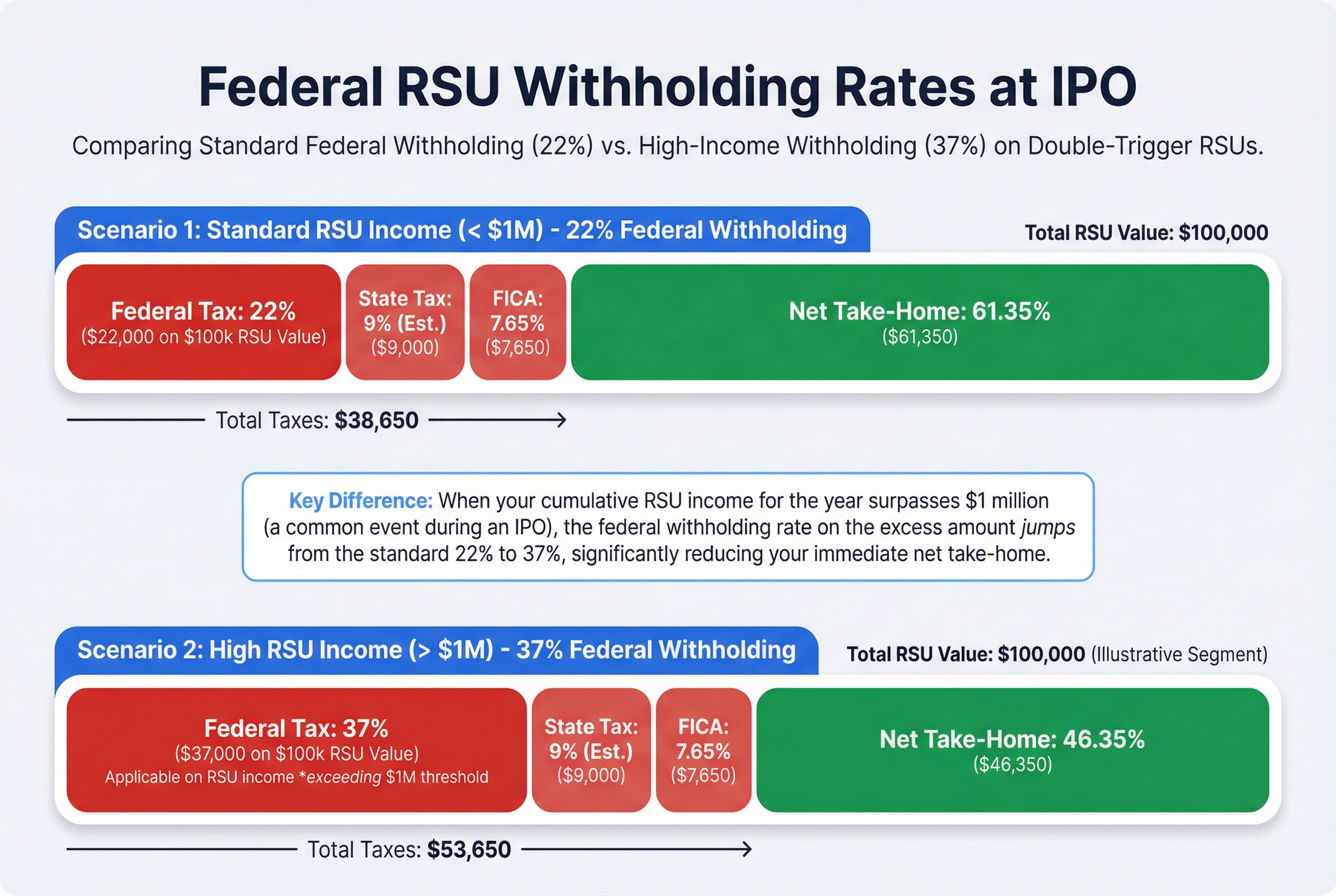

When your double-trigger RSUs vest at IPO, your company withholds taxes automatically. The standard federal withholding is 22%. If your RSU income exceeds $1 million, withholding jumps to 37%.

But here's the problem: withholding rates and actual tax rates are different things.

Your actual tax rate depends on your total income for the year. When you add RSU income to your salary and other earnings, you might land in the 35% or 37% federal tax bracket. Then add state taxes (0% to 13% depending where you live). Your real tax rate could hit 40%, 45%, even 50% in high-tax states.

The math gets brutal fast.

Real Numbers: How Bad Can It Get?

Let's look at Alex, a senior engineer whose double-trigger RSUs vest at IPO.

Alex's situation:

- RSU income at IPO: $400,000 (2,000 shares at $200 each)

- Company withholds: 30% = $120,000 in shares sold automatically

- Alex's salary: $200,000

- Total income for the year: $600,000

The tax reality:

- Federal tax rate at $600k income: 35%

- California state tax: 9.3%

- Combined rate: 44.3%

- Total tax owed on RSUs: $177,200

- Amount already withheld: $120,000

- Alex owes at tax time: $57,200

Alex needs to come up with $57,200 in cash. And here's the cruel twist: if there's a 180-day lockup period after the IPO, Alex can't sell shares to cover this gap. The money needs to come from savings or salary.

Why Your Tax Bracket Matters More Than You Think

RSU income gets added to your regular salary. This creates an income spike that can push you into a higher tax bracket just for that year.

Example brackets (2024):

- 32% bracket: Starts at $191,950 for single filers

- 35% bracket: Starts at $243,725

- 37% bracket: Starts at $609,350

If you normally earn $150,000, you're in the 24% bracket. But add $500,000 in RSU income? You're suddenly in the 35% or 37% bracket for that extra income.

The withholding your company does assumes a flat rate. It doesn't account for bracket creep.

How to Prepare (Starting Right Now)

Start saving 1-2 years before your expected IPO. Treat this like saving for a down payment on a house.

Here's your action plan:

Calculate your potential tax gap:

- Estimate how many RSUs will vest (check your grant documents)

- Guess at a share price (use recent 409A valuation as a baseline)

- Multiply shares × price = RSU income

- Calculate 45% of that number (conservative estimate for federal + state)

- Subtract the amount your company will withhold (usually 22-30%)

- The remainder is your gap

Build your cash reserve:

- Set aside money each month in a high-yield savings account

- Don't invest this money (you need it to be there, not subject to market swings)

- Aim to save your estimated tax gap plus 20% buffer

Make estimated tax payments:

In the year of your IPO, you might need to make quarterly estimated tax payments to avoid penalties. If you owe more than $1,000 beyond withholding, the IRS expects you to pay throughout the year, not just in April.

Talk to a CPA in Q3 or Q4 of your IPO year. They can calculate what you owe and help you make estimated payments before January.

Consider selling at vest:

Some employees choose to sell enough shares immediately at vest to cover the full tax bill. Yes, you'll miss out if the stock goes up. But you'll also avoid scrambling for cash or going into debt.

This is especially smart if there's a lockup period. You can't predict what the stock price will be when lockup expires.

Get Professional Help (Not Optional)

Work with a CPA who specializes in equity compensation. Your regular tax preparer might not understand the nuances of RSU taxation, lockup periods, or estimated payments.

A specialist can:

- Calculate your exact tax liability before filing

- Set up estimated payment schedules

- Model different scenarios (sell at vest vs. hold)

- Help you avoid penalties

Budget $1,000 to $3,000 for tax prep in your IPO year. It's worth every penny when you're dealing with six-figure tax bills.

The Lockup Period Makes Everything Harder

Here's the timing trap: you owe taxes in April for RSUs that vested in June of the previous year. But if there's a 180-day lockup, you might not be able to sell shares until December.

You need cash before you can access your shares.

This is why saving ahead matters so much. You can't count on selling shares to cover your tax bill if those shares are locked up.

Some employees take out short-term loans or use credit cards to bridge the gap. This is expensive and risky. Much better to have cash ready.

Federal withholding rates applied automatically upon RSU settlement at IPO.

Federal withholding rates applied automatically upon RSU settlement at IPO.

The tax surprise is the most painful part of double-trigger RSUs for most employees. But it's also the most preventable. Start planning now, save aggressively, and work with a professional. Your future self will thank you.

Next, let's talk about what happens if you leave your company before the IPO. Spoiler: it's not good news.

What Happens If You Leave Before the IPO (The 'Must Be Present to Win' Clause)

Here's the harsh truth that catches most employees by surprise: if you leave your pre-IPO company before the IPO happens, you typically lose all your RSUs. Even the ones that already vested on your time schedule.

Think of it like a raffle where you must be physically present to claim your prize. You bought tickets four years ago. Your numbers got drawn. But if you're not in the room when they call your name, you get nothing. Someone else doesn't win your prize. It just disappears.

This is called a "continuous service requirement," and it's buried in almost every pre-IPO RSU grant agreement.

The Fine Print That Changes Everything

Most double-trigger RSU grants include language like "you must be employed on the settlement date" or "continuous service through liquidity event required." This means both triggers apply:

- First trigger: You stay for your vesting schedule (say, 4 years)

- Second trigger: You're still employed when the IPO happens

If you leave between these two events, you forfeit everything. This is completely legal and standard practice. But companies rarely explain it clearly during hiring.

Real Money at Stake

Jordan's story: She joined a startup in 2019 with 8,000 RSUs vesting over 4 years. By 2023, all 8,000 had time-vested. Then she got her dream job offer. She checked her grant agreement and saw the dreaded phrase: "must be employed on settlement date."

Jordan left anyway. Eight months later, her old company went public at $35 per share. She lost $280,000 (8,000 shares × $35).

Maya's story: Maya had identical terms, except her grant said "RSUs remain eligible if employee completes 4 years of service." After her 4-year anniversary, she left. When the IPO happened 6 months later, she received all 8,000 shares.

The difference? One sentence in their grant agreements.

Check Your Grant Right Now

Pull out your RSU grant agreement and search for these phrases:

- "Continuous service"

- "Employed on settlement date"

- "Termination of employment"

- "Forfeiture upon separation"

If you see this language, you have golden handcuffs. Leaving before the IPO means losing everything, regardless of how long you've worked there.

Are There Exceptions?

Sometimes, but rarely:

Termination without cause: Some grants protect you if the company fires you without cause. Your RSUs might survive until the IPO. Read your grant carefully.

Negotiated severance: Senior executives sometimes negotiate partial RSU acceleration in severance packages. This is uncommon for individual contributors and rare even for managers.

Flexible vesting terms: A tiny number of companies (like Maya's) use "service-based" rather than "employment-based" requirements. You can leave after completing your service period and keep your RSUs.

Don't assume you have these protections. Most employees don't.

The Golden Handcuffs Effect

This is why pre-IPO employees feel trapped. You might hate your job, have a better offer elsewhere, or need to relocate for family. But leaving could mean forfeiting hundreds of thousands of dollars.

The closer you get to an IPO, the tighter these handcuffs feel. Leaving 6 months before a $40 IPO when you have 10,000 vested RSUs means walking away from $400,000.

Companies know this. It's part of why they structure RSUs this way.

What to Do With This Information

First, find your grant agreement and read the termination provisions. Know exactly what you're giving up if you leave.

Second, factor this into any job decision. That competing offer might pay $20k more in salary, but you could be leaving $300k on the table.

Third, if you're seriously considering leaving, talk to a lawyer about your specific grant terms. Sometimes the language is ambiguous enough to negotiate.

But in most cases, the rule is simple: leave before the IPO, lose your RSUs. Period.

Now, what if your company offers you a way to get cash before the IPO? That's where tender offers and early liquidity programs come in.

When Companies Waive the Second Trigger: Tender Offers and Early Liquidity

Some pre-IPO companies crack open a small exit door before the main doors swing wide. They do this through tender offers or secondary sales.

Think of it like a concert venue letting a few people leave early through a side exit. Everyone else still waits for the main doors to open after the show ends.

What Is a Tender Offer?

A tender offer lets you sell some of your RSUs before the IPO happens. The company or outside investors buy your shares at a set price. This is a partial waiver of the second trigger, but only for employees who choose to participate.

Companies like Stripe, Databricks, and SpaceX have run tender offers. They let employees get cash without waiting years for an IPO.

The Tax Trap You Need to Know About

Here's the critical part: selling in a tender offer creates immediate taxable income. You lose the double-trigger protection.

Example: Priya's Tender Offer

Priya has 10,000 time-vested RSUs at a company valued at $50 per share. The company announces a tender offer where she can sell 20% of her holdings.

She sells 2,000 RSUs for $100,000. This creates $100,000 of ordinary income on her tax return. She owes roughly $35,000 in taxes (federal plus state). She nets $65,000 cash but faces a $35,000 tax bill due in April.

Her remaining 8,000 RSUs still wait for the IPO.

Key Points About Tender Offers

Participating in a tender offer is completely optional. You can decline and wait for the IPO. Here's what matters:

- Only a portion of your RSUs are typically eligible (often 10% to 20%)

- You owe taxes immediately, just like the IPO happened

- You need cash on hand to pay the tax bill

- The shares aren't publicly traded, so you can't sell more to cover taxes

When This Makes Sense (And When It Doesn't)

Tender offers work well if you need cash now or want to reduce your concentration risk. Maybe you want a down payment for a house. Maybe you're nervous about keeping all your eggs in one basket.

They're terrible if you can't afford the tax bill. Getting $65,000 cash but owing $35,000 in taxes only works if you have that $35,000 available.

Now let's look at what happens when your company gets acquired instead of going public.

Double Trigger RSUs: How They’re Treated in an IPO

Acquisition vs. IPO: How the Second Trigger Works Differently

Think of your double-trigger RSUs like a race with two possible finish lines. An IPO is one finish line. An acquisition is the other. Both count as winning, but the prize you get looks different.

Acquisitions Usually Trigger Settlement

When another company buys your employer, that typically satisfies the second trigger. Your RSUs are now worth something because there's a liquidity event. But what you actually receive depends on how the deal is structured.

The two main types of acquisitions:

- Cash acquisition: The buyer pays cash for your company

- Stock acquisition: The buyer pays with their own stock

Let's look at both scenarios with real numbers.

Cash Acquisitions: Immediate Money, Immediate Taxes

Example: Lisa works at Company B, which gets acquired by a private equity firm for cash. She has 6,000 time-vested RSUs. The acquisition values each RSU at $40.

Here's what happens:

- Lisa's RSUs convert to $240,000 cash (6,000 × $40)

- She gets paid within 30 days

- The full $240,000 is taxed as ordinary income (same as salary)

- No lockup period, she has immediate liquidity

- She owes taxes by April 15th of the following year

This is like getting a massive bonus check. You have the cash right away, but you'll owe a big tax bill.

Stock Acquisitions: New Company, New Waiting Period

Example: Jamal works at Company A, which Google acquires for stock. He also has 6,000 time-vested RSUs worth $240,000 in the deal.

Here's what happens:

- Jamal's RSUs convert to Google stock worth $240,000

- The $240,000 is still taxed as ordinary income (even though he gets stock, not cash)

- Google might require him to vest the new shares over 1-2 years

- He can't sell during this new vesting period

- He needs cash to pay taxes but doesn't have liquidity yet

This is trickier. You owe taxes on money you can't access yet. Many employees are surprised by this.

Acceleration vs. Settlement: Know the Difference

Some acquisitions include accelerated vesting. This means all your unvested RSUs vest immediately when the deal closes. You get everything at once.

Other acquisitions only trigger settlement of already-vested RSUs. Your unvested RSUs might get cancelled or convert to the buyer's unvested RSUs. You don't get them all immediately.

Check your grant agreement for "change of control" provisions. This legal language explains what happens to your specific RSUs in an acquisition. Some grants say "100% acceleration upon change of control." Others don't.

The Acquisition Price Matters More Than You Think

Here's the hard truth: you might receive less than you hoped.

If your company's last valuation was $50 per share but the acquisition happens at $35 per share, your RSUs are worth $35 each. Not $50. The acquisition price is the only price that matters.

This is different from an IPO, where the public market determines the price and it can go up over time. In an acquisition, the price is locked in by the deal terms.

What About Lockups and Earn-Outs?

Cash deals: Usually no lockup. You get paid and you're done.

Stock deals: The acquiring company might restrict when you can sell. Common lockup periods are 6-12 months.

Earn-outs: Some acquisitions include earn-out provisions. You only get the full value if the business hits certain targets post-acquisition. This is less common but worth checking.

You Have Less Control in Acquisitions

Unlike an IPO where you can watch the market and plan your sale, acquisitions happen behind closed doors. You often learn about them only weeks before they close.

The acquiring company sets the terms. Your employer negotiates, but individual employees rarely have input. This is why understanding your grant agreement now matters. It's the only protection you have.

Now that you understand how your RSUs work in different exit scenarios, let's create a practical checklist of what you should do right now to prepare.

Your Pre-IPO RSU Checklist: What to Do Right Now

Think of preparing for your RSU liquidity event like training for a marathon. You can't just show up on race day and expect to succeed. You need a training plan, the right gear, and months of preparation.

Here's your action plan, broken down by timeline:

Do This Week

1. Find and read your grant agreement. It's probably in your email or your company's equity management portal (like Carta or Shareworks). Look for a PDF titled "Restricted Stock Unit Agreement" or similar.

2. Identify what's already vested. Your agreement shows your vesting schedule. Circle the dates when shares vest. If you started 2 years ago with a 4-year vest, you've already earned 50% of your RSUs on the time side.

3. Look for the trigger language. Search your document for phrases like "continuous service requirement" or "liquidity event." This confirms you have double-trigger RSUs.

4. Calculate your potential tax bill. Use this simple formula: (Number of time-vested RSUs × estimated IPO price) × 0.35 = approximate tax owed. Round up to be safe.

Do This Month

5. Start building your tax savings fund. Target saving 50% of your potential RSU value. If you might owe $85,000 in taxes, aim to save at least $42,500 before IPO.

6. Find a CPA who specializes in equity compensation. Ask coworkers for referrals. Interview 2-3 CPAs. Make sure they've handled RSU taxation at IPO before.

7. Ask HR about your company's IPO timeline. You won't get a firm date, but you might learn "we're targeting next year" versus "maybe in 3-5 years."

Do This Quarter

8. Review your complete financial picture. List all income sources, existing investments, and potential deductions. Your CPA needs this to plan properly.

9. Ask about secondary liquidity options. Some companies offer tender offers where you can sell a portion of shares early. HR or your equity portal will have this info.

10. Set up a brokerage account. You'll need somewhere to hold shares after IPO. Fidelity, Schwab, and E-Trade all work fine. Do this now while there's no pressure.

Real Example: Ryan's 2-Year Action Plan

Ryan works at a pre-IPO company expected to go public in 2 years. Here's his checklist:

Today: Reviews his grant agreement. Discovers he has 8,000 RSUs, with 6,000 already time-vested. Calculates potential value at $30/share ($240,000 gross) and tax bill ($85,000).

This year: Starts saving $3,000/month toward his tax fund. Meets with a CPA in October to create a tax strategy. Opens a brokerage account.

Next year: Continues saving $3,000/month. Checks in with HR quarterly about IPO timeline. Asks about any tender offer opportunities.

IPO year: Makes estimated tax payment in Q2 (after shares vest and sell). Reviews lockup period terms. Works with CPA on final tax filing.

Critical Don'ts

Don't make major life decisions without considering RSU timing. Leaving your job, buying a house, or having a baby all affect your financial picture. If your IPO is 6 months away and you have $200,000 in time-vested RSUs, quitting now costs you real money.

Don't assume the IPO will happen on schedule. Companies delay all the time. Market conditions change. Save as if it might take longer than expected.

Don't try to time the market. You can't predict whether your stock will hit $25 or $35 at IPO. Plan for a conservative estimate and be pleasantly surprised if it's higher.

Your Monthly Check-In

Set a calendar reminder to review this checklist monthly. Ask yourself:

- Am I on track with my tax savings?

- Has anything changed with the IPO timeline?

- Do I need to adjust my financial plans?

The employees who handle their RSU windfall best are the ones who prepare early. Start your checklist today, even if your IPO is years away.

Frequently Asked Questions

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

[ANSWER NEEDED]

Educational Content Only

This content is for educational purposes only and does not constitute financial advice. The information provided is general in nature and may not appl...

YourEmployeeStock.com is not a registered investment advisor.

Related Articles

What Are RSUs? A Complete Guide to Restricted Stock Units

Restricted Stock Units (RSUs) are a type of stock compensation where your company promises to give you shares after you meet certain conditions, usually working there for a set period. Unlike stock options, RSUs always have value as long as the company's stock has value. This guide explains how RSUs work, when you'll owe taxes, and how to make the most of this benefit.

TaxHow RSUs Are Taxed

RSUs are taxed as ordinary income when they vest, but there's more to the story. Learn about withholding, the tax gap, and strategies to manage your RSU tax bill.

BasicsEquity Compensation Basics: A Simple Guide to Understanding Your Stock Benefits

Equity compensation means getting paid partly in company stock instead of just cash. This guide breaks down what equity compensation is, the main types you'll encounter (RSUs, stock options, ESPP), how it affects your total pay, and what you need to know to make smart decisions about your stock benefits.

Not sure what to do with your equity?

Get a free personalized analysis